|

시장보고서

상품코드

2063567

의료용 M2M 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Healthcare M2M - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

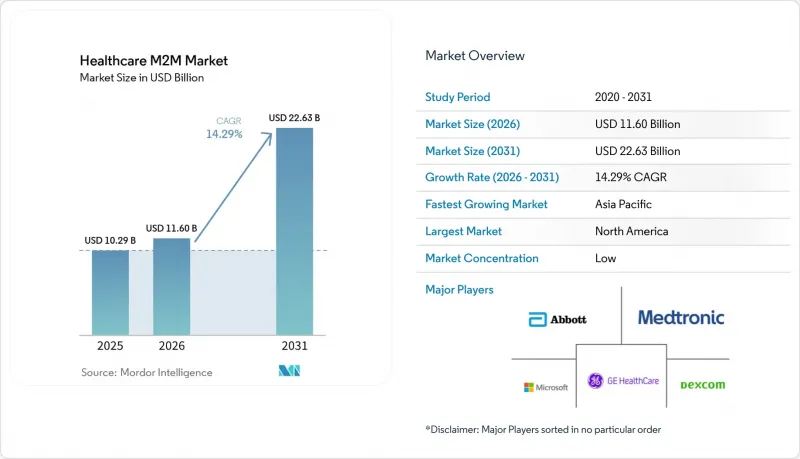

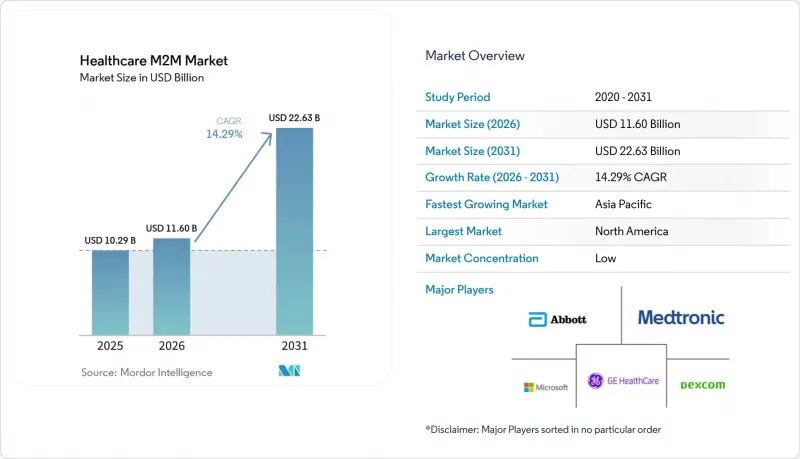

Mordor Intelligence에 의하면, 의료용 M2M 시장 규모는 2025년 102억 9,000만 달러에서 2026년에는 116억 달러로 확대되어 2026년부터 2031년까지 CAGR 14.29%로 성장을 지속하여, 2031년에는 226억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 용도(RPM, 원격의료, 입원 환자 모니터링, 임상 업무, 자산 추적, 복약 순응도), 연결 방식(셀룰러, LPWA, Wi-Fi, BLE, Zigbee, RFID), 구성 요소(디바이스, 플랫폼, 서비스), 최종 사용자(병원, 재택치료, 당일 수술센터, 진단센터), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 예측치는 달러 기준입니다.

세계 의료용 M2M 시장 동향과 인사이트

RPM/RTM 및 가상 진료에 대한 보험 적용 범위 확대

미국 CMS(의료보험 및 의료서비스 센터)의 영구 청구 코드 99453-99458 및 98975-98981에 따라, 팬데믹 기간에 시행되었던 시범 프로젝트가 의료 제공업체들에게 예측 가능한 월별 수익으로 전환되었습니다. 미국의 민간 보험사들도 이러한 코드를 채택하고 있으며, 한편 프랑스에서는 인슐린 치료를 받는 2형 당뇨병 환자를 대상으로 Dexcom ONE+에 대한 보험 급여가 이루어지고 있어, 이에 따라 다른 EU 보험사들도 웨어러블 기기의 보험 적용 범위를 재검토하고 있습니다. 인도에서는 농촌 지역의 고혈압 대책을 목적으로 ‘아유슈만 바라트’ 프로그램 하에서 RPM에 대한 보험 급여를 시범적으로 시행하고 있으며, 초기 데이터에 따르면 환자 1인당 모니터링 비용은월5달러 미만으로 나타나는 것으로 보입니다.

이러한 정책은 의료기기 수요를 촉진하고, FHIR 인터페이스를 통해 데이터를 EHR에 통합하는 플랫폼의 확산을 가속화할 것입니다. 그 결과, 북미에서는 단기적인 수요 증가가 예상되며, 아시아·태평양 지역에서도 상환 체계가 성숙되면 도입이 잇따를 전망입니다.

증가하는 만성 질환의 부담과 고령화에 따른 재택 돌봄 수요

2024년, 일본의 고령자 인구는 29.3%에 달했고, 한국은 19.2%에 달하고, 시설 요양 수용 능력에 부담이 가중되고 있습니다. 인도에는 6,200만 명의 당뇨병 환자가 있으며, 비전염성 질환이 연간 사망자의 52%를 차지하고 있습니다. 중국에서는 2025년에 현 단위에서 6,800만 건의 원격 영상 진단이 이루어졌으며, 이는 5G가 지방 진료소와 전문의를 어떻게 연결하고 있는지를 보여주고 있습니다. 배터리 수명이 10년인 저비용 LTE-M 모듈은 현재 혈당 측정기나 낙상 감지기에 기본으로 탑재되어 있어, 번거로운 전력 제약 없이 지속적인 모니터링을 가능하게 하고 있습니다. 전반적으로, 인구 동향 및 역학적 요인이 예측 기간 동안 의료용 M2M 시장의 지속적인 성장을 뒷받침할 것으로 보입니다.

확대되는 공격 대상 영역에서 발생하는 사이버 보안, 개인정보 보호 및 규정 준수 비용

2024년 체인지 헬스케어(Change Healthcare)에서 발생한 랜섬웨어 사건과 어센션 헬스(Ascension Health)의 정보 유출 사건은 M2M 게이트웨이를 통해 연결된 주입 펌프와 원격 측정 허브에 취약점이 있음을 드러냈습니다. FDA의 새로운 사이버 보안 규정에 따라 각 플랫폼의 검증 비용이 50만-200만 달러 증가했으며, 제품 출시 일정이 단축되고 있습니다.

EU에서 조만간 시행될 ‘사이버 복원력 법’은 24시간 이내의 사고 보고와 제3자 감사를 의무화하며, Quectel과 같은 모듈 공급업체에 하드웨어의 신뢰 경로(RoT) 메커니즘을 탑재하도록 강제하게 될 것입니다. 보안 예산을 확보하지 못하는 공급업체는 병원의 선정 대상에서 제외될 위험이 있으며, 이로 인해 의료용 M2M 시장의 단기적인 성장은 둔화될 것입니다.

부문별 분석

2025년에도 원격 환자 모니터링(RPM) 및 연결형 의료기기는 용도 매출의 과반수인 56.14%를 차지했습니다. 그럼에도 불구하고 원격의료·가상 진료 분야가 가장 빠르게 성장하고 있으며, 2031년까지 연평균 16.56%의 성장률이 예상됩니다. 이러한 급속한 성장에는 몇 가지 요인이 있습니다. 첫째, 미국 정부는 팬데믹 기간 중 원격의료에 관한 특별 조치를 영구화하여, 병원 및 진료소에 대해 행동 의학, 만성 질환 관리, 전문 진료 이용에 대한 확실한 보상을 보장했습니다. 둘째, 대규모 공공 플랫폼이 가상 진료가 확실한 실효성을 지닌다는 것을 입증하고 있습니다. 예를 들어, 인도의 ‘eSanjeevani’는 이미 3억 6,000만 건의 진료 기록을 보유하고 있으며, 일상적인 1차 진료 사례 10건 중 7건을 내원 예약 없이 처리하고 있습니다.

병원 내에서는 저전력 블루투스 기기 덕분에 간호사 한 명이 더 많은 병상을 관리할 수 있게 되면서, 무선 환자 모니터링이 점차 보급되고 있습니다. Philips와 호아그 병원 간의 장기적인 ‘장비 서비스(EaaS)’ 계약에서는 하드웨어, 유지보수, 업그레이드가 단일 구독 요금에 통합되어 있어, 막대한 설비 투자를 관리하기 쉬운 운영 비용으로 전환하고 있습니다. 아직 규모는 작지만, 복약 순응도 지원 도구는 각 제약사의 주목을 받고 있습니다. 레스메드사의 ‘프로펠러 헬스’ 센서는 흡입기에 부착되어, 흡입할 때마다 시간을 기록하고 그 데이터를 클라우드로 전송합니다. 이는 환자가 실제로 약을 복용하고 있음을 보험사에 입증하고자 하는 천식이나 COPD 임상시험의 후원자에게 유용한 증거가 됩니다.

기존의 이동통신(4G, LTE, 5G)은 여전히 가장 큰 점유율을 차지하고 있으며, 2025년에는 접속 관련 수익의 37.91%를 차지할 것으로 전망됩니다. 이는 스마트폰의 보급과 2G/3G 기기의 단종에 힘입은 결과입니다. 그러나 가장 눈부신 성장을 보이고 있는 것은 단거리 메시 프로토콜입니다. 재택 간병 프로그램을 통해 주택에 인체 감지 센서, 문 센서, 낙상 감지기가 도입됨에 따라, Zigbee, Z-Wave, Thread 시장은 2031년까지 연평균 15.31%의 성장률을 보일 것으로 전망됩니다. 2024년에 제정된 상호운용성 표준 ‘Matter’를 통해, 단일 허브가 여러 게이트웨이를 거치지 않고도 다양한 기기, 스마트 스피커, 조명, 혈당 측정기 등에서 데이터를 수집할 수 있게 됩니다.

고령화가 진행되고 있는 각국 정부도 이러한 움직임에 주력하고 있습니다. 일본에서는 돌봄 제공업체에게 수 초 이내에 경보를 전송하는 Thread 기반 낙상 감지 센서에 대한 보조금이 지급되고 있으며, 한국에서도 이와 유사한 우대 조치가 시행되고 있습니다. LTE-M이나 NB-IoT는 데이터 전송량이 극히 적지만, 수년 동안 배터리 수명이 필요한 저전력 트래커나 복약 관리 기기 분야에서 지속적인 성장을 이어가고 있습니다. 병상 모니터에서는 여전히 Wi-Fi가 주류를 이루고 있지만, Wi-Fi 6E의 핸드오프 시 지연이 발생할 가능성이 있기 때문에 병원에서는 생명 유지에 필수적인 통신 트래픽을 위해 전용 5G 네트워크를 도입하는 사례가 늘고 있습니다. 웨어러블 기기에서는 블루투스 저에너지(Bluetooth Low Energy)가 주류를 이루고 있으며, 새로운 LE Audio 규격을 통해 보청기로 직접 스트리밍하는 것도 가능해지면서 의료 기술과 소비자용 기술의 경계가 모호해지고 있습니다.

지역별 분석

북미는 2025년에 매출의 37.65%를 차지할 것으로 예상되며, CMS(미국 의료보험의료서비스센터)의 보상 기준 명확화와 활발한 민간 5G 시범 사업에 힘입고 있습니다. AdventHealth의 초기 성과에 따르면, 간호사의 이동 시간이 현저히 단축되었으며, 이는 설비 투자의 타당성을 입증해 주어, 유사한 시스템 도입이 잇따르고 있습니다. FDA(미국 식품의약국)의 사이버 보안 규제는 시장 진입 장벽을 높이지만, 소규모 공급업체를 도태시키고 의료용 M2M 시장 내 통합을 촉진하고 있습니다. 캐나다와 멕시코는 정책을 조율하여 지역 내 사업 전개를 간소화하는 연속적인 규제 블록을 형성하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 16.71%를 기록하며 가장 빠르게 성장하고 있는 시장으로, 중국의 300개 의료용 대규모 언어 모델(LLM)과 인도의 3억 6,000만 명을 아우르는 원격 진료 인프라가 성장을 주도하고 있습니다. 일본과 한국은 고령화 사회에 대응하기 위해 재택 모니터링에 보조금을 지원하고 있으며, 한편 아시아태평양 전체의 5G 보급률은 18%에 달하고, 지역 진료소에서 엣지 AI를 활용할 수 있게 되었습니다. 양자 AI를 활용한 심장학 임상시험에 관한 지역 간 협력은 공급업체 간의 위상을 재편할 가능성을 내포한 획기적인 기회를 시사하고 있습니다.

유럽에서는 MDR(의료기기 규정)에 따라 의무화된 시판 후 조사를 통해 이식형 원격 측정 기술이 필수 요건으로 자리 잡으면서 꾸준한 성장이 예상됩니다. 벨기에와 핀란드에서는 소규모 병원에서도 10밀리초 미만의 프라이빗 5G 구현이 가능하다는 사실이 입증되어, EU 전역으로의 도입 확대가 촉진되고 있습니다. 중동 걸프 국가들에서는 의사 부족 문제를 해결하기 위해 5G를 활용한 키오스크형 원격 의료를 도입하고 있는 반면, 남미의 진전은 아마존 강 유역의 만성 질환 다발 지역을 대상으로 한 브라질의 데이터 통신 요금제 지원 프로그램에 달려 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the healthcare m2M market size is expected to grow from USD 10.29 billion in 2025 to USD 11.60 billion in 2026 and is forecast to reach USD 22.63 billion by 2031 at 14.29% CAGR over 2026-2031.

This report is Segmented by Application (RPM, Telemedicine, Inpatient Monitoring, Clinical Operations, Asset Tracking, Medication Adherence), Connectivity (Cellular, LPWA, Wi-Fi, BLE, Zigbee, RFID), Component (Devices, Platforms, Services), End User (Hospitals, Homecare, Ascs, Diagnostic Centers), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in USD Value.

Global Healthcare M2M Market Trends and Insights

Reimbursement Expansion For RPM/RTM And Virtual Care

Permanent U.S. CMS billing codes 99453-99458, and 98975-98981 convert what were pandemic-era pilot projects into predictable monthly revenue for providers. Private U.S. insurers mirror these codes, while France reimburses Dexcom ONE+ for insulin-treated Type 2 diabetes, prompting other EU payers to re-evaluate wearable coverage. India pilots RPM reimbursement under Ayushman Bharat to target rural hypertension, and initial data suggest per-patient monitoring costs fall below USD 5 per month.

Such policies upstream device demand and accelerate platform roll-outs that aggregate data into EHRs through FHIR interfaces. The upshot is a near-term boost in North America and a pipeline of adoption across Asia-Pacific once reimbursement frameworks mature.

Rising Chronic Disease Burden And Aging At-Home Care Needs

Japan's senior population hit 29.3% in 2024, and South Korea's reached 19.2%, straining institutional care capacity. India counts 62 million diabetes patients, with non-communicable diseases causing 52% of annual deaths. China processed 68 million county-level remote imaging cases in 2025, demonstrating how 5G links rural clinics to specialists. Low-cost LTE-M modules with 10-year batteries are now standard in glucometers and fall detectors, enabling continuous surveillance without burdensome power constraints. Collectively, demographic and epidemiologic pressures will propel sustained Healthcare M2M market growth throughout the forecast horizon.

Cybersecurity, Privacy, And Compliance Costs Across Expanded Attack Surface

The 2024 Change Healthcare ransomware event and Ascension Health breach revealed vulnerabilities in infusion pumps and telemetry hubs connected via M2M gateways. New FDA cybersecurity rules add USD 0.5-2 million to each platform's validation costs and compress launch timelines.

The EU's forthcoming Cyber Resilience Act introduces 24-hour incident reporting and third-party audits, compelling module vendors like Quectel to embed hardware root-of-trust mechanisms. Vendors lacking security budgets risk exclusion from hospital formularies, tempering near-term Healthcare M2M market growth.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation Of Connected Devices, Wearables, And Cloud/AI Analytics

- Hospital Digitization for Operational Efficiency

- Interoperability And Legacy Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Remote Patient Monitoring (RPM) and connected medical devices still brought in a majority-share 56.14% of application revenue in 2025. Even so, Telemedicine & Virtual Care is set to expand the fastest, rising 16.56% annually through 2031. Several shifts explain the jump. First, Washington made pandemic telehealth waivers permanent, giving hospitals and clinics reliable reimbursement for behavioral health, chronic care, and specialty visits. Second, big public platforms prove that virtual care carries real weight. India's eSanjeevani, for example, has already logged 360 million visits, handling 7 out of 10 routine primary-care cases without requiring an office appointment.

Inside hospitals, wireless patient monitoring is spreading thanks to low-energy Bluetooth gear that lets a single nurse oversee more beds. Philips' long-term "equipment-as-a-service" deal with Hoag Hospital even bundles hardware, maintenance, and upgrades into a single subscription fee, turning hefty capital outlays into manageable operating costs. Although still small, medication-adherence tools are catching the eye of drug makers. ResMed's Propeller Health sensor clips onto an inhaler, time-stamps each puff, and pushes the data to the cloud-handy proof for asthma and COPD trial sponsors eager to show payers that patients really take their meds.

Classic cellular, 4G, LTE, and 5G, remains the largest slice, accounting for 37.91% of connectivity revenue in 2025, buoyed by smartphone ubiquity and the retirement of 2G/3G gear. Yet the brightest growth story belongs to short-range mesh protocols. Zigbee, Z-Wave, and Thread should grow 15.31% annually through 2031 as aging-in-place programs outfit homes with motion sensors, door contacts, and fall detectors. Matter, the interoperability standard finalized in 2024, lets a single hub pull data from assorted devices, smart speakers, lights, and glucose meters, without multiple gateways.

Governments with aging demographics are leaning in. Japan is subsidizing Thread-based fall sensors that alert caregivers within seconds, and South Korea has similar incentives. LTE-M and NB-IoT keep growing in low-power trackers and pill dispensers that send only a trickle of data but need batteries to last years. Wi-Fi still rules bedside monitors, but hospitals increasingly add private 5G layers for life-critical traffic because Wi-Fi 6E hand-offs can lag. Bluetooth Low Energy dominates wearables, and the new LE Audio spec even streams directly to hearing aids, blurring the line between medical and consumer tech.

Geography Analysis

North America accounted for 37.65% revenue in 2025, underpinned by CMS reimbursement clarity and dense private 5G pilots. Early outcomes from AdventHealth show notable reductions in nurse walking time, validating capital outlays and spurring copycat deployments. FDA cybersecurity rules raise entry barriers but also weed out sub-scale suppliers, nudging consolidation within the Healthcare M2M market. Canada and Mexico harmonize policies, creating a contiguous regulatory bloc that simplifies regional roll-outs.

Asia-Pacific is the fastest-growing theatre, with a 16.71% CAGR, propelled by China's 300 medical LLMs and India's 360 million-strong teleconsultation backbone. Japan and South Korea subsidize home-based monitoring to offset aging demographics, while 5G penetration across APAC reaches 18%, enabling edge AI at community clinics. Regional partnerships on quantum-AI cardiology trials hint at leapfrogging opportunities that could reorder vendor hierarchies.

Europe is growing steadily as MDR-mandated post-market surveillance makes embedded telemetry table stakes. Belgium and Finland prove sub-10 ms private 5G is feasible even in smaller hospitals, encouraging wider EU adoption. Middle-East Gulf states deploy kiosk-based telemedicine over 5G to remedy physician shortages, whereas South America's progress hinges on Brazil's subsidized data-plan program that targets Amazon basin chronic-disease hotspots.

- Abbott Laboratories

- Aeris Communications

- AT&T

- Boston Scientific

- Cisco Systems

- Dexcom

- GE Healthcare

- Insulet

- Koninklijke Philips

- KORE Wireless

- Masimo

- Medtronic

- Microsoft Corporation (Azure IoT)

- Oracle Health (Cerner)

- Orange Business

- Quectel Wireless Solutions

- Resmed

- Semtech (incl. Sierra Wireless)

- Siemens Healthineers

- Telefonica Tech

- Telit Cinterion

- u-blox

- Verizon Communications Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reimbursement Expansion For RPM/RTM And Virtual Care

- 4.2.2 Rising Chronic Disease Burden and Aging At-Home Care Needs

- 4.2.3 Proliferation of Connected Medical Devices, Wearables, And Cloud/AI Analytics

- 4.2.4 Hospital Digitization for Operational Efficiency (Patient Monitoring, Asset/Staff Tracking)

- 4.2.5 Private 5G And Edge Deployments Enabling Deterministic Clinical Connectivity

- 4.2.6 Decentralized Clinical Trials Integrating Regulated Sensor/eSource Data

- 4.3 Market Restraints

- 4.3.1 Cybersecurity, Privacy, And Compliance Costs Across an Expanded Attack Surface

- 4.3.2 Interoperability And Legacy Integration Complexity

- 4.3.3 2G/3G Sunsets Driving Costly Migrations To LTE-M/NB-Iot

- 4.3.4 Battery Longevity and Power Constraints in Medical Wearables/Implantable

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Remote Patient Monitoring (RPM) and Connected Medical Devices

- 5.1.2 Telemedicine & Virtual Care

- 5.1.3 Inpatient Wireless Patient Monitoring

- 5.1.4 Clinical Operations & Workflow Management

- 5.1.5 Asset & Staff Tracking

- 5.1.6 Medication Adherence & Connected Drug Delivery

- 5.1.7 Other Applications

- 5.2 By Connectivity Technology

- 5.2.1 Cellular (4G/LTE/5G)

- 5.2.2 LPWA (LTE-M, NB-IoT)

- 5.2.3 Wi-Fi

- 5.2.4 Bluetooth Low Energy (BLE)

- 5.2.5 Zigbee/Z-Wave/Thread

- 5.2.6 RFID/NFC

- 5.3 By Component

- 5.3.1 Medical Devices

- 5.3.2 Platforms & Software

- 5.3.3 Services

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Homecare Patients

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Diagnostic & Imaging Centers/Labs

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 Aeris Communications

- 6.3.3 AT&T Inc.

- 6.3.4 Boston Scientific Corporation

- 6.3.5 Cisco Systems, Inc.

- 6.3.6 Dexcom, Inc.

- 6.3.7 GE HealthCare

- 6.3.8 Insulet Corporation

- 6.3.9 Koninklijke Philips N.V.

- 6.3.10 KORE Wireless

- 6.3.11 Masimo Corporation

- 6.3.12 Medtronic plc

- 6.3.13 Microsoft Corporation (Azure IoT)

- 6.3.14 Oracle Health (Cerner)

- 6.3.15 Orange Business

- 6.3.16 Quectel Wireless Solutions

- 6.3.17 ResMed Inc.

- 6.3.18 Semtech (incl. Sierra Wireless)

- 6.3.19 Siemens Healthineers AG

- 6.3.20 Telefonica Tech

- 6.3.21 Telit Cinterion

- 6.3.22 u-blox

- 6.3.23 Verizon Communications Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment