|

시장보고서

상품코드

2063558

석고 및 스플린트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Casting And Splinting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

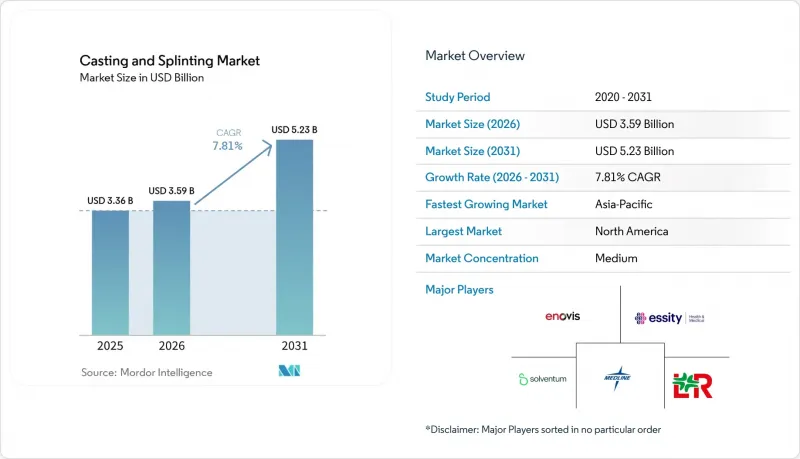

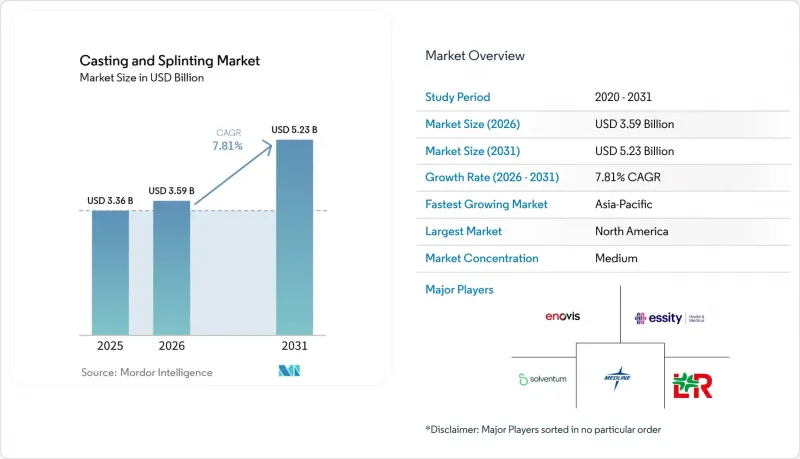

Mordor Intelligence에 의하면, 석고 및 스플린트 시장 규모는 2025년에 33억 6,000만 달러로 평가되었습니다. 2026년에 35억 9,000만 달러에서 2031년까지 52억 3,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 7.81%로 성장할 것으로 전망됩니다.

본 보고서는 제품 유형(석고 용품·기구 등), 소재(유리 섬유/합성 폴리우레탄 등), 용도(골절 치료 등), 최종 사용자(병원 등), 유통 채널(의료 기관에 대한 직접 판매 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 석고 및 스플린트 시장 동향 및 인사이트

노화에 따른 취약성 골절이 수요를 뒷받침하고 있습니다.

의료 시스템은 고령자의 안정적인 손상에 대한 보존적 치료를 중시하는 비수술적 치료 경로를 확대함으로써, 취약성 골절의 지속적인 증가에 대응하고 있습니다. 고령자의 손목·전완 골절은 수술이 적합하지 않은 경우 종종 깁스나 부목으로 전환되기 때문에 외래 및 재활 현장에서 고정 기구에 대한 지속적인 수요가 증가하고 있습니다. 대퇴골 경부 골절 후 관리에서는 회복 기간 동안 보호용 보조기나 부츠에 대한 추가적인 수요가 발생하며, 고정 기구의 사용 기간이 급성기를 넘어 연장됩니다. 유럽의 보험사들은 ‘패스트트랙 골절 클리닉’의 표준화를 추진하고 있으며, 이 모델은 고령 인구가 증가하고 있는 아시아의 주요 도시 지역으로도 확산되고 있습니다. 취약성 골절의 예방 및 관리 경로에 대한 관심이 높아짐에 따라, 통합적인 근골격계 치료에서 석고와 스플린트의 지속적인 사용이 뒷받침되고 있습니다. 취약성 골절의 예방 및 관리에 관한 WHO의 지속적인 지침은 정형외과 진료 분야의 서비스 모델과 자원 배분을 지속적으로 형성하고 있습니다.

외래, ASC, 응급 치료로 워크플로우 전환

2025년 초까지 미국에는 12,294곳의 외래수술센터(ASC)가 있었으며, 그중 3분의 1 이상의 시설에서 정형외과 서비스를 제공하고 있었고, 당시 외과적 시술의 대부분은 외래 환경에서 이루어지고 있었습니다. ASC가 당일 퇴원 워크플로우와 효율화된 공급망을 중시하는 보상 개정안을 꾸준히 확보해 나감에 따라, 지급 정책의 일관성이 이러한 전환을 뒷받침하고 있습니다. 의료진은 경화 속도가 빠르고, 짧은 경과 관찰 기간 내에 조기 보행을 가능하게 하는 가볍고 발열이 적은 합성 깁스 시스템을 점점 더 많이 채택하고 있습니다. 재고 전략에서는 발주, 보관, 코딩을 간소화하는 사전 포장 키트나 전용 SKU가 중시되고 있으며, 이에 따라 수익성이 높은 제품의 비중이 높아지고 있습니다. 워크플로우의 디지털화는 MotionMD와 같은 플랫폼이 특정 고정용 SKU를 적절한 청구 코드나 치료 과정 내의 기록과 연계하도록 지원함으로써 도입을 더욱 가속화하고 있습니다.

폴리우레탄 내 디이소시아네이트에 관한 규제 동향

폴리우레탄 가공에 사용되는 단량체성 디이소시아네이트에 대한 새로운 EU 노출 기준은 작업장 공기질 및 취급 절차에 대해 더욱 엄격한 규제를 도입함으로써, 제조 공정의 재설계 및 추가 교육 의무를 초래하고 있습니다. 기준이 전면 시행됨에 따라, 사업장은 환기 설비를 갖추어야 하며, 지속적인 모니터링을 실시하고, 정해진 주기에 따라 근로자에 대한 교육을 갱신해야 합니다. 이러한 요건들은 평균 판매 가격(ASP)이 낮고 대량으로 소비되는 소모품에 전가하기 어려운 비용을 추가함으로써, 표준 석고 테이프의 이익률에 압박을 가하고 있습니다. 유럽의 각 공급업체들은 규제 대상인 입찰 프로젝트에 참여할 기회를 유지하기 위해 MDR 인증 취득을 추진하는 한편, 디이소시아네이트가 포함되지 않은 대체재 개발을 가속화하고, 수성 분산액으로의 전환을 추진하고 있습니다. 업계 매체의 보도에 따르면, EU 전역에 걸쳐 통일된 노출 기준치와 일정이 강조되고 있으며, 이러한 요소들이 현재 조달 및 제품 설계에 대한 의사결정에 영향을 미치고 있습니다.

부문별 분석

2025년에는 임상의들이 안정성이 허용하는 범위 내에서 기능적 치료를 채택함에 따라, 깁스 용품 및 기구가 매출의 55.23%를 차지했습니다. 병원에서는 전위 골절이나 수술 직후의 고정 시 경성 깁스의 사용이 보편화되어 있으며, 이것이 깁스용 도구 및 부속품 도입의 기반을 뒷받침하고 있습니다. 스플린트는 조절성, 위생 측면, 가벼운 활동으로의 조기 복귀가 요구되는 외래 치료 과정에서 지지를 넓혀가고 있습니다. 또한, 의료기관에서는 깁스를 제거할 때 발생하는 분진에 대한 노출을 줄이기 위해, 인체공학에 기반한 깁스 커터와 집진용 액세서리의 중요성을 더욱 강조하고 있습니다. 석고 및 스플린트 시장에서는 대량 처리를 수행하는 시설의 워크플로우를 표준화하는 패키지형 스플린트 키트나 색상별로 구분된 재료로의 전환이 진행되고 있습니다.

부목용 소모품 및 기기 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 8.56%로 성장할 것으로 전망됩니다. 기성품 유리섬유 및 열가소성 수지 부목은 외래 진료나 응급 진료 클리닉에서 착용이 간편하고 장착 시간이 짧다는 장점 덕분에 부목 시장에서 주도적인 점유율을 차지하고 있습니다. 일반적인 반복성 스트레스 장애용 야간 부목은 재택 사용 및 원격 지도를 지원하는 보험 적용 방침의 혜택을 받고 있습니다. 가소성이 있는 알루미늄 폼으로 만든 부목은 간편성과 재사용성이 중시되는 응급의료 키트에서 여전히 중요한 역할을 하고 있습니다. 석고 및 스플린트 시장에서는 의료 제공업체가 각 고정 처치에 대해 적절한 보상을 받을 수 있도록 제품 설계를 코딩 및 문서화 도구와 연동하고 있습니다. 기능성 보조기 개념이 널리 보급됨에 따라, 석고 및 스플린트 시장의 제품 구성은 보호 기능을 유지하면서도 감독 하에 운동을 할 수 있게 해주는 탈부착 가능한 시스템을 중시하는 경향을 보이고 있습니다.

2025년에는 유리섬유 또는 합성 폴리우레탄이 매출의 45.15%를 차지했습니다. 2024년 1월 『BMC Musculoskeletal Disorders』지에 실린 기사에서는 획기적인 바이오 폴리에스테르 깁스가 소개되었습니다. 이 혁신적인 깁스는 기존의 유리섬유 깁스와 동등한 안정성을 갖추고 있을 뿐만 아니라, 환자의 만족도를 높이고, 환경 친화적이며, 안전성도 향상시켰습니다. 이 연구에서는 100명의 환자가 봉투를 이용한 무작위 배정을 통해 두 그룹 중 하나에 배정되었습니다. 하나는 바이오 폴리에스테르 깁스군(대만 타이베이의 Taipei Smart Materials 사 제품인 ‘MEDlite Thermo Casting Tape’ 사용), 다른 하나는 유리섬유 깁스군(미국 미네소타주 메이플우드의 3M Health Care 사 제품인 ‘Scotchcast’ 사용)입니다. 각 그룹은 50명의 환자로 구성되었습니다. 기존의 합성 깁스에는 이소시아네이트 등의 유해 성분이 포함되어 있는 경우가 많아, 가려움, 발적, 건조 등의 피부 트러블을 유발할 가능성이 있습니다. 이 새로운 바이오 석고는 새로 개발된 무독성 생분해성 공중합체로 만들어졌습니다. 이 공중합체(폴리(에틸렌 세바신산-코-에틸렌 아디핀산)(PESA))는 친환경 자원인 세바신산으로부터 합성되었으며, 에틸렌글리콜, 트리메식산, 아미노카프로산, 아디핀산과 공중합되어 있습니다. 특히, 동물 실험을 통해 이러한 화학적 알레르겐에 피부가 노출될 경우 천식 반응을 유발할 가능성이 있는 것으로 밝혀졌습니다.

저온 열가소성 수지는 치과 진료실에서 재성형이 가능하기 때문에 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 8.65%를 기록하며 가장 빠르게 성장하고 있는 소재입니다. 열가소성 수지는 온수 또는 온도가 조절된 환경에서 연화되어, 임상의가 장치를 완전히 다시 장착하지 않고도 착용감을 미세하게 조정할 수 있게 해줍니다. 지속가능성에 관한 규제가 있는 지역에서는 성형 업체의 인증과 병원의 조달 기준에 힘입어, 인증을 받은 바이오 열가소성 수지 배합이 비하중용 기기에 등장하기 시작하고 있습니다. 저점착성 수지를 사용한 폴리에스터계 테이프는 톱으로 제거할 때 발생하는 분진을 줄여주고, 소아의 경과 관찰 영상 진단에서 중요하게 여겨지는 투과성을 향상시킨다는 특징이 있습니다. 석고 및 스플린트 시장에서는 일상적인 착용 시 충분한 강성을 유지하면서도 피부 트러블, 악취, 침투를 줄여주는 소재에 대한 선호가 계속해서 나타나고 있습니다.

파리 석고는 도입 비용과 공급의 용이성이 제품 선정의 기준이 되는 예산 제약이 있는 환경에서 여전히 중요한 역할을 하고 있습니다. 알루미늄 스플린트는 재사용성과 현장에서의 신속한 적용이 요구되는 특수한 용도에 활용되고 있습니다. 디이소시아네이트에 대한 규제가 대체재 도입을 촉진하고, 진료소들이 소형 가열 장치에 투자하고 있는 시장에서는 열가소성 수지의 채택이 가속화되고 있습니다. 석고 및 스플린트 시장에서는 구매자들이 롤당 비용, 조절성, 환자의 편안함, 진료소의 처리 능력을 비교 검토하는 과정에서 기존의 유리섬유 테이프와 지속적으로 확대되고 있는 열가소성 수지 제품 라인이 모두 수용되고 있습니다. 공급업체들이 차세대 복합 소재와 항균 첨가제를 출시함에 따라 소재의 선택지는 계속해서 다양해지고 있으며, 이것이 경쟁상의 차별화를 지속시키고 있습니다.

지역별 분석

북미는 외래 진료와의 연계, ASC(외래수술센터(ASC))로의 광범위한 보급, 가치 기반 의료(Value-Based Care) 하에서 보험 적용이 보장되는 프리미엄 고정 기술의 급속한 도입을 배경으로, 2025년에는 매출의 45.64%를 차지했습니다. 이 지역의 외래 진료 인프라는 2025년 기준 미국 전역에 1만 2,294곳이 있는 ASC(외래수술센터(ASC))와 입원 시설 밖에서 이루어지는 시술의 높은 비중을 바탕으로 하고 있으며, 이로 인해 골절 치료는 당일 고정 옵션으로 이어지고 있습니다. 의료진은 소아 및 성인 환자의 경우, 착용 편의성과 치료 순응도를 높이기 위해 맞춤형 3D 프린팅 스플린트와 물에 젖어도 문제가 없는 라이너 시스템을 도입하고 있습니다. 클리닉이나 ASC에서는 신속성을 중시하고 있어, 짧은 시간 내에 경화되는 저발열성 합성 소재의 도입이 확대되고 있으며, 이를 통해 짧은 경과 관찰 기간 후 퇴원이 가능해졌습니다. 지역 내 병원 간 통합으로 인해 외상 환자 수가 일부 이동하는 한편, 이익률을 유지하기 위해 재고 관리의 자동화와 코딩 정확성에 대한 중요성이 커지고 있습니다. 2025년 프로 스포츠에서 나타난 부상 양상의 변화는 안전 대책이 부상 유형에 미치는 영향을 여실히 보여주고 있으며, 규정 개정에 따라 하지 부상이 감소하고 있습니다. 북미의 석고 및 스플린트 시장에서는 외래 진료 전반에 걸쳐 공급의 신뢰성, 환자의 편의성, 정확한 기록 관리가 계속해서 중요시되고 있습니다.

아시아태평양에서는 도시화에 따라 외상 발생률이 증가하고, 또한 보편적 의료 보장 프로그램으로 인해 3차 의료 기관 이외의 곳에서도 안정화 처치를 받을 수 있는 기회가 확대됨에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.31%를 나타낼 것으로 예측됩니다. 중국에서는 고령화에 따라 취약성 골절 환자 수가 증가하고 있는 반면, 인도와 동남아시아에서는 자금 조달 및 의뢰 네트워크 확충을 통해 지역 차원의 골절 치료 접근성이 향상되고 있습니다. 일본의 주요 의료기관에서 실시된 소아용 3D 프린팅 부목에 대한 시범 시험에서는 양호한 기능적 결과가 보고되었으며, 임상적 수용성과 맞춤형 제작의 장점이 조화를 이루는 분야에서 고급 제품에 대한 관심이 높아지고 있습니다. 일부 시장에서는 정부의 지원을 통해 석유화학제품공급을 안정화시키고, 깁스 테이프에 필요한 수지의 안정적인 공급을 확보하는 것을 목표로 하고 있습니다. 광역적인 지역 전체에 걸쳐 자원이 부족한 환경에서는 비용과 공급의 지속성 측면에서 석고가 여전히 중요한 역할을 하고 있지만, 유통망이 개선됨에 따라 유리섬유 제품의 사용이 증가하고 있습니다. 석고 및 스플린트 시장은 프리미엄 맞춤형 제품과 대량 소비형 소모품 모두를 반영하여 아시아태평양 전체에서 제품 포트폴리오의 균형을 잘 맞추고 있습니다.

유럽은 규제 변경과 무역 마찰이라는 이중의 압박에 직면해 있으며, 이러한 요인들은 공급업체의 소재 선정 및 수출 동향에 영향을 미치고 있습니다. EU의 새로운 이소시아네이트 노출 한계치는 규정 준수를 위한 투자를 필요로 하며, 수지 재조제를 촉진하는 한편, 석고용 테이프의 제품 선택을 좌우하는 입찰 사양서에도 영향을 미치고 있습니다. 2025년 이후, 일부 수출 시장에서 의료기기에 부과되는 수입 관세로 인해 공급업체들은 비용 위험을 줄이기 위해 물류 경로를 조정하거나 생산 거점을 재배치하도록 촉구하고 있습니다. 프랑스에서는 일생 동안 흔히 겪는 발목 부상에 대한 탈부착식 부목의 사용이 보험 급여 정책에 의해 지원되고 있어, 기능적인 해결책에 대한 안정적인 수요가 유지되고 있습니다. 스페인과 이탈리아에서는 최저 단가를 평가하는 공공 입찰 지침서를 계속 따르고 있으며, 이로 인해 경량 합성 소재와 함께 석고의 역할도 유지되고 있습니다. 유럽공급업체들은 차별화 요인으로 MDR 인증 및 지속가능성 노력을 강조하는 한편, 병원 및 클리닉을 대상으로 한 주문 및 교육을 효율화하기 위한 디지털 포털을 확충하고 있습니다. 유럽의 석고 및 스플린트 시장은 규제 준수를 원동력으로 한 제품 발전과, 외상 및 정형외과 분야의 대규모 수요에 따른 꾸준한 활용 사이의 균형을 반영하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the casting and splinting market size is projected to be USD 3.36 billion in 2025, USD 3.59 billion in 2026, and reach USD 5.23 billion by 2031, growing at a CAGR of 7.81% from 2026 to 2031.

This report is Segmented by Product Type (Casting Supplies & Equipment, and More), Material (Fiberglass/Synthetic Polyurethane, and More), Application (Fracture Management, and More), End-User (Hospitals, and More), Distribution Channel (Direct To Providers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Casting And Splinting Market Trends and Insights

Aging-Related Fragility Fractures Sustaining Demand

Health systems are responding to sustained increases in fragility fractures by expanding non-operative pathways that emphasize conservative care for stable injuries in older adults. Wrist and forearm fractures in seniors often transition to casting and splinting when surgery is not indicated, reinforcing recurring demand for immobilization devices in outpatient and rehabilitation settings. Post-hip fracture care creates downstream need for protective orthoses and boots during recovery, extending immobilization use beyond the acute event. European payers have moved to standardize fast-track fracture clinics, a model that is diffusing to major Asian urban centers where geriatric cohorts are expanding. Heightened attention to prevention and care pathways for fragility events underscores continuous utilization of casting and splinting products within integrated musculoskeletal care. Ongoing WHO guidance on fragility fracture prevention and management continues to shape service models and resource allocation in orthopedic care.

Shift to Outpatient, ASC, and Urgent Care Workflows

The United States counted 12,294 ambulatory surgery centers by early 2025 with orthopedic services embedded across more than one third of sites, and outpatient settings handled the large majority of surgical procedures by that time. Payment policy alignment supports this shift as ASCs gain steady reimbursement updates that favor same-day discharge workflows and streamlined supply chains. Providers increasingly adopt lightweight, low-exotherm synthetic casting systems that cure quickly and support rapid ambulation within narrow observation windows. Inventory strategies favor prepackaged kits and dedicated SKUs that simplify ordering, storage, and coding, which raises mix toward higher-margin products. Workflow digitization further accelerates adoption, as platforms like MotionMD help tie specific immobilization SKUs to appropriate billing codes and documentation within the episode of care.

Regulatory Exposure to Diisocyanates in Polyurethanes

New EU exposure limits for monomeric diisocyanates in polyurethane processing introduce tighter controls on workplace air quality and handling procedures, prompting manufacturing reformulation and additional training obligations. Facilities must adapt ventilation, implement continuous monitoring, and refresh worker education on defined intervals as the limits phase into full enforcement. These requirements add costs that are harder to pass through for low-ASP, high-volume consumables, creating margin pressure on standard casting tapes. European suppliers are accelerating development of diisocyanate-free alternatives and moving to water-based dispersions, while advancing MDR certifications to preserve access in regulated tenders. Communication from industry publications has highlighted the harmonized exposure thresholds and timelines across the EU that are now shaping procurement and product design decisions.

Other drivers and restraints analyzed in the detailed report include:

- Digital/3D Scanning and Additive Manufacturing Enable Custom Immobilization

- Material Innovation Toward Lightweight Fiberglass and Thermoformable Systems

- Polymer and Logistics Volatility Impacting Input Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Casting supplies and equipment held 55.23% of revenue in 2025 as clinicians adopt functional treatment where stability permits. Hospitals maintain steady utilization of rigid casts for displaced fractures and immediate post-operative stabilization, which anchors the installed base of casting tools and accessories. Splinting gains traction for ambulatory care pathways that require adjustability, hygiene, and faster return to light activity. Clinics also emphasize ergonomic cast cutters and dust extraction accessories to reduce particulate exposure during removal. The casting and splinting market continues to shift mix toward prepackaged splinting kits and color-coded materials that standardize workflows across high-volume sites.

Splinting supplies and equipment are projected to grow at 8.56% CAGR during 2026-2031. Prefabricated fiberglass and thermoplastic splints capture a leading share within splinting due to ease of application and lower setup times in outpatient and urgent care clinics. Night splints for common repetitive strain conditions benefit from coverage policies that support home use and remote guidance. Malleable aluminum foam splints retain a role in emergency medical kits where simplicity and reusability matter. The casting and splinting market aligns product design with coding and documentation tools that help providers secure appropriate reimbursement for each immobilization episode. As functional bracing philosophies diffuse, the product mix within the casting and splinting market favors removable systems that maintain protection while enabling monitored motion.

Fiberglass or synthetic polyurethane accounted for 45.15% of revenue in 2025. A January 2024 article in BMC Musculoskeletal Disorders highlighted a groundbreaking biobased polyester cast. This innovative cast not only matches the stability of traditional fiberglass casts but also enhances patient satisfaction, all while being more eco-friendly and safer. In the study, 100 patients were randomly assigned via sealed envelopes to one of two groups: the biobased polyester cast group (using MEDlite Thermo Casting Tape from Taipei Smart Materials, Taipei, Taiwan) or the fiberglass cast group (utilizing Scotchcast from 3M Health Care, Maplewood, Minnesota, U.S.). Each group comprised 50 patients. Traditional synthetic casts often contain harmful components such as isocyanates, which can lead to skin issues, including itching, redness, and dryness. This novel biobased cast is crafted from a newly developed, nontoxic, and biodegradable copolymer. This copolymer, named poly(ethylene sebacate-co-ethylene adipate) (PESA), is synthesized from the green resource sebacic acid and is copolymerized with ethylene glycol, trimesic acid, aminocaproic acid, and adipic acid. Notably, animal studies have indicated that skin exposure to such chemical allergens can trigger asthmatic responses.

Low-temperature thermoplastics are the fastest-growing material at an 8.65% CAGR for 2026-2031 due to chairside remoldability. Thermoplastics soften in warm-water or controlled-heat setups and allow clinicians to fine-tune fit without complete reapplication. In regions with sustainability mandates, qualified bio-based thermoplastic formulations have begun to appear in non-load-bearing devices, supported by molder certifications and hospital procurement criteria. Polyester-based tapes with low-tack resins emphasize lower dust during saw removal and improved radiolucency, which is valued in pediatric follow-up imaging. The casting and splinting market shows ongoing preference for materials that reduce skin complications, odor, and maceration, while maintaining adequate rigidity in daily wear.

Plaster of Paris remains relevant for budget-constrained settings where acquisition cost and supply simplicity guide product selection. Aluminum splints serve specialized use cases that benefit from reusability and quick field application. Thermoplastic adoption gains momentum in markets where regulation around diisocyanates encourages alternatives and where clinics invest in small-form heating equipment. The casting and splinting market accommodates both incumbent fiberglass tapes and expanding thermoplastic lines, as buyers weigh per-roll cost against adjustability, patient comfort, and clinic throughput. As suppliers roll out next-generation composites and antimicrobial additives, material choice continues to diversify, which sustains competitive differentiation.

Geography Analysis

North America held 45.64% of revenue in 2025 on the strength of outpatient alignment, broad ASC penetration, and fast adoption of premium immobilization technologies that secure coverage under value-based care. The region's outpatient infrastructure rests on 12,294 ASCs in the United States by 2025 and a high share of procedures performed outside inpatient settings, which channel fracture care toward same-day stabilization options. Providers deploy custom 3D-printed splints and water-friendly liner systems to improve comfort and adherence in pediatric and adult cases. Clinic and ASC focus on speed supports uptake of low-exotherm synthetics that set quickly, enabling discharge within short observation windows. Regional consolidation among hospitals has shifted some trauma volumes while intensifying emphasis on inventory automation and coding accuracy to defend margins. Changes in professional sport injury profiles during 2025 illustrate how safety policy can influence case mix, with some lower-extremity injuries reduced under updated rules. The casting and splinting market in North America continues to emphasize supply reliability, patient comfort, and clean documentation across ambulatory pathways.

Asia-Pacific is projected to grow at an 8.31% CAGR over 2026-2031 as urbanization raises trauma incidence and as universal coverage programs expand access to stabilization beyond tertiary hubs. China's aging cohort accelerates fragility volumes, while India and Southeast Asia advance district-level access to fracture care through broader funding and referral networks. Pilots of pediatric 3D-printed splints in leading Japanese centers have reported favorable functional outcomes, reinforcing premium-tier interest where clinical acceptance aligns with customization benefits. Government support in select markets has aimed to stabilize petrochemical inputs and ensure consistent availability of resins necessary for casting tapes. In lower-resource environments across the broader region, plaster maintains a role due to cost and supply continuity, while fiberglass adoption rises with improvements in distribution. The casting and splinting market balances product portfolios across APAC to reflect both premium customization and volume-led consumables.

Europe faces dual pressures from regulatory changes and trade frictions that influence material selection and export dynamics for suppliers. New EU diisocyanate exposure limits require investments in compliance, catalyze resin reformulations, and influence tender specifications that shape product choice for casting tapes. Import tariffs on medical devices in some export markets since 2025 have nudged suppliers to adjust logistics routes or rebalance production footprints to mitigate cost exposure. In France, reimbursement policies sustain use of removable splints for common ankle injuries encountered over a lifetime, maintaining steady demand for functional solutions. Spain and Italy continue to rely on public-tender formularies that reward lowest unit costs, which preserves a role for plaster alongside lighter synthetics. European suppliers emphasize MDR certifications and sustainability credentials as differentiators while extending digital portals to streamline ordering and training for hospitals and clinics. The casting and splinting market in Europe reflects a balance of compliance-driven product evolution and steady utilization in high-volume trauma and orthopedic pathways.

- Breg (FastForm)

- DeRoyal Industries

- Dynatronics/Bird & Cronin

- Enovis/DJO (Exos, Aircast, ProCare)

- Essity (Delta-Cast, Ortho-Glass)

- Henry Schein (ECA casting tape)

- Lohmann & Rauscher (Cellona, padding)

- Medline Industries

- Orfit Industries

- Performance Health (Rolyan)

- SAM Medical (SAM Splint)

- Solventum (3M Health Care, Scotchcast)

- Stryker (Cast removal systems)

- Tynor Orthotics

- United Ortho

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging-related fragility fractures sustaining demand

- 4.2.2 Rising trauma and road injuries elevating fracture burden

- 4.2.3 Shift to outpatient/ASC and urgent care workflows

- 4.2.4 Material innovation toward lightweight fiberglass and thermoformable systems

- 4.2.5 Digital/3D scanning and additive manufacturing enable custom immobilization

- 4.2.6 Water-friendly, hygiene-focused liners improving adherence

- 4.3 Market Restraints

- 4.3.1 Regulatory exposure to diisocyanates in polyurethanes

- 4.3.2 Complications/skin issues push substitutions to functional bracing

- 4.3.3 Pricing pressure and limited differentiation in commodity SKUs

- 4.3.4 Polymer and logistics volatility impacting input costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Casting supplies & equipment

- 5.1.1.1 Casting tapes

- 5.1.1.2 Plaster casts

- 5.1.1.3 Cast cutters

- 5.1.1.4 Tools & accessories

- 5.1.2 Splinting supplies & equipment

- 5.1.2.1 Prefabricated fiberglass/plaster

- 5.1.2.2 Thermoplastic sheets/rolls

- 5.1.2.3 Aluminum foam

- 5.1.2.4 Night splints

- 5.1.1 Casting supplies & equipment

- 5.2 By Material

- 5.2.1 Fiberglass/synthetic polyurethane

- 5.2.2 Plaster of Paris

- 5.2.3 Thermoplastic (low-temp)

- 5.2.4 Polyester fabric

- 5.2.5 Aluminum (splints)

- 5.3 By Application

- 5.3.1 Fracture management

- 5.3.1.1 Upper extremity

- 5.3.1.2 Lower extremity

- 5.3.2 Acute sprains and strains

- 5.3.3 Postoperative immobilization

- 5.3.4 Pediatric fracture care

- 5.3.5 Sports injuries

- 5.3.1 Fracture management

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Orthopedic & trauma clinics

- 5.4.3 Ambulatory surgery centers

- 5.4.4 Rehab/OT/PT clinics

- 5.4.5 Home care

- 5.5 By Distribution Channel

- 5.5.1 Direct to providers

- 5.5.2 Distributor/Dealer

- 5.5.3 E-commerce

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Breg (FastForm)

- 6.3.2 DeRoyal Industries

- 6.3.3 Dynatronics/Bird & Cronin

- 6.3.4 Enovis/DJO (Exos, Aircast, ProCare)

- 6.3.5 Essity (Delta-Cast, Ortho-Glass)

- 6.3.6 Henry Schein (ECA casting tape)

- 6.3.7 Lohmann & Rauscher (Cellona, padding)

- 6.3.8 Medline Industries

- 6.3.9 Orfit Industries

- 6.3.10 Performance Health (Rolyan)

- 6.3.11 SAM Medical (SAM Splint)

- 6.3.12 Solventum (3M Health Care, Scotchcast)

- 6.3.13 Stryker (Cast removal systems)

- 6.3.14 Tynor Orthotics

- 6.3.15 United Ortho

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment