|

시장보고서

상품코드

2063594

병원용 로봇 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Hospital Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

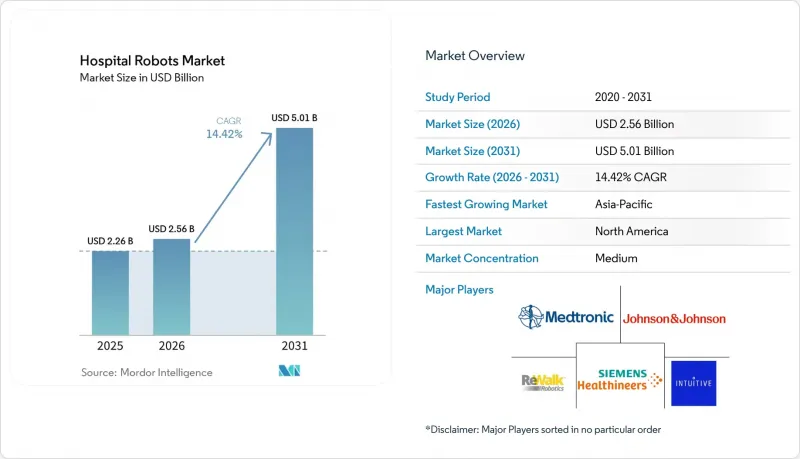

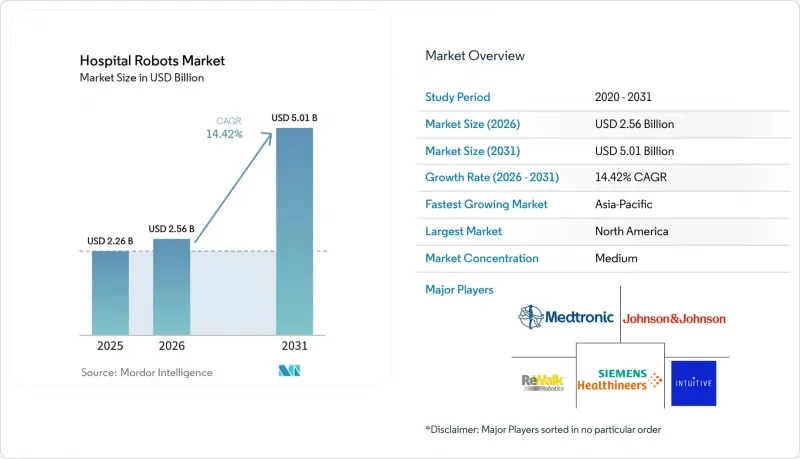

Mordor Intelligence에 의하면, 병원용 로봇 시장 규모는 2025년에 22억 6,000만 달러, 2026년에 25억 6,000만 달러, 2031년까지 50억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 14.42%로 성장할 전망입니다.

본 보고서는 제품 유형(외과용, 재활용, 서비스·물류용, 소독용, 텔레프레즌스용, 약국 자동화용), 용도(외과 수술, 재활, 물류, 청소, 환자 참여, 조제), 구성 요소(하드웨어, 소프트웨어, 서비스), 최종 사용자(종합병원, 전문병원, 당일 수술센터(ASC), 기타), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

전 세계 병원용 로봇 시장 동향과 인사이트

팬데믹 이후 감염 예방 대책에 대한 관심 고조

병원은 UV-C 소독 예산을 유지하고 있습니다. 이는 자동 순환 시스템을 통해 수술실이나 중환자실 내의 병원체 농도가 수 분 이내에 감소되어, 수술 부위 감염으로 인한 고액의 재입원 비용을 절감할 수 있기 때문입니다. LightStrike+는 3,500만 사이클 이상을 완료했으며, ISO 15883을 준수하는 감사 로그를 제공함으로써 Joint Commission(미국 의료기관 평가 기관)의 심사를 간소화합니다. 코로나19 기간 동안 이 플랫폼을 도입한 의료기관에서는 포괄지불제 하에서 병원 내 감염이 불이익 대상이 되기 때문에 지속적인 이용 사례가 보고되고 있습니다. FDA의 510(k) 승인을 통해 생체의공학 엔지니어들은 일상적인 유지보수가 기존 프로토콜을 준수하고 있음을 확신할 수 있습니다. 설비 투자 예산이 회복되는 가운데, 소독 로봇은 병원 내 로봇 시장의 보다 광범위한 도입을 향한 가시적인 첫걸음으로 자리매김하고 있습니다.

저침습 수술의 급속한 보급

Intuitive Surgical사의 da Vinci 5는 힘 피드백과 향상된 3D 시야 기능을 추가하여 기존의 촉각적 한계를 해소하는 동시에, 2026년에 새롭게 승인될 심장 수술 적응증을 가능하게 합니다. 동료 심사를 거친 연구에서는 여전히 비용 대비 효과에 대한 평가가 엇갈리고 있지만, 환자의 회복이 빨라진다는 점은 가치 기반 계약을 뒷받침하고 있습니다. 정형외과 프로그램도 비슷한 추세를 보이고 있으며, 스트라이커(Stryker)사의 마코(Mako) 플랫폼은 2025년에 무릎 및 고관절 수술 건수가 150만 건을 돌파할 것으로 예상되며, 워크플로우가 표준화됨에 따라 규모 확대 가능성이 입증되었습니다. 외과 의사들이 정밀도를 추구하는 한편, 환자들은 더 작은 절개를 원함에 따라, 이러한 발전들이 맞물려 병원용 로봇 시장은 두 자릿수 성장세를 유지하고 있습니다.

막대한 설비 투자와 ROI에 대한 우려

100만 달러에서 250만 달러에 달하는 도입 비용은 한 자릿수 이익률로 운영되는 병원에게 장벽이 되고 있습니다. 베어드사의 조사에 따르면, 경영진의 77%가 ROI 검증을 최우선 구매 기준으로 삼고 있으며, 71%는 여전히 내부 유보금을 자금원으로 활용하고 있습니다. 인튜이티브 서지컬(Intuitive Surgical)이나 스트라이커(Stryker)가 제공하는 사용량 기반 리스는 초기 비용을 줄여주는 반면, 이용 위험을 공급업체 측으로 전가하게 됩니다. 명확한 DRG 코드가 존재하지 않기 때문에 의료기관은 로봇 관련 비용을 기존의 보상액에 포함시키고 있으며, 이로 인해 수술 건수가 많은 시설이 우대받게 되어 중규모 의료기관에서의 단기적인 병원용 로봇 시장 보급이 제한되고 있습니다.

부문별 분석

2025년에는 외과용 로봇이 매출의 59.12%를 차지했습니다. 이는 8,000대 이상의 다빈치(da Vinci) 시스템 도입 실적에 더해, 마코(Mako)를 통한 150만 건의 수술 실적이 견인한 정형외과 분야에서의 도입 가속화에 기인한 것입니다. 재활 플랫폼 시장은 고령화의 진행과 로봇 보행 요법을 통한 비용 절감을 인식한 보험사들의 지원에 힘입어, 2031년까지 연평균 성장률(CAGR) 15.06%를 나타낼 것으로 전망됩니다. 뇌졸중 및 척수 손상의 유병률이 높아짐에 따라, 이 분야의 성장률은 병원용 로봇 시장 전체의 연평균 성장률(CAGR)을 상회할 것입니다.

존슨앤드존슨의 ‘Ottava(오타바)’가 FDA 심사에 들어갔고, 설치 공간에 드는 비용을 절감해 준다는 테이블 일체형 디자인이 등장하면서 경쟁이 치열해지고 있습니다. Moxi나 Aethon의 TUG와 같은 서비스·물류 유닛은 검체, 린넨, 식사의 운반을 자동화함으로써 수익원을 다각화하고 있습니다. 소독 로봇과 텔레프레즌스 로봇은 여전히 틈새 시장이지만, 전략적으로 중요하며, 감염 예방 및 원격 진료 프로그램을 뒷받침함으로써 지속적으로 진화하고 있는 병원용 로봇 시장을 주도하고 있습니다.

2025년에도 로봇 보조 전립선 전적출술, 자궁 전적출술, 대장 절제술이 고액 보험 급여 대상에 포함됨에 따라, 외과 분야는 47.38%의 점유율을 유지했습니다. 재활 분야는 연평균 성장률(CAGR) 15.67%를 나타낼 것으로 예측되며, 2025년 ReWalk 7의 승인을 계기로 보험사들이 외래 외골격 치료 및 재택 이용을 허용하게 되면서 성장세가 가속화되고 있습니다.

약국 업무가 Moxi로 전환됨에 따라 물류 및 배송량이 증가했고, 간호사의 근무 시간이 확보되었으며, 약품 처리 간격이 단축되었습니다. LightStrike+가 감염 관리 지표를 지원하기 때문에 팬데믹 이후에도 청소 업무에 대한 도입은 계속되고 있습니다. 원격 진료의 도입 규모는 여전히 작지만, 영양 지도 및 전문의 상담의 적용 범위는 확대되고 있습니다. 이 모든 것을 종합해 보면, 병원용 로봇 시장은 수술실의 범위를 넘어 확장되고 있습니다.

지역별 분석

북미는 2025년에 매출의 38.83%를 차지해, 유리한 상환 제도와 풍부한 도입 실적을 바탕으로 성장하고 있습니다. 대도시권의 의료 시스템은 포화 상태에 이르렀기 때문에 성장은 외래 진료 시설이나 소규모 시스템으로의 전환을 추진하는 지역 병원으로 이동하고 있습니다. 캐나다는 주 정부 예산에 따른 설비 투자 제한으로 인해 미국에 뒤처지고 있지만, 멕시코에서는 민간 시설에서의 도입 사례가 곳곳에서 눈에 띕니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 16.14%로 성장할 것입니다. 이는 중국 지방 자치단체가 2급 도시에 수술용 로봇을 도입하기 위한 보조금과, 일본의 5G 원격 조작 기술 확산을 통한 지역 간 격차 해소가 뒷받침하고 있습니다. 인도의 민간 기업들은 의료 관광 수요를 흡수하기 위해 다빈치(da Vinci)와 마코(Mako) 장비에 투자하고 있으며, 이로 인해 병원용 로봇 시장의 보급률이 높아지고 있습니다.

유럽은 MDR(의료기기 규정)에 따른 승인 절차가 장기화되고 있음에도 불구하고 꾸준히 성장하고 있습니다. 독일, 프랑스, 영국이 도입을 주도하는 반면, 남유럽 및 동유럽 시장의 도입 속도는 완만합니다. 중동 및 남미는 여전히 초기 단계에 있지만, 걸프협력회의(GCC) 회원국의 병원과 브라질의 학술 기관에서는 임상적 가치를 입증하고 향후 확대를 위한 지침이 될 전략적인 시범 사업이 진행되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the hospital robots market size is projected to be USD 2.26 billion in 2025, USD 2.56 billion in 2026, and reach USD 5.01 billion by 2031, growing at a CAGR of 14.42% from 2026 to 2031.

This report is Segmented by Product Type (Surgical, Rehabilitation, Service & Logistics, Disinfection, Telepresence, Pharmacy Automation), Application (Surgery, Rehabilitation, Logistics, Cleaning, Patient Engagement, Medication Dispensing), Component (Hardware, Software, Services), End User (General Hospitals, Specialty Hospitals, Ascs, and Others), and Geography. Market Forecasts are in Value (USD).

Global Hospital Robots Market Trends and Insights

Heightened Post-Pandemic Focus on Infection Control

Hospitals maintain UV-C disinfection budgets because automated cycles reduce pathogen loads in operating rooms and ICUs within minutes, trimming costly readmissions tied to surgical-site infections. LightStrike+ has completed over 35 million cycles and provides ISO 15883-compliant audit logs that simplify Joint Commission reviews. Facilities that adopted the platform during COVID-19 report persistent usage as bundled payments penalize hospital-acquired infections. The FDA 510(k) clearance reassures biomedical engineers that routine maintenance fits existing protocols. As capital budgets rebound, disinfection robots remain a visible first step toward wider hospital robots market deployment.

Rapid Adoption of Minimally Invasive Surgery

Intuitive Surgical's da Vinci 5 adds force feedback and enhanced 3D vision, addressing earlier tactile gaps and enabling newly approved cardiac indications in 2026. Peer-reviewed studies still show mixed cost-outcome profiles, but faster patient recovery supports value-based contracts. Orthopedic programs mirror the trend; Stryker's Mako platform surpassed 1.5 million knee and hip procedures in 2025, confirming scale potential when pathways standardize workflows. Together, these advances sustain double-digit growth for the hospital robots market as surgeons seek precision and patients demand smaller incisions.

High Capital Expenditure and ROI Concerns

Acquisition prices ranging from USD 1 million to USD 2.5 million deter hospitals operating on single-digit margins. A Baird survey found 77% of executives rank ROI validation as the top purchasing criterion, and 71% still rely on retained earnings for funding. Usage-based leases from Intuitive Surgical and Stryker reduce upfront cash but shift utilization risk to vendors. Absent distinct DRG codes, facilities bundle robotic costs into existing reimbursements, favoring high-volume centers and limiting near-term hospital robots market adoption among mid-tier providers.

Other drivers and restraints analyzed in the detailed report include:

- Shortage of Clinical Staff and Rising Labor Costs

- Integration of 5G-Enabled Telerobotics

- Complex Regulatory and Credentialing Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surgical robots contributed 59.12% revenue in 2025, benefiting from an installed base of more than 8,000 da Vinci systems and accelerating orthopedic adoption driven by Mako's 1.5 million procedures. Rehabilitation platforms are on track for 15.06% CAGR through 2031, fueled by aging demographics and payers that recognize cost savings from robotic gait therapy. This pocket outpaces the overall hospital robots market CAGR as stroke and spinal cord injury prevalence rise.

Price competition intensifies as Johnson & Johnson's Ottava table-integrated design enters FDA review, promising reduced footprint costs. Service and logistics units such as Moxi and Aethon's TUG diversify revenue by automating specimen, linen, and meal transport. Disinfection and telepresence robots remain niche yet strategic, anchoring infection prevention and remote consultation programs that feed the evolving hospital robots market.

Surgery retained 47.38% share in 2025 because robotic prostatectomy, hysterectomy, and colorectal resections command premium reimbursement. Rehabilitation, projected at 15.67% CAGR, gains traction as insurers accept outpatient exoskeleton therapy and home use following ReWalk 7 clearance in 2025.

Logistics-delivery volumes rise as pharmacy runs shift to Moxi, freeing nursing time and reducing medication turnaround intervals. Cleaning deployments persist post-pandemic as LightStrike+ supports infection-control metrics. Remote engagement remains modest yet expands coverage for dietetic and specialist consults. Together, these indications broaden the hospital robots market beyond the operating suite.

Geography Analysis

North America contributed 38.83% revenue in 2025, underpinned by favorable reimbursement and a deep installed base. Saturation appears in large urban systems, so growth tilts toward ambulatory sites and community hospitals upgrading to compact systems. Canada trails the United States because provincial budgets limit capital purchases, while Mexico sees sporadic private installations.

Asia-Pacific advances at 16.14% CAGR through 2031, supported by China's provincial grants that install surgical robots in tier-2 cities and Japan's 5G teleoperation rollouts that bridge rural gaps. India's private groups invest in da Vinci and Mako units to capture inbound medical tourism, lifting hospital robots market penetration.

Europe grows steadily despite longer approval cycles under MDR. Germany, France, and the United Kingdom lead deployments, whereas Southern and Eastern markets adopt at a slower rate. The Middle East and South America remain in the early stages but display strategic pilots in Gulf Cooperation Council hospitals and Brazilian academic centers that prove clinical worth and inform future scaling.

- ABB Ltd.

- Aethon Inc. (ST Engineering)

- Cyberdyne

- Diligent Robotics Inc.

- Ekso Bionics

- F&P Robotics AG

- Intuitive Surgical

- Johnson & Johnson

- KUKA AG

- Medtronic

- Omnicell

- Panasonic Corporation

- ReWalk Robotics

- Siemens Healthineers

- Smiths Group

- Stryker

- Swisslog Healthcare (KUKA AG)

- Xenex Disinfection Services Inc.

- Yaskawa Electric Corp.

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened Post-Pandemic Focus on Infection Control

- 4.2.2 Rapid Adoption of Minimally-Invasive Surgery

- 4.2.3 Shortage of Clinical Staff & Rising Labor Costs

- 4.2.4 Integration of 5G-Enabled Telerobotics

- 4.2.5 Hospital-At-Home Logistics Pilots Using Mobile Robots

- 4.2.6 Growing Emphasis on Precision Medicine and Personalized Surgical Planning

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure & ROI Concerns

- 4.3.2 Complex Regulatory & Credentialing Pathways

- 4.3.3 Cyber-Physical Security Vulnerabilities

- 4.3.4 Shortage of Skilled Robotics Technicians & Maintenance Support

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Surgical Robots

- 5.1.2 Rehabilitation Robots

- 5.1.3 Service & Logistics Robots

- 5.1.4 Disinfection Robots

- 5.1.5 Telepresence Robots

- 5.1.6 Pharmacy Automation Robots

- 5.2 By Application

- 5.2.1 Surgery

- 5.2.2 Rehabilitation

- 5.2.3 Logistics & Supply Delivery

- 5.2.4 Cleaning & Disinfection

- 5.2.5 Patient Engagement & Monitoring

- 5.2.6 Medication Dispensing

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By End User

- 5.4.1 General Hospitals

- 5.4.2 Specialty Hospitals

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Rehabilitation Centers

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 ABB Ltd.

- 6.3.2 Aethon Inc. (ST Engineering)

- 6.3.3 Cyberdyne Inc.

- 6.3.4 Diligent Robotics Inc.

- 6.3.5 Ekso Bionics Holdings Inc.

- 6.3.6 F&P Robotics AG

- 6.3.7 Intuitive Surgical Inc.

- 6.3.8 Johnson & Johnson

- 6.3.9 KUKA AG

- 6.3.10 Medtronic

- 6.3.11 Omnicell Inc.

- 6.3.12 Panasonic Corporation

- 6.3.13 ReWalk Robotics Ltd.

- 6.3.14 Siemens Healthineers AG

- 6.3.15 Smith & Nephew plc

- 6.3.16 Stryker Corporation

- 6.3.17 Swisslog Healthcare (KUKA AG)

- 6.3.18 Xenex Disinfection Services Inc.

- 6.3.19 Yaskawa Electric Corp.

- 6.3.20 Zimmer Biomet Holdings Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment