|

시장보고서

상품코드

2063557

의료 상호운용성 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Healthcare Interoperability AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

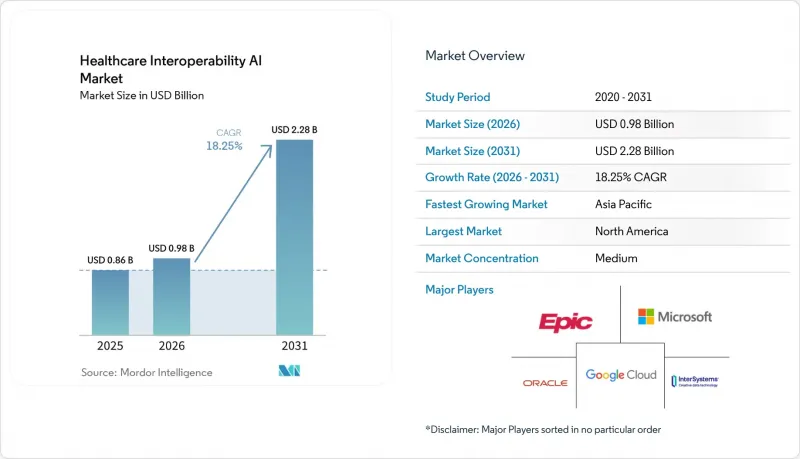

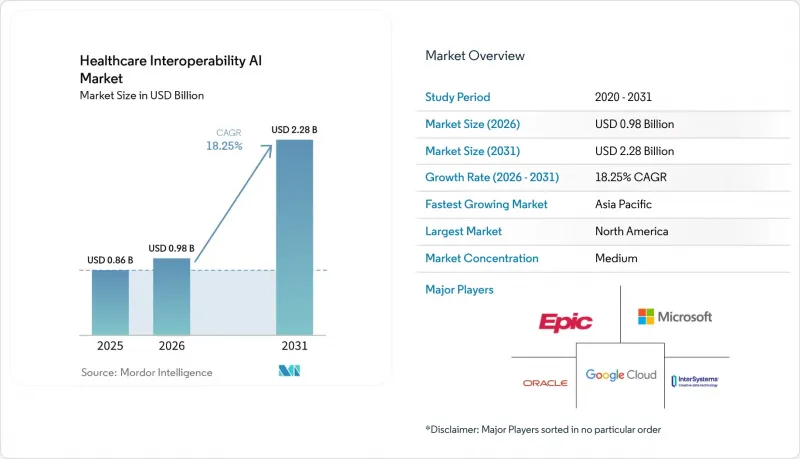

Mordor Intelligence에 의하면, 의료 상호운용성 인공지능(AI) 시장 규모는 2025년에 8억 6,000만 달러로 평가되었습니다. 2026년부터 2031년에 걸쳐 CAGR 18.25%로 성장을 지속하여, 2031년에는 22억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어·기타), 용도(데이터 수집·정규화·기타), 도입 형태(클라우드·기타), 최종 사용자(의료 제공업체·기타), 상호운용성 수준(기초 수준·기타), 지역(북미, 유럽, 아시아태평양·기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료 상호운용성 인공지능(AI) 시장 동향 및 인사이트

규제 요건이 FHIR 기반 데이터 교환 및 API 상호운용성을 가속화

미국 정책에 따라, 보험사는 2027년 1월 1일까지 환자 접근, 의료 제공업체 접근, 보험사 간, 사전 승인 등 4가지 FHIR R4 기반 API를 공개하고 운영해야 할 의무가 부과되었습니다. 결정까지의 기간은 표준 절차의 경우 7일, 신속 처리의 경우 72시간으로 정해져 있으며, 2026년부터는 사전 승인 지표에 관한 연례 공개 보고가 시작됩니다. 이러한 규칙은 리소스 모델, 보안, 일괄 데이터 액세스를 표준화하는 HL7 FHIR R4 및 관련 구현 가이드를 기반으로 하며, 이를 통해 통합의 불일치를 줄이고 확장 가능한 데이터 교환을 지원합니다. 유럽에서는 ‘유럽 헬스 데이터 스페이스(European Health Data Space)’를 통해 2026년 1월까지 의료 제공업체 및 공급업체에 상호운용성 및 보안에 관한 의무를 부과하고, 2029년 3월까지 환자 요약 정보 및 전자 처방전의 1차 이용 데이터 교환을 의무화하며, 2031년 3월까지 영상·검사 데이터를 단계적으로 도입하도록 규정하고 있으며, 위반 시에는 막대한 행정 과태료가 부과됩니다. DARWIN EU는 2025년까지 증거 생성 역량을 확대하고, 표준화된 교환 및 큐레이션에 기반한 다중 데이터베이스 RWD 연구에 대해 더욱 강력한 제도적 지원을 제공했습니다. 미국의 TEFCA 거버넌스는 Facilitated FHIR과 결합되어, 상호운용성을 양자 간 연결에서 네트워크 규모의 데이터 유동성으로 전환하는 데 도움이 되는 중립적인 교환 조건을 설정하고 있습니다. 이러한 정책들은 API 우선 아키텍처, 구조화된 데이터 교환, 그리고 AI 시스템이 조직의 경계를 넘어 안정적으로 활용될 수 있도록 지원하는 동의 기반 워크플로우에 대한 투자를 촉진하고 있습니다.

지급자와 의료 제공업체 간의 자동화 의무(ePA, 첨부 자료)에 따른 AI 중개형 정보 교환의 확대

2024년, 의사들로부터 사전 승인과 관련된 높은 행정적 부담이 보고되었습니다. 여기에는 빈번한 의뢰 및 문서 작성에 소요되는 시간 낭비가 포함되어 있어, EHR 워크플로우 내에서 증거를 자동으로 수집하고 양식을 입력할 필요성이 커졌습니다. HL7의 Da Vinci 구현 가이드는 CRD, DTR, PAS를 통해 ePA를 운영화하여, 실시간 검증, 구조화된 문서 정보의 수집, FHIR 기반의 제출을 가능하게 합니다. 이러한 정보는 AI를 통해 보완되며, 진료 기록에서 증거를 추출할 수 있습니다. 연방 정부의 일정 및 공개 보고 요건은 이용 관리 기준을 충족하면서 감사 가능한 의사결정을 가능하게 하는 자동화를 촉진하고 있습니다. 초기 시범 사례에서는 구조화된 데이터와 NLP를 활용하여 주문 시나 이의 제기 시 문서화된 기준을 사전에 입력함으로써, 처리 시간과 승인률 측면에서 상당한 개선이 나타났습니다. Da Vinci CDex를 통한 첨부 파일 자동화 덕분에 지불 기관은 개별 임상 요소를 요청할 수 있게 되었으며, 이는 팩스 기반 첨부 파일보다 확장성이 뛰어나며 임상 검토 담당자에 대한 설명 가능성을 뒷받침합니다. 규제 당국과 보험사가 알고리즘에 의한 결정을 면밀히 검토하는 가운데, 입력 내용, 근거, 시점을 추적할 수 있는 시스템은 ePA의 지속적인 성과를 유지하기 위한 필수 요건이 될 것입니다.

개인정보, 동의, 국경을 넘는 데이터 전송에 대한 제한

GDPR(EU 개인정보보호규정)에 따르면, 건강 데이터는 명시적인 동의가 필요한 특별 범주로 분류되며, 이를 위반할 경우 고액의 행정 과태료가 부과됩니다. 이로 인해 AI 모델 개발을 위한 2차 활용 파이프라인과 국경을 넘는 데이터 흐름에 드는 비용과 복잡성이 증가합니다. HIPAA는 미국의 기본적인 보호 조치 및 정보 유출 통지 규정을 정하고 있으며, AI 워크로드를 실행하는 클라우드 네이티브 환경에서 조직이 PHI(개인 건강 정보)의 암호화, 접근 제어, 위험 평가를 어떻게 설계해야 하는지를 규정하고 있습니다. 제안된 HIPAA 보안 규정 개정안에 따라 암호화, 다단계 인증, 자산 목록, 취약점 스캔에 관한 보다 강력한 요건이 공식적으로 마련됨에 따라, 이를 통해 관리형 보안 제어 기능을 제공하는 플랫폼으로의 현대화가 가속화될 가능성이 있습니다. EHDS는 2차 이용 데이터를 위한 안전한 처리 환경을 도입하지만, 엄격한 시행 및 상호주의 조건에 따라 EU 역외 신청자의 접근이 제한될 가능성이 있으며, 이로 인해 조직은 EU 내 컴퓨팅 엔클레이브로 이전해야 할 수 있습니다. 최근 기록적인 수준의 정보 유출 사례는 프로덕션 파이프라인에 AI를 도입할 때 동의 사항을 반영한 데이터 흐름, 강력한 암호화, 감사 추적이 필요함을 여실히 보여주고 있습니다. 규정 준수, 동의, 국경을 넘는 데이터 전송에 관한 규정이 지속적인 운영에 필요한 기술적 안전 조치를 정의하게 됨에 따라, 이러한 거버넌스 요건은 의료 상호운용성 인공지능(AI) 시장 전반에 걸쳐 공급업체 선정 및 아키텍처 패턴에 영향을 미치고 있습니다.

부문별 분석

2025년 시점에서 소프트웨어는 의료 상호운용성 인공지능(AI) 시장의 48.79% 점유율을 차지했으나, 구매자들이 신뢰할 수 있는 실시간 데이터 접근을 실현하기 위해 개별 연결을 통합된 허브로 집약함에 따라 플랫폼/미들웨어는 2031년까지 20.46%라는 가장 높은 연평균 성장률(CAGR)을 나타낼 전망입니다. 이러한 변화는 다수의 엔드포인트에 걸쳐 단일 거버넌스 계층을 적용하는 동의 기반 미들웨어를 통해 HL7v2 피드, 일괄 내보내기, FHIR 구독을 중개해야 하는 운영상의 요구를 반영한 것입니다. 플랫폼의 성장은 CCDA에서 FHIR로의 변환, 이벤트 라우팅, 검증 로그를 턴키 워크플로에 통합하는 클라우드 네이티브 데이터 서비스를 통해 더욱 가속화되고 있으며, 이를 통해 대규모 혁신에 소요되는 도입 시간과 비용을 절감할 수 있습니다. 에코시스템 벤더는 제3자가 임상 및 관리 업무 자동화를 구축하는 데 활용할 수 있는 수백 개의 프로덕션용 API와 알림 훅을 공개하고 있으며, 이를 통해 트래픽이 많은 플랫폼 주변의 네트워크 효과가 확대되고 있습니다. 의료 상호운용성 인공지능(AI) 시장은 감사 추적, 접근 제어, 분석 및 모델 훈련에 즉시 대응할 수 있는 구조화된 출력을 확보하면서도 데이터 수집을 확장할 수 있는 플랫폼의 이점을 누리고 있습니다.

엔드포인트의 복잡성이 증가하는 가운데, 오케스트레이터는 유지보수 부담을 줄이고, 새로운 표준으로의 업그레이드를 간소화하며, 하류 AI 이용 사례를 가속화하는 예측 가능한 통합 패턴을 구축합니다. 이 플랫폼은 FHIR 네이티브 데이터 스토어와 관리형 이벤트 인프라를 결합하여, 개발자가 변경 사항을 구독하고, API를 통해 컨텍스트를 확보하며, 완전한 환자 및 청구 내역을 바탕으로 의사 결정 지원 시스템을 구축할 수 있도록 합니다. 또한, 대량의 데이터 교환에는 일관된 정책 적용을 수반하는 동의에 기반한 강제 조치가 필요하지만, 미들웨어는 이를 일원화하고, 감사 및 환자의 접근 권한 관리를 위해 문서화할 수 있습니다. 주요 시장에서 규제 일정이 확정된 지금, 수요는 맞춤형 임시 인터페이스에서 벗어나 다양한 이용 사례에 운영 투자를 분산시키는 확장 가능한 플랫폼으로 전환되고 있습니다. 플랫폼 주도형 접근 방식은 데이터 수집과 용도 로직을 분리하고, 분석용 정규화된 출력을 표준화함으로써 새로운 증거 요건이나 규제 변경에 대해서도 미래를 내다보는 대응이 가능해집니다.

2025년 의료 상호운용성 인공지능(AI) 시장 규모 중 데이터 수집 및 정규화가 46.35%를 차지했습니다. 이는 일상적인 분석 및 보고서 작성을 위해 HL7v2 메시지, CCDA 파일 및 기타 형식을 FHIR 리소스로 표준화해야 하는 기본적인 요구를 반영한 것입니다. 임상 문서의 이해는 LLM을 활용한 추출 기술을 통해 비정형화된 메모나 보고서를 ePA, 품질 지표, RWD/RWE 제출을 지원할 수 있는 정형화된 데이터로 변환하기 때문에 연평균 성장률(CAGR) 21.34%로 가장 빠르게 성장할 것으로 예측됩니다. 또한, AI 시스템이 증거 필드에 미리 데이터를 입력하고 타임라인 및 감사 요건에 따라 결정 사항을 추적함에 따라, 첨부 파일 처리 및 지급 대상자를 위한 워크플로우도 확대되고 있습니다. 이러한 용도는 확립된 비교 대상에 대해 변수 수준의 성능 및 코호트 수준의 재현성을 확인하기 위해, 신뢰할 수 있는 정보 출처에 대한 참조나 검증 프레임워크에 의존하고 있습니다. 이벤트 기반 데이터 교환이 성숙해짐에 따라, 실시간 정규화 및 NLP를 통한 추출이 치료 조정 및 이용 관리를 위한 후속 자동화 과정에 활용되게 될 것입니다.

의료 상호운용성 인공지능(AI) 업계에서는 의료용 NLP와 사용자 정의 가능한 변환 템플릿을 통합한 플랫폼이 개발 주기를 단축하고 오버헤드를 줄이면서 지역별 문서 작성의 미묘한 차이에 적응합니다. 읽기 전용 EHR 연결 기능을 갖춘 임상 데이터 추출 도구는 인용 정보가 포함된 레지스트리 호환 출력을 생성하는 데 도움이 되며, 이를 통해 신뢰성이 향상되고 임상 품질 프로그램에의 도입이 가속화됩니다. 정교한 워크플로우에서 담당자가 AI가 추출한 데이터를 검토함으로써 코딩 정확도와 수익이 향상되어, 의료 제공 기관에 측정 가능한 재무적 효과를 가져다줍니다. FDA 지침에 따라 신뢰성에 대한 기대치가 명확해지는 가운데, 설명 가능성, 데이터 세트의 계보, 공정성 감사를 운영 파이프라인에 통합하는 시스템에 대한 수요가 증가하고 있습니다. 이러한 기능들은 임상 문서, 보험사 제출 자료, 규제 대응을 위한 증거 수집에 이르기까지 일관된 자동화를 뒷받침합니다.

지역별 분석

2025년 의료 상호운용성 인공지능(AI) 시장 규모에서 북미는 48.62%의 점유율을 차지했습니다. 이는 FHIR API에 관한 CMS의 명확한 일정과, 표준화되고 합의에 중점을 둔 상호운용성을 촉진하는 TEFCA 기반 교환 모델의 도입에 힘입은 것입니다. 의료 시스템, 보험사, 벤더는 구조화된 증거를 추출하고, ePA, 품질 관리 프로그램, 운영 분석을 추진하기 위해 AI에 의존하며, 이벤트 주도형 아키텍처와 자동화를 확대되고 있습니다. TEFCA의 도입은 차별 없는 접근에 대한 공통된 기대를 확립함으로써, 네트워크 간 교환이 개선되고 API 우선 오케스트레이션을 위한 플랫폼의 기회가 확대될 것입니다. 이러한 환경 속에서 FHIR API, 알림, 워크플로우 구현을 위한 벤더들의 투자가 가속화되고 있으며, 이에 따라 실시간 조화 및 임상 시스템에 통합된 LLM 기반 추출에 대한 기준이 높아지고 있습니다. 그 결과, 북미의 의료 상호운용성 인공지능(AI) 시장은 정책 주도의 도입과 관리 및 임상 측면 모두에서 데이터 교환을 지원하는 플랫폼의 급속한 발전이 두드러지는 특징을 보이고 있습니다.

유럽에서는 EHDS에 따라 종합적인 체계를 구축하고 있으며, 상호 운용 가능한 1차 이용 데이터 교환 기한과 안전한 처리 환경을 통한 2차 이용 접근에 관한 거버넌스 모델을 정하고 있습니다. 이는 AI 개발과 증거 생성을 지원하는 것입니다. DARWIN EU는 규제 기준을 충족하는 RWD(실세계 데이터) 연구공급을 확대하고 신속한 다국간 분석을 가능하게 하기 위해, 표준화된 데이터 흐름과 공통 모델의 중요성을 강조하고 있습니다. EHDS 시행 시한이 다가옴에 따라, 유럽의 의료 서비스 제공업체와 벤더들은 시스템을 FHIR 프로파일 및 안전한 교환 요건에 부합하도록 조정해야 하며, 이에 따라 변환 및 이벤트를 표준화하고 자동화하는 플랫폼에 대한 수요가 발생하고 있습니다. 이러한 변화에 따라, 유럽의 의료 상호운용성 인공지능(AI) 시장은 분석, 감시, AI 모델 검증에 활용할 수 있는 더 높은 수준의 상호운용성과, 보다 광범위한 2차 활용에 대한 접근을 실현할 수 있는 체제가 점차 갖춰지고 있습니다. 정책 측면에서의 견고한 기반과 각국의 다양한 이행 상황이 공존하고 있으며, 이로 인해 이질적인 지역 시스템들을 일관된 흐름으로 통합할 수 있는 오케스트레이션 계층에 대한 단기적인 수요가 유지되고 있습니다.

아시아태평양은 각국의 헬스케어 스택 및 FHIR을 중심으로 한 프로그램들이 접근성 확대, 정보 교환의 표준화, 공중보건 및 만성질환 관리 워크플로우에 AI를 접목하는 것을 추진함에 따라 연평균 성장률(CAGR) 22.27%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 아시아태평양의 일부 시장에서 클라우드 퍼스트를 도입함에 있어, 레거시 시스템의 제약을 피하고 보안, 감사 가능성, 스트리밍 데이터 소스를 위한 신속한 AI 도입을 실현하는 매니지드 서비스를 선호하는 경향이 있습니다. 해당 지역 전체의 공공 부문 차원에서의 노력에는 인구 수준 분석 및 기관 간 협력을 지원하는 표준 기반의 데이터 교환이 포함되어 있으며, 이를 통해 주요 이용 사례에서 이벤트 주도형 아키텍처의 역할이 더욱 중요해지고 있습니다. 따라서 APAC 지역의 의료 상호운용성 인공지능(AI) 시장은 그린필드 설계, 현대화를 위한 규제 측면의 지원, 그리고 다양한 의료 시스템 전반에 걸쳐 확장 가능하며 동의에 중점을 둔 AI 도입에 대한 수요 증가의 혜택을 받고 있습니다. 이러한 프로그램이 성숙해짐에 따라, 표준화된 데이터 수집, 실시간 알림, 그리고 강력한 거버넌스를 결합한 플랫폼 제공업체들이 이 지역 전체에서 성장 기회를 포착하게 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the healthcare interoperability aI market size reached USD 0.86 billion in 2025 and is projected to reach USD 2.28 billion by 2031, at a CAGR of 18.25% from 2026 to 2031.

This report is Segmented by Component (Software and Others), Application (Data Ingestion and Normalization, and Others), Deployment Mode (Cloud, and Others), End User (Healthcare Providers, and Others), Interoperability Level (Foundational, and Others), and Geography (North America, Europe, Asia-Pacific, and Others). The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Interoperability AI Market Trends and Insights

Regulatory Mandates Accelerating FHIR-Based Exchange and API Interoperability

U.S. policy now compels payers to publish and operate four FHIR R4-based APIs by January 1, 2027, covering Patient Access, Provider Access, Payer-to-Payer, and Prior Authorization, with decision timelines set at 7 days standard and 72 hours expedited and with annual public reporting of prior authorization metrics starting in 2026.These rules are built on HL7 FHIR R4 and associated implementation guides that standardize resource models, security, and bulk data access, which reduces integration variability and supports scalable exchange. In Europe, the European Health Data Space sets mandatory interoperability and security obligations by January 2026 for providers and vendors, requires primary-use data exchange of patient summaries and e-prescriptions by March 2029, and phases in imaging and lab data by March 2031 with significant administrative fines for non-compliance. DARWIN EU expanded its evidence-generation capacity through 2025, signaling stronger institutional support for multi-database RWD studies that depend on standardized exchange and curation. U.S. TEFCA governance, alongside Facilitated FHIR, sets neutral exchange conditions that help interoperability move from bilateral connections to network-scale data liquidity. These policies direct investment toward API-first architectures, structured data exchange, and consent-aware workflows that AI systems can use reliably across organizational boundaries.

Payer-Provider Automation Mandates (ePA, Attachments) Scaling AI-Mediated Exchange

Physicians reported high administrative burdens from prior authorization in 2024, including frequent requests and time lost to documentation, which heightened the need for automated evidence retrieval and form completion inside EHR workflows. The HL7 Da Vinci Implementation Guides operationalize ePA through CRD, DTR, and PAS, enabling real-time checks, structured documentation capture, and FHIR-based submission that can be augmented by AI to extract evidence from charts. Federal timelines and public reporting requirements incentivize automation that meets utilization management standards while providing auditable decisions. Early pilots show material cycle-time and approval-rate gains when structured data and NLP are used to pre-populate documented criteria at order time and during appeals. Attachments automation through Da Vinci CDex allows payers to request discrete clinical elements, which scales better than fax-based attachments and supports explainability for clinical reviewers. As regulators and plans scrutinize algorithmic decisions, systems that trace inputs, justifications, and timings will become requirements for sustained ePA performance.

Privacy, Consent, and Cross-Border Data Transfer Constraints

GDPR classifies health data as a special category that requires explicit consent and imposes steep administrative penalties for violations, which increases the cost and complexity of secondary-use pipelines and cross-border flows for AI model development. HIPAA sets U.S. baseline safeguards and breach notification rules, which shape how organizations design encryption, access controls, and risk assessments for PHI in cloud-native environments that run AI workloads. Proposed HIPAA Security Rule updates would formalize stronger requirements on encryption, multifactor authentication, asset inventories, and vulnerability scanning, which can accelerate modernization toward platforms that provide managed security controls. EHDS introduces secure processing environments for secondary-use data, while strict enforcement and reciprocity conditions can limit access for non-EU applicants, which pushes organizations toward in-region compute enclaves. Recorded breach volumes in recent years underscore the need for consent-aware data flows, robust encryption, and audit trails when deploying AI in production pipelines. These governance demands influence vendor selection and architecture patterns across the Healthcare Interoperability AI Market because compliance, consent, and cross-border transfer rules now define technical guardrails for sustained operations.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native Health Data Platforms Embed AI for Unstructured-To-FHIR Conversion

- RWD/RWE Pipelines Need Automated Normalization and Terminology Mapping

- Heterogeneous Legacy Systems and Shortages of Skilled Integration Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 48.79% of Healthcare Interoperability AI market share in 2025, while Platforms/Middleware is projected to post the fastest 20.46% CAGR through 2031 as buyers consolidate point connections into orchestrated hubs for reliable real-time data access. This shift reflects the operational need to mediate HL7v2 feeds, bulk exports, and FHIR Subscriptions through consent-aware middleware that enforces a single governance layer across many endpoints. Platform growth is further supported by cloud-native data services that streamline CCDA-to-FHIR conversion, event routing, and validation logs into turnkey workflows, which lowers implementation time and cost for large-scale transformations. Ecosystem vendors publish hundreds of production APIs and notification hooks that third parties consume to build clinical and administrative automation, which increases network effects around high-volume platforms. The Healthcare Interoperability AI Market benefits from platforms that can scale ingestion while ensuring audit trails, access controls, and structured outputs that are ready for analytics and model training.

As endpoint complexity grows, orchestrators reduce maintenance overhead, simplify upgrades to new standards, and create predictable integration patterns that accelerate downstream AI use cases. Platforms combine FHIR-native data stores and managed event infrastructure so developers can subscribe to changes, retrieve context through APIs, and build decision support on top of complete patient and claims histories. High-volume exchange also requires consent-aware enforcement with consistent policy application, which middleware can centralize and document for audits and patient access rights. With regulatory timelines now fixed in major markets, demand has shifted from custom one-off interfaces to scalable platforms that spread operational investment across many use cases. Platform-led approaches also future-proof against new evidence needs and regulatory updates by decoupling data capture from application logic and by standardizing normalized outputs for analytics.

Data Ingestion and Normalization accounted for 46.35% of the Healthcare Interoperability AI market size in 2025, reflecting the foundational need to standardize HL7v2 messages, CCDA files, and other formats into FHIR resources for routine analytics and reporting. Clinical Document Understanding is projected to grow the fastest at a 21.34% CAGR as LLM-enabled extraction turns unstructured notes and reports into structured data that can support ePA, quality measures, and RWD/RWE submissions. Attachment processing and payer workflows are also expanding as AI systems pre-populate evidence fields and track determinations against timelines and audit requirements. These applications rely on source-of-truth references and validation frameworks that confirm variable-level performance and cohort-level replication against established comparators. As event-driven exchange matures, real-time normalization and NLP extraction will feed downstream automation for care coordination and utilization management.

Within the Healthcare Interoperability AI industry, platforms with integrated medical NLP and configurable transformation templates shorten delivery cycles and adapt to local documentation nuances with less overhead. Clinical abstraction tools with read-only EHR connectivity help produce registry-ready outputs with embedded citations, which increases trust and speeds adoption in clinical quality programs. Coding accuracy and revenue improvements follow when human reviewers validate AI-extracted data in refined workflows, which contribute to measurable financial impact for provider organizations. With FDA guidance clarifying credibility expectations, demand is rising for systems that integrate explainability, dataset lineage, and fairness audits into operational pipelines. These capabilities underpin consistent automation across clinical documentation, payer attachments, and regulatory evidence capture.

Geography Analysis

North America accounted for 48.62% share of the Healthcare Interoperability AI market size in 2025, supported by firm CMS timelines for FHIR APIs and by adoption of TEFCA-based exchange models that favor standardized, consent-aware interoperability. Health systems, payers, and vendors are scaling event-driven architectures and automation that rely on AI to extract structured evidence and to power ePA, quality programs, and operations analytics. TEFCA implementation sets shared expectations for nondiscriminatory access, which improves cross-network exchange and expands the platform opportunity for API-first orchestration. Vendor investments in FHIR APIs, notifications, and workflow-enablement accelerate in this environment, which raises the baseline for real-time harmonization and for LLM-based extraction integrated into clinical systems. As a result, the Healthcare Interoperability AI Market in North America is characterized by policy-led adoption and rapid platform improvements that support both administrative and clinical exchange.

Europe is building a comprehensive framework under EHDS that sets deadlines for interoperable primary-use data exchange and a governance model for secondary-use access through secure processing environments, which supports AI development and evidence generation. DARWIN EU expands the supply of regulatory-grade RWD studies and elevates the importance of standardized data flows and common models to enable rapid, multi-country analyses. As EHDS deadlines approach, European providers and vendors must align systems to FHIR profiles and secure exchange requirements, which creates demand for platforms that standardize and automate transformations and events. These changes position the Healthcare Interoperability AI Market in Europe for higher baseline interoperability and broader secondary-use access that can be harnessed for analytics, surveillance, and AI model validation. Policy strength coexists with varied national implementations, which sustains near-term demand for orchestration layers that can align heterogeneous local systems into consistent flows.

Asia-Pacific is projected to be the fastest-growing region at a 22.27% CAGR as national health stacks and FHIR-centered programs expand access, standardize exchange, and embed AI in public health and chronic disease management workflows. Cloud-first deployments in several APAC markets avoid legacy constraints and favor managed services that deliver security, auditability, and rapid AI enablement for streaming data sources. Public-sector initiatives across the region are incorporating standards-based exchange that supports population-level analytics and cross-institutional coordination, which increases the role of event-driven architectures for critical use cases. The Healthcare Interoperability AI Market in APAC therefore benefits from greenfield design, regulatory support for modernization, and growing demand for consent-aware AI deployment that can scale across diverse health systems. As these programs mature, platform providers that combine standardized ingestion, real-time notifications, and strong governance will capture growth opportunities across this region.

- Amazon Web Services

- Change Healthcare (Optum)

- CitiusTech

- Datavant

- Edifecs

- Epic Systems

- Experian Health

- GE Healthcare

- Google Cloud

- IBM

- Informatica

- InterSystems

- Lyniate (Rhapsody & Corepoint)

- Microsoft

- NextGen Healthcare

- Oracle

- Particle Health

- Redox

- Smile Digital Health

- Snowflake

- Verato

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Mandates Accelerating FHIR-Based Exchange and API Interoperability

- 4.2.2 Payer-Provider Automation Mandates (ePA, Attachments) Scaling AI-Mediated Exchange

- 4.2.3 Cloud-Native Health Data Platforms Embed AI for Unstructured-To-FHIR Conversion

- 4.2.4 RWD/RWE Pipelines Need Automated Normalization and Terminology Mapping

- 4.2.5 LLM-Assisted Clinical Document Understanding Reduces Integration Backlog

- 4.2.6 Event-Driven Streaming (FHIR Subscriptions, IoMT) Enabling Real-Time Harmonization

- 4.3 Market Restraints

- 4.3.1 Privacy, Consent, and Cross-Border Data Transfer Constraints

- 4.3.2 Heterogeneous Legacy Systems and Shortages of Skilled Integration Talent

- 4.3.3 Validation Burden and Explainability Risks for AI-Generated Mappings

- 4.3.4 Ecosystem Lock-In and Commercial Disincentives to Portability

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Platforms/Middleware

- 5.2 By Application

- 5.2.1 Data Ingestion and Normalization

- 5.2.2 Clinical Document Understanding

- 5.2.3 Patient Matching and Identity Resolution

- 5.2.4 Prior Authorization and Claims Attachments Automation

- 5.2.5 Others

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By End User

- 5.4.1 Healthcare Providers

- 5.4.2 Healthcare Payers

- 5.4.3 Life Sciences / Pharma Companies

- 5.4.4 Others

- 5.5 By Interoperability Level

- 5.5.1 Foundational

- 5.5.2 Structural

- 5.5.3 Semantic

- 5.5.4 Organizational

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Amazon Web Services

- 6.3.2 Change Healthcare (Optum)

- 6.3.3 CitiusTech

- 6.3.4 Datavant

- 6.3.5 Edifecs

- 6.3.6 Epic Systems Corporation

- 6.3.7 Experian Health

- 6.3.8 GE HealthCare

- 6.3.9 Google Cloud

- 6.3.10 IBM

- 6.3.11 Informatica

- 6.3.12 InterSystems

- 6.3.13 Lyniate (Rhapsody & Corepoint)

- 6.3.14 Microsoft

- 6.3.15 NextGen Healthcare

- 6.3.16 Oracle

- 6.3.17 Particle Health

- 6.3.18 Redox

- 6.3.19 Smile Digital Health

- 6.3.20 Snowflake

- 6.3.21 Verato

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment