|

시장보고서

상품코드

2063554

의약품 제조 실행 시스템 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Pharmaceutical Manufacturing Execution System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

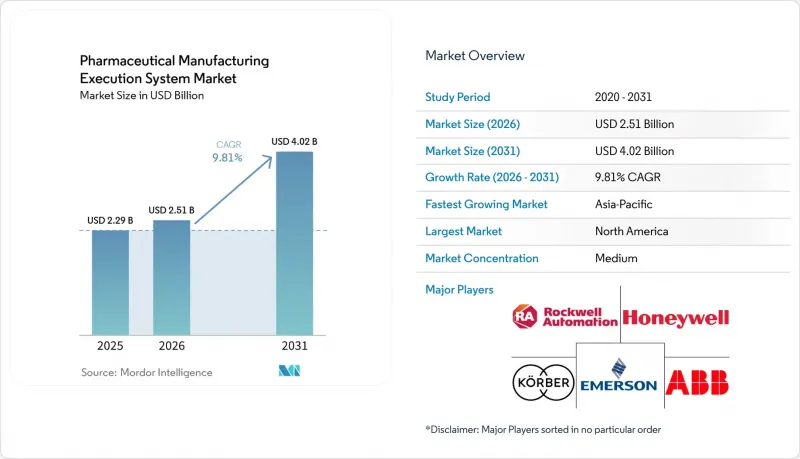

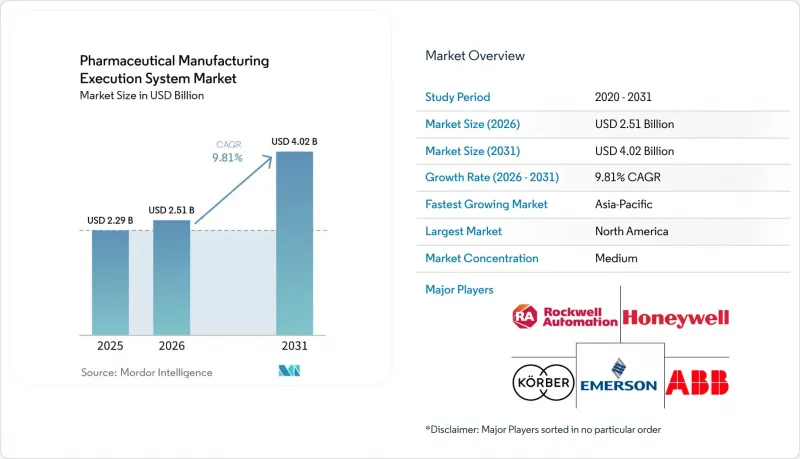

Mordor Intelligence에 의하면, 의약품 제조 실행 시스템(PMES) 시장 규모는 2025년에 22억 9,000만 달러, 2026년에 25억 1,000만 달러, 2031년까지 40억 2,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 9.81%로 성장할 것으로 전망됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(On-Premise 및 클라우드/SaaS), 기능(전자 배치 기록(EBR), 레시피/워크플로우 관리 등), 최종 사용자(제약사, 바이오의약품 제조업체 등) 및 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

전 세계 의약품 제조 실행 시스템(MES) 시장 동향 및 인사이트

규정 준수 및 데이터 무결성 요건이 MES 투자를 가속화

규제 대상 제조업체들은 엄격한 조사에 대응할 수 있는 신뢰성 높은 전자 기록, 전자 서명 및 감사 추적과 관련된 21 CFR Part 11 요건을 준수하기 위해, 검증된 전자 시스템을 강화하고 있습니다. MES 플랫폼은 통제된 워크플로우, 타임스탬프가 포함된 작업, 그리고 변조가 불가능한 감사 로그를 통해 이에 대응함으로써 오류 위험을 줄이고 데이터 무결성을 강화합니다. 시리얼화 및 상호 운용 가능한 추적성을 통해 제품 수명 주기 전반에 걸쳐 단위 수준, 로트 수준, 출하 수준의 가시성을 확보하기 위해 MES와 엔터프라이즈 리포지토리 간의 통합이 더욱 진전되고 있습니다. 제조업체들은 종이 또는 하이브리드 형식의 기록을 디지털화된 배치 실행 및 예외 대응형 검토로 대체함으로써 사이클 타임을 단축하고, 실질적인 편차 정보, 서명, 증거의 무결성을 통해 출하 준비 태세를 강화하고 있습니다. 이러한 규정 준수 중심의 변화는 검증된 템플릿, 안전한 개발 라이프사이클, 그리고 입증된 감사 대응 능력을 우선시하는 프로젝트 범위 설정 및 공급업체 평가에서도 드러나고 있습니다. 따라서 의약품 제조 실행 시스템 시장은 ALCOA를 완벽하게 준수하는 데이터 무결성을 입증할 수 있고, 감사 및 검사를 위한 증거 생성을 효율화할 수 있는 플랫폼으로 점차 전환되고 있습니다.

Pharma 4.0: 디지털화의 기세가 비즈니스 모델을 재구축하고 있습니다.

업무의 디지털화는 검증된 상태를 유지하면서, 검증 및 변경 관리에 민첩성을 부여하는 클라우드 지원, 컨테이너화, 그리고 로우코드 지원 아키텍처로 발전하고 있습니다. 현장 실행, 품질 관리 및 분석을 통합하는 MES 플랫폼은 운영자, 감독자, 품질 보증(QA) 담당자가 운영 현황을 공통적으로 파악할 수 있도록 하여, 실시간 의사 결정과 배치 처리의 최적화를 지원합니다. 지속적 개선 프로그램 또한 표준화된 마스터 레시피와 전자 작업 지시서를 활용하여 편차를 제거하고 대기 시간을 단축하고 있으며, 이는 실시간 출하를 위한 노력과 일치합니다. 로우코드 도구가 MES 생태계에 통합됨에 따라, 공정 엔지니어는 복잡한 맞춤형 코드 없이도 워크플로우와 양식을 신속하게 반복 개선할 수 있게 되어, 위험 기반 접근 방식에 따른 설계 및 검증 주기를 단축할 수 있습니다. 그 결과, 의약품 제조 실행 시스템 시장은 실행, 품질, 일련번호 부여, 분석을 통합하고, 단일 라인에서 여러 공장으로 구성된 네트워크에 이르기까지 확장 가능한 유연한 도입 옵션을 제공함으로써, Pharma 4.0의 원칙에 부합하는 형태로 진화하고 있습니다.

높은 도입 비용과 프로그램의 복잡성 때문에 중견 기업에서의 도입이 지연되고 있습니다.

MES는 단순한 소프트웨어 설치가 아닌 변혁 프로그램이기 때문에 소규모 조직의 경우 IT 및 QA 팀에게 있어 프로그램의 복잡성은 여전히 장벽으로 작용하고 있습니다. 클라우드 네이티브 및 관리형 서비스 모델은 인프라 소유에 따른 부담을 줄이고, 적합성 평가를 효율화하며, 안전한 개발 및 릴리스 관행을 실천하는 벤더에게 검증 문서 작성의 부담을 전가할 수 있기 때문에 지지를 얻고 있습니다. 또한, 제조 팀이 사용자 정의 코드를 최소화하면서 검증된 워크플로우와 양식을 보다 신속하게 설정할 수 있도록 지원함으로써 가치 창출을 가속화하는 로우코드 툴킷도 등장하고 있습니다. 일부 공급업체는 현재 사전 검증된 컨텐츠, 컨설팅 시간, 업계 템플릿을 패키지로 묶어, 신생 제약 및 바이오기술 기업 팀의 검증 업무 부담을 덜어주고 있습니다. 이러한 진전이 있음에도 불구하고, 많은 중견 기업의 구매 담당자들은 변경 관리 역량이나 현장의 준비 상황에 맞추어 도입 속도를 조정하고 있어, 기술적 진전이 있음에도 불구하고 전체 일정이 장기화될 가능성이 있습니다. 의약품 제조 실행 시스템(PMES) 시장에서는 단계적인 로드맵, 클라우드 호스팅 방식의 시범 도입, 그리고 별도의 수정 없이 공장 간에 복제 가능한 사전 구축된 컨텐츠를 제공함으로써 이러한 제약 사항에 지속적으로 대응하고 있습니다.

부문별 분석

2025년 기준으로 소프트웨어는 의약품 제조 실행 시스템 시장의 56.64%를 차지하고 있으며, 서비스 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 10.23%로 확대될 것으로 전망됩니다. 이는 전문가 주도의 도입, 검증 및 라이프사이클 지원에 대한 수요가 증가하고 있음을 반영한 것입니다. 구매 기업들은 검증된 EBR(전자 배치 기록), 편차 관리, 일련번호 통합 기능에 더해, 안전한 개발 기법과 견고한 감사 추적을 갖춘 공급업체를 계속해서 우선적으로 선택하고 있습니다. 조직이 여러 거점으로 도입을 확대함에 따라, 품질 시스템에 부합하는 버전 관리, 회귀 테스트, 릴리스 노트를 관리하기 위한 지속적인 서비스도 필요해집니다. 따라서 의약품 제조 실행 시스템 시장에서는 업그레이드 후에도 검증 상태를 유지하기 위해 교육, 관리형 검증, 연중무휴 24시간 지원의 도입률이 확대되고 있습니다. 인력 측면에서는 벤더와 시스템 통합사업자가 인증 교육 과정을 통해 기술 격차 해소를 지원하고 있으며, 이를 통해 운영 담당자, 품질 보증(QA) 담당자, IT 관리자가 규정 준수 요건을 충족하는 운영을 유지할 수 있게 되었습니다. 이러한 서비스 중심 모델은 클라우드 MES를 통해 더욱 강화되고 있습니다. 클라우드 MES에서는 제공업체가 인프라의 적합성을 확인하고, 사전 검증된 컨텐츠를 제공함으로써 도입 시나 정기적인 업데이트 시 고객의 부담을 줄여줍니다.

서비스의 성장은 기존 환경(브라운필드)에서 MES를 자동화 시스템, 품질 관리 시스템 및 엔터프라이즈 시스템과 통합하는 데 따르는 복잡성도 반영하고 있습니다. 업계 팀들은 규정 준수를 저해하지 않으면서 프로젝트 기간을 단축하기 위해, 미리 구축된 커넥터, 검증 템플릿 및 레시피 가속기를 제공하는 파트너를 점점 더 선호하고 있습니다. 의약품 제조 실행 시스템 업계에서는 변경 관리 하에서 양식 및 워크플로우 설정을 신속하게 진행하기 위해 로우코드 도구를 도입하고 있으며, 그 결과 거버넌스 및 라이프사이클 관리 서비스에 대한 수요가 증가하고 있습니다. 또한, 각 벤더사는 위험 기반의 보증 활동 및 현장의 준비 상황에 맞추어 범위를 조정하기 위해, 신규 라이선스나 서비스형(as-a-service) 제공에 컨설팅 시간을 포함시키고 있습니다. 이러한 서비스 주도형 가치 제공으로의 전환에 따라, 대형 제약사, 바이오기술 기업, CDMO(수탁 제조·개발 기업) 전반에 걸쳐 디지털 성숙도가 향상됨에 따라, 의약품 제조 실행 시스템 시장은 지속적인 서비스 확장의 기반을 마련하고 있습니다.

2025년에는 On-Premise 도입이 55.81%를 차지했으나, 구매자들이 데이터 주권과 민첩성, 가치 실현 속도의 균형을 모색함에 따라 2026년부터 2031년까지 클라우드/SaaS가 연평균 성장률(CAGR) 13.65%로 가장 빠르게 성장할 것으로 예측됩니다. 클라우드 네이티브 MES 및 서비스형 모델은 인프라 소유 부담을 줄이고 전 세계적인 확장을 가속화할 뿐만 아니라, 벤더가 관리하는 자동 테스트 패키지를 통해 업그레이드의 표준화를 실현하고 있습니다. 컨테이너화된 플랫폼은 생산 실행을 라인 근처에서 유지하면서 분석 및 보고 기능을 탄력적인 클라우드 컴퓨팅으로 이전하는 하이브리드 토폴로지를 가능하게 하여 유연성을 높여줍니다. 최신 스위트에 탑재된 로우코드 기능을 통해 프로세스 담당 팀은 복잡한 맞춤형 코드를 작성하지 않고도 양식과 워크플로를 설정할 수 있으므로, 설계 주기가 단축되고 IT 업무 적체가 줄어듭니다. 또한, 각 인터넷 서비스 제공업체들은 안전한 개발 기법, 강화된 지침, 그리고 검증된 운영에 대한 고객의 품질 기대에 부응하는 문서 패키지를 통해 사이버 보안 대책을 강화하고 있습니다.

현재 하이브리드 모델은 팀이 기존 플랜트를 현대화하는 동시에, 규제 대상 공정의 가동 시간과 확실한 제어를 유지하기 위한 현실적인 가교 역할을 하고 있습니다. CDMO가 지역을 넘어 포트폴리오를 확장해 나가는 가운데, 표준화된 마스터 레시피, 고객별 맞춤형 품질 워크플로우, 그리고 통합된 거버넌스를 통해 신속한 온보딩을 실현하는 멀티테넌트 SaaS가 주목받고 있습니다. 시리얼화 클라우드 오케스트레이션은 포장 이벤트, 시운전, 출하 메시지를 배치 컨텍스트와 연계하고, 다운스트림 공정에서의 조회에 대응함으로써 분산형 공급망 네트워크를 더욱 지원합니다. 따라서 의약품 제조 실행 시스템(PMES) 시장은 도입의 유연성을 중심으로 통합되는 추세입니다. On-Premise, 프라이빗 클라우드, 퍼블릭 클라우드 옵션을 조합하여 제어성, 확장성, 규정 준수 간의 균형을 맞출 수 있습니다. 사전 검증된 컨텐츠, 관리형 업데이트 및 ‘보안 설계(Secure by Design)’ 스택을 제공하는 공급업체는 감사 대응 능력을 저해하지 않으면서 총 소유 비용(TCO)을 간소화하고자 하는 구매자들에게 앞으로도 계속해서 두각을 나타낼 것입니다.

지역별 분석

2025년 북미는 성숙한 규제 체계와 바이오기술 클러스터 전반에 걸친 혁신 기업들의 견고한 기반을 바탕으로 의약품 제조 실행 시스템(MES) 시장 점유율의 37.23%를 차지했습니다. 2026년 구매 담당자들의 최우선 과제는 검증된 상태를 유지하면서 여러 공장에 걸친 변경 속도를 높일 수 있는 클라우드 기반 MES 도입에 집중하고 있습니다. 대형 제약사와 주요 CDMO는 기존 사이트의 개량을 지속하며, EBR의 표준화, 일련번호 관리의 통합, 그리고 다양한 제품 포트폴리오 전반에 걸친 예외 기반 검토를 실현하고 있습니다. 또한, 이 지역에서는 일정 관리, 배치 실행, 품질 관리(QC) 기록을 규정 준수 기준에 부합하는 형태로 통합하는 폐쇄형 시스템의 세포 치료 플랫폼 및 오케스트레이션 도구에 대한 투자도 이루어지고 있습니다. 이러한 기반을 통해 기업들이 멀티사이트 템플릿을 확대하고, 데이터 무결성을 강화하며, 공급망의 회복탄력성을 구축함에 따라 의약품 제조 실행 시스템 시장의 지속적인 성장이 뒷받침되고 있습니다.

아시아태평양은 바이오의약품 생산 능력 확대와 CDMO 서비스의 규모 확대에 힘입어, 2026년부터 2031년까지 의약품 제조 실행 시스템(MES) 시장 규모가 연평균 성장률(CAGR) 15.83%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 지역입니다. 제조업체들이 새로운 생산 라인이나 시설을 증설함에 따라, 표준화된 EBR, 검증 완료된 클라우드 옵션, 그리고 인증 소요 시간을 단축해 주는 공급업체 관리형 업그레이드에 대한 수요가 증가하고 있습니다. 각 지역의 CDMO는 스폰서를 신속하게 온보딩하고, 다중 고객 포트폴리오 전반에 걸쳐 일관된 품질 관리 관행을 유지하기 위해 모듈식 MES 컨텐츠를 도입하고 있습니다. 또한, 공급업체는 사용자 정의 코드를 최소화하고 유효성 검증을 간소화하기 위해 구형 기기 및 포인트 시스템용 커넥터 전략에 대해 고객과 협력하고 있습니다. 이러한 우선순위에 따라, 의약품 제조 실행 시스템 시장은 APAC 지역의 확대되는 제조 거점 전반에 걸쳐 상호 운용성, 클라우드 확장성 및 ‘보안 설계(Secure by Design)’ 운영에 지속적으로 초점을 맞추었습니다.

유럽에서는 표준화된 데이터 거버넌스, 사이버 보안에 대한 기대감의 고조, 그리고 검증된 디지털 시스템을 중시하는 품질 설계(QbD) 접근 방식을 통해 시장이 지속적으로 진화하고 있습니다. EU 전역에서 일련번호 부여, 추적 및 추적 가능성, 그리고 현장 수준의 적합성 평가에 대한 조화가 진행됨에 따라, MES, ERP 및 엔터프라이즈 리포지토리 간의 연계가 더욱 긴밀해지고 있습니다. 또한, 유럽의 의약품 제조 실행 시스템 시장에서는 분석 기능과 마스터 데이터를 통합하면서도 현지에서의 제어 기능을 유지하는 클라우드 및 하이브리드 방식의 도입이 중요시되고 있습니다. 벤더들이 로우코드 기능과 사전 검증된 컨텐츠를 강화함에 따라, 유럽의 제조업체들은 특히 바이오의약품 클러스터에서 검증의 엄격성을 저해하지 않으면서 업그레이드를 가속화하고 있습니다. 기업들이 업무의 현대화, 시리얼화 대상 범위의 확대, 그리고 다중 거점용 템플릿 확장을 추진함에 따라, 이러한 동향은 의약품 제조 실행 시스템 시장의 꾸준한 수요를 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the pharmaceutical manufacturing execution system market size is projected to be USD 2.29 billion in 2025, USD 2.51 billion in 2026, and reach USD 4.02 billion by 2031, growing at a CAGR of 9.81% from 2026 to 2031.

This report is Segmented by Component (Software and Services), Deployment (On-Premise, and Cloud / SaaS), Functionality (Electronic Batch Records (EBR), Recipe/Workflow Management, and More), End User (Pharmaceutical Manufacturers, Biopharmaceutical Manufacturers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasted in Terms of Value (USD).

Global Pharmaceutical Manufacturing Execution System Market Trends and Insights

Regulatory Compliance and Data Integrity Requirements Accelerate MES Investment

Regulated manufacturers are reinforcing validated electronic systems to align with 21 CFR Part 11 requirements for trustworthy electronic records, e-signatures, and audit trails that can support rigorous investigations. MES platforms address this with controlled workflows, time-stamped actions, and immutable audit logs that reduce error risk and strengthen data integrity. Serialization and interoperable traceability are pushing deeper integration between MES and enterprise repositories to ensure unit-level, lot-level, and shipment-level visibility across the full product lifecycle. As manufacturers replace paper and hybrid records with digitized batch execution and review-by-exception, they compress cycle times and enhance release readiness with actionable deviations, signatures, and evidentiary completeness. This compliance-driven shift is visible in project scoping and vendor assessments that prioritize validated templates, secure development lifecycles, and proven audit-readiness. The pharmaceutical manufacturing execution system market is therefore tilting toward platforms that can demonstrate full ALCOA-aligned data integrity and streamlined evidence generation for audits and inspections.

Pharma 4.0 Digitalization Momentum Reshapes Operational Models

Digitalization in operations is advancing toward cloud-ready, containerized, and low-code-enabled architectures that bring agility to validation and change control while preserving the validated state. MES platforms that unify shop-floor execution with quality and analytics create a common operating picture for operators, supervisors, and QA, which supports real-time decision-making and better batch disposition. Continuous improvement programs are also leaning on standardized master recipes and electronic work instructions to eliminate variability and reduce hold times, which is consistent with ambitions for real-time release. As low-code tools become embedded in MES ecosystems, process engineers can iterate workflows and forms faster without heavy custom code, which shortens design-validation cycles under risk-based approaches. The net effect is that the pharmaceutical manufacturing execution system market is aligning with Pharma 4.0 principles by converging execution, quality, serialization, and analytics with flexible deployment choices that scale from a single line to multi-plant networks.

High Implementation Cost and Program Complexity Delay Mid-Market Adoption

Program complexity remains a barrier for organizations with lean IT and QA teams because MES is a transformation program rather than a simple software install. Cloud-native and managed service models are gaining favor because they reduce infrastructure ownership, streamline qualification, and shift more validation documentation to vendors that operate secure development and release practices. Low-code toolkits are also emerging to accelerate value by letting manufacturing teams configure validated workflows and forms faster with less custom code. Some vendors now package pre-validated content, consultancy hours, and industry templates to cut validation effort for emerging pharma and biotech teams. Even with these advances, many mid-market buyers pace deployments to align with change control capacity and site readiness, which can lengthen overall timelines despite technology gains. The pharmaceutical manufacturing execution system market continues to address this restraint with phased roadmaps, cloud-hosted pilots, and pre-built content that can be replicated across plants without rework.

Other drivers and restraints analyzed in the detailed report include:

- Need for Real-Time Visibility Drives Review-by-Exception Adoption

- Growth in Biologics, Cell and Gene Therapies Demands Specialized Execution Infrastructure

- Integration with Legacy Systems Fragments Digital Continuity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 56.64% of the pharmaceutical manufacturing execution system market share in 2025, and Services is projected to expand at 10.23% CAGR over 2026-2031, reflecting rising demand for expert-led deployment, validation, and lifecycle support. Buyers continue to prioritize vendors with proven EBR, deviation management, and serialization integration, along with secure development practices and robust audit trails. As organizations expand multi-site deployments, they also require sustained services to manage versions, regression testing, and release notes in line with quality systems. The pharmaceutical manufacturing execution system market is therefore seeing broader attach rates for training, managed validation, and 24x7 support to maintain a validated state across upgrades. On the workforce side, vendors and integrators are helping close skills gaps with certified curricula so operators, QA, and IT administrators can sustain compliant operations. This services-centric model is reinforced by cloud MES, where providers qualify infrastructure and deliver pre-validated content that reduces customer burden during deployments and routine updates.

Services growth also reflects the complexity of integrating MES with automation, quality, and enterprise systems in brownfield environments. Industry teams increasingly favor partners that bring pre-built connectors, validation templates, and recipe accelerators to shrink project timelines without sacrificing compliance. The pharmaceutical manufacturing execution system industry is adopting low-code tools to speed configuration of forms and workflows under change control, which in turn elevates demand for governance and lifecycle management services. Vendors are also bundling consultancy hours with new licenses and as-a-service offerings to align scope with risk-based assurance activities and site readiness. This migration toward service-led value delivery positions the pharmaceutical manufacturing execution system market for sustained services expansion as digital maturity advances across large pharma, biotech, and CDMOs.

On-premise deployments held 55.81% in 2025, while Cloud/SaaS is projected to be the fastest-growing path at 13.65% CAGR over 2026-2031 as buyers balance data sovereignty with agility and speed to value. Cloud-native MES and as-a-service models are reducing infrastructure ownership, enabling faster global rollouts, and standardizing upgrades with automated testing packages managed by the vendor. Containerized platforms add flexibility by allowing hybrid topologies that keep production execution close to the line while moving analytics and reporting to elastic cloud compute. Low-code capabilities in modern suites help process teams configure forms and workflows without heavy custom code, which compresses design cycles and reduces IT backlog. Providers are also strengthening cybersecurity controls with secure development practices, hardening guidance, and documentation packs that align with customer quality expectations for validated operations.

Hybrid models now serve as a pragmatic bridge as teams modernize brownfield plants while maintaining uptime and deterministic control for regulated steps. As CDMOs scale portfolios across regions, multi-tenant SaaS becomes attractive for standardized master recipes, client-specific quality workflows, and faster onboarding with centralized governance. Cloud orchestration of serialization further supports distributed supply networks by linking packaging events, commissioning, and shipment messages with batch context for downstream queries. The pharmaceutical manufacturing execution system market is therefore converging on deployment flexibility, where on-premise, private cloud, and public cloud options can be mixed to balance control, scalability, and compliance. Providers that deliver pre-validated content, managed updates, and secure-by-design stacks will continue to stand out as buyers look to simplify total cost of ownership without compromising audit-readiness.

Geography Analysis

North America held 37.23% of the pharmaceutical manufacturing execution system market share in 2025, anchored by mature regulatory frameworks and a deep base of innovators across biotech clusters. Buyer priorities in 2026 center on cloud-enabled MES deployments that preserve validated state while improving speed of change across multiple plants. Large pharma and leading CDMOs continue retrofits at legacy sites to standardize EBR, integrate serialization, and enable review-by-exception across diverse product portfolios. The region is also investing in closed-system cell therapy platforms and orchestration tools that unify scheduling, batch execution, and QC evidence in a compliant manner. This foundation supports continued growth in the pharmaceutical manufacturing execution system market as firms expand multi-site templates, strengthen data integrity, and build supply resilience.

Asia-Pacific is the fastest-growing region with a 15.83% CAGR over 2026-2031 for the pharmaceutical manufacturing execution system market size, driven by capacity build-outs in biologics and the scale-up of CDMO services. As manufacturers add new lines and facilities, demand is rising for standardized EBR, validated cloud options, and vendor-managed upgrades that reduce time to qualification. Regional CDMOs adopt modular MES content to onboard sponsors quickly and maintain harmonized quality practices across multi-client portfolios. Vendors are also working with customers on connector strategies for older equipment and point systems to minimize custom code and simplify validation. These priorities keep the pharmaceutical manufacturing execution system market focused on interoperability, cloud scaling, and secure-by-design operations across APAC's expanding manufacturing footprint.

Europe continues to advance through standardized data governance, stronger cybersecurity expectations, and quality-by-design approaches that favor validated digital systems. Across the EU, harmonization of serialization, track-and-trace, and site-level qualification is prompting tighter coupling between MES, ERP, and enterprise repositories. The pharmaceutical manufacturing execution system market in Europe is also emphasizing cloud and hybrid deployments that preserve local control while centralizing analytics and master data. As vendors deepen low-code capabilities and pre-validated content, European manufacturers are accelerating upgrades without compromising validation discipline, especially in biologics clusters. These patterns reinforce steady demand in the pharmaceutical manufacturing execution system market as firms modernize operations, expand serialization coverage, and scale multi-site templates.

- ABB Ltd.

- Apprentice.io, Inc.

- COPA-DATA GmbH

- Critical Manufacturing, S.A.

- Dassault Systemes

- Emerson Electric

- Honeywell International

- Korber AG

- MasterControl, Inc.

- MPDV Mikrolab GmbH

- Parsec Automation Corporation

- POMS Corporation

- Rockwell Automation, Inc.

- SAP

- Schneider Electric SE

- Siemens Healthineers

- Yokogawa Electric

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Compliance and Data Integrity Requirements

- 4.2.2 Pharma 4.0 Digitalization Momentum (ISPE)

- 4.2.3 Need For Real-Time Visibility and End-To-End Traceability

- 4.2.4 Growth In Biologics, Cell and Gene Therapies

- 4.2.5 Computer Software Assurance (CSA) Enabling Risk-Based Validation

- 4.2.6 Continuous Manufacturing (ICH Q13) and Real-Time Release

- 4.3 Market Restraints

- 4.3.1 High Implementation Cost and Program Complexity

- 4.3.2 Integration With Legacy Systems and Data Silos

- 4.3.3 Validation Talent Gaps and CSV/CSA Transition Bottlenecks

- 4.3.4 Master Data and Process Standardization Readiness Shortfalls

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud / SaaS

- 5.3 By Functionality

- 5.3.1 Electronic Batch Records (EBR)

- 5.3.2 Recipe / Workflow Management

- 5.3.3 Equipment Management

- 5.3.4 Deviation & CAPA Integration

- 5.3.5 Serialization Integration

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Pharmaceutical Manufacturers

- 5.4.2 Biopharmaceutical Manufacturers

- 5.4.3 Cell & Gene Therapy Manufacturers

- 5.4.4 CMOs / CDMOs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ABB Ltd.

- 6.3.2 Apprentice.io, Inc.

- 6.3.3 COPA-DATA GmbH

- 6.3.4 Critical Manufacturing, S.A.

- 6.3.5 Dassault Systemes SE

- 6.3.6 Emerson Electric Co.

- 6.3.7 Honeywell International Inc.

- 6.3.8 Korber AG

- 6.3.9 MasterControl, Inc.

- 6.3.10 MPDV Mikrolab GmbH

- 6.3.11 Parsec Automation Corporation

- 6.3.12 POMS Corporation

- 6.3.13 Rockwell Automation, Inc.

- 6.3.14 SAP SE

- 6.3.15 Schneider Electric SE

- 6.3.16 Siemens AG

- 6.3.17 Yokogawa Electric Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment