|

시장보고서

상품코드

2063559

플라스틱 헬스케어 포장 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Plastic Healthcare Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

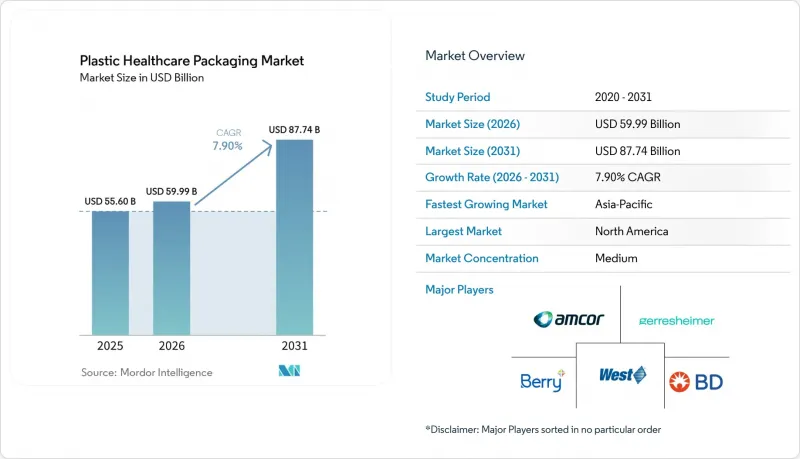

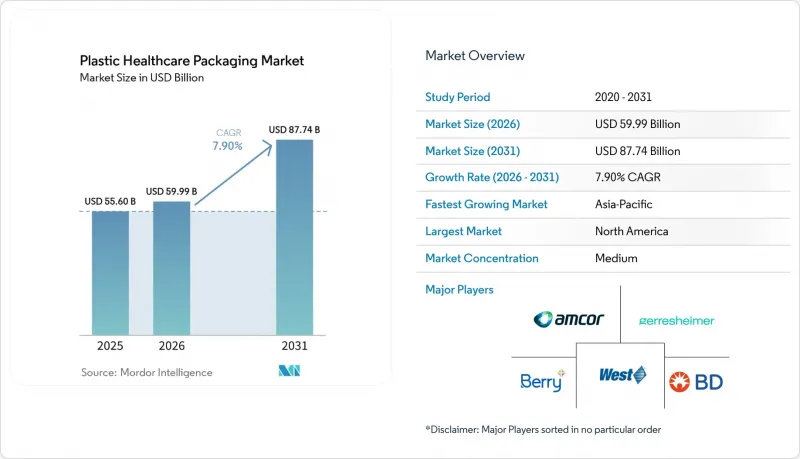

Mordor Intelligence에 의하면, 플라스틱 헬스케어 포장 시장 규모는 2025년 556억 달러로 평가되었고, 2026년 599억 9,000만 달러로 추정되고, 2031년까지 877억 4,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 7.90%를 나타낼 것으로 예측됩니다.

본 보고서는 포장 유형별(병·용기, 블리스터 팩, 바이알·앰플 등), 소재별(HDPE, LDPE/LLDPE, PP 등), 제품 유형별(1차, 2차, 3차), 기술별(사출 성형 등), 최종 사용자별(제약, 의료기기, 뉴트라슈티컬 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 플라스틱 헬스케어 포장 시장 동향 및 인사이트

바이오의약품의 급증으로 인해, 높은 차단성을 지닌 플라스틱 용기에 대한 수요가 증가하고 있습니다.

단일클론 항체, 세포 치료제, 유전자 편집 제품은 현재 임상시험용 의약품 신청의 40% 이상을 차지하고 있습니다. 이러한 치료법에는 극히 낮은 수증기 투과율이 요구되지만, 이는 COC·COP를 통해 일관되게 충족되고 있는 기준입니다. 또한, 이러한 수지는 성형 유리에 수반되는 텅스텐 용출물을 제거하여, 장기 보관 중 단백질 응집의 위험을 줄여줍니다. 2026년 1월부터 유럽약전(European Pharmacopoeia)은 COC·COP에 관한 기준을 도입하여 추출물 시험을 표준화하고, 유럽 전역의 승인 절차를 효율화할 예정입니다. West Pharmaceutical Services나 Daikyo Seiko와 같은 기업들은 이러한 규제 명확화를 활용하여, 약제와 접촉 시 99% 이상의 중성성을 보장하는 FluroTec 코팅이 적용된 엘라스토머 재질 캡의 생산을 확대되고 있습니다. 또한, 카탈렌트와 레시팜은 ISO 13485 규정을 지속적으로 준수하기 위해 자동 미립자 검사 기능을 탑재한, 분당 400유닛의 생산 능력을 갖춘 블로우-필-씰(BFS) 라인을 도입하여 생산 능력을 강화하고 있습니다. 이러한 발전은 플라스틱 헬스케어 포장 시장에서 폴리머의 중요성이 높아지고 있음을 전반적으로 뒷받침하고 있습니다.

재택의료로의 전환이 1회 투여 제제 수요를 견인하고 있습니다.

미국과 유럽의 의료보험사들은 병원 치료에 비해 30-50% 낮은 환급률을 제시함으로써 재택 정맥주사 요법을 장려하고 있습니다. 이러한 추세에 따라 제약사들은 치료제를 프리필드 주사기나 1회 투여용 블리스터에 재포장하고 있습니다. 벡톤 디킨슨(Becton Dickinson)의 ‘BD Effivax’나 게레스하이머(Geresheimer)의 ‘Gx RTF’ 주사기와 같은 솔루션은 조제 과정을 생략함으로써 간호 절차를 간소화하고, 여러 가지 처방약을 복용하는 고령 환자의 투약 오류를 대폭 줄여줍니다. FDA의 2024년 지침 초안은 사용자 친화적인 포장의 중요성을 강조하고 있으며, 위변조 방지 기능과 어린이 안전 잠금 장치가 탑재된 블리스터 팩의 도입을 가속화하고 있습니다. 이러한 추세에 따라 2031년까지 플라스틱 헬스케어 포장 시장에서는 지속적인 수요가 예상됩니다.

유럽, 새로운 규제로 일회용 플라스틱에 대한 규제를 강화

유럽의 ‘포장 및 포장 폐기물 규정(PPWR)’은 2030년까지 모든 포장을 재활용 가능하도록할 것을 의무화하고 있으며, 같은 해까지 PET의 재생재 함유율을 30%로 높일 목표를 설정하고 있습니다. 의료용 포장에는 일시적인 적용 예외가 있지만, 제조업체는 대안이 존재하지 않음을 입증해야 하며, 이로 인해 모노머 재질의 블리스터 포장으로의 전환이 촉진되고 있습니다. 독일에서는 제약사가 회수 네트워크에 자금을 출연할 의무가 있으며, 이로 인해 블리스터 팩 1개당 0.05-0.15유로의 비용이 추가되어 제네릭 의약품의 이익률을 압박하고 있습니다. 이러한 재정적 과제는 뛰어난 차단 성능을 지닌 PVC-PVDC 라미네이트의 가치 제안을 저해하며, 2030년 이후 플라스틱 헬스케어 포장 시장의 성장을 제한할 가능성이 있습니다.

부문별 분석

바이알 및 앰플 시장은 2026-2031년 연평균 성장률(CAGR) 11.8%를 기록할 전망이며, 플라스틱 헬스케어 포장 시장의 다른 모든 형태를 앞지를 것으로 전망됩니다. 제약사들은 동결건조 공정 중 층간 박리를 방지하고 콜드체인 물류 과정에서 파손을 견딜 수 있는 능력을 갖추고 있어, 고부가가치 바이오의약품용으로 COC·COP 소재 바이알을 점점 더 선호하고 있습니다. 2025년에는 고형 경구용 의약품 및 영양 보충제용 HDPE의 내화학성이 주도적인 역할을 하여, 병 및 용기가 플라스틱 헬스케어 포장 시장의 47.8%를 차지했습니다. 그러나 보험사 측이 복약 순응도를 높이기 위해 블리스터 카드로 전환하고 있는 탓에, 그 성장세는 둔화되고 있습니다. EU의 FMD 및 미국의 DSCSA에 따른 일련번호 부여 의무는 로트 단위의 추적성을 중시하고 있으며, 이는 벌크 병보다 블리스터 웹이나 단회 투여용 주사기에 더 효과적으로 통합될 수 있기 때문에 장기적인 시장 변화를 시사하고 있습니다.

폴리프로필렌은 수지 시장의 성장을 주도하고 있으며, 연평균 성장률(CAGR)은 12.5%로 전망됩니다. 121℃에서 20분간 오토클레이브 멸균을 견디고, 최대 50kGy의 감마선 조사를 견딜 수 있는 능력을 갖추고 있어 선호되는 선택지입니다. 이러한 높은 열변형 온도 덕분에 주사기 캡, 주사기 실린더, 흡입기 본체 등에서 금형을 재사용할 수 있게 되어, 컨버터의 규모의 경제가 향상됩니다. 2025년, HDPE는 저렴한 가격과 방습성 덕분에 플라스틱 헬스케어 포장 시장의 33.45%를 차지했습니다. 그러나 프랑스에서 재활용이 불가능한 PVC-PVDC 재질의 블리스터에 대한 EPR(확대 생산자 책임) 요금 등의 규제 조치로 인해, 전체 PP 구조로의 전환이 가속화되고 있으며, 이는 폴리프로필렌 시장의 성장을 더욱 뒷받침하고 있습니다.

지역별 분석

2025년, 북미는 매출의 38.67%를 차지했습니다. 이는 DSCSA(의약품 안전 추적법)의 시행 기한에 따라, 처방약 포트폴리오 전반에 걸쳐 블리스터의 일련번호 부여와 NFC 라벨 도입이 가속화된 데 기인합니다. 미국은 이 분야에서 선도적인 위치를 차지하고 있으며, 재택 주사를 권장하는 메디케어 어드밴티지의 보상 제도에 힘입고 있습니다. 한편, 캐나다는 FDA 기준을 준수하고 있어 국경을 넘는 업무의 원활한 진행에 기여하고 있습니다. 전 세계 제약사들이 아시아에서 관심을 돌리는 가운데, 멕시코의 의약품 수탁 제조 거점이 그 혜택을 누리고 있으며, 이는 현지 플라스틱 가공업체들에게 호재가 되고 있습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 9.8%를 나타낼 것으로 예측되며, 시장을 주도할 전망입니다. 중국 국가의약품감독관리국은 추출물 관련 지침을 ICH Q3E에 부합하도록 조정함으로써, 게레스하이머사의 장자강 공장에서 생산된 COC 바이알에 대한 승인을 신속히 처리했습니다. 인도에서는 론자(Lonza)의 향후 확장 계획에 따라 2026년 말까지 캡슐 쉘과 캡의 연간 생산 능력이 20억 개 증가할 전망입니다. 싱가포르를 비롯한 동남아시아 국가들은 세액 공제를 통해 제약용 클린룸에 대한 투자를 장려하고 있으며, 폴리프로필렌 주사기 및 PET 흡입기 본체의 현지 생산을 촉진하고 있습니다.

유럽에서는 엄격한 규정 준수 기준에 힘입어 2025년에도 시장 점유율이 20%대 중반을 유지했습니다. ‘위조 의약품 지침’에 따라 일련번호 부여가 광범위하게 추진된 반면, 독일의 ‘VerpackG(포장법)’에서는 모든 제품 단위별로 EPR(생산자 책임 회수) 비용 부담이 의무화됨에 따라 재활용 가능성에 대한 관심이 높아지고 있습니다. 프랑스에서는 CITEO가 PVC 블리스터에 부과하는 요금 제도로 인해, 많은 제네릭 의약품 기업들이 PP/PET 하이브리드 소재로의 전환을 추진하고 있습니다. 한편, 남유럽 시장에서는 신소재 도입 속도가 완만하지만, EU 전역의 추적성 요건을 준수하기 위해 코드 통합용 하드웨어에 대한 투자가 계속되고 있어 플라스틱 헬스케어 포장 분야 수요를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the plastic healthcare packaging market size is projected to expand from USD 55.60 billion in 2025 and USD 59.99 billion in 2026 to USD 87.74 billion by 2031, registering a CAGR of 7.90% between 2026 to 2031.

This report is Segmented by Packaging Type (Bottles & Jars, Blister Packs, Vials & Ampoules, and More), Material (HDPE, LDPE/LLDPE, PP, and More), Product Type (Primary, Secondary, Tertiary), Technology (Injection Molding, and More), End User (Pharmaceutical, Medical Device, Nutraceutical, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Value (USD).

Global Plastic Healthcare Packaging Market Trends and Insights

Biologics Boom Increasing Need for High-Barrier Plastic Containers

Monoclonal antibodies, cell therapies, and gene-editing products now represent over 40% of investigational drug filings. These modalities require ultra-low moisture vapor transmission rates, a standard consistently achieved by COC and COP. These resins also eliminate the tungsten leachables associated with molded glass, reducing the risk of protein aggregation during long-term storage. Starting January 2026, the European Pharmacopoeia will implement benchmarks for COC and COP, standardizing extractables testing and streamlining approval processes across Europe. Companies such as West Pharmaceutical Services and Daikyo Seiko are leveraging this regulatory clarity by scaling up production of FluroTec-coated elastomer closures, which ensure over 99% drug-contact neutrality. Additionally, Catalent and Recipharm are enhancing production capabilities by installing blow-fill-seal lines with a capacity of 400 units per minute, incorporating automated particulate inspection to maintain ISO 13485 compliance. These advancements collectively reinforce the growing prominence of polymers in the plastic healthcare packaging market.

Home-Healthcare Shift Fueling Demand for Unit-Dose Formats

Healthcare payers in the United States and Europe are incentivizing in-home infusion by offering reimbursements at 30-50% lower rates compared to hospital-based treatments. This trend is driving manufacturers to repackage therapies into prefilled syringes and single-dose blisters. Solutions like Becton Dickinson's BD Effivax and Gerresheimer's Gx RTF syringes simplify nursing procedures by eliminating the need for reconstitution, significantly reducing medication errors among elderly patients managing multiple prescriptions. The FDA's 2024 draft guidance emphasizes the importance of user-friendly packaging, accelerating the adoption of tamper-evident, child-resistant blisters. These developments are creating a sustained demand trajectory for the plastic healthcare packaging market through 2031.

Europe Tightens Grip on Single-Use Plastics with New Regulations

Europe's Packaging and Packaging Waste Regulation (PPWR) requires all packaging to be recyclable by 2030 and establishes a 30% recycled-content target for PET by the same year. Although medical packaging has temporary exemptions, producers must provide evidence of no viable alternatives, driving a shift toward monomer blisters. In Germany, pharmaceutical companies are now obligated to fund collection networks, adding costs of EUR 0.05-0.15 per blister pack, which reduces profit margins for generic products. These financial challenges undermine the value proposition of PVC-PVDC laminates, despite their superior barrier properties, potentially limiting growth in the plastic healthcare packaging market beyond 2030.

Other drivers and restraints analyzed in the detailed report include:

- Smart NFC-Enabled Packs for Adherence and Anti-Counterfeiting

- Adoption of Cyclic-Olefin Polymers for mRNA Vaccine Vials

- FDA's New Guidelines Heighten Scrutiny on Polymers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vials and ampoules are projected to grow at an 11.8% CAGR from 2026 to 2031, surpassing all other formats in the plastic healthcare packaging market. Pharmaceutical manufacturers increasingly prefer COC and COP vials for high-value biologics due to their ability to prevent delamination during lyophilization cycles and resist breakage during cold-chain logistics. In 2025, bottles and jars accounted for 47.8% of the plastic healthcare packaging market, driven by HDPE's chemical resilience for solid orals and nutraceuticals. However, growth is slowing as payers transition to adherence-friendly blister cards. Serialization mandates from both the EU FMD and the U.S. DSCSA emphasize batch-level traceability, which integrates more effectively into blister webs and unit-dose syringes than bulk bottles, signaling a long-term market shift.

Polypropylene is leading resin growth, with a projected CAGR of 12.5%. Its ability to endure autoclave sterilization at 121 °C for 20 minutes and withstand gamma doses up to 50 kGy makes it a preferred choice. Its high heat-deflection temperature enables the re-use of tooling across parenteral closures, syringe barrels, and inhaler bodies, enhancing economies of scale for converters. In 2025, HDPE held 33.45% of the plastic healthcare packaging market, supported by its affordability and moisture barrier properties. However, regulatory measures, such as France's EPR fee on non-recyclable PVC-PVDC blisters, are accelerating the shift toward all-PP structures, further driving polypropylene's growth.

Geography Analysis

In 2025, North America accounted for 38.67% of the revenue, driven by DSCSA deadlines that accelerated blister serialization and NFC-label adoption across prescription portfolios. The U.S. leads the region, supported by Medicare Advantage reimbursements favoring at-home injections. Meanwhile, Canada aligns closely with FDA standards, facilitating smoother cross-border operations. As global sponsors shift focus from Asia, Mexico's contract-drug manufacturing hubs are benefiting, providing a boost to local plastics converters.

Asia-Pacific is set to lead with a projected 9.8% CAGR from 2026 to 2031. China's National Medical Products Administration, aligning its extractables guidance with ICH Q3E, has expedited approvals for COC vials from Gerresheimer's Zhangjiagang facility. In India, Lonza's upcoming expansion will add two billion annual capsule shells and closures by late 2026. Southeast Asian nations, spearheaded by Singapore, are incentivizing pharma cleanroom investments with tax credits, encouraging local production of polypropylene syringes and PET inhaler bodies.

Europe maintained a share in the mid-20s percentage range in 2025, bolstered by stringent compliance norms. The Falsified Medicines Directive spurred widespread serialization, while Germany's VerpackG mandates EPR costs on every unit, shifting focus towards recyclability. In France, CITEO's fees on PVC blisters have prompted many generic firms to transition to PP/PET hybrids. While Southern European markets are slower to adopt new materials, they are still investing in code-aggregation hardware to adhere to pan-EU traceability mandates, sustaining demand in the plastic healthcare packaging sector.

- Amcor plc

- AptarGroup Inc.

- Becton Dickinson & Co.

- Berry Global Group

- Catalent

- Comar LLC

- Datwyler Holding

- Gerresheimer

- Huhtamaki Oyj

- KP Pharma (Klockner Pentaplast)

- Nolato

- Plastipak Holdings

- RPC M&H Plastics

- Schott AG (SCHOTT Pharma)

- SGD Pharma

- Tekni-Plex Inc.

- Weener Plastics

- West Pharmaceutical Services

- Wihuri Group (Winpak)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Biologics Boom Increasing Need for High-Barrier Plastic Containers

- 4.2.2 Home-Healthcare Shift Fueling Demand for Unit-Dose Formats

- 4.2.3 Cost Advantage of Plastic Versus Glass in Sterile Applications

- 4.2.4 Stricter Drug-Traceability Rules Favoring Tamper-Evident Packs

- 4.2.5 Smart NFC-Enabled Packs for Adherence & Anti-Counterfeiting

- 4.2.6 Adoption Of Cyclic-Olefin Polymers for mRNA Vaccine Vials

- 4.3 Market Restraints

- 4.3.1 Escalating Sustainability Regulations on Single-Use Plastics

- 4.3.2 Volatility in Medical-Grade Resin Supply & Prices

- 4.3.3 Glass-To-Plastic Conversion Hesitancy for Injectable Biologics

- 4.3.4 Rising Recalls Tied to Extractables & Leachables in Polymers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Packaging Type

- 5.1.1 Bottles & Jars

- 5.1.2 Blister Packs

- 5.1.3 Vials & Ampoules

- 5.1.4 Pouches & Bags

- 5.1.5 Tubes

- 5.1.6 Syringes

- 5.1.7 Others

- 5.2 By Material

- 5.2.1 HDPE

- 5.2.2 LDPE / LLDPE

- 5.2.3 PP

- 5.2.4 PVC

- 5.2.5 PET

- 5.2.6 Others

- 5.3 By Product Type

- 5.3.1 Primary Packaging

- 5.3.2 Secondary Packaging

- 5.3.3 Tertiary Packaging

- 5.4 By Technology

- 5.4.1 Injection Molding

- 5.4.2 Blow Molding

- 5.4.3 Extrusion

- 5.4.4 Thermoforming

- 5.4.5 Fill & Seal

- 5.4.6 3D Printing

- 5.5 By End User

- 5.5.1 Pharmaceutical Manufacturers

- 5.5.2 Medical Device Manufacturers

- 5.5.3 Nutraceutical & Dietary Supplement Manufacturers

- 5.5.4 Home Healthcare Providers

- 5.5.5 Diagnostic & Clinical Laboratories

- 5.5.6 Contract Packaging Organizations

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Amcor plc

- 6.3.2 AptarGroup Inc.

- 6.3.3 Becton Dickinson & Co.

- 6.3.4 Berry Global Group

- 6.3.5 Catalent Inc.

- 6.3.6 Comar LLC

- 6.3.7 Datwyler Holding

- 6.3.8 Gerresheimer AG

- 6.3.9 Huhtamaki Oyj

- 6.3.10 KP Pharma (Klockner Pentaplast)

- 6.3.11 Nolato AB

- 6.3.12 Plastipak Holdings

- 6.3.13 RPC M&H Plastics

- 6.3.14 Schott AG (SCHOTT Pharma)

- 6.3.15 SGD Pharma

- 6.3.16 Tekni-Plex Inc.

- 6.3.17 Weener Plastics

- 6.3.18 West Pharmaceutical Services

- 6.3.19 Wihuri Group (Winpak)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment