|

시장보고서

상품코드

2063573

마이크로서저리 로봇 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Microsurgery Robot - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

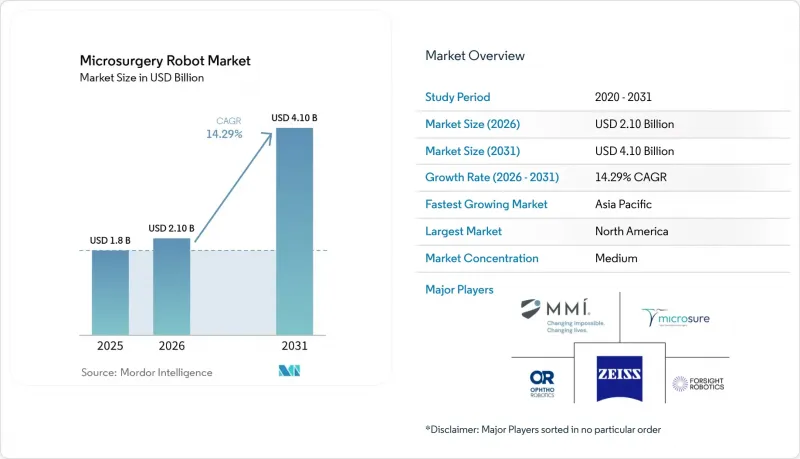

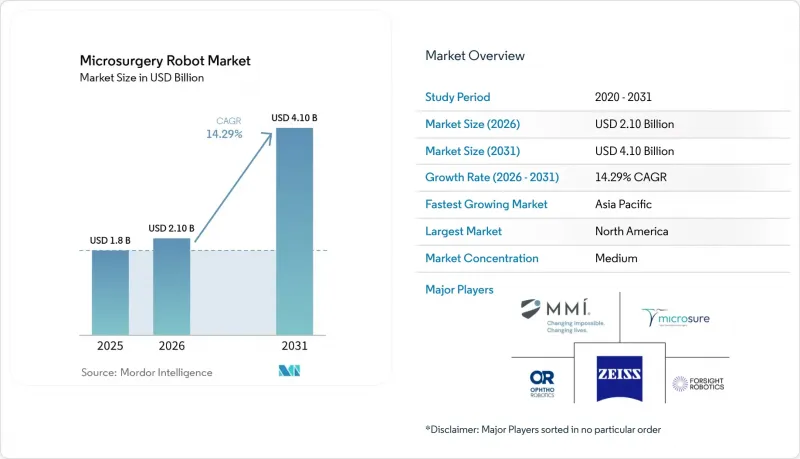

마이크로서저리 로봇 시장 규모는 2025년 18억 달러로 평가되었습니다. 2026년 21억 달러에서 2031년까지 41억 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 14.29%를 나타낼 것으로 예측됩니다.

본 보고서는 임상 용도(종양학, 재건외과, 안과, 이비인후과, 기타), 기술(원격 조작형, 공동 조작형, 반자율형), 최종 사용자(대학병원, 전문병원, 당일 수술센터, 지역 병원), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 마이크로서저리 로봇 시장 동향 및 인사이트

림프부종의 부담 증가와 림프관 및 미세혈관 재건에 대한 수요

림프부종은 전 세계적으로 2억 5,000만 명에게 영향을 미치고 있으며, 이 중 1,000만 명은 미국에 거주하고 있습니다. 림프정맥 문합술은 1년 후 사지의 부피를 14.26% 감소시켜, 환자의 거의 절반이 압박복 착용을 단계적으로 줄일 수 있게 해줍니다. 손의 움직임을 10 : 1 또는 20 : 1로 확대하는 로봇을 통해 일반 성형외과 의사도 펠로우십 수련을 받은 의사와 동등한 수술 성과를 거둘 수 있게 되었으며, 숙련도에 도달하기까지 필요한 사례 수는 수동 수술의 경우 40건인 반면, 로봇 수술의 경우 15건으로 충분합니다. 생존 기간이 연장됨에 따라 유방암 관련 림프부종의 발생률이 증가하고 있는 점도 수요를 뒷받침하고 있습니다.

CE 마크를 획득한 전용 마이크로서저리 로봇 : 서브mm 단위의 문합 시 동작 스케일링 및 진동 필터링 구현

Symani와 MUSA가 2021년부터 2022년에 걸쳐 CE 마크를 획득함에 따라, 유럽의 의료 기관들은 3년간의 선점 우위를 확보했으며, 2025년까지 900건 이상의 임상 사례를 기록했습니다. 모션 스케일링은 손의 10mm 움직임을 기구의 1mm 움직임으로 변환하고, 칼만 필터는 8Hz 이상의 진동 주파수를 제거함으로써 위치 편차를 최대 90%까지 줄여줍니다. 이 로봇들을 자율형이 아닌 보조형 기기로 분류함으로써, 유럽의 보험사와의 보험금 지급 협상이 원활하게 진행되었습니다.

초기 단계 적응증에 따른 높은 도입 비용, 설치 시간 및 불투명한 보험 급여 절차

이 시스템의 가격은 50만 달러에서 250만 달러이며, 연간 10만 달러에 육박하는 서비스 계약비는 포함되어 있지 않습니다. Symani의 설치에는 최대 1시간이 소요되며, 이로 인해 하루 수술 건수가 1건 줄어들게 되어 당일 수술(ASC)의 수익성이 저하됩니다. CPT 코드는 림프관 수술을 포함하고 있지만, 로봇 기술에 대한 가산점이 제공되지 않기 때문에 병원은 차액을 자체 부담하고 있으며, 이비인후과 및 신경혈관 적응증에 대해서는 해당 코드가 전혀 존재하지 않습니다.

부문별 분석

2025년 마이크로서저리 로봇 시장 점유율에서 종양학 수술이 23.18%를 차지했습니다. 이는 여러 개의 초미세 외과적 문합이 필요한 복잡한 자유 피판 재건술을 반영한 것입니다. 재건 수술 시장은 연평균 성장률(CAGR) 16.56%로 확대될 것으로 예상되며, 림프부종 환자 수가 증가함에 따라 이 부문의 마이크로서저리 로봇 시장 규모를 끌어올릴 것으로 전망됩니다.

병원 측은 재건 수술의 적응증을 ‘ 수요의 원동력’으로 보고 있습니다. 이는 유방암 생존자 한 명 한 명이 림프정맥 우회술의 장기적인 대상이 되기 때문입니다. 한편, 안과 분야에서의 도입은 명확한 임상적 유효성이 입증된 최초의 안과용 유전자 치료제 투여를 통해 가속화되고 있습니다. 심혈관 및 소화기 분야에서의 도입은 혈관 직경이 서브mm 단위의 정밀도를 필요로 하지 않기 때문에 여전히 저조한 상태입니다.

지역별 분석

북미는 2025년 매출의 45.18%를 차지했습니다. 조기 CPT 코드 지정과 2024년 4월 Symani의 FDA 승인이 상업적 모멘텀을 가져왔으며, 현재는 민간 보험사들도 로봇을 이용한 림프정맥 문합술에 대해 사례별로 승인하고 있습니다. 캐나다의 단일 지불자 제도에서는 자본 예산이 수년 후까지 고정되어 있어 도입 속도가 완만하지만, 멕시코의 민간 병원은 수술 비용을 40% 낮춤으로써 미국 환자들을 유치하고 있습니다.

아시아태평양은 중국의 3차 의료기관이 2025년 상반기에 74대(7억 위안, 약 9,600만 달러 상당)를 구매함에 따라 연평균 성장률(CAGR) 17.77%로 가장 빠른 성장세를 보일 것으로 전망됩니다. 일본에서는 학술적 활용이 활발하여, 2025년 중반까지 로봇 보조 췌두십이지장 절제술이 162건 시행되었으나, 국가 보험 적용 여부는 여전히 검토 중입니다. 한국과 호주에서는 특정 대상을 대상으로 한 보조금이나 최근의 규제 승인으로 인해 틈새 수요가 창출되고 있지만, 지방으로의 확산이 이루어지지 않고 있어 주요 도시 이외의 지역에서의 이용은 제한적입니다.

유럽에서는 CE 마크 획득으로 인해 조기 도입이 가능해졌기 때문에 2025년 매출에서 큰 비중을 차지했습니다. 독일, 영국, 프랑스는 해당 지역 내 도입 대수에서 상당한 점유율을 차지하고 있지만, 병원 운영의 분산화와 NHS의 예산 긴축으로 인해 성장세는 완만해지고 있습니다. MDR에 따른 시판 후 조사로 인해 중소기업의 진입 비용은 상승하고 있지만, 독일에서는 로봇 수술과 수동 림프절 수술에 대한 보험 급여가 동일하기 때문에 병원의 경제성은 안정적입니다. 중동 및 아프리카 및 남미 지역의 도입률은 보험 환급 체계가 제한적이기 때문에 여전히 낮은 수준을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the microsurgery robot market size is projected to expand from USD 1.8 billion in 2025 and USD 2.10 billion in 2026 to USD 4.10 billion by 2031, registering a CAGR of 14.29% between 2026 to 2031.

This report is Segmented by Clinical Application (Oncology, Reconstructive, Ophthalmology, ENT, Other), Technology (Teleoperated, Co-Manipulated, Semi-Autonomous), End-User (Academic Centers, Specialty Hospitals, Ascs, Community Hospitals), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

Global Microsurgery Robot Market Trends and Insights

Rising Lymphedema Burden and Demand for Lymphatic and Microvascular Reconstruction

Lymphedema affects 250 million people worldwide, including 10 million in the United States . Lymphovenous anastomosis reduces limb volume by 14.26% at one year and lets nearly half of the patients taper compression garments. Robots that scale hand motion 10:1 or 20:1 permit general plastic surgeons to match fellowship-trained outcomes, and proficiency arrives in 15 robotic cases versus 40 manual cases. Demand is reinforced by the incidence of breast cancer-related lymphedema as survivorship lengthens.

CE-Marked Purpose-Built Microsurgery Robots Enabling Motion Scaling and Tremor Filtration in Sub-Millimeter Anastomoses

European centers gained a three-year head start after Symani and MUSA secured CE marks in 2021-2022, logging more than 900 clinical cases by 2025. Motion scaling converts a 10-mm hand move into a 1-mm instrument motion, and Kalman filters delete tremor frequencies above 8 Hz, cutting positional variance by up to 90% . Classifying these robots as assistive rather than autonomous devices eased reimbursement talks with European payers.

High Capital Cost, Setup Time, and Uncertain Reimbursement Pathways in Early-Stage Indications

Systems list from USD 500,000 to USD 2.5 million, excluding yearly service contracts that approach USD 100,000. Symani setup consumes up to one hour, cutting a daily block by one case and diluting ASC economics. CPT codes cover lymphatic work yet offer no uplift for robotic technique, so hospitals self-fund the delta while ENT and neurovascular indications lack any code.

Other drivers and restraints analyzed in the detailed report include:

- Clinical Validation in Ophthalmic and ENT Microsurgery Expanding Addressable Procedures

- Digitization of Open Microsurgery Workflows

- Regulatory Stringency and Need for Large-Scale, Multi-Center Outcomes Evidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oncology procedures held 23.18% of the 2025 microsurgery robot market share, reflecting complex free-flap reconstruction that demands multiple supermicrosurgical anastomoses. Reconstructive work is forecast to expand at a 16.56% CAGR, lifting the microsurgery robot market size for this segment as lymphedema cases climb.

Hospitals view reconstructive indications as a volume engine because each breast cancer survivor represents a long-term candidate for lymphovenous bypass. Meanwhile, ophthalmology adoption is accelerating through gene-therapy delivery, the first ophthalmic use case to prove clear clinical benefit. Cardiovascular and gastrointestinal adoption remains muted because their vessel diameters do not require sub-millimeter accuracy.

Geography Analysis

North America held 45.18% of 2025 revenue. Early CPT coding and the April 2024 FDA clearance of Symani created commercial momentum, and private insurers now approve lymphovenous anastomosis when performed robotically on a case-by-case basis. Canada's single-payer system moves more slowly because capital budgets are locked years ahead, while Mexico's private hospitals lure U.S. patients at 40% lower procedure cost.

Asia-Pacific is forecast to expand at the fastest 17.77% CAGR as Chinese tertiary hospitals bought 74 units in the first half of 2025, worth more than 700 million RMB or about USD 96 million. Japan shows strong academic use, with 162 robotic pancreatoduodenectomy cases by mid-2025, but national reimbursement remains under review. South Korea and Australia provide targeted subsidies and recent regulatory clearances that open niche demand, although rural dispersion limits utilization outside major cities.

Europe contributed a significant share of the 2025 turnover after CE marks allowed earlier adoption. Germany, the United Kingdom, and France account for a notable share of regional installs, yet decentralized hospital governance and NHS budget tightening moderate growth. Post-market surveillance under MDR raises the cost of entry for smaller firms, though Germany's reimbursement parity between robotic and manual lymphatic surgery smooths hospital economics. Adoption in the Middle East, Africa, and South America remains less percentage due to limited reimbursement frameworks.

- AcuSurgical

- Bionaut Labs

- Brain Lab

- Carl Zeiss

- CASCINATION AG

- Collin Medical

- ForSight Robotics

- High Tech Campus Eindhoven

- iotaMotion

- Keranova

- LENSAR Inc.

- Medical Microinstruments, Inc.

- MicroSure B.V.

- NDR Medical Technology

- Ophthorobotics AG

- XACT Robotics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Lymphedema Burden and Demand for Lymphatic and Microvascular Reconstruction

- 4.2.2 CE-Marked Purpose-Built Microsurgery Robots Enabling Motion Scaling and Tremor Filtration in Sub-Millimeter Anastomoses

- 4.2.3 Clinical Validation in Ophthalmic and ENT Microsurgery, Expanding Addressable Procedures

- 4.2.4 Digitization Of Open Microsurgery Workflows

- 4.2.5 Surgeons' Skill Bottleneck in Super microsurgery Accelerating Hospitals' Shift to Robotic Platforms

- 4.2.6 Gene/Cell Therapy Delivery Use-Cases Requiring Robotic Precision

- 4.3 Market Restraints

- 4.3.1 High Capital Cost, Setup Time, And Uncertain Reimbursement Pathways in Early-Stage Indications

- 4.3.2 Regulatory Stringency and Need for Large-Scale, Multi-Center Outcomes Evidence

- 4.3.3 Limited Instrument Ecosystems and Cross-Specialty Workflow Integration

- 4.3.4 Credentialing/Training Standardization Gaps Slow Multi-Site Scale-Up

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Clinical Application

- 5.1.1 Oncology surgery

- 5.1.2 Urology surgery

- 5.1.3 Obstetrics and gynecology surgery

- 5.1.4 Micro anastomosis

- 5.1.5 Reconstructive surgery

- 5.1.6 ENT surgery

- 5.1.7 Gastrointestinal surgery

- 5.1.8 Cardiovascular surgery

- 5.1.9 Neurovascular surgery

- 5.1.10 Ophthalmology surgery

- 5.1.11 Other applications

- 5.2 By Technology

- 5.2.1 Teleoperated multi-arm microsurgical systems

- 5.2.2 Co-manipulated/handheld robotic assist systems

- 5.2.3 Semi-autonomous image-guided micro-robots

- 5.3 By End-user

- 5.3.1 Academic medical centers

- 5.3.2 Specialty hospitals

- 5.3.3 Ambulatory surgical centers

- 5.3.4 Community / General hospitals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 AcuSurgical

- 6.3.2 Bionaut Labs

- 6.3.3 Brainlab

- 6.3.4 Carl Zeiss Meditec AG

- 6.3.5 CASCINATION AG

- 6.3.6 Collin Medical

- 6.3.7 ForSight Robotics

- 6.3.8 High Tech Campus Eindhoven

- 6.3.9 iotaMotion Inc.

- 6.3.10 Keranova

- 6.3.11 LENSAR Inc.

- 6.3.12 Medical Microinstruments, Inc.

- 6.3.13 MicroSure B.V.

- 6.3.14 NDR Medical Technology

- 6.3.15 Ophthorobotics AG

- 6.3.16 XACT Robotics

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment