|

시장보고서

상품코드

2063555

스마트 패치 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Smart Patches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

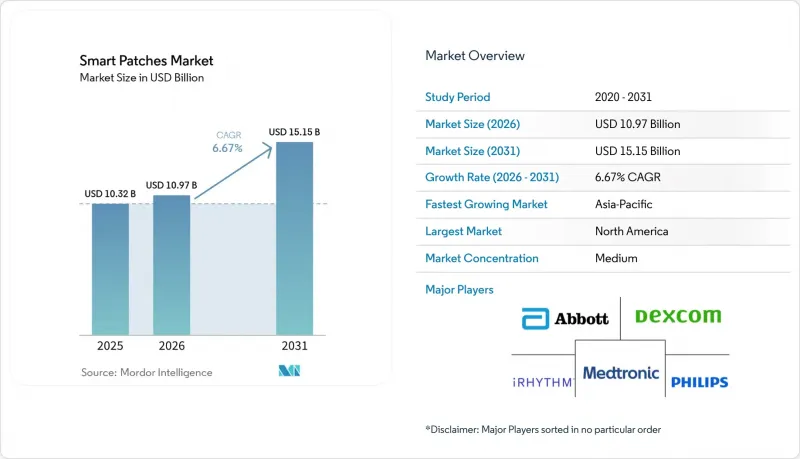

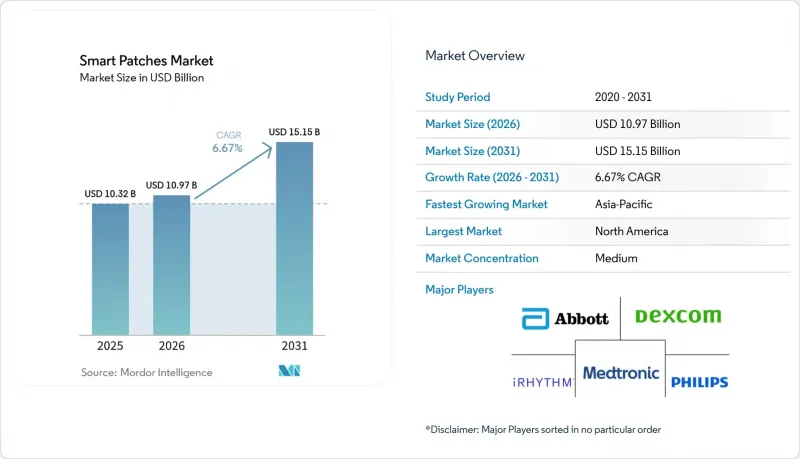

Mordor Intelligence에 의하면, 스마트 패치 시장 규모는 2025년 103억 2,000만 달러에서 2026년에는 109억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 6.67%로 성장을 지속하여, 2031년에는 151억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(모니터링 패치 등), 용도별(당뇨병 관리, 심장 모니터링, 체온 모니터링, 다중 매개변수 RPM 등), 최종 사용자별(병원 및 진료소, 재택 간호, 외래 진료 센터, 스포츠 및 피트니스), 그리고 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 스마트 패치 시장 동향 및 인사이트

RPM의 상환과 원격의료의 확대가 지속적인 재택 모니터링 도입을 뒷받침하고 있습니다.

2026년 1월부터 시행되는 미국의 새로운 RPM 코드(99445, 99470)에 따라, 의료 제공업체는 패치에서 전송되는 호흡, 활동 및 다중 매개변수 데이터에 대해 청구할 수 있게 되며, 청구 가능한 서비스가 혈당 및 혈압 이외의 항목으로 확대됩니다. 2027년까지 연장된 연방 정부의 원격의료에 대한 유연한 대응 조치 덕분에, 임상의들은 대면 진료 없이도 RPM을 시작할 수 있게 되었으며, 지속적인 패치 데이터에 의존하는 ‘재택 병원’ 모델이 촉진되고 있습니다. 펜 메디신(Penn Medicine)의 PATH 프로그램과 같은 대규모 의료 시스템의 시범 사업에서는 패치가 생체 신호를 지휘 센터로 전송함으로써 재입원율 감소 및 병상 이용 일수 감소 효과가 보고되고 있습니다. 민간 보험사들도 메디케어의 보장 범위를 따르기 시작하면서, 웨어러블 모니터링은 의료 제공업체들에게 일상적인 수익원이 되어가고 있습니다. 이 보상 체계를 통해 패치는 단순한 건강 관리 기기에서 보상 대상이 되는 임상적 평가 지표로 그 위상이 바뀌었으며, 도입에 있어 주요 장애물이 제거되었습니다.

당뇨병 및 심혈관 질환의 부담 증가로 인해 모니터링 방식이 피부 패치나 CGM으로 전환되고 있습니다.

세계적으로 집중 인슐린 요법을 받고 있는 환자 수는 1,100만 명을 넘어섰지만, 자동 인슐린 투여 시스템의 도입률은 여전히 15% 미만에 그치고 있어, 혈당 측정 기능이 통합된 펌프 시장에는 여전히 큰 성장 여지가 남아 있습니다. 애보트는 2025년 1분기에 CGM(연속 혈당 모니터링) 부문에서 17억 달러의 매출을 기록했으며, 덱스콤은 연간 46억 달러의 매출을 전망하고 있어, 견조한 수요가 입증되고 있습니다. 이와 동시에 심장 모니터링 분야의 성장도 두드러졌으며, 2024년에 메드트로닉사의 이식형 심장 모니터 ‘LINQ II’가 FDA 승인을 획득하여 장기적인 부정맥 감지가 가능해졌습니다. 당뇨병 환자와 심장 질환 환자가 겹치는 계층은 다중 매개변수 패치의 혜택을 받고 있으며, 이에 따라 각 업체들은 혈당, 심전도, 가속도계 기능을 하나의 부착형 기기에 통합하도록 장려받고 있습니다. CGM 사용이 HbA1c 수치 감소 및 입원율 감소로 이어진다는 임상 연구 결과에 따라, 보험사들의 피부 부착형 센서에 대한 보험 적용 의지가 높아지고 있습니다.

접착제로 인한 피부 자극과 MARSI가 착용 시간 및 순응도를 제한함

의료용 접착제로 인한 피부 손상은 웨어러블 패치의 임상시험에서 여전히 가장 많이 보고되는 이상반응으로, 홍반이나 표피 박리 형태로 나타나며, 이로 인해 조기에 제거해야 하는 경우가 많습니다. 실리콘 젤은 자극을 줄여주지만, 아크릴 계열에 비해 초기 접착력이 약하고 피부 전처리 과정이 필요하기 때문에 소비자들의 사용을 방해하고 있습니다. 2026년 『npj Flexible Electronics』지에 실린 연구에 따르면, 폴리우레탄이 혼합된 나노 메쉬 전극은 6시간 동안 흐르는 물에 노출된 후에도 접착력을 유지한 반면, 폴리비닐알코올(PVA) 전극의 경우 기능을 유지한 비율은 그 3분의 1에 불과했습니다. 표준화된 MARSI 시험이 없는 상황에서 제조업체는 확실한 접착력과 피부 내성을 동시에 확보해야 하며, 이로 인해 7일을 초과하는 착용 기간을 주장하는 것이 복잡해지고 있습니다.

부문별 분석

모니터링 패치는 애보트의 Libre나 데크콤의 G7과 같은 CGM 주력 제품들의 호조에 힘입어 2025년 매출의 54.21%를 차지했습니다. 스마트 패치 시장의 약물 전달 분야는 마이크로니들 백신, 경피 진통제, 패치 펌프가 감지 및 치료 기능을 통합함에 따라 연평균 성장률(CAGR) 8.23%로 성장할 전망입니다. 2026년 초에 출시될 메드트로닉의 ‘MiniMed 780G’와 애보트의 ‘Instinct’ 센서가 결합된 제품은 최초의 오픈 플랫폼형 인슐린 펌프 겸 CGM이 되어, 공급업체를 초월한 치료 생태계의 방향을 제시하고 있습니다.

복합 제품의 독점권이 투자를 유치함에 따라, 약물 전달에 할당되는 스마트 패치 시장 규모는 꾸준히 확대될 것으로 전망됩니다. 전기 자극 패치는 여전히 틈새 시장이지만, 오피오이드 사용을 억제하는 통증 관리 수단으로서 의사들 사이에서 채택이 확대되고 있습니다. 통합 플랫폼은 소모품과 데이터 흐름을 하나로 통합함으로써, 여러 질환을 앓고 있는 환자의 기기 사용 부담을 줄여줍니다. 복합 제품에 대한 규제는 개발 기간을 연장시키지만, 경쟁 우위를 가져다주며 마이크로니들 제조의 규모 확대를 위한 자본 배분을 촉진하고 있습니다. 고분자 반도체 연구를 통해 플렉서블 기판 위에서 저전력 로직 회로를 구현할 수 있게 된 지금, 약물 전달 패치는 투여량을 실시간으로 조정하는 폐루프 알고리즘을 탑재하기에 가장 적합한 위치에 있습니다.

지역별 분석

북미는 메디케어의 원격 환자 모니터링(RPM) 지급, OTC(일반의약품) CGM 출시, 그리고 재택의료의 보급에 힘입어 2025년 매출의 46.90%를 차지했습니다. 아시아태평양의 스마트 패치 시장 규모는 2031년까지 연평균 성장률(CAGR) 8.23%로 확대되며, 가장 빠른 성장세를 보일 것으로 예측됩니다. HLB Lifecare사의 15일간 지속형 Picoling CGM에 대한 한국 식품의약품안전처(MFDS)의 승인 및 Sibionics사의 GS3에 대한 중국 국가약품감독관리국(NMPA)의 허가와 같은 지역별 승인을 통해, 국내 업체들은 폼 팩터 및 가격 면에서 유럽 및 미국의 기존 기업들보다 낮은 가격을 책정할 수 있게 되었습니다.

유럽의 성장세가 둔화되고 있습니다. 이는 기업들이 의료기기 규정(MDR) 준수 및 재설계 주기를 장기화시키는 새로운 배터리 규제에 대응하는 데 어려움을 겪고 있기 때문입니다. 독일의 DiGA 제도에서는 클래스 IIa 패치가 보험 적용 대상이지만, 그 보급은 당뇨병이나 부정맥 치료 사례에 집중되어 있습니다. 남미와 중동의 신흥 시장에서는 신속한 시장 진입을 위해 CE 마크에 의존하고 있지만, 견고한 환불 제도가 부재하여 판매량 증가세가 주춤하고 있습니다. 아시아태평양의 만성 질환 환자층은 전자상거래 및 1차 진료 네트워크를 통해 일반 소비자용 CGM을 도입함으로써, 의료기관 중심의 경로를 뛰어넘을 가능성이 있습니다. 인도에서 MicroTech Medical사의 LinX CGM이 2026년에 승인된 것은 해당 지역 전체로 그 기세가 확산되고 있음을 시사하지만, 인슐린 펌프와의 통합은 아직 초기 단계에 머물러 있습니다. 현지 가격 책정 및 스마트폰 생태계에 정통한 공급업체야말로 스마트 패치 시장에서 가장 빠르게 성장하고 있는 지역에서 시장 점유율을 확보하는 데 가장 유리한 입장에 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the smart patches market size is expected to grow from USD 10.32 billion in 2025 to USD 10.97 billion in 2026 and is forecast to reach USD 15.15 billion by 2031 at 6.67% CAGR over 2026-2031.

This report is Segmented by Type (Monitoring Patches, and More), Application (Diabetes Management, Cardiac Monitoring, Temperature Surveillance, Multiparameter RPM, and More), End-User (Hospitals & Clinics, Home Care, Ambulatory Centers, Sports & Fitness), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Smart Patches Market Trends and Insights

RPM Reimbursement and Telehealth Expansion Sustain Continuous, At-Home Monitoring Adoption

New U.S. RPM codes (99445, 99470), effective January 2026, let providers bill for patch-transmitted respiratory, activity, and multi-parameter data, broadening billable services beyond glucose and blood pressure. Federal telehealth flexibilities, extended through 2027, allow clinicians to start RPM without in-person visits, fueling hospital-at-home models that rely on continuous patch data. Large health-system pilots such as Penn Medicine's PATH program report reduced readmissions and lower bed-day utilization when patches stream vitals to command centers. Private payers have started mirroring Medicare coverage, turning wearable monitoring into a routine revenue stream for providers. The reimbursement framework repositions patches from wellness gadgets to reimbursable clinical endpoints, removing a primary adoption barrier.

Diabetes and Cardiovascular Disease Burden Shifts Monitoring to Skin Patches and CGMs

Global intensive-insulin populations exceed 11 million, yet automated insulin delivery adoption remains under 15%, leaving large headroom for integrated glucose-sensing pumps. Abbott recorded USD 1.7 billion in CGM revenue in 1Q 2025, and Dexcom forecasted USD 4.6 billion full-year sales, underscoring robust demand. Parallel cardiac-monitoring growth is evident in the 2024 FDA clearance of Medtronic's LINQ II insertable cardiac monitor, enabling long-term arrhythmia detection. Overlapping diabetic and cardiac cohorts benefit from multi-parameter patches, prompting vendors to fuse glucose, electrocardiogram, and accelerometry on one adhesive. Clinical studies linking CGM use to lower HbA1c and reduced hospitalization intensify payer willingness to reimburse skin-worn sensors.

Adhesive-Related Skin Irritation and MARSI Limit Wear Time and Compliance

Medical-adhesive skin injury remains the most cited adverse event in wearable-patch trials, presenting as erythema or epidermal stripping that forces premature removal. Silicone gels mitigate irritation but provide weaker initial tack than acrylics, requiring skin-prep steps that deter consumer use. A 2026 npj Flexible Electronics study showed polyurethane-blended nanomesh electrodes retained adhesion after six hours of water flow, while only one-third of poly(vinyl alcohol) electrodes remained functional. Manufacturers must balance secure adhesion with dermatologic tolerance in the absence of standardized MARSI testing, complicating claims for wear beyond seven days.

Other drivers and restraints analyzed in the detailed report include:

- OTC CGMs Expand TAM Beyond Insulin Users, Catalyzing Consumer and Primary-Care Uptake

- Hospital-at-Home and Early-Discharge Pathways Standardize Patch-Based Vitals Monitoring

- Cybersecurity and Privacy Compliance Increase Cost and Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monitoring patches accounted for 54.21% of 2025 revenue, anchored by CGM flagships such as Abbott Libre and Dexcom G7. The drug-delivery subset of the smart patches market is on track for an 8.23% CAGR as microneedle vaccines, transdermal analgesics, and patch pumps integrate sensing and therapy. Medtronic's MiniMed 780G paired with Abbott's Instinct sensor in early 2026 represents the first open-platform insulin pump-plus-CGM, demonstrating a pathway for cross-vendor therapeutic ecosystems.

The smart patches market size allocated to drug delivery is projected to climb steadily as combination-product exclusivity attracts investment. Electrical-stimulation patches, though still niche, are gaining physician adoption for opioid-sparing pain management. Integrated platforms cut device burden for multi-morbidity patients, unifying consumables and data flows. Combination-product regulation extends timelines but offers competitive moats, encouraging capital allocation toward microneedle manufacturing scale-up. With polymer-semiconductor research now enabling low-power logic on flexible substrates, drug-delivery patches are well positioned to embed closed-loop algorithms that titrate dosing in real time.

Geography Analysis

North America commanded 46.90% of 2025 revenue, aided by Medicare RPM payments, OTC CGM launches, and hospital-at-home adoption. The smart patches market size in Asia-Pacific is expected to log the fastest advance, expanding at 8.23% CAGR through 2031. Regional approvals, such as South Korea MFDS clearance for HLB Lifecare's 15-day Picoling CGM and China NMPA authorization for Sibionics GS3, enable domestic vendors to undercut Western incumbents on form factor and price.

European growth trails as companies grapple with Medical Device Regulation conformity and new battery mandates that prolong redesign cycles. Germany's DiGA pathway reimburses Class IIa patches, yet uptake centers on diabetes and arrhythmia use cases. Emerging markets in South America and the Middle East rely on CE marks for quick entry but lack robust reimbursement, dampening volume. Asia-Pacific's chronic-disease base stands to leapfrog clinic-centric pathways by adopting direct-to-consumer CGMs through e-commerce and primary-care networks. India's 2026 clearance of MicroTech Medical's LinX CGM hints at broader regional momentum, though integration with insulin pumps remains nascent. Vendors attuned to local pricing and smartphone ecosystems are best placed to capture share in the fastest-growing geography of the smart patches market.

- Abbott Laboratories

- Blue Spark Technologies

- Dexcom

- Epicore Biosystems, Inc.

- GE Healthcare

- G-Tech Medical, Inc.

- iRhythm Technologies

- Isansys Lifecare Ltd.

- Koninklijke Philips

- Medtronic

- Nemaura Medical, Inc.

- Sensium Healthcare

- SmartCardia SA

- VitalConnect, Inc.

- VivaLNK, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 RPM Reimbursement and Telehealth Expansion Sustain Continuous, At-Home Monitoring Adoption

- 4.2.2 Diabetes And Cardiovascular Disease Burden Shifts Monitoring to Skin Patches and CGMs

- 4.2.3 OTC CGMs Expand TAM Beyond Insulin Users, Catalyzing Consumer and Primary-Care Uptake

- 4.2.4 Hospital-At-Home and Early-Discharge Pathways Standardize Patch-Based Vitals Monitoring

- 4.2.5 FDA DHT Guidance Normalizes Patch Data in Clinical Trials and Endpoints

- 4.2.6 Miniaturized, Flexible Electronics and Long-Wear Adhesives Unlock Multi-Day Comfort

- 4.3 Market Restraints

- 4.3.1 Adhesive-Related Skin Irritation and MARSI Limit Wear Time and Compliance

- 4.3.2 Cybersecurity and Privacy Compliance Increase Cost and Integration Complexity

- 4.3.3 RF Coexistence and EMC Issues in Hospitals Risk Data Loss or Alarms

- 4.3.4 EU Battery Rules Drive Redesigns (Removability/Labeling), Raising Compliance Burden

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Monitoring Patches (vitals, CGM, ECG)

- 5.1.2 Drug Delivery Patches (transdermal, microneedle, patch pumps)

- 5.1.3 Electrical Stimulation Patches (neuromodulation/TENS)

- 5.2 By Application

- 5.2.1 Diabetes Management (CGM)

- 5.2.2 Cardiac Monitoring / Arrhythmia Detection (ECG)

- 5.2.3 Temperature / Fever & Infection Surveillance

- 5.2.4 Multiparameter RPM (home and ambulatory)

- 5.2.5 Wound Monitoring & Post-operative Care

- 5.2.6 Clinical Trials Data Capture (decentralized)

- 5.3 By End-User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Home Care Settings

- 5.3.3 Ambulatory/Diagnostic & Cardiac Centers

- 5.3.4 Sports & Fitness / Workforce Health

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 Blue Spark Technologies

- 6.3.3 Dexcom, Inc.

- 6.3.4 Epicore Biosystems, Inc.

- 6.3.5 GE HealthCare

- 6.3.6 G-Tech Medical, Inc.

- 6.3.7 iRhythm Technologies, Inc.

- 6.3.8 Isansys Lifecare Ltd.

- 6.3.9 Koninklijke Philips N.V.

- 6.3.10 Medtronic plc

- 6.3.11 Nemaura Medical, Inc.

- 6.3.12 Sensium Healthcare

- 6.3.13 SmartCardia SA

- 6.3.14 VitalConnect, Inc.

- 6.3.15 VivaLNK, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment