|

시장보고서

상품코드

2063591

임상 문서 분야 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Clinical Documentation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

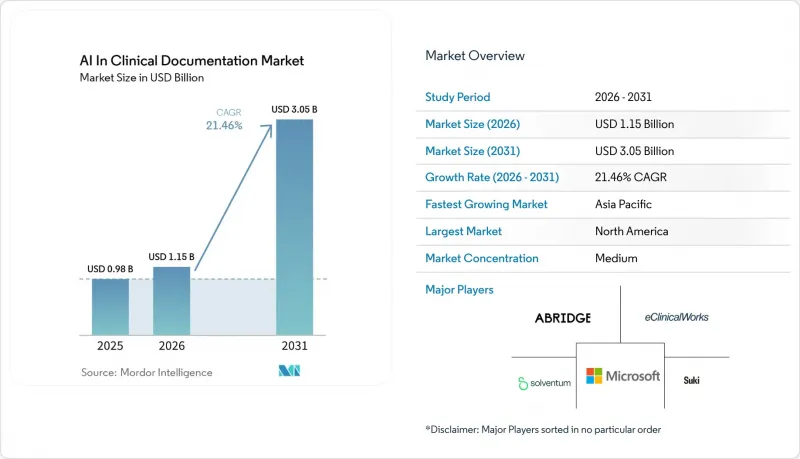

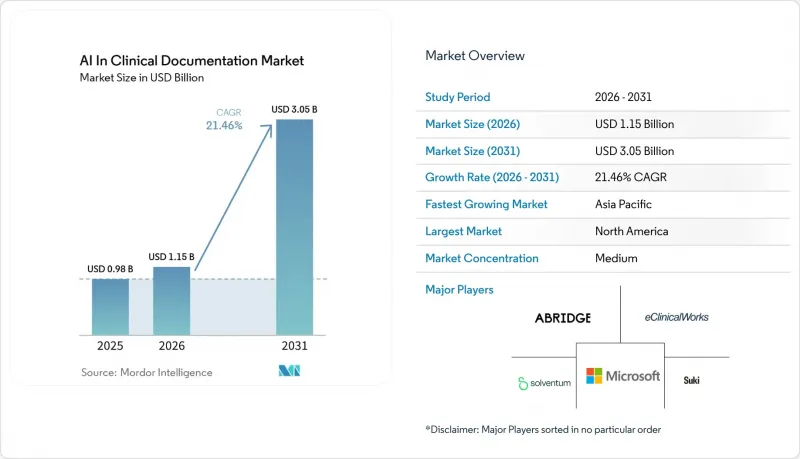

임상 문서 분야 인공지능(AI) 시장 규모는 2025년 9억 8,000만 달러로 평가되었습니다. 2026년에는 11억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 21.46%로 성장을 지속하여, 2031년에는 30억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어/AI 플랫폼, 기타), 도입 형태(클라우드/SaaS, On-Premise), 용도(앰비언트·임상 기록, 기타), 최종 사용자(병원 및 통합 의료 네트워크, 기타), 임상 환경(입원 환자, 기타), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 임상 문서 분야 인공지능(AI) 시장 동향 및 인사이트

앰비언트 스크라이빙 및 CDI(임상 문서 개선)와 CAPD(임상 문서 자동 생성)는 문서 작성의 부담을 줄여주며,

앰비언트 스크라이빙은 조직이 인력을 증원하지 않고도 근무 시간 외 진료 기록 작성 부담을 줄이고 진료 흐름을 개선하는 데 우선순위를 둔 결과, 임상 현장의 주류로 자리 잡았습니다. 외래 진료 현장의 사례에 따르면, AI가 생성한 기록은 문서 작성 시간을 단축하고 효율성 향상에 기여하는 것으로 나타났으며, 이를 통해 임상의가 절약한 시간을 근무 시간 단축이 아닌 환자 진료 시간 확대에 활용함으로써, 일일 진료 건수 증가로의 전환이 촉진되고 있습니다. 의료 기관은 프런트엔드의 앰비언트 스크라이빙과 백엔드의 CDI(임상 문서 개선) 또는 CAPD(임상 문서 자동 검증) 검토를 결합함으로써, 서술적인 기록을 구체적이고 감사 가능한 문구로 변환하여 보다 적절한 코딩을 실현하고 후속 단계에서의 조회 건수를 줄이고 있습니다. 각 벤더사는 AI가 필요한 수식어를 제안하고, 근거를 제시하여 이를 ICD-10 및 HCC 코드에 매핑함으로써, 코딩의 복잡성과 수익의 일관성이 측정 가능한 수준으로 향상되었다고 보고하고 있습니다. 이로 인해 진료 기록 수정 건수가 줄어들었을 뿐만 아니라, 현금 회수 주기도 단축되고 있습니다. 2026년에 사전 승인 및 상호 운용성 규정이 적시성과 투명성을 중시하는 가운데, 지불 기관은 간결하고 체계적이며 추적 가능한 임상 제출 자료를 기대하고 있으며, 이에 따라 스크라이빙과 일관성 검사의 결합이 진료 현장에서 전략적인 수단이 되고 있습니다. 따라서 임상 문서 작성 시장에서 AI는 처리 능력, 코딩의 특이성, 설명 가능성을 중심으로 제품 로드맵을 조정하고 있으며, 이러한 요소들이 결합되어 거부 위험을 낮추고 의료 시스템 및 지불 기관에 더 명확한 재정적 수익을 창출하고 있습니다.

EHR과 긴밀하게 통합된 솔루션이 기업 차원의 워크플로우 내 도입을 촉진합니다.

문서 작성 지원 기능이 EHR 워크플로우 내에 직접 통합되어 있는 경우, 임상의가 외부 창을 전환하거나 데이터를 다시 입력할 필요가 없기 때문에 도입 확대가 가장 빠르게 진행됩니다. 의료 기관에서는 AI가 생성한 기록, 지시 사항, 코딩 제안이 최소한의 클릭 조작과 명확한 근거 링크와 함께 EHR에 다시 기록됨으로써 신뢰성과 감사 가능성이 강화되고, 보다 원활한 도입과 지속적인 이용률 향상이 보고되고 있습니다. EHR 네이티브 방식이나 긴밀하게 통합된 접근 방식은 도입, 권한, 임상 컨텐츠가 기존의 거버넌스 및 보안 프레임워크 내에서 관리되므로 IT 부서의 부담도 줄여줍니다. 특히 복잡한 템플릿을 사용하는 전문 분야에서 시간적 제약이 있는 진료 상황에서 일선 사용자들이 절차나 화면 전환을 줄이기를 원할 경우, 미미한 정확도 향상보다는 통합의 깊이가 더 중요해집니다. 앰비언트 캡처와 구조화된 기록 기능을 결합한 환경에서는 지불자의 요구 사항을 조기에 파악할 수 있으며, 퇴원, 의뢰, 사전 승인 단계에서 발생할 수 있는 불필요한 마찰을 줄일 수 있습니다. 임상 문서 작성 시장에서 AI는 표준에 부합하는 통합으로 지속적으로 수렴하고 있으며, 이를 통해 임상의의 업무 흐름이 유지되고, 음성 및 텍스트가 기존 기록 시스템 내에서 지시사항, 코드, 환자 지침으로 변환됩니다.

환경 음향의 수집 및 저장과 관련된 환자의 동의 및 개인정보 보호 제한

일부 환경에서는 특히 환자가 모델 사용 방법, 데이터 처리, 공급업체에 대한 접근 권한 등에 대해 상세한 설명을 들은 경우, 동의 획득 여부가 상시 음성 녹음 도입의 걸림돌이 되고 있습니다. 외래 진료에 대한 조사 연구에 따르면, AI의 기능이나 데이터 흐름에 관한 상세한 정보를 환자에게 제공할 경우 동의율이 낮아질 가능성이 있으며, 응답자의 상당수가 진료 데이터를 공급업체와 일절 공유하지 않기를 바라는 것으로 나타났습니다. 또한, 환자들은 음성 수집 도구가 사용되고 있다는 사실을 알게 되면 민감한 주제에 대해 말을 삼가게 될 가능성이 있다고 보고하고 있습니다. 이로 인해 선택 편향이 발생하여, 고위험군 환자에 대해 생성되는 진료 기록의 임상적 완전성이 훼손될 우려가 있습니다. 이러한 경향은 도입 설계에 영향을 미치며, 옵트아웃 선택권과 진료 중의 명확한 동의 절차가 환자 경험의 핵심이 되도록 요구하고 있습니다. 일부 조직에서는 투명성이 높은 사용자 인터페이스와 가시성이 뛰어난 녹음 제어 기능을 활용하여 원본 음성 데이터의 이동을 제한하는 한편, 신속한 삭제 및 단말기 내 처리를 중시하는 접근 방식을 우선시함으로써 안심감과 개인정보 보호에 대한 우려를 해소하고 있습니다. 동의 절차가 성숙해지고, 문서화 도구가 ‘프라이버시 바이 디자인’을 전면에 내세우게 됨에 따라, 임상 문서화 분야의 AI 시장은 모든 의료 현장에서 효율성과 환자의 신뢰, 그리고 규제상의 기대치 간의 균형을 맞출 수 있게 될 것입니다.

부문별 분석

소프트웨어 및 AI 플랫폼은 2025년에 시장 가치의 58.24%를 차지했으며, 2031년까지 연평균 23.44%의 성장률을 보일 것으로 전망됩니다. 이는 영구 라이선스에서 진료 건수에 따라 유연하게 조정되는 SaaS로 전환한 것을 반영한 것입니다. 가격 책정 방식의 진화에 따라, 요금은 고정된 라이선스 수에 따라 결정되는 것이 아니라 달성된 성과에 연동되게 되어, 대규모 도입 시 경제적 타당성이 향상되고, 진료 건수가 적은 기간의 유휴 비용이 절감됩니다. 기업의 구매 담당자들은 계절에 따라 사용자 수를 유연하게 확장할 수 있다는 점과, 앰비언트 스크라이빙 및 일관성 검사 기능을 하나의 경험으로 통합할 수 있다는 점을 중요하게 여기며, 이를 통해 플랫폼 차원의 사용자 유지율이 높아집니다. 벤더 측 발표에 따르면, 다중 모드 데이터 수집, 구조화된 기록, 코딩 지원이 다양한 전문 분야에 걸쳐 대규모의 단일 워크플로우로 운영되는 기업 내 도입 확대가 강조되고 있습니다. 이 구성은 표준화된 거버넌스, 신속한 도입, 그리고 입원 및 외래를 포함한 모든 의료 현장에서 일관된 결과를 뒷받침합니다. 임상 문서 작성 시장에서 AI는 클릭 횟수를 최소화하고, 토큰 사용량을 줄이며, 감사가 용이한 추적 가능한 결과물을 제공하는 플랫폼을 계속해서 높이 평가했습니다.

하드웨어와 디바이스는 현재 총 지출에서 차지하는 비중이 줄어들고 있지만, 조직이 캡처 환경에 대해 보다 세밀한 제어를 원하거나 원시 음성 데이터의 이동을 최소화하고자 하는 경우에는 여전히 중요한 역할을 하고 있습니다. 엣지 캡처와 중앙 집중형 언어 모델을 결합함으로써, 동의와 관련된 기밀성을 확보하고, 연결 환경이 불안정할 때를 대비한 백업 기능을 제공할 수 있습니다. 병원이 문서화 지원을 간호 및 관련 의료 직종의 업무 흐름까지 확대함에 따라, 주변 기기, 환경 마이크 및 병실 설정 서비스에 대한 수요는 병상 수에 따라 증가할 가능성이 있습니다. 또한, 도입이 단일 전문 분야의 시범 사업에서 입원, 일일 경과 기록, 퇴원 요약, 치료 이관 등을 포함하는 복잡한 단계로 전환됨에 따라 전문 서비스도 확대되고 있습니다. 클라우드 제공업체와 EHR 벤더들은 가치 실현까지 걸리는 시간을 단축하기 위해 의료 전용 솔루션 아키텍처에 투자하고 있으며, 이를 통해 소프트웨어 기능과 운영상의 변경 관리 간의 격차가 줄어들고 있습니다. 그 결과, 임상 문서 작성 업계에서 AI는 ‘소프트웨어 퍼스트’ 플랫폼을 중심으로 구축되는 동시에, 복잡한 환경에서의 도입을 가속화하고 마찰을 줄여주는 서비스를 강화하고 있습니다.

클라우드/SaaS 도입은 2025년에 시장 가치의 51.35%를 차지했으며, 연평균 성장률(CAGR) 23.82%라는 가장 빠른 속도로 확대되고 있습니다. 이는 모델을 통합함으로써 현지에서 별도의 유지보수 작업 없이도 임상 용어, 안전 대책 및 프롬프트 전략을 신속하게 업데이트할 수 있기 때문입니다. 의료 시스템은 거점 및 전문 분야를 넘나들며 일제히 전개되는 동기화된 개선의 혜택을 받아, 시범 단계에서 측정 가능한 성과를 얻기까지 걸리는 시간을 단축할 수 있습니다. 또한, 의료 제공업체들은 모델 성능과 공정성에 대한 중앙 집중형 모니터링을 선호하며, 추론 경로가 표준화되어 있을 경우 그 운영이 더욱 간소화됩니다. 클라우드 기반 아키텍처는 기존의 기업 거버넌스 관행과 부합하며, 모델의 동작에 업데이트가 필요한 경우에도 신속한 정책 변경을 가능하게 합니다. 모델의 품질이 향상됨에 따라, 지역별 버전 간의 불일치 위험이 줄어들고 신뢰성이 높아지는 동시에 현장 직원의 교육 부담도 경감됩니다. 소프트웨어와 모니터링 체계가 모두 확장됨에 따라 총소유비용(TCO)이 절감되므로, 많은 조직은 임상 문서 분야 인공지능(AI) 시장에서 앞으로도 클라우드 중심 모델을 선호하며 계속 채택할 것으로 보입니다.

개인정보 보호를 중시하고 지연에 민감한 워크플로우에서는 하이브리드 방식이 주목받고 있습니다. 이 설계에서는 음성 캡처와 1차 텍스트 변환이 로컬에서 수행되며, 익명화된 텍스트가 클라우드 호스팅 모델로 전송되어 요약 및 코딩 지원이 이루어집니다. 이를 통해 동의와 관련된 우려 사항과 확장성 간의 균형을 맞출 수 있습니다. 이러한 접근 방식을 통해 의료 현장 외부에서 원본 음성이 공개될 위험을 줄이면서도, 프롬프트 엔지니어링 및 안전 대책에 대한 중앙 집중식 관리를 통한 개선 효과를 유지할 수 있습니다. 하이브리드 설계는 저지연 음성 수집을 필요로 하면서도 컨텐츠 구조화에는 보다 강력한 클라우드 모델을 활용하고자 하는 다국어 클리닉의 요구 사항에도 부합합니다. 네트워크 환경이 불안정한 입원 병동에서는 특히 긴급성이 높은 시기에 데이터를 EHR로 확실하게 전송하기 위해 하이브리드 구성이 채택되고 있습니다. 규제 요건이 변화하는 가운데, 이 아키텍처를 통해 의료 시스템은 워크플로우의 변경을 최소화하면서 엣지와 클라우드 간에 처리를 유연하게 전환할 수 있게 됩니다. 임상 문서 작성 시장에서 AI는 클라우드를 기본으로 하되, 특정 규제나 운영상의 요구에 따라 하이브리드 방식을 활용하는 등 두 가지 접근 방식이 모두 유지될 전망입니다.

지역별 분석

북미는 대규모 EHR 도입과 임상의의 경험 및 관리 효율성을 우선시하는 지속적인 임상 IT 지출에 힘입어, 2025년에는 세계 시장 규모의 50.16%를 차지했습니다. 2026년까지 확대된 상호운용성 이니셔티브와 네트워크 수준의 데이터 교환을 통해 구조화된 임상 정보의 이동 속도가 빨라지고 있으며, 이를 통해 읽기 가능하고 기계 처리 가능한 문서화가 지원되고 있습니다. 미국의 병원 및 의사 그룹은 여러 진료과에 걸쳐 앰비언트 스크라이빙을 확대하는 동시에, 보험 적용 기준 및 위험 조정 요구 사항에 부합하는 CDI 오버레이와 코딩 지원 체계를 구축하고 있습니다. 임상 거버넌스는 도입의 핵심이므로, 각 기관은 근거에 기반한 성과와 EHR 내에서의 신속한 검증을 중시하고 있습니다. 미국병원협회(AHA)는 앰비언트 툴의 사용이 조직 전체로 확대됨에 따라, 의료 기관의 시스템이 업무 흐름을 어떻게 표준화하고 품질을 모니터링하고 있는지를 보여주는 초기 도입 사례를 소개했습니다. 개인정보 보호와 안전에 대한 기대가 높아지는 가운데, 북미의 임상 문서 작성용 AI 시장에서는 각 기재 내용의 출처가 되는 근거를 명확히 제시하고, 팀 간에 일관된 편집 이력을 제공하는 설계가 높이 평가받고 있습니다.

유럽에서는 상환 모델이 다양하며, 많은 시스템에서 시간 단축에 따른 직접적인 수익 증가가 그리 뚜렷하지 않기 때문에 도입은 신중하게 진행되고 있습니다. 개인정보 보호를 중시하는 법역에 위치한 병원이나 진료소에서는 원본 음성 데이터의 이동을 제한하고, 신속한 삭제 정책과 단말기 내 기록 및 클라우드 상의 요약 정보를 결합한 하이브리드 설계를 선호하는 경향이 있습니다. 구매자들은 특히 사소한 오류라도 업무 처리 과정에서 마찰을 일으킬 가능성이 있는 다국어 환경에서 설명 가능성과 일관성을 중요하게 여깁니다. 의료기관과 보험사들은 최종 진료 기록에 대한 임상적 설명 책임을 확보하기 위해 명확한 인적 검토 절차와 감사 기록에 중점을 두고 있습니다. 이러한 우선순위들 중에서 앰비언트 스크리빙은 문서 작성 부담이 특히 큰 전문 분야에서 먼저 도입되기 시작했으며, 거버넌스가 성숙해짐에 따라 데이터 무결성을 보장하는 체계가 추가되면서 점차 확대되는 경향을 보이고 있습니다. 모델이 각 지역의 언어 및 임상 관행에 적응해 감에 따라, 유럽의 임상 문서 작성용 AI 시장은 데이터 노출을 최소화하고 추적성을 극대화하도록 설계됨에 따라 성장할 것으로 예측됩니다.

아시아태평양은 각국의 디지털 헬스 전략과 공공 부문 프로그램이 표준화 및 상호운용성 달성을 가속화하고 있어, 연평균 성장률(CAGR) 23.24%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 도시 지역이나 학술 기관의 의료 시스템에서는 임상 현장에서 다양한 언어를 사용하는 환자층을 지원하기 위한 생성형 도구의 시범 운영이 진행되고 있으며, 대부분의 경우 실제 업무 흐름 속에서 의료용 언어 모델을 검증하는 공동 연구를 통해 이루어지고 있습니다. 또한, 의료 제공업체들은 언어 및 지연 요건과 관할 구역을 초월하는 데이터 보호에 대한 기대치를 모두 충족시키는 하이브리드 도입 방식도 모색하고 있습니다. 인구 밀도가 높은 도시 지역에서 진료를 제공하는 공립 및 사립 병원들은 처리 능력 향상이라는 명확한 이점을 인식하고 있으며, 표준화가 진행됨에 따라 외래 및 응급실 현장에서의 도입이 촉진되고 있습니다. 구매자들은 각국의 코드 세트 및 임상 관행에 대응할 수 있는 도구를 원하고 있으며, 이를 통해 작성된 문서가 현지 규정을 준수하도록 하고 있습니다. 영어 및 비영어권 언어에 대한 기능이 향상됨에 따라, 아시아태평양의 임상 문서 분야 인공지능(AI) 시장은 언어 지원 및 상호 운용성을 갖춘 설계를 통해 그 성장세를 이어갈 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the aI in clinical documentation market size is expected to grow from USD 0.98 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 3.05 billion by 2031 at 21.46% CAGR over 2026-2031.

This report is Segmented by Component (Software/AI Platforms, and Others), Deployment (Cloud/SaaS, On-Premises), Application (Ambient Clinical Scribing, and Others), End User (Hospitals and IDNs, and Others), Clinical Setting (Inpatient, and Others), and Geography (North America, Europe, Asia-Pacific, and Others). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Clinical Documentation Market Trends and Insights

Ambient Scribing and CDI or CAPD Reduce Documentation Burden and Increase

Throughput Ambient scribing moved into the clinical mainstream as organizations prioritized reduced after-hours charting and improved visit flow without adding staff. Evidence from ambulatory settings shows that AI-generated notes can reduce documentation time and improve perceived efficiency, which supports a shift toward higher daily visit volumes when clinicians absorb time savings into added patient slots rather than shorter workdays. Providers are pairing front-end ambient scribing with back-end CDI or CAPD reviews so that narrative notes are transformed into specific, auditable statements that support better coding and fewer downstream queries. Vendors report measurable uplifts in coded complexity and revenue integrity where AI suggests needed qualifiers and maps to ICD-10 and HCC codes with supporting rationales, reducing amended encounters and tightening cash cycles. As prior authorization and interoperability rules emphasize timeliness and transparency in 2026, payers expect clinical submissions that are concise, structured, and traceable, making combined scribing and integrity checks a strategic lever at the point of care. The AI in clinical documentation market is therefore aligning product roadmaps around throughput, coding specificity, and explainability, which together reduce denial risk and create clearer financial returns for health systems and payers.

Deep EHR-Native Integrations Drive In-Workflow Adoption at Enterprise Scale

Adoption scales fastest when documentation support is embedded directly inside EHR workflows so clinicians do not toggle between external windows or re-enter data. Health systems are reporting smoother rollouts and higher sustained use where AI-generated notes, orders, and coding suggestions write back to the EHR with minimal clicks and clear evidence links, reinforcing trust and auditability. EHR-native or tightly integrated approaches also reduce IT lift because deployment, permissions, and clinical content are managed within existing governance and security frameworks. Integration depth matters more than marginal accuracy gains when frontline users seek fewer steps and fewer screen changes during time-pressed encounters, especially in specialties with complex templates. Environments that couple ambient capture with structured write-back can surface payer requirements earlier and reduce avoidable friction at discharge, referral, or prior authorization checkpoints. The AI in clinical documentation market continues to converge around standards-aligned integrations that keep the clinician in flow and convert audio and text into orders, codes, and patient instructions within the native system of record.

Patient Consent and Privacy Constraints on Ambient Audio Capture and Storage

Consent dynamics remain a gating factor for always-on audio in some settings, especially when patients receive detailed disclosures about model usage, data handling, and vendor access. Survey research in ambulatory care shows that consent rates can drop when patients are given more granular information on AI features and data flows, and a notable share of respondents prefer that encounter data is not shared with vendors at all. Patients also report they may self-censor on sensitive topics if they know audio capture tools are in use, which introduces selection bias that can erode the clinical completeness of generated notes for higher-risk populations. These patterns shape deployment design, making opt-out options and clear in-visit consent flows central to patient experience. Some organizations are prioritizing approaches that limit the movement of raw audio and emphasize rapid deletion or on-device processing to address comfort and privacy concerns, supported by transparent user interfaces and visible recording controls. As consent processes mature and documentation tools foreground privacy by design, the AI in clinical documentation market can balance efficiency with patient trust and regulatory expectations across care settings.

Other drivers and restraints analyzed in the detailed report include:

- Accuracy Gains in Medical Speech Recognition and LLMs Elevate Note Quality and Speed

- Revenue Integrity and Audit Pressure Expand AI-Supported CDI or CAPD and Coding

- Clinical Risk or Liability Necessitating Human Review and Strong Governance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software and AI Platforms captured 58.24% of market value in 2025 and are projected to grow at 23.44% through 2031, reflecting a shift from perpetual licenses to flexible SaaS aligned to encounter volume. The pricing evolution links fees to realized outcomes rather than fixed seats, which improves economic alignment in large deployments and reduces idle cost during low-volume periods. Enterprise buyers value the ability to scale users seasonally and to bundle ambient scribing with integrity overlays as a single experience, which increases stickiness at the platform level. Vendor announcements highlight growing enterprise adoption where multimodal capture, structured write-back, and coding support run as one workflow at scale across many specialties. This configuration supports standardized governance, faster onboarding, and more consistent results across inpatient and ambulatory settings. The AI in clinical documentation market continues to reward platforms that minimize clicks, compress token usage, and deliver traceable outputs that are simple to audit.

Hardware and devices play a smaller role in total spend today but remain relevant where organizations seek more control over capture environments or want to minimize movement of raw audio. Edge capture paired with centralized language models can address consent sensitivities and provide a backup when connectivity is variable. As hospitals extend documentation support to nursing and allied health workflows, demand for peripherals, ambient microphones, and room setup services can rise with bed capacity. Professional services also expand as deployments move from single-specialty pilots to complex rollouts that involve admissions, daily progress notes, discharge summaries, and care transitions. Cloud providers and EHR vendors are investing in health-specific solution architectures to reduce time to value, which narrows gaps between software capabilities and operational change management. As a result, the AI in clinical documentation industry is building around software-first platforms while reinforcing services that accelerate adoption and reduce friction in complex environments.

Cloud/SaaS deployment held 51.35% of market value in 2025 and is expanding at the fastest 23.82% CAGR, since centralizing models allows rapid updates to clinical vocabularies, safety guardrails, and prompt strategies without local maintenance. Health systems benefit from synchronized improvements that roll out across sites and specialties at once, which shortens the time from pilot to measurable returns. Providers also favor centralized monitoring of model performance and fairness, which is simpler to run when inference paths are standardized. Cloud-based configuration aligns with existing enterprise governance practices and allows rapid policy changes if model behaviors need updates. As model quality rises, the risk of inconsistent local versions decreases, which improves trust and reduces training overhead for frontline staff. Many organizations will continue to prefer cloud-centric models in the AI in clinical documentation market because the total cost of ownership is lower when both software and oversight scale together.

Hybrid patterns are gaining traction in privacy-centric and latency-sensitive workflows. In these designs, audio capture and primary transcription occur locally while de-identified text is sent to cloud-hosted models for summarization and coding support, which balances consent concerns with scalability. This approach reduces exposure of raw audio outside the care setting while preserving centralized improvements in prompt engineering and safety rails. Hybrid designs also align with the needs of multilingual clinics that want low-latency capture while leveraging stronger cloud models for structuring content. Inpatient areas with variable network conditions use hybrid set-ups to copy data to the EHR reliably, especially during high-acuity periods. As regulatory requirements evolve, this architecture gives health systems flexibility to shift processing across the edge or cloud with minimal workflow change. The AI in clinical documentation market will likely sustain both approaches, with cloud as the default and hybrid for specific regulatory or operational needs.

Geography Analysis

North America accounted for 50.16% of global value in 2025 due to large-scale EHR installations and sustained clinical IT spending that prioritizes clinician experience and administrative efficiency. Interoperability initiatives and network-level data exchange that expanded by 2026 are enabling faster movement of structured clinical information, which supports documentation that is both readable and machine-actionable. U.S. hospitals and physician groups are scaling ambient scribing across multiple service lines while building CDI overlays and coding support that align with coverage criteria and risk adjustment needs. Clinical governance is central to adoption, so organizations emphasize evidence-linked outputs and rapid verification inside the EHR. The American Hospital Association has profiled early deployments that show how provider systems are standardizing workflows and monitoring quality as ambient tools expand into enterprise use. With privacy and safety expectations rising, the AI in clinical documentation market in North America rewards designs that surface the source evidence for each claim and provide consistent edit trails across teams.

Europe shows measured uptake because reimbursement models vary and direct revenue gains from saved minutes are less pronounced in many systems. Hospitals and clinics in privacy-centric jurisdictions often prefer hybrid designs that limit the movement of raw audio, with quick deletion policies and on-device capture paired with cloud summarization. Buyers emphasize explainability and consistency, especially in multilingual environments where small errors can create administrative friction. Provider and payer organizations focus on clear human review steps and audit logs that preserve clinical accountability for final notes. Within these priorities, ambient scribing often enters through specialties where documentation burden is acute and then expands with integrity overlays as governance matures. As models adapt to local languages and clinical conventions, the AI in clinical documentation market in Europe is expected to grow through designs that minimize data exposure and maximize traceability.

Asia-Pacific is the fastest-growing region at 23.24% CAGR as national digital-health strategies and public-sector programs accelerate standardization and interoperability goals. Health systems in cities and academic centers are piloting generative tools that support multilingual patient populations in clinical settings, often through collaborations that test medical language models in real-world workflows. Providers are also exploring hybrid deployments that match language and latency needs with data protection expectations across jurisdictions. Public and private hospitals that serve dense urban populations see clear benefits in throughput and note standardization, which strengthens adoption in ambulatory and emergency settings. Buyers look for tools that can handle code sets and clinical conventions across countries so documentation outputs are locally compliant. As capabilities improve across English and non-English languages, the AI in clinical documentation market in Asia-Pacific is expected to sustain its momentum through language support and interoperable designs.

- Abridge

- Amazon Web Services

- Ambience Healthcare

- Augmedix

- CodaMetrix

- Corti

- DeepScribe

- Dolbey

- eClinicalWorks (Sunoh.ai)

- Eleos Health

- Fathom

- Google Cloud

- Heidi Health

- Iodine Software

- Meditech

- Microsoft (Nuance)

- Oracle Health

- ScribeAmerica

- Solventum

- Suki AI

- Tali AI

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ambient Scribing and CDI/CAPD Reduce Documentation Burden and Increase Throughput

- 4.2.2 Deep EHR-Native Integrations Drive In-Workflow Adoption at Enterprise Scale

- 4.2.3 Accuracy Gains in Medical Speech Recognition and LlMs Elevate Note Quality and Speed

- 4.2.4 Revenue Integrity and Audit Pressure Expand AI-Supported CDI/CAPD and Coding

- 4.2.5 Multilingual, Specialty-Tuned Models Open ED, Inpatient, and Complex Specialty Use

- 4.2.6 Enterprise AI Platforms and GPU Access Enable Bundled, Scaled Deployments

- 4.3 Market Restraints

- 4.3.1 Patient Consent and Privacy Constraints on Ambient Audio Capture and Storage

- 4.3.2 Clinical Risk/Liability Necessitating Human Review and Strong Governance

- 4.3.3 Unit Economics Sensitivity to LLM/ASR Inference Cost and Latency

- 4.3.4 Accent/Language Performance Gaps Limiting Equitable Global Rollout

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software / AI platforms

- 5.1.2 Services

- 5.1.3 Hardware and Devices

- 5.2 By Deployment

- 5.2.1 Cloud / SaaS

- 5.2.2 On-Premises

- 5.3 By Application

- 5.3.1 Ambient Clinical Scribing

- 5.3.2 Medical Speech Recognition

- 5.3.3 Clinical Documentation Integrity (CDI) / CAPD

- 5.3.4 Automated Medical Transcription and Note Summarization

- 5.3.5 Others

- 5.4 By End User

- 5.4.1 Hospitals and IDNs

- 5.4.2 Physician Groups and Clinics

- 5.4.3 Diagnostic Imaging Centers

- 5.4.4 Healthcare Payers

- 5.4.5 Others

- 5.5 By Clinical Setting

- 5.5.1 Inpatient

- 5.5.2 Outpatient

- 5.5.3 Emergency and Urgent Care

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Abridge

- 6.3.2 Amazon Web Services

- 6.3.3 Ambience Healthcare

- 6.3.4 Augmedix

- 6.3.5 CodaMetrix

- 6.3.6 Corti

- 6.3.7 DeepScribe

- 6.3.8 Dolbey

- 6.3.9 eClinicalWorks (Sunoh.ai)

- 6.3.10 Eleos Health

- 6.3.11 Fathom

- 6.3.12 Google Cloud

- 6.3.13 Heidi Health

- 6.3.14 Iodine Software

- 6.3.15 MEDITECH

- 6.3.16 Microsoft (Nuance)

- 6.3.17 Oracle Health

- 6.3.18 ScribeAmerica

- 6.3.19 Solventum

- 6.3.20 Suki AI

- 6.3.21 Tali AI

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment