|

시장보고서

상품코드

2063580

외래 종양학 주입 치료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Outpatient Oncology Infusion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

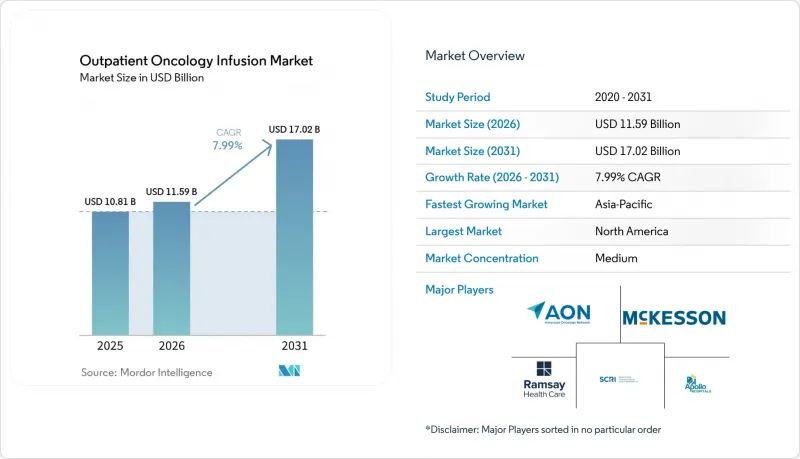

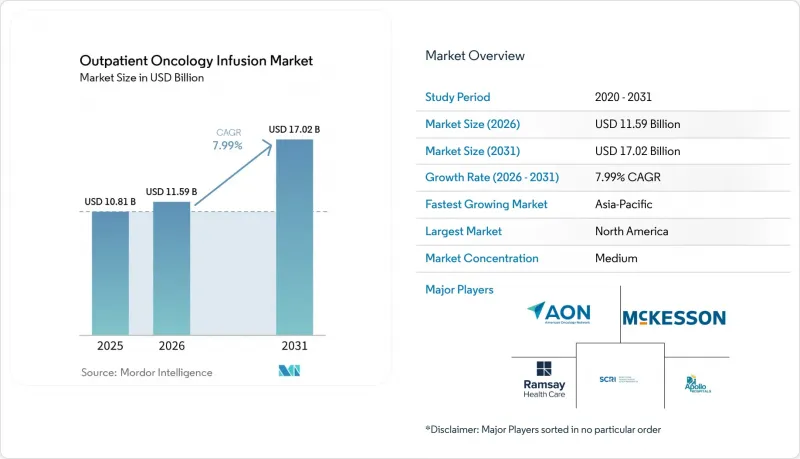

외래 종양학 주입 치료 시장 규모는 2025년 108억 1,000만 달러로 평가되었습니다. 2026년에는 115억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 7.99%로 성장을 지속하여, 2031년에는 170억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 의료 제공 환경(병원 외래, 진료소/지역 암 진료 등), 치료법(세포독성 화학요법 등), 종양 유형(유방암, 폐암, 대장암 등) 및 지역(북미, 유럽, 아시아·태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계의 외래 종양학 주입 치료 시장 동향 및 인사이트

정맥 주사형 면역요법 및 생물학적 제제의 급속한 보급

항체-약물 복합체(ADC)를 뒷받침하는 규제상의 움직임에 따라, 정기적인 정맥 내 투여 주기, 투여 전 사전 투약 및 투여 후 모니터링이 필요한 적응증이 추가되면서, 1회 내원당 평균 치료 시간이 늘어남에 따라 수액 치료 수요가 완전히 달라졌습니다. 유방암에 대한 다토포타맙-델크스테칸의 승인 절차와 그 후 폐암으로의 적응증 확대는 의료진이 기존의 세포독성 요법과는 다른 ADC 전용 프로토콜을 실제 진료에 적용함에 따라 이러한 추세를 더욱 강화하고 있습니다. 2026년에는 이피나타맙-델크스테칸이 진행성 소세포폐암에 대해 우선심사(Priority Review)를 받았습니다. 이는 승인될 경우 점적 투여 횟수가 더욱 증가할 것임을 시사하며, 면역 관련 독성 모니터링을 통해 상황이 더욱 복잡해질 것입니다. 따라서 외래 종양학 주입 치료 시장의 성장은 신약 승인뿐만 아니라, 면역요법에 따른 정맥 주입 및 관찰 기간 연장에 힘입어 뒷받침되고 있습니다. 이러한 추세는 환자 경험을 유지하면서 사전 투약 절차와 이상반응 모니터링을 표준화하고 있는 의료기관에 유리하게 작용합니다. 또한, 예약 취소나 대기 시간을 늘리지 않으면서도 의자 점유 시간을 더 길게 할 수 있는 확장성 있는 예약 모델에 대한 필요성도 높아지고 있습니다.

비용, 접근성, 환자 경험의 관점에서 외래 및 통원 치료로의 전환

CMS는 예외로 인정된 캠퍼스 외 의료 제공 기관에서의 약물 투여에 대해 병원 외래 진료비의 상당 부분을 적용하는 ‘시설 중립형 지급 조치’를 최종 결정했습니다. 이에 따라, 과거 정책 변경 이후 해당 시설로 이전된 서비스에 대한 상환액이 삭감됩니다. 이러한 규정 변경에 따라, 총 비용 절감, 환자의 이동 시간 단축, 일정 관리 효율화가 가능한 외래 또는 의료기관 간 협력 시설에서 적절한 화학요법 및 생물학적 제제의 정맥 주입을 실시하려는 동기가 높아지고 있습니다. 2026년에 외래 화학요법 및 종양 수액 치료 시장이 점차 확대됨에 따라, 여러 의료 기관을 운영하는 의료 제공업체들은 수익성을 확보하고 환자 접근성을 유지하기 위해 중증도 및 자원 집약도에 따라 서비스 구성을 조정하고 있습니다. 환자와 의뢰 의사는 안전성, 적시적인 치료 시작, 일관된 진료팀을 모두 갖춘 의료기관을 선호하는 경향이 있으며, 이는 유지 요법 및 정기적인 생물학적 제제 투여 분야에서 지역 의료기관의 성장을 뒷받침하고 있습니다. 그 결과, 예측 가능한 진료 경험, 투명한 비용 구조, 그리고 보험사와의 협력을 바탕으로 한 치료 계획을 제공하는 의료 기관으로 환자 수가 점차 재분배되고 있습니다.

상환 압박(시설 중립화, 340B 시정 조치)이 이익률을 압박하고 있습니다.

사이트 중립 정책에 따라, 예외로 인정된 병원 외부 부서에서의 약물 투여에 대해서는 현재 병원 외래 진료비의 상당액이 지급되고 있습니다. 이로 인해 지난 몇 년간 점적 요법 서비스 시장 점유율을 확대해 온 시설들의 보상액이 직접적으로 감소하고 있습니다. 또한 CMS는 비약제 OPPS 갱신에 대해 340B와 관련된 다년간의 회수 조정을 실시하고 있으며, 이로 인해 병원의 예산은 더욱 빠듯해지고, 수액 주입용 의자나 약국에 대한 설비 투자 장벽이 높아지고 있습니다. 의료기관 단체는 일률적인 시설 중립 요금 체계에서는 특히 대학병원이나 안전망 시스템이 담당하는 중증 환자층을 대상으로 한 복잡한 종양학적 점적 요법을 뒷받침하기 위해 필요한 대기 체계나 집중적인 인력 배치가 충분히 고려되지 않았다고 지적하고 있습니다. 이러한 복합적인 영향으로 인해, 보다 선별적인 사업 확대, 중증도에 따른 서비스 구성의 최적화, 그리고 낭비를 최소화하는 예약 관리 및 약국 업무 흐름의 신속한 도입이 진행되고 있습니다. 외래 종양학 주입 치료 시장에서 이러한 압박은 높은 시간 준수율과 예측 가능한 비용을 유지할 수 있는 탄탄한 운영 규율과 보험사와의 협력 체계를 갖춘 의료기관에 유리하게 작용합니다. 중기적으로는 정책 환경에 따라 비용 대비 효과가 높은 시설로의 환자 유입이 증가하고, 고비용 시설의 성장이 억제될 것으로 예측됩니다.

부문별 분석

2025년 기준, 병원 외래 진료 부문은 통합된 진단, 수술 조정, 그리고 복잡한 생물학적 제제 및 세포 치료에 필요한 거버넌스의 지원을 받아 외래 종양학 주입 치료 시장의 53.23%를 차지했습니다. 한편, 보험사의 시설 중립적 정책이 저비용 환경을 뒷받침하는 가운데, 독립형 외래 수액 센터는 2031년까지 연평균 성장률(CAGR) 9.01%로 성장할 것으로 전망됩니다. 이러한 구성 비율의 차이는 병원이 중증도가 더 높은 환자나 임상시험의 업무 흐름을 관리할 수 있는 능력을 반영하는 반면, 외래 센터는 예측 가능한 일정 범위에 부합하는 유지 요법이나 치료 프로토콜에 따른 생물학적 제제에 중점을 두고 있음을 보여줍니다. 의료 시스템이 품질과 이익률을 유지하기 위해 중증도에 따라 진료과를 재편하고, 환자 선별을 표준화하고 있는 만큼, 외래 종양학 주입 치료 시장은 이러한 구조를 중심으로 재편이 진행되고 있습니다. 보험사의 정책 또한 특정 외래 부문에서의 약물 투여에 대한 지급 수준을 낮춤으로써 이러한 추세를 뒷받침하고 있으며, 이로 인해 간접비가 낮고 처리 능력이 높은 시설로 환자 수가 이동하고 있습니다.

환자의 선호도 역시 중요한 요소입니다. 지역 의료시설에서는 통원 거리가 짧고, 치료 시작이 빠르며, 일관된 간호팀의 서비스를 받을 수 있는 경우가 많기 때문입니다. 한편, 병원 내 각 부서는 치료의 신속한 상급 의뢰, 이상반응 관리, 그리고 동일 캠퍼스 내 다학제적 전문 지식 활용이라는 측면에서 여전히 필수적인 역할을 수행하고 있습니다. 2026년에는 이러한 균형이 제로섬의 변화가 아니라, 안전성과 낮은 총비용을 모두 갖춘 센터로 적절한 증례를 선별하여 재분배하는 형태가 될 것입니다. 두 시설 모두에서 진료를 실시하는 의료기관은 각 치료법을 적절한 시설에 배정하기 위해 일원화된 분류 및 예약 모델을 채택하고 있습니다.

예측 기간 동안, 병원 외래 진료 부서는 세포 치료나 빈번한 검사실에서의 투여량 조정이 필요한 정맥 주사 요법 등 복잡한 치료 프로토콜을 계속해서 담당할 것으로 예측됩니다. 이러한 치료에서는 병설된 약국, 응급 대응 능력, 그리고 전문 분야의 상담이 중요합니다. 한편, 외래 수액 치료 센터는 표준화된 치료 요법과 효율적인 치료 의자 회전율을 강점으로 삼아, 보험 지급 측의 비용 효율성을 뒷받침함으로써, 보다 광범위한 외래 화학요법 및 종양 수액 치료 시장보다 더 높은 성장률을 보일 것으로 전망됩니다.

외래 화학요법 및 종양 주입 치료 시장 규모는 각 센터가 사전 투약 절차를 개선하고, 예측에 기반한 일정 관리를 도입하여 주간 피크 시간을 평준화하며, 생물학적 제제의 점적 관찰 시간을 엄격하게 관리함에 따라 이러한 구성 변화를 반영하게 될 것입니다. 특정 외부 병원을 기반으로 한 서비스에 대한 지급액을 낮추는 정책 조치로 인해, 1회 수액 투여 시작당 비용과 시간 준수 성과에 대한 관심이 높아지고 있습니다. 인증 기준과 품질 관리 프로그램은 고위험 치료를 관리하는 병원 제휴 센터에게 여전히 중요한 차별화 요소로 작용하고 있습니다. 병원과 지역 의료 거점을 결합한 네트워크 사업자는 외래 화학요법 및 종양 수액 치료 시장에서의 점유율을 유지하기 위해, 데이터에 기반한 일정 관리, 일관된 인력 배치, 그리고 환자 지원 서비스를 우선시하고 있습니다.

지역별 분석

북미는 2025년, 성숙한 종양학 네트워크, 첨단 생물학적 제제의 광범위한 이용 가능성, 그리고 대규모 치료 경로를 따라 운영할 수 있도록 지원하는 보험사와의 계약을 바탕으로 외래 종양학 주입 치료 시장의 43.24%를 차지했습니다. 2026년의 정책 환경은 시설 중립적인 지급 조치와 지속적인 품질 보고를 통해 비용 관리를 강화하고 있으며, 이를 통해 서비스 구성의 최적화와 예측 기반 스케줄링의 보급이 촉진되고 있습니다. 다중 사이트 모델을 운영하는 의료 기관은 복잡한 치료 요법에 대한 병원 차원의 감독과 유지 요법을 위한 지역 시설 이용을 양립시키고 있습니다. 중증도가 높은 환자를 진료하는 리더에게 있어 지속적인 인증, 규정 준수 및 직원 교육은 여전히 필수적인 요건입니다. 지불자가 가치를 중시하는 가운데, 치료 경로 준수와 사전 승인 절차의 효율화를 동시에 달성한 의료기관은 치료 시작의 예측 가능성이 높아지고 재심사 횟수가 줄어드는 이점을 누리고 있습니다. 따라서 북미의 외래 종양학 주입 치료 시장은 안정적인 접근성, 엄격한 비용 관리, 그리고 기술을 활용한 처리 능력 향상이 결합된 특징을 가지고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.13%를 나타낼 것으로 예측되며, 이는 대도시권 및 지역 거점의 수용 능력 확대를 위한 투자를 반영한 것입니다. 민간 및 공공 의료기관은 확대되는 병원 시스템 내에서 정맥주사 요법에 대한 접근성을 개선하는 종양학 서비스를 지속적으로 구축하고 있습니다. 보험사 및 보건부가 보다 광범위한 종양학 인프라에 투자하는 가운데, 주사 센터는 복잡한 생물학적 제제의 안전하고 확실한 투여를 보장하기 위해 표준 업무 절차(SOP) 및 약사 교육에 주력하고 있습니다. 예측 기간 동안, 특히 생물학적 제제의 사용이 증가하고 있는 도시 지역 시장에서 투여 일정 분석 및 투여량 조제 기준의 도입이 확대될 것으로 예측됩니다. 이를 통해 규모 확대와 임상 거버넌스를 뒷받침할 시설 간 표준화의 기회가 마련됩니다. 외래 종양학 주입 치료 시장에서는 주요 도시의 환자 동선 예측 가능성 향상과 약제 조제의 현대화를 통해 이러한 투자의 성과가 나타날 것으로 보입니다.

기타 지역에서는 자금 조달 상황, 인력 확보 상황, 그리고 지역의 질병 부담에 따라 의료 제공업체의 동향에 차이가 나타납니다. 유럽에서는 각국의 지급 체계와 복잡한 치료 요법을 분산된 방식으로 관리할 수 있는 전문 의료 체계의 필요성 사이에서 균형을 모색하고 있습니다. 중동 및 아프리카 시장에서는 첨단 치료 프로토콜을 통합하는 3차 의료기관을 핵심으로 삼아, 보다 광범위한 종양학 프로그램 내에 정맥 주사 투여 거점을 점진적으로 확대되고 있습니다. 라틴아메리카에서는 지역별 지불 주체 구성과 최근 출시된 생물학적 제제에 대한 접근성 차이로 인해 정맥 주사 서비스에 대한 수요가 유지되고 있습니다. 각 지역에서 교육, 품질 관리 및 일정 관리 도구의 확장성은 여전히 생산성 향상과 환자 경험 개선에 핵심적인 역할을 하고 있습니다. 외래 종양학 주입 치료 시장에서는 임상 거버넌스와 지역 사회에 대한 접근성을 모두 갖춘 사업자가 계속해서 우위를 점하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the outpatient oncology infusion market size is expected to grow from USD 10.81 billion in 2025 to USD 11.59 billion in 2026 and is forecast to reach USD 17.02 billion by 2031 at 7.99% CAGR over 2026-2031.

This report is Segmented by Care Setting (Hospital Outpatient Departments, Physician Office / Community Oncology, and More), Therapy Type (Cytotoxic Chemotherapy, and More), Tumor Type (Breast Cancer, Lung Cancer, Colorectal Cancer, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Value (USD).

Global Outpatient Oncology Infusion Market Trends and Insights

Rapid Uptake of Infusion-Based Immunotherapies and Biologics

Regulatory momentum behind antibody-drug conjugates has reshaped infusion demand by adding indications that require scheduled intravenous cycles, bundled premedication, and post-infusion monitoring, which raises average chair-time per visit. The approval path for datopotamab deruxtecan in breast cancer and subsequent expansion into lung cancer reinforces this trend as providers operationalize ADC-specific protocols that differ from legacy cytotoxic regimens. In 2026, ifinatamab deruxtecan received Priority Review for extensive-stage small cell lung cancer, signaling additional high-intensity infusion volumes if approved, and adding complexity through monitoring of immune-related toxicities. Growth in the outpatient oncology infusion market is therefore being supported both by new agent approvals and by extended infusion administration and observation windows linked to immunotherapies. These dynamics reward centers that standardize premedication pathways and adverse event surveillance while sustaining patient experience. They also heighten the need for scalable scheduling models that accommodate longer chair occupancy without increasing cancellations or wait times.

Shift to Outpatient and Ambulatory Settings for Cost, Access, and Patient Experience

CMS finalized a site-neutral payment step that sets a significant share of the hospital outpatient rate for drug administration in excepted off-campus provider-based departments, which reduces reimbursement for services that had migrated to these locations after prior policy changes. This rule change increases incentives to deliver appropriate chemotherapy and biologic infusions in ambulatory or physician-aligned sites that offer lower total costs, shorter patient travel times, and streamlined scheduling. As the outpatient oncology infusion market adapts in 2026, providers that operate multiple sites are aligning service mix by acuity and resource intensity to protect margins and sustain access. Patients and referring clinicians favor locations that balance safety, timely starts, and consistent care teams, which has aided community-site growth for maintenance therapies and routine biologics. The result is a gradual redistribution of volume toward centers that offer predictable experience, transparent cost structures, and pathway-adherent regimens backed by payer alignment.

Reimbursement Pressure (site-neutral, 340B remedy) Compresses Margins

Site-neutral policies now pay significantly of the hospital outpatient rate for drug administration in excepted off-campus departments, which directly reduces reimbursement in locations that captured growing shares of infusion services in prior years. CMS has also implemented a multi-year 340B-related recoupment adjustment to the non-drug OPPS update, which further tightens hospital budgets and raises the bar for capital commitments to infusion chairs and pharmacies. Provider associations have flagged that uniform site-neutral rates do not fully account for the standby capacity and intensive staffing needed to support complex oncology infusions, especially for sicker populations served by academic and safety-net systems. The combined effect is more selective expansion, closer alignment of service mix by acuity, and faster adoption of scheduling and pharmacy workflows that minimize waste. In the outpatient oncology infusion market, these pressures reward centers with strong operational discipline and payer alignment that can sustain high on-time starts and predictable costs. Over the medium term, the policy environment is expected to drive more volume into cost-efficient sites and curb the growth of higher-cost locations.

Other drivers and restraints analyzed in the detailed report include:

- Payer and Policy Incentives for Site-of-Care Optimization and Value-Based Oncology

- Throughput Technologies (AI scheduling, pharmacy automation) Expand Capacity

- Oncology Drug Shortages Disrupt Scheduling and Regimen Delivery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hospital outpatient departments accounted for 53.23% of the outpatient oncology infusion market in 2025, underpinned by integrated diagnostics, surgical coordination, and the governance required for complex biologics and cellular therapies, while standalone ambulatory infusion centers are projected to grow at a 9.01% CAGR through 2031 as payer site-neutral policies favor lower-cost settings. This volume split reflects the ability of hospital sites to manage higher acuity and clinical trial workflows, while ambulatory centers focus on maintenance regimens and pathway-adherent biologics that fit predictable scheduling blocks. The outpatient oncology infusion market is reorganizing around this mix as health systems align service lines by acuity and standardize case selection to sustain quality and margin. Payer policy has reinforced the trend by setting lower payment levels for drug administration in certain off-campus departments, which redirects volume to settings with lean overhead and strong throughput.

Patient experience preferences also matter, since community sites often offer shorter travel, faster starts, and consistent nursing teams. Hospital-based departments remain critical for rapid escalation of care, adverse event management, and access to multidisciplinary expertise within the same campus. In 2026, the balance is not a zero-sum shift but a targeted reallocation of appropriate cases toward centers that combine safety with lower all-in costs. Providers that operate across both settings are adopting centralized triage and scheduling models to place each regimen in the right site.

Over the forecast period, hospital outpatient departments are expected to retain complex protocols such as cellular therapies and infusions requiring frequent lab-based dose adjustments, where co-located pharmacy, emergency capability, and subspecialty consults are important. Ambulatory infusion centers are expected to outgrow the broader outpatient oncology infusion market on the strength of standardized regimens and efficient chair turnover that underpin payer-aligned cost advantages.

The outpatient oncology infusion market size will reflect this mix shift as centers refine premedication pathways, adopt predictive scheduling to level midday peaks, and closely manage infusion observation windows for biologics. Policy steps that lower payments for selected off-campus hospital-based services intensify the focus on cost per infusion start and on-time performance. Accreditation standards and quality programs remain important differentiators for hospital-affiliated centers that manage higher-risk therapy. Network players that combine hospital and community footprints are prioritizing data-driven scheduling, consistent staffing, and patient support services to protect their share in the outpatient oncology infusion market.

Geography Analysis

North America held 43.24% of the outpatient oncology infusion market in 2025, supported by mature oncology networks, broad availability of advanced biologics, and payer contracts that enable pathway-aligned operations at scale. The policy environment in 2026 reinforces cost discipline through site-neutral payment steps and ongoing quality reporting, which have encouraged service mix optimization and broader adoption of predictive scheduling. Providers that deploy multi-site models balance hospital-based oversight for complex regimens with community site access for maintenance therapies. Ongoing accreditation, compliance, and staff education remain table stakes for leaders serving higher-acuity patients. As payers press for value, providers that align pathway adherence with streamlined prior authorization benefit from more predictable starts and fewer re-reviews. The outpatient oncology infusion market in North America is therefore characterized by steady access combined with disciplined cost management and technology-enabled throughput.

Asia-Pacific is projected to grow at a 9.13% CAGR through 2031, reflecting investment in capacity expansion across large urban centers and regional hubs. Private and public providers continue to build oncology services that improve access to infusion care within expanding hospital systems. As payers and ministries of health invest in broader oncology infrastructure, infusion centers are focusing on standard operating procedures and pharmacist training to ensure safe, reliable administration of complex biologics. Over the forecast period, adoption of scheduling analytics and dose preparation standards is expected to rise, particularly in urban markets with growing biologic use. This creates opportunities for cross-center standardization that supports scale and clinical governance. The outpatient oncology infusion market will reflect these investments through more predictable patient flow and modernization of pharmacy compounding across major cities.

In other regions, providers are moving at different speeds depending on funding, workforce availability, and local disease burden. Europe continues to balance national payment frameworks with the need for specialty capacity that can manage complex regimens in a decentralized fashion. Middle East and Africa markets are gradually adding infusion sites within broader oncology programs, often anchored by tertiary hospitals that centralize advanced protocols. Latin America maintains demand for infusion services, shaped by local payer mix and variable access to recent biologic launches. Across regions, scalability of training, quality monitoring, and scheduling tools remains central to raising productivity and patient experience. The outpatient oncology infusion market continues to favor operators that pair clinical governance with accessible community footprints.

- American Oncology Network (AON)

- Apollo Cancer Centers

- Aster DM Healthcare

- City of Hope

- Florida Cancer Specialists & Research Institute (FCS)

- Fortis Healthcare

- GenesisCare

- HCA Healthcare / Sarah Cannon Cancer Institute

- HCG (Healthcare Global Enterprises)

- Manipal Hospitals (Day Care & Domiciliary Chemo)

- Mediclinic Southern Africa

- Memorial Sloan Kettering Cancer Center (MSK)

- Netcare (South Africa)

- OneOncology

- Ramsay Health Care (Australia)

- Subang Jaya Medical Centre (Ramsay Sime Darby)

- The Oncology Institute (TOI)

- The US Oncology Network (McKesson)

- UT MD Anderson Cancer Center

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising cancer incidence and survivorship expand outpatient infusion volumes

- 4.2.2 Shift to outpatient and ambulatory settings for cost, access and experience

- 4.2.3 Rapid uptake of infusion-based immunotherapies and biologics

- 4.2.4 Payer and policy incentives for site-of-care optimization and value-based oncology

- 4.2.5 Throughput technologies (AI scheduling, pharmacy automation) expand capacity

- 4.2.6 Biosimilar adoption lowers acquisition costs and broadens access

- 4.3 Market Restraints

- 4.3.1 Oncology nurse and pharmacist shortages constrain throughput and expansion

- 4.3.2 Reimbursement pressure (site-neutral, 340B remedy) compresses margins

- 4.3.3 Oncology drug shortages disrupt scheduling and regimen delivery

- 4.3.4 Shift to subcutaneous and at-home supportive care reduces chair time revenue

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Care Setting

- 5.1.1 Hospital Outpatient Departments

- 5.1.2 Physician Office / Community Oncology

- 5.1.3 Ambulatory Infusion Centers

- 5.2 By Therapy Type

- 5.2.1 Cytotoxic Chemotherapy

- 5.2.2 Monoclonal Antibodies

- 5.2.3 Checkpoint Inhibitors (PD-1/PD-L1, CTLA-4)

- 5.2.4 Antibody-Drug Conjugates (ADCs)

- 5.2.5 Supportive Care Biologics and Agents (e.g., G-CSF, IVIG, iron)

- 5.3 By Tumor Type

- 5.3.1 Breast Cancer

- 5.3.2 Lung Cancer

- 5.3.3 Colorectal Cancer

- 5.3.4 Prostate Cancer

- 5.3.5 Hematologic Malignancies (e.g., lymphoma, leukemia, myeloma)

- 5.3.6 Gynecologic Cancers

- 5.3.7 Melanoma

- 5.3.8 Head & Neck Cancers

- 5.3.9 Gastric & Esophageal Cancers

- 5.3.10 Liver & Pancreatobiliary Cancers

- 5.3.11 Bladder Cancer

- 5.3.12 Renal Cell Carcinoma

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 American Oncology Network (AON)

- 6.3.2 Apollo Cancer Centers

- 6.3.3 Aster DM Healthcare

- 6.3.4 City of Hope

- 6.3.5 Florida Cancer Specialists & Research Institute (FCS)

- 6.3.6 Fortis Healthcare

- 6.3.7 GenesisCare

- 6.3.8 HCA Healthcare / Sarah Cannon Cancer Institute

- 6.3.9 HCG (Healthcare Global Enterprises)

- 6.3.10 Manipal Hospitals (Day Care & Domiciliary Chemo)

- 6.3.11 Mediclinic Southern Africa

- 6.3.12 Memorial Sloan Kettering Cancer Center (MSK)

- 6.3.13 Netcare (South Africa)

- 6.3.14 OneOncology

- 6.3.15 Ramsay Health Care (Australia)

- 6.3.16 Subang Jaya Medical Centre (Ramsay Sime Darby)

- 6.3.17 The Oncology Institute (TOI)

- 6.3.18 The US Oncology Network (McKesson)

- 6.3.19 UT MD Anderson Cancer Center

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment