|

시장보고서

상품코드

2063571

표적 치료제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Targeted Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

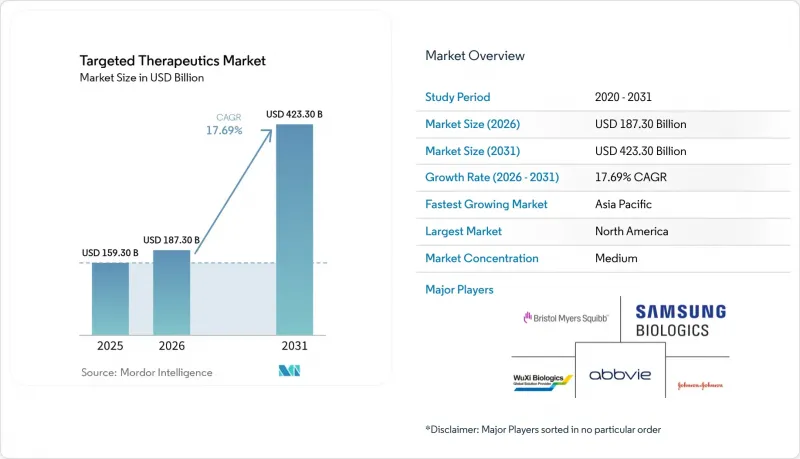

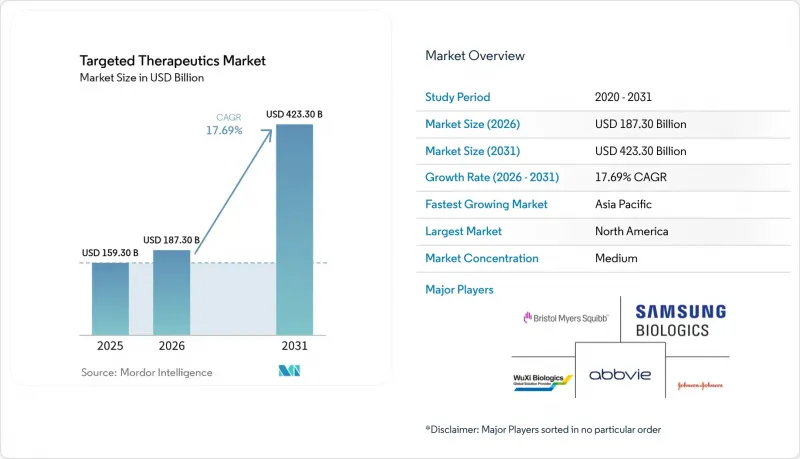

표적 치료제 시장 규모는 2025년 1,593억 달러로 평가되었습니다. 2026년에는 1,873억 달러로 확대되어 2031년까지 4,233억 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 17.69%로 성장할 전망입니다.

본 보고서는 치료법별(단일클론 항체 등), 용도별(종양학, 자가면역·염증성 질환 등), 투여 경로별(비경구 투여 등), 유통 채널별(병원 약국 등) 및 지역별(북미, 유럽, 아시아·태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 표적 치료제 시장 동향 및 인사이트

종양학 분야에서 바이오마커 기반 치료법의 적용 확대

2025년에는 동반 진단 승인 건수가 40% 급증하면서, 변이를 특정하는 소규모 임상시험이 가능해졌습니다. 이로 인해 후기 단계의 중도 탈락률이 감소하고, 환자 1인당 수익이 증가하고 있습니다. 메디케어가 2025년부터 차세대 염기서열 분석(NGS) 패널 검사 1회당 최대 3,200달러를 보상하기로 결정함에 따라, 지역 종양 클리닉에서의 도입이 가속화되었습니다. ACT Genomics가 2026년 4월, 101개 유전자·7일 소요 시간을 자랑하는 패널을 출시함에 따라 아시아태평양의 검사 격차가 줄어들었고, 해당 지역 내 환자의 적격성 기준 상한선이 높아졌습니다. 검사 범위의 확대는 결과적으로 KRAS G12C나 RET 융합 유전자 등에 대한 틈새 억제제 수요를 높여, 대상 환자 수가 적음에도 불구하고 프리미엄 가격 책정을 뒷받침하고 있습니다. 따라서 진단과 치료 간의 피드백 루프로 인해 개별 적응증이 좁아지는 반면, 표적 치료제 시장은 확대되고 있습니다.

단일클론 항체의 혁신과 수명 주기 연장

규제 당국은 2026년에 피하 투여형 아미반타맙을 승인하여 투여 시간을 5시간에서 10분 미만으로 단축하는 한편, 주사 관련 반응을 최대 80%까지 줄였습니다. 2024년 12월 출시된 피하 투여형 니볼마브나 2024년에 출시된 오클레리주맙 등 유사한 제품들의 출시는 업계 전반이 환자에게 편리한 제형으로 전환되고 있음을 보여줍니다. 일본의 의약품 및 의료기기 종합기구(PMDA)는 2025년 6월, 승인한 단일클론항체(mAb)가 100건에 달하며, 복잡한 바이오의약품에 대응할 수 있는 규제 역량을 입증했습니다. 현재, 제품 수명 연장을 위해 지속형 제제, 새로운 링커, ADC로의 전환 등이 결합되고 있으며, 선발 기업들이 바이오시밀러에 의한 시장 잠식을 대비하는 가운데, 이는 독점 기간의 연장으로 이어지고 있습니다. 그 결과, 특허 만료의 위기가 다가오고 있음에도 불구하고, mAb는 표적 치료제 시장에서 여전히 성장의 주축으로 자리 잡고 있습니다.

고가의 전문 의약품에 비해 저렴한 가격과 지불 주체에 의한 규제

메디케어의 첫 번째 IRA(인플레이션 억제법)에 따른 가격 협상 주기에서 2026년에 파트 D 대상 10개 품목의 가격 상한선이 설정되어 연방 정부가 60억 달러를 절감하는 성과를 거두었으나, 제약사의 평생 수익 곡선은 압박을 받고 있습니다. NICE(영국 국립의료기술평가기구)를 중심으로 한 유럽의 의료기술평가 기관들은 QALY(질 조정 생존년)당 5만 파운드를 초과하는 치료법을 기각하고 있으며, 차세대 억제제의 정가에 압력을 가하고 있습니다. 사전 승인 절차로 인해 치료 시작이 최대 2주 지연되고, 실제 복용 순응도가 낮아지면서, 매출이 가장 높았던 해의 매출액이 감소하고 있습니다. 한때 가격 책정의 ‘안식처’였던 신흥 시장도 중앙 조달 및 외부 참조 가격 제도로 전환되면서 차익 거래 기회가 줄어들고 있습니다. 이러한 동향들이 복합적으로 작용하여, 표적 치료제 시장의 본래라면 높은 성장세를 억제하고 있습니다.

부문별 분석

단일클론 항체는 2025년 치료법별 매출의 65.87%를 차지했으며, 이 부문의 표적 치료제 시장 규모는 2031년까지 연평균 성장률(CAGR) 24.19%로 확대될 것으로 전망됩니다. 2026년에 승인된 투여 시간 5분의 피하 투여형 아미반타맙은 바이오시밀러가 1세대 제품 시장 점유율을 서서히 잠식해 가는 상황에서도 투여 방식의 개선이 어떻게 수익성을 지킬 수 있는지를 보여주고 있습니다. ADC로의 전환은 독점권을 더욱 연장합니다. 다이이치 산쿄의 델크스테칸-링커 기술은 아스트라제네카 및 머크와 체결한 수십억 달러 규모의 계약을 뒷받침하고 있으며, 향후 로열티 수입을 이 부문의 성장 곡선에 반영하고 있습니다.

한때 정밀 종양학의 주축이었던 저분자 표적 억제제는 현재, 종양 특이적 결합과 세포 독성 페이로드를 결합한 이중 특이성 항체 및 ADC와의 크로스 플랫폼 경쟁에 직면해 있습니다. 제조 리드타임의 장기화(GMP 바이오접합 시설의 경우 18개월)는 생산 능력의 한계를 드러내는 동시에 시장 진입 장벽이 되어, 자금력이 풍부한 기존 기업들에게 단기적인 우위를 공고히 하고 있습니다. 이러한 요인들이 복합적으로 작용함에 따라, 단일클론 항체는 표적 치료제 업계의 주요 수익원으로서의 입지를 공고히 하는 동시에, 차세대 구조로의 포트폴리오 다각화를 촉진하고 있습니다.

2025년 신청 매출 중 종양학 부문이 68.90%를 차지했으며, 종양학 부문 매출이 2031년까지 연평균 성장률(CAGR) 25.67%로 확대됨에 따라 이 부문의 표적 치료제 시장 점유율은 더욱 상승할 것으로 예측됩니다. 메디케어의 동반 진단 적용 범위 확대는 주요 비용 장벽을 제거하고, 지역 암 전문의들의 차세대 염기서열 분석(NGS) 도입을 촉진하며, 치료 가능한 환자층을 확대했습니다.

종양학 이외의 분야에서는 IL-17 및 JAK 억제제의 보험 적용이 확대됨에 따라 자가면역 질환 및 염증성 질환이 그 뒤를 바짝 쫓고 있습니다. 2025년 4월 FDA가 만성 자연발진성 두드러기 치료제인 듀피센트를 승인함에 따라, 수십억 달러 규모 시장 확대의 길이 열렸습니다. 혈액 악성 종양의 경우, 림보셀타맙과 같은 BCMA를 표적으로 하는 이중 특이성 항체가 효과를 발휘하고 있으며, 이 약물은 70%의 전체 반응률을 기록하여 블록버스터가 될 가능성을 시사하고 있습니다. 한때는 주변적인 존재에 불과했던 심장 대사 질환도, PCSK9 및 Lp(a)를 표적으로 하는 siRNA를 통해 주목을 받고 있으며, 해당 파이프라인은 만성 질환에 할당된 광범위한 예산과 부합하고 있습니다. 이러한 다양화로 인해 포트폴리오의 위험은 완화되고 있지만, 표적 치료제 시장에서 종양학이 차지하는 핵심적인 위상은 여전히 유지되고 있습니다.

지역별 분석

북미는 2025년 매출의 47.30%를 차지했습니다. 이는 조기 진단이 보편화된 데 더해, 피하 투여 방식의 도입에 따라 진료 장소가 의사의 진료소로 전환된 것에 대해 보험 지급 측의 지원이 뒷받침된 결과입니다. FDA는 2025년에 15개의 획기적인 항암 치료제를 승인함으로써, 해당 지역이 혁신의 중심지로서의 위상을 공고히 했습니다. 삼성바이오로직스가 2025년 4월 생산 능력을 78만 4,000리터로 확대한 점과, 브리스톨-마이어스 스퀴브가 미국에서 5년에 걸쳐 400억 달러를 투자할 계획인 점은 장기적인 제조 거점으로서의 확고한 위상을 보여주고 있습니다.

아시아태평양은 임상시험 개시까지의 기간을 최대 9개월 단축한 중국과 일본의 규제 간소화에 힘입어, 2031년까지 연평균 22.18%의 성장률을 보일 것으로 전망됩니다. WuXi Biologics는 252개의 ADC 및 196개의 이중 특이성 항체 프로그램을 지원하고 있으며, 이 지역은 전 세계 공급망에서 없어서는 안 될 존재가 되었습니다. 인도의 Shilpa Biologics와 Syngene는 2025년에 OEB-5 바이오접합 시설을 증설할 예정이며, 한편 ACT Genomics의 101개 유전자 패널 업그레이드는 바이오마커 검사 부족 문제를 해소하고 환자의 적격성을 높이고 있습니다.

유럽에서는 EMA의 바이오시밀러 규제 간소화로 인해 승인까지 소요되는 기간이 최대 18개월 단축됨에 따라, 2025년에도 안정적인 시장 점유율을 유지했습니다. 의료기술평가(HTA)는 여전히 고가 제품 시장 출시를 제한하고 있지만, 시설 비용을 절감하는 피하 투여 제제의 보험 적용으로 인해 환자들의 접근성은 확대되고 있습니다. 중동 및 아프리카 및 남미에서는 여전히 인프라 격차가 존재하며, 대상 환자의 25% 미만이 NGS 검사를 받고 있어, 미충족 의료 수요가 높음에도 불구하고 해당 지역에서의 보급은 여전히 더딘 상태입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the targeted therapeutics market size is expected to increase from USD 159.30 billion in 2025 to USD 187.30 billion in 2026 and reach USD 423.30 billion by 2031, growing at a CAGR of 17.69% over 2026-2031.

This report is Segmented by Therapy Type (Monoclonal Antibodies, and More), Application (Oncology, Autoimmune & Inflammatory Diseases, and More), Route of Administration (Parenteral, and More), Distribution Channels (Hospital Pharmacies and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Targeted Therapeutics Market Trends and Insights

Expanding Oncology Adoption of Biomarker-Guided Regimens

Companion diagnostic approvals jumped 40% in 2025, enabling smaller, mutation-defined trials that lower late-stage attrition and boost per-patient revenue . Medicare's 2025 decision to reimburse next-generation sequencing (NGS) panels at up to USD 3,200 per test accelerated uptake among community oncology clinics. ACT Genomics' April 2026 launch of a 101-gene, seven-day-turnaround panel is narrowing Asia-Pacific's testing gaps and lifting the region's patient eligibility ceiling. Broader testing has, in turn, raised demand for niche inhibitors such as KRAS G12C and RET fusions, supporting premium pricing despite smaller cohorts. The feedback loop between diagnostics and therapeutics is therefore expanding the targeted therapeutics market even as precision narrows individual indications.

Monoclonal Antibody Innovation and Lifecycle Extensions

Regulators cleared subcutaneous amivantamab in 2026, cutting chair time from five hours to under ten minutes and slashing infusion-related reactions by up to 80%. Similar launches, including subcutaneous nivolumab in December 2024 and ocrelizumab in 2024, illustrate an industry-wide shift toward patient-friendly formats. Japan's Pharmaceuticals and Medical Devices Agency logged its 100th approved mAb in June 2025, confirming regulatory capacity to keep pace with complex biologics. Lifecycle extensions now bundle long-acting delivery, novel linkers, and ADC conversions, prolonging exclusivity windows as originators brace for biosimilar erosion. As a result, mAbs remain the growth anchor within the targeted therapeutics market despite looming patent cliffs.

Affordability and Payer Controls on High-Cost Specialty Drugs

Medicare's first IRA negotiation cycle set price ceilings for 10 Part D drugs in 2026, delivering USD 6 billion in federal savings but squeezing manufacturers' lifetime revenue curves. European health technology assessment bodies, led by NICE, reject therapies exceeding GBP 50,000 per quality-adjusted life year, pressuring list prices of next-in-class inhibitors. Prior authorization hurdles delay treatment initiation by up to two weeks, cutting real-world adherence and reducing peak-year sales. Emerging markets, once pricing havens, are moving toward central procurement and external reference pricing, narrowing the arbitrage window. Collectively, these trends temper the otherwise high-growth trajectory of the targeted therapeutics market.

Other drivers and restraints analyzed in the detailed report include:

- Label Expansions and Expedited Approvals Across Major Markets

- North America Scale with APAC Acceleration in Access and Manufacturing

- Biosimilar Erosion in Key Targeted Biologic Classes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monoclonal antibodies held 65.87% of 2025 therapy-type revenue, and the targeted therapeutics market size for this segment is projected to expand at a 24.19% CAGR through 2031. The 2026 approval of five-minute subcutaneous amivantamab exemplifies how delivery upgrades protect margins even as biosimilars nibble at first-generation assets. ADC conversions further extend exclusivity: Daiichi Sankyo's deruxtecan linker technology underpins multibillion-dollar deals with AstraZeneca and Merck, embedding future royalties into the segment's growth curve.

Small-molecule targeted inhibitors, once the workhorses of precision oncology, now face cross-platform competition from bispecifics and ADCs that combine tumor-specific binding with cytotoxic payloads. Elevated manufacturing lead times, 18 months for GMP bioconjugation suites, signal tight capacity but also erect barriers to entry, consolidating short-term advantage among cash-rich incumbents. Collectively, these forces secure monoclonal antibodies' role as the revenue backbone of the targeted therapeutics industry while encouraging portfolio diversification into next-generation constructs.

Oncology accounted for 68.90% of 2025 application revenue, and the targeted therapeutics market share for this segment is expected to climb further as oncology revenues grow at a 25.67% CAGR to 2031. Companion diagnostic coverage expansions under Medicare removed a major cost barrier, raising NGS uptake by community oncologists and expanding the treatable patient base.

Outside oncology, autoimmune and inflammatory diseases are catching up as IL-17 and JAK inhibitors gain reimbursement traction; the April 2025 FDA nod for Dupixent in chronic spontaneous urticaria opened a multi-billion-dollar market extension. Hematologic malignancies benefit from BCMA-targeted bispecifics like linvoseltamab, which posted a 70% overall response rate, hinting at blockbuster potential. Cardiometabolic disorders, once peripheral, are drawing attention through PCSK9 and Lp(a)-targeting siRNAs, aligning the pipeline with broad chronic-disease budgets. This diversification softens portfolio risk while preserving oncology's centrality to the targeted therapeutics market.

Geography Analysis

North America held 47.30% of 2025 revenue, buoyed by early diagnostic adoption and payer support for site-of-care shifts to physician offices following subcutaneous roll-outs. The FDA cleared 15 breakthrough oncology agents in 2025, reinforcing the region's innovation hub status. Samsung Biologics' April 2025 expansion to 784,000 liters and Bristol Myers Squibb's USD 40 billion, five-year U.S. investment signal long-term manufacturing anchorage.

Asia-Pacific is forecast to grow at 22.18% through 2031, powered by Chinese and Japanese regulatory streamlining that cut clinical start-up times by up to nine months. WuXi Biologics supports 252 ADC and 196 bispecific programs, making the region indispensable for global supply. India's Shilpa Biologics and Syngene added OEB-5 bioconjugation suites in 2025, while ACT Genomics' 101-gene panel upgrade addresses biomarker testing deficits, boosting patient eligibility.

Europe maintained a steady share in 2025 due to EMA biosimilar streamlining that shortened approval timelines by up to 18 months. Health technology assessments continue to constrain high-priced launches, yet reimbursement of subcutaneous formats that trim facility costs has broadened patient access. Infrastructure gaps persist in the Middle East & Africa and South America, where fewer than 25% of eligible patients receive NGS, keeping regional uptake muted despite high unmet need.

- Abbvie

- Amgen

- Astellas Pharma

- AstraZeneca

- Bayer

- BeiGene, Ltd.

- Bristol-Myers Squibb

- Daiichi Sankyo

- Eisai

- Eli Lilly and Company

- Exelixis, Inc.

- Roche

- Genmab

- GlaxoSmithKline

- Incyte

- Johnson & Johnson

- Merck

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Samsung Group

- Sanofi

- Takeda Pharmaceuticals

- Wuxi Biologics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Oncology Adoption of Biomarker-Guided Regimens

- 4.2.2 Monoclonal Antibody Innovation and Lifecycle Extensions

- 4.2.3 Label Expansions and Expedited Approvals Across Major Markets

- 4.2.4 North America Scale with APAC Acceleration in Access and Manufacturing

- 4.2.5 ADC Platform and Deal Momentum, Broadening Targeted Options

- 4.2.6 Shift To Subcutaneous/Long-Acting Formats Enabling Site-Of-Care Change

- 4.3 Market Restraints

- 4.3.1 Affordability and Payer Controls on High-Cost Specialty Drugs

- 4.3.2 Biosimilar Erosion in Key Targeted Biologic Classes

- 4.3.3 Capacity And CMC Constraints for Complex Biologics

- 4.3.4 Uneven Biomarker Testing and Access Limiting Addressable Populations

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Type

- 5.1.1 Monoclonal Antibodies

- 5.1.2 Small-Molecule Targeted Inhibitors

- 5.1.3 Antibody-Drug Conjugates

- 5.1.4 Bispecific And Multispecific Antibodies

- 5.1.5 RNA-Targeted Therapeutics

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Autoimmune & Inflammatory Diseases

- 5.2.3 Hematologic Malignancies

- 5.2.4 Respiratory & Allergy

- 5.2.5 Hematology

- 5.2.6 Cardiovascular & Metabolic

- 5.2.7 Rare Genetic & Metabolic Disorders

- 5.2.8 Infectious Diseases

- 5.3 By Route of Administration

- 5.3.1 Parenteral

- 5.3.2 Oral

- 5.3.3 Others

- 5.4 By Distribution Channels

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 Astellas Pharma Inc.

- 6.3.4 AstraZeneca plc

- 6.3.5 Bayer AG

- 6.3.6 BeiGene, Ltd.

- 6.3.7 Bristol Myers Squibb Company

- 6.3.8 Daiichi Sankyo Company, Limited

- 6.3.9 Eisai Co., Ltd.

- 6.3.10 Eli Lilly and Company

- 6.3.11 Exelixis, Inc.

- 6.3.12 F. Hoffmann-La Roche Ltd

- 6.3.13 Genmab A/S

- 6.3.14 GSK plc

- 6.3.15 Incyte Corporation

- 6.3.16 Johnson & Johnson

- 6.3.17 Merck & Co., Inc.

- 6.3.18 Novartis AG

- 6.3.19 Pfizer Inc.

- 6.3.20 Regeneron Pharmaceuticals, Inc.

- 6.3.21 Samsung Biologics

- 6.3.22 Sanofi

- 6.3.23 Takeda Pharmaceutical Co. Ltd.

- 6.3.24 WuXi Biologics

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment