|

시장보고서

상품코드

2063592

소아천식 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Pediatric Asthma Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

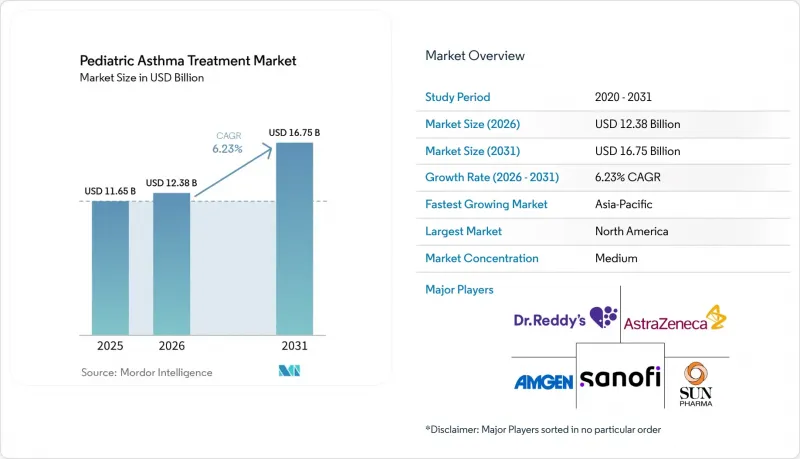

Mordor Intelligence에 의하면, 소아천식 치료 시장 규모는 2025년 116억 5,000만 달러, 2026년 123억 8,000만 달러에서 2031년까지 167억 5,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 6.23%를 나타낼 것으로 예측됩니다.

본 보고서는 치료 유형(장기 관리 약물 및 즉효성 약물), 약물 분류(흡입용 코르티코스테로이드, 장시간 작용형 베타 자극제 등), 투여 경로(흡입, 경구, 주사), 최종 사용자(병원, 진료소, 재택 간호), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계 소아천식 치료 시장 동향과 인사이트

소아천식 유병률 증가와 조기 진단

보건 기관의 보고에 따르면, 소아천식으로 인한 부담은 지속적으로 존재하며, 격차도 여전히 해소되지 않고 있어, 이로 인해 소아천식 치료 시장의 치료 대상층은 계속해서 확대되고 있습니다. 개정된 지침에서는 반복되는 천명 패턴, 다른 원인의 배제, 그리고 치료에 대한 반응을 종합적으로 고려함으로써 5세 미만 아동의 천식 진단 방법이 명확해졌습니다. 이로 인해 치료 개입 시기가 앞당겨지고, 유지 요법 약물의 사용이 증가하고 있습니다. 중국의 2025년 소아 지침은 악화 위험을 줄이기 위한 기초 조치로 흡입 스테로이드제를 권장하고 있으며, 소아천식 치료 시장에서 유지 요법 약물에 대한 일관된 접근을 중심으로 진료 워크플로우를 조정하고 있습니다. 서태평양 지역을 대상으로 한 종단적 모델에 따르면, 장기적으로 유병률이 지속적으로 증가할 것으로 예측되며, 이는 해당 지역 전체에서 나타나는 도시화와 알레르겐 노출 경향과 일치합니다. 5세부터 실시하는 폐기능 검사에 더해, FeNO나 혈액 호산구 수 등의 바이오마커를 일상적으로 활용하는 것이 외래 진료 현장에서 점차 보편화되고 있으며, 이를 통해 조절제 조기 도입과 치료 기간의 장기화가 촉진되고 있습니다. 이러한 변화들이 복합적으로 작용하여 소아천식 치료 시장에서 수년에 걸친 치료의 안정적인 기반을 뒷받침하고 있습니다.

대기 오염과 호흡기 감염증이 천식을 악화시킵니다.

최신 ‘State of the Air’ 보고서에 따르면, 1억 5,610만 명이 오존 및 미세먼지 농도가 건강에 유해한 수준인 지역에 거주하고 있으며, 이로 인해 소아천식 치료 시장에서 소아용 응급약에 대한 수요와 응급의료 이용률이 높은 수준을 유지하고 있습니다. 미국 환경보호청(EPA)의 증거에 따르면, 단기간의 PM2.5 노출이 소아천식 발작의 중증도 증가와 관련이 있는 것으로 나타났으며, 폐 발달에 미치는 만성적인 영향도 기록되어 있습니다. 이에 따라 노출 관리는 중요한 임상적 대책이 되고 있습니다. 이러한 상황은 소아천식 치료 시장에서 고위험 시즌 동안 항염증성 완화제 전략의 활용과 유지 요법의 강화를 촉진하고 있습니다. 중국의 전국적인 소아 치료 지침에 따르면, 중증 소아 환자의 경우 표준 치료를 시행하더라도 재발성 악화가 자주 보고되며, 이러한 경향은 환경적 요인과 복약 순응도 부족을 반영하고 있습니다. PM2.5, PM10, 이산화질소를 줄여 대기질을 개선하는 것이 소아의 호흡기 건강에 유익하다는 사실이 입증되었으며, 이는 공중보건 대책을 통해 장기적으로 증상 악화 빈도를 낮출 수 있음을 시사합니다. 이러한 추세에 따라 소아천식 치료 시장에서 증상 완화제의 처방량은 최저 수준을 유지하게 되며, 유지 요법제의 성장은 지속될 것입니다.

첨단 치료법의 높은 비용과 지불 주체 측의 장벽

미국의 의료 정책에서는 소아용 생물학적 제제에 대해 엄격한 조건이 설정되어 있으며, 치료를 계속하기 위해서는 알레르겐 민감도 또는 바이오마커 기준에 대한 증명, 흡입용 코르티코스테로이드로 증상이 충분히 조절되지 않는다는 사실의 입증, 최근의 폐기능 검사 결과, 그리고 치료 결과의 개선을 보여주는 증거가 필요합니다. 이로 인해 소아천식 치료 시장에서 치료 시작까지의 시간이 지연되고 있습니다. 이러한 요건들은 처방 의사, 전문 약국 및 지원 포털 간의 협력이 필요한 경우가 많아, 가족들에게 행정적 부담이 될 수 있습니다. 일부 보험 플랜의 기준에는 알레르기 표현형에 대한 특정 총 IgE 수치 범위, 응급 치료제 사용 감소 입증, 갱신 전 FEV1 개선 등이 포함되어 있으며, 이를 통해 고비용 제품에 대한 결과 기반의 지속적인 이용 관리가 제도화되어 있습니다. 각 제약사는 환자 지원 프로그램 및 직접 구매 모델을 통해 흡입제 가격을 인하하고 미국 내 접근성을 높임으로써, 합리적인 가격을 실현하기 위해 노력하고 있습니다. 그럼에도 불구하고, 접근성상의 장벽은 소아천식 치료 시장 전체에서 보급을 저해하는 단기적인 제약 요인으로 남아 있습니다.

부문별 분석

2025년에는 장기 관리 약물이 58.47%를 차지해, 이는 지침에 따른 ICS의 일상적 사용과 MART의 보급 확대를 반영한 것입니다. 한편, 즉각적인 효과가 있는 완화제는 2026년부터 2031년까지 연평균 성장률(CAGR) 6.45%를 나타낼 것으로 예측되며, 조절제 역시 마찬가지입니다. SABA 단독 요법의 회피 및 기저선에서 저용량 ICS 사용에 대한 광범위한 합의가 소아천식 치료 시장의 기반으로서 조절제를 지속적으로 뒷받침하고 있습니다. 소아천식 치료 시장은 5세 미만 아동에 대한 진단 절차가 명확해진 데 힘입어 성장하고 있습니다. 이로 인해 치료 시작 시기가 앞당겨지면서, 컨트롤러의 사용 기간이 길어지고 있습니다. 또한 중국의 국가 지침에서도 급성 위험을 줄이기 위한 기초로서 ICS가 강조되고 있으며, 이는 급성장하는 아시아태평양(APAC)에서 컨트롤러의 기반을 뒷받침하고 있습니다. 대기 오염 및 바이러스와 관련된 증상 악화의 변동성으로 인해, 치료를 받고 있는 소아 환자들 사이에서도 응급약 사용량이 유지되고 있으며, 이는 소아천식 치료 시장 내 신속 작용 치료제의 성장을 뒷받침하고 있습니다.

즉각적인 효과가 있는 치료제의 성장은 산불 연기와 도시 지역의 대기 오염과 같은 현상으로 인한 구조적 수요도 반영하고 있습니다. 이러한 요인들은 증상의 갑작스러운 악화를 부추기며, 신속한 치료 강화를 촉진합니다. MART(유지 요법과 필요 시 요법의 병용)의 사용이 확대됨에 따라, 현행 지침 하에서는 ICS와 포르모테롤의 병용이 유지 요법과 필요 시 요법의 역할을 모두 수행하기 때문에 유지 요법 약물과 즉효성 치료제의 경계가 모호해지고 있습니다. 복약 순응도를 개선하기 위한 행동 계획이나 기술 훈련은 응급약 사용을 억제할 수 있지만, 많은 1차 진료 경로에는 여전히 과제가 남아 있어, 이로 인해 소아천식 치료 시장 수요 다양성이 유지되고 있습니다. 환경적·계절적 요인으로 인해 신속한 완화 요법의 선택지가 더욱 확대되고 있는 상황에서도, 치료의 기반이 되는 장기 관리 약물의 역할은 앞으로도 지속될 전망입니다.

CAGR이란, CAGR을 의미하며, 2031년까지의 기간 동안 바이오의약품의 CAGR은 7.41%입니다. 흡입용 스테로이드제는 비용 대비 효과가 뛰어나고 치료 전 단계에서 핵심적인 위치를 차지하고 있어, 2025년에는 34.73%의 시장 점유율로 1위를 유지할 것으로 전망됩니다. 한편, 바이오의약품은 2031년까지의 기간 동안 연평균 성장률(CAGR)이 7.41%를 기록하며 가장 빠르게 성장할 것으로 전망됩니다. 이 지침에서는 저용량 ICS를 조기에 도입하거나, 중등도 질환에 대한 병용 요법을 권장하고 있으며, 이는 소아천식 치료 시장에서 ICS의 안전성 모니터링과 단계적 감량 원칙에 따라 고용량 ICS의 사용이 억제됨에 따라, 특정 표현형에서 병용 요법이나 표적 요법이 치료의 주도권을 분담할 기회가 생겨나고 있습니다. 바이오로직스의 성장세는 소아용 적응증 확대와 연 2회 투여 제제의 등장을 반영한 것으로, 이는 소아천식 치료 시장에서 치료 지속률을 높이고 환자의 편의성을 향상시키기 위한 것입니다.

제2형 염증성 천식에 대한 바이오마커 기반 치료 선택 및 제약사의 접근성 개선 도구가 전문의약품의 꾸준한 증가를 뒷받침하고 있지만, 한편으로 보험사는 급여 기준을 엄격하게 유지하고 있습니다. 소아천식 치료 업계에서는 판매량이 많은 제네릭 의약품과 판매량이 적은 전문의약품 간의 균형이 계속해서 유지되고 있으며, 이러한 구성이 주요 포트폴리오의 이익률 추이를 좌우하고 있습니다.

지역별 분석

북미는 2025년에 36.41%의 점유율을 차지해, 이는 1인당 지출액이 높고 생물학적 제제가 조기에 도입된 점을 반영한 것입니다. 한편, 아시아·태평양 지역은 2026년부터 2031년까지 연평균 성장률(CAGR) 11.52%를 기록하며 가장 빠르게 성장하는 지역이 될 전망입니다. 미국과 캐나다에서는 SABA 단독 요법에 대한 지침과 1차 진료 단계에서 조기 ICS(흡입 스테로이드) 사용의 중요성이 강조됨에 따라 조절제 사용이 지속되고 있으며, 이것이 소아천식 치료 시장의 기반을 지탱하고 있습니다. 대기 오염으로 인한 증상 악화로 인해 산불 시즌 동안 응급약 사용이 급증하고 있으며, 이로 인해 단기적인 판매량에 변동이 발생하고 있습니다. 지급자 측의 단계적 확대 제한 및 수량 제한 등의 정책으로 인해, 전문 치료제의 도입 속도는 완만해졌으며, 보험 적용은 충분히 기록된 중증 사례에 집중되고 있습니다.

아시아태평양에서는 도시화와 전문의에 대한 접근성 개선으로 진단 및 치료가 확대되고 있으며, 소아 의료 분야에서 ICS를 핵심으로 하는 국가 지침에 힘입어 성장을 주도하고 있습니다. 중국에서 소아용 표적 치료제의 승인과 국제 지침에 기반한 조기 진단 기준 덕분에, 주요 도시 지역에서는 표현형에 기반한 치료로 꾸준히 전환되고 있습니다. 흡입기 사용 교육 및 스페이서, DPI에 대한 접근성은 점차 개선되고 있지만, 자원이 부족한 지역에서는 여전히 불균형한 상태이며, 이로 인해 소아천식 치료 시장에서 다양한 치료법의 조합이 유지되고 있습니다. 주요 시장에서 중산층을 대상으로 한 보험 적용이 확대되는 가운데, 혈당 조절제 복용 준수 프로그램과 학교를 거점으로 한 시범 사업이 치료의 보급 범위를 넓힐 준비를 마쳤습니다.

유럽에서는 각국의 지침 간 조화와 중증 환자에 대한 기술 평가를 바탕으로 여전히 큰 시장 점유율을 유지하고 있지만, 탈탄소화 정책에 따라 흡입기 제품 포트폴리오와 입찰 동향이 재편되고 있습니다. EMA(유럽의약품청)의 저 GWP(지구온난화지수) 추진제 지지 및 관련 기기 요건은 지난 10년 동안 제조 계획의 재편을 촉진해 왔으며, 특정 조달 건에서는 일시적으로 DPI나 소프트 미스트 방식의 기기가 우대받고 있습니다. 각국의 의료 제도에서도 소아 코호트를 대상으로 한 연결형 센서의 평가와, 복약 순응도 데이터를 1차 진료 워크플로우에 통합하기 위한 실용적인 방법론에 대한 검토가 진행되고 있습니다. 전반적으로, 유럽에서의 지침 채택과 지속가능성으로의 전환이 맞물려 소아천식 치료 시장의 다양한 제품 포트폴리오를 지속적으로 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

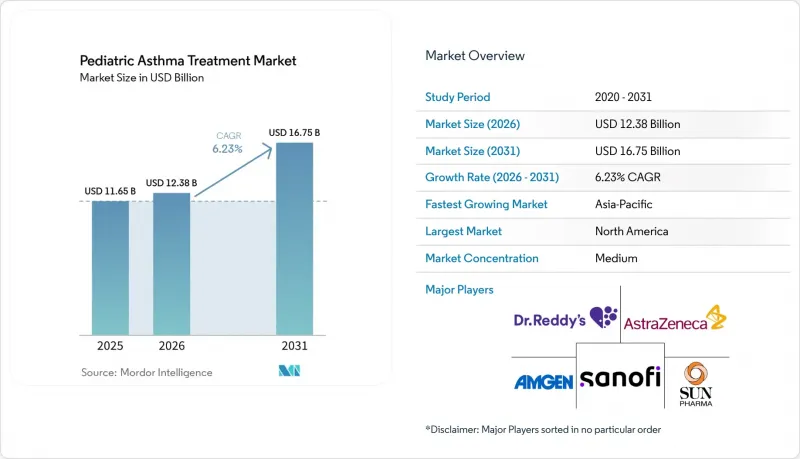

JHS 26.06.23According to Mordor Intelligence, the pediatric asthma treatment market size is projected to expand from USD 11.65 billion in 2025 and USD 12.38 billion in 2026 to USD 16.75 billion by 2031, registering a CAGR of 6.23% between 2026 to 2031.

This report is Segmented by Treatment Type (Long-Term Control Medications, and Quick-Relief Medications), Drug Class (Inhaled Corticosteroids, Long-Acting Beta Agonists, and More), Route of Administration (Inhaled, Oral, and Injectable), End User (Hospitals, Clinics, and Home Care), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasted in Terms of Value (USD).

Global Pediatric Asthma Treatment Market Trends and Insights

Rising Pediatric Asthma Prevalence and Earlier Diagnosis

Health agencies report a consistent pediatric asthma burden and persistent disparities, which continue to expand the treated pool within the pediatric asthma treatment market. Updated guidance now clarifies how to diagnose asthma in children under 5 by combining recurrent wheeze patterns, exclusion of other causes, and response to therapy, which moves intervention earlier and increases controller use. China's 2025 pediatric guideline reinforces inhaled corticosteroids as the foundation for reducing exacerbation risk and aligns clinic workflows around consistent controller access in the pediatric asthma treatment market. Longitudinal modeling for the Western Pacific Region projects continued increases in prevalence over the long term, which aligns with urbanization and allergen exposure patterns seen across the region. Routine biomarker use, such as FeNO and blood eosinophils, along with lung function testing from age 5, is becoming more common in outpatient settings, which supports earlier controller initiation and longer treatment duration. Together, these shifts support a stable base of multi-year therapy within the pediatric asthma treatment market.

Air Pollution and Respiratory Infections Elevate Exacerbations

The latest State of the Air report shows that 156.1 million people live in counties with unhealthy ozone or particulate levels, which sustains high rescue medication demand and emergency utilization for children in the pediatric asthma treatment market. EPA evidence links short-term PM2.5 exposure to higher asthma attack severity in children and documents chronic impacts on lung development, making exposure management a material clinical lever. These conditions reinforce the use of anti-inflammatory reliever strategies and controller intensification during high-risk seasons in the pediatric asthma treatment market. National pediatric guidance in China indicates that severe pediatric cases commonly report recurrent exacerbations despite standard therapies, a pattern that reflects environmental load and adherence gaps. Air quality improvements that reduce PM2.5, PM10, and nitrogen dioxide have documented benefits for pediatric respiratory health, which indicates that public health measures can lower exacerbation frequency over time. These dynamics keep a floor under reliever volume and sustain controller growth in the pediatric asthma treatment market.

High Cost and Payer Barriers for Advanced Therapies

US medical policies set rigorous conditions for pediatric biologics that require documented allergen sensitivity or biomarker criteria, demonstration of inadequate control on inhaled corticosteroids, recent pulmonary function testing, and evidence of improved outcomes to continue therapy, which slows time to treatment in the pediatric asthma treatment market. These requirements often introduce coordination across prescribers, specialty pharmacies, and assistance portals, which can add administrative friction for families. Several plan criteria include specific total IgE ranges for allergic phenotypes, proof of decreased rescue use, and improved FEV1 before renewal, which formalizes outcomes-based continuous-term utilization management on high-cost products. Manufacturers are addressing affordability with patient assistance programs and direct purchasing models that lower pricing on inhaled medicines and improve availability in the United States. Even so, access frictions remain a near term limiter on uptake across the pediatric asthma treatment market.

Other drivers and restraints analyzed in the detailed report include:

- Guideline Shift to ICS-Containing Regimens Increases Controller Use

- Pediatric Biologic Label Expansions and Access Programs

- Safety Warnings and Side Effects Affecting Long-Term Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Long-term control medications held 58.47% in 2025, reflecting guideline-anchored daily ICS use and wider MART adoption, while quick relief options are projected to grow at 6.45% CAGR in 2026 to 2031 and controllers. Broader alignment around no SABA-only management and the use of low-dose ICS at baseline continues to support controllers as the bedrock of the pediatric asthma treatment market. The pediatric asthma treatment market benefits from clearer diagnostic pathways under age 5, which moves therapy earlier and lengthens time on controllers. National guidance in China also emphasizes ICS as the cornerstone for reducing acute risk, supporting the controller base in fast-growing APAC settings. Exacerbation volatility tied to pollution and viruses sustains rescue volumes even among treated children, which keeps quick relief options growing inside the pediatric asthma treatment market.

Quick relief growth also reflects structural demand from wildfire smoke events and urban air quality episodes, which intensify breakthrough symptoms and prompt swift treatment escalation. As MART use spreads, the boundary between controller and reliever blurs, since ICS formoterol serves both maintenance and as needed roles under current guidance. Action plans and technique training that improve adherence can moderate rescue use, but gaps remain in many primary care pathways, which maintains demand diversity in the pediatric asthma treatment market. Long term control medications that anchor role is likely to persist even as quick relief options post higher growth on environmental and seasonal dynamics.

Inhaled corticosteroids led with 34.73% in 2025 due to their efficacy to cost profile and central position across all treatment steps, while biologics are the fastest growing class with a 7.41% CAGR outlook to 2031. Guidance endorses low-dose ICS early and supports combination use for moderate disease, which stabilizes ICS volume in the pediatric asthma treatment market. Safety monitoring and step-down principles help contain high-dose ICS usage, creating opportunities for combinations and targeted options to share control in selected phenotypes. Biologic momentum reflects pediatric label expansions and the arrival of twice-yearly dosing, which aim to improve persistence and patient convenience in the pediatric asthma treatment market.

Biomarker-guided selection for Type 2 inflammatory asthma and improved access tools from manufacturers are supporting a steady rise in specialty use, while payers maintain rigorous criteria for coverage. The pediatric asthma treatment industry continues to balance high volume generics with low volume specialty products, a mix that defines margin trajectories for leading portfolios.

Geography Analysis

North America commanded 36.41% in 2025, reflecting high per capita spending and early adoption of biologics, while the Asia Pacific is the fastest-growing region at an 11.52% CAGR from 2026 to 2031. Guidance against SABA-only regimens and the emphasis on early ICS across primary care sustain controller use in the United States and Canada, which underpins the base of the pediatric asthma treatment market. Pollution-related exacerbations have intensified rescue patterns during wildfire seasons, adding volatility to short-term volumes. Payer policies with step edits and quantity limits moderate specialty adoption curves and keep coverage concentrated among well-documented severe cases.

Asia Pacific leads growth as urbanization and better access to specialists expand diagnosis and treatment, supported by national guidance that centers on ICS in pediatric care. Pediatric approvals for targeted therapies in China and earlier diagnosis criteria from global guidance support a steady shift toward phenotype-guided care in major urban centers. Device education and access to spacers and DPIs are improving but remain uneven across lower resource settings, which sustains a wide therapy mix in the pediatric asthma treatment market. As middle income coverage expands in large markets, controller adherence programs and school based pilots are poised to extend reach.

Europe sustains a significant share supported by national guideline alignment and technology appraisals for severe cases, while decarbonization policies reshape inhaler portfolios and tender dynamics. The EMA's support for low GWP propellants and associated device requirements are reshuffling manufacturing plans through this decade and temporarily favoring DPIs or soft mist devices in certain procurements. National health systems are also evaluating connected sensors for pediatric cohorts and assessing practical pathways to integrate adherence data into primary care workflows. Overall, Europe's combination of guideline adoption and sustainability transitions continues to support diversified portfolios in the pediatric asthma treatment market.

- Amgen

- AstraZeneca

- Boehringer Ingelheim

- Chiesi Farmaceutici

- Cipla Limited B.V.

- Covis Pharma

- Dr. Reddy's Laboratories Ltd.

- GlaxoSmithKline

- Glenmark Pharmaceuticals

- Hikma Pharmaceuticals

- Lupin

- Novartis

- Orion

- Regeneron Pharmaceuticals

- F. Hoffmann-La Roche Ltd (Genentech, Inc.)

- Sanofi

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Pediatric Asthma Prevalence and Earlier Diagnosis

- 4.2.2 Air Pollution and Respiratory Infections Elevate Exacerbations

- 4.2.3 Guideline Shift to ICS-Containing Regimens Increases Controller Use

- 4.2.4 Pediatric Biologic Label Expansions and Access Programs

- 4.2.5 Smart Inhaler Adherence Programs in Schools and Primary Care

- 4.2.6 At-Home Autoinjectors Enabling Home Dosing and Persistence

- 4.3 Market Restraints

- 4.3.1 High Cost And Payer Barriers for Advanced Therapies

- 4.3.2 Safety Warnings and Side Effects Affecting Long-Term Use

- 4.3.3 Decarbonization-Driven pMDI Propellant Transition And Reformulation Drag

- 4.3.4 Pediatric Inhaler Technique Variability Undermining Real-World Efficacy

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Treatment Type

- 5.1.1 Long-term Control Medications

- 5.1.2 Quick-relief Medications

- 5.2 By Drug Class

- 5.2.1 Inhaled Corticosteroids

- 5.2.2 Long-Acting Beta Agonists

- 5.2.3 Leukotriene Receptor Antagonists

- 5.2.4 Short-Acting Beta Agonists

- 5.2.5 Long-Acting Muscarinic Antagonists Combination Inhalers

- 5.2.6 Biologics

- 5.2.7 Others

- 5.3 By Route of Administration

- 5.3.1 Inhaled

- 5.3.2 Oral

- 5.3.3 Injectable

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Clinics

- 5.4.3 Home Care

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Amgen Inc.

- 6.3.2 AstraZeneca PLC

- 6.3.3 Boehringer Ingelheim International GmbH

- 6.3.4 Chiesi Farmaceutici S.p.A.

- 6.3.5 Cipla Limited B.V.

- 6.3.6 Covis Pharma

- 6.3.7 Dr. Reddy's Laboratories Ltd.

- 6.3.8 GlaxoSmithKline plc

- 6.3.9 Glenmark Pharmaceuticals Ltd.

- 6.3.10 Hikma Pharmaceuticals PLC

- 6.3.11 Lupin Limited

- 6.3.12 Novartis AG

- 6.3.13 Orion Corporation

- 6.3.14 Regeneron Pharmaceuticals, Inc.

- 6.3.15 F. Hoffmann-La Roche Ltd (Genentech, Inc.)

- 6.3.16 Sanofi SA

- 6.3.17 Sun Pharmaceutical Industries Ltd.

- 6.3.18 Teva Pharmaceutical Industries Ltd.

- 6.3.19 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment