|

시장보고서

상품코드

2063602

의료용 코팅 첨가제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Medical Coating Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

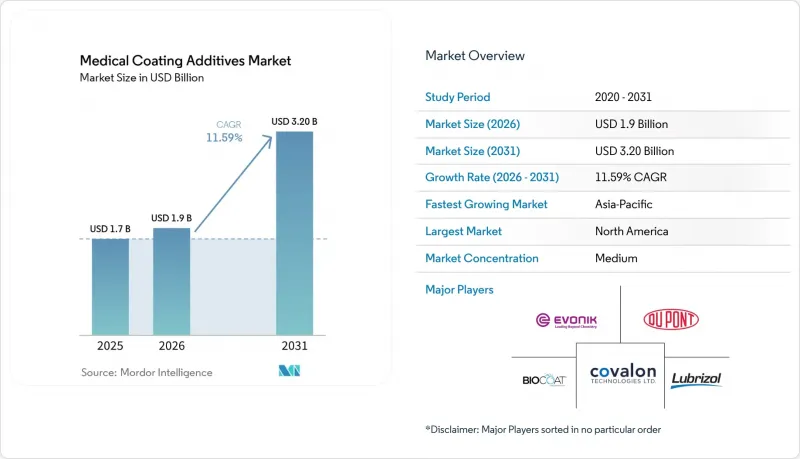

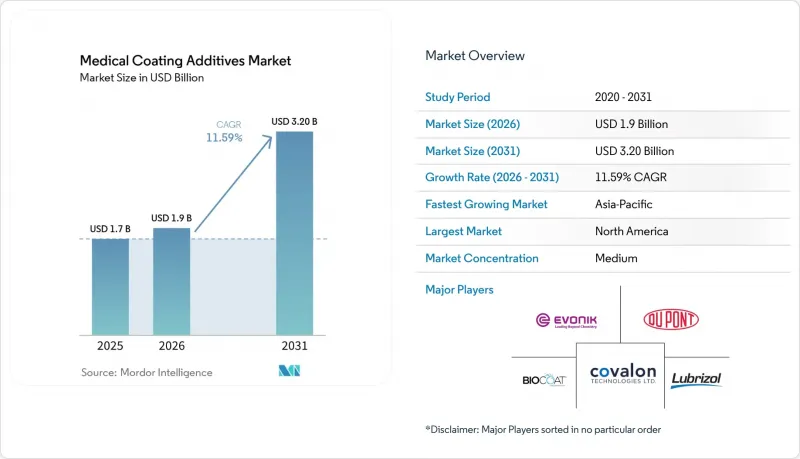

Mordor Intelligence에 의하면, 의료용 코팅 첨가제 시장 규모는 2025년 17억 달러에서 2026년에는 19억 달러로 확대되어 2031년까지 32억 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 11.59%로 성장할 전망입니다.

본 보고서는 첨가제의 기능(항균제 등), 첨가제의 화학 조성(실리콘 및 실리콘계 유체 등), 배합 유형(용제계, 수계 등), 용도(카테터·가이드와이어 등), 기판(금속, 폴리머 등), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 의료용 코팅 첨가제 시장 동향 및 인사이트

저침습 수술의 보급이 카테터 및 가이드와이어 수요를 끌어올리고 있습니다.

경피적 관상동맥 중재술, 경카테터 판막 교체술, 신경혈관 혈전 제거술 등의 시술이 보급됨에 따라, 윤활 코팅이 적용된 카테터 및 가이드와이어에 대한 전 세계적 수요는 계속해서 확대되고 있습니다. 기존에는 PTFE 미세 분말을 사용하여 0.05 미만의 마찰 계수를 실현했던 이러한 의료기기에서는 현재 친수성 코팅으로 폴리비닐피롤리돈, 폴리에틸렌글리콜 및 실리콘 오일의 혼합물이 점점 더 많이 사용되고 있습니다. 카테터 치료가 증가함에 따라 안전성에 대한 기대가 높아지면서, 윤활성과 항균성을 겸비한 의료기기에 대한 수요가 증가하고 있습니다.

병원 내 감염(HAI)이 미국 의료 시스템에 큰 부담으로 작용하고 있습니다.

병원 내 감염은 미국 의료 시스템에 연간 280억 달러 이상의 비용을 초래하고 있습니다. 이러한 재정적 압박에 더해, 보험 급여 감액 조치까지 겹치면서 병원들은 항균 코팅이 적용된 카테터나 임플란트의 도입을 촉진하고 있습니다. 메티실린 내성 황색포도상구균(MRSA)과 클로스트리디움 디피실(C. difficile)은 중환자실(ICU) 환경에서 여전히 만연하고 있어, 은 이온, 산화아연, 4급 암모늄염 등의 첨가제에 대한 수요를 높이고 있습니다. 항균 용액으로 처리된 의료기기는 24시간 이내에 세균 수를 대폭 감소시키는 것으로 입증되었습니다. 독성 위험 평가 기준을 준수하는 것은 검증 비용을 증가시킬 가능성이 있지만, 동시에 항균 기술에 대한 수요를 더욱 높이는 결과로 이어지고 있습니다.

엄격한 생체적합성 및 MDR/ISO 10993 요건으로 인해 시장 출시까지의 기간이 연장됨

EU의 MDR에서 의무화하고 있는 추출물 및 용출물에 관한 시험은 제제 1개당 15,000-5만 달러의 비용이 소요되며, 승인까지의 기간을 최대 18개월까지 연장시킵니다. ISO 10993-5의 세포독성 시험 및 ISO 10993-10의 감작성 시험에서는 일반적인 품질 관리 과정에서 간과되기 쉬운 잔류 광개시제나 윤활제가 종종 확인되므로, 배합을 재검토해야 합니다. FDA와 MDR의 추출 조건에 대한 이중 준수 요건은 특히 인증 시험소에 대한 접근이 제한적인 아시아태평양의 OEM 업체들에게 시험 부담을 더욱 가중시킵니다.

부문별 분석

2025년, 항균 첨가제는 28.16%의 시장 점유율을 차지하며 의료용 코팅 첨가제 시장을 주도했습니다. 은 이온, 산화아연 및 4급 암모늄계는 병원의 조달 기준을 충족하며, 감염 관리에 대한 보상 인센티브와도 부합합니다. 그러나 EPA와 EU의 살생물제 규제에 따른 서로 다른 승인 절차로 인해 전 세계 시장 출시 일정이 지연되고 있습니다. 저침습 수술로의 전환과 PFAS의 단계적 폐지를 배경으로, 미끄럼성 개량제는 급속한 성장을 이루고 있습니다. 2031년까지 의료용 코팅 첨가제 시장에서 미끄럼성 개질제 시장 점유율은 230 베이시스 포인트 증가할 것으로 예측됩니다. 이러한 성장은 PTFE 미세 분말에서 실리콘 오일, 폴리에틸렌글리콜, 폴리비닐피롤리돈의 혼합물로 전환된 데 기인하며, 주요 윤활성 기준을 유지하고 있습니다.

2025년에는 실리콘이 매출의 26.15%를 차지했습니다. 이는 실리콘이 타의 추종을 불허하는 열 안정성, 표면 에너지 저감 능력, 그리고 멸균에 대한 내성을 갖추고 있기 때문입니다. 그러나 실리콘의 이화는 후속 공정인 인쇄나 접착에 지장을 줄 가능성이 있습니다. 이 과제로 인해 배합 설계자들은 새로운 규제 기준치를 밑돌도록 사이클로실록산 함유량을 제한하고 있습니다. 2031년까지 의료용 코팅 분야의 무기 나노 첨가제 시장 규모는 해당 부문에서 가장 높은 연평균 성장률(CAGR)인 14.98%를 나타낼 것으로 전망됩니다. 1중량% 미만의 첨가량으로도 효과를 발휘하는 은 나노입자는 항균 효과를 나타내며, 한편 자외선 차단과 항균성을 모두 갖춘 산화아연 나노입자는 웨어러블 기기나 이식형 기기에서 점점 더 선호되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 36.71%를 차지했습니다. 이는 1인당 의료비 상승, 중재적 심장학의 보급, 그리고 클래스 III 의료기기에 대한 확립된 규제 절차에 힘입은 결과입니다. FDA의 VHP 멸균 승인 및 EPA의 에틸렌옥사이드(EtO) 배출 제한으로 인해 재인증을 위한 예산이 필요해지면서, 강력한 연구개발(R&D) 및 규제 대응 팀을 보유한 기존 공급업체들이 혜택을 보고 있습니다. 멕시코에서 니어쇼어링이 급증함에 따라 카테터 및 주사기 조립 능력은 향상되고 있지만, 이 지역은 여전히 미국 및 유럽산 고순도 실란과 UV 올리고머 수입에 의존하고 있습니다.

2025년, 유럽은 독일의 제조 역량과 영국의 의료 기술 허브에 힘입어 큰 시장 점유율을 유지했습니다. 그러나 EU의 MDR(의료기기 규정)에 따른 화학적 특성 평가 의무화로 인해 검증 기간이 길어지고 비용이 증가하고 있어, 중소기업에게는 과제가 되고 있습니다. 독일의 정형외과용 임플란트 분야는 항균성 나노 실버 분말 수요를 주도하고 있는 반면, 프랑스의 카테터 산업은 EU의 그린 딜에 부합하기 위해 자외선 경화형이며 용제를 포함하지 않는 탑코트를 채택하고 있습니다. 아시아태평양은 2031년까지 14.56%라는 가장 높은 연평균 성장률(CAGR)을 기록하며 시장을 주도할 것으로 전망됩니다. 중국의 규제 개혁에 따라 의료기기 등록이 가속화되고 있으며, 실리콘 오일 및 나노 은 첨가제의 현지 조달이 진행되고 있습니다. 인도에서는 카테터 및 임플란트용 코팅 생산 라인을 구축하기 위해 생산 연계형 인센티브(PLI)가 활용되고 있지만, 고순도 유기실란공급망이 파편화되어 있다는 과제는 여전히 남아 있습니다. 한편, 아세안(ASEAN)의 의료기기 지침에 따라 표시 및 성능 시험 기준이 통일됨에 따라, 여러 국가에서 제품을 출시하는 데 드는 비용이 절감될 뿐만 아니라, 해당 지역의 OEM 제조업체들에게 시장 기회가 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the medical coating additives market size is expected to increase from USD 1.7 billion in 2025 to USD 1.9 billion in 2026 and reach USD 3.20 billion by 2031, growing at a CAGR of 11.59% over 2026-2031.

This report is Segmented by Additive Function (Antimicrobial, and More), Additive Chemistry (Silicones & Silicone Fluids, and More), Formulation Type (Solvent-Borne, Water-Borne, and More), Application (Catheters & Guidewires, and More), Substrate Material (Metals, Polymers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Coating Additives Market Trends and Insights

Minimally Invasive Procedures Boost Demand for Catheters and Guidewires

As procedures like percutaneous coronary intervention, transcatheter valve replacement, and neurovascular thrombectomy gain traction, the global demand for lubricious-coated catheters and guidewires continues to grow. These devices, which historically achieved friction coefficients below 0.05 with PTFE micropowders, are now increasingly utilizing blends of polyvinylpyrrolidone, polyethylene glycol, and silicone fluids for their hydrophilic coatings. The rise in catheter interventions, coupled with growing safety expectations, has driven the need for devices offering both lubricity and antimicrobial features.

Hospital-Acquired Infections (HAIs) Strain U.S. Healthcare

Hospital-acquired infections impose costs exceeding USD 28 billion annually on the U.S. healthcare system. These financial pressures, along with reimbursement penalties, are encouraging hospitals to adopt antimicrobial-coated catheters and implants. Methicillin-resistant S. aureus and C. difficile remain prevalent in intensive care settings, increasing the demand for additives such as silver-ion, zinc-oxide, and quaternary-ammonium. Devices treated with antimicrobial solutions have demonstrated significant bacterial reduction within 24 hours. While compliance with toxicological risk assessments can raise validation costs, it also reinforces the demand for antimicrobial technologies.

Stringent Biocompatibility and MDR/ISO 10993 Requirements Extend Time-To-Market

EU MDR-mandated extractables and leachables studies, costing USD 15,000 to 50,000 per formulation, extend approval cycles by up to 18 months. ISO 10993-5 cytotoxicity and ISO 10993-10 sensitization protocols often identify residual photoinitiators and slip agents overlooked by routine quality control, necessitating reformulation. The requirement for dual compliance with FDA and MDR extraction conditions further increases testing burdens, particularly for Asia-Pacific OEMs with limited access to accredited laboratories.

Other drivers and restraints analyzed in the detailed report include:

- Waterborne and UV/EB-Curable Systems Gain Traction Amid Stricter VOC Regulations

- FDA's 2024 Endorsement of VHP Sterilization Broadens Options for Heat-Sensitive Devices

- Intravascular Particulate Shedding Scrutiny Elevates Integrity Testing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, antimicrobial additives dominated the medical coating additives market with 28.16% shares. Silver-ion, zinc-oxide, and quaternary-ammonium systems meet hospital procurement standards and align with infection-control reimbursement incentives. However, varying pathways under the EPA and EU Biocidal Products Regulation extend global launch timelines. Slip modifiers are experiencing rapid growth, driven by a shift toward minimally invasive procedures and the phase-out of PFAS. By 2031, the market share for slip modifiers in medical coating additives is expected to increase by 230 basis points. This growth is attributed to the transition from PTFE micropowders to blends of silicone fluids, polyethylene glycol, and polyvinylpyrrolidone, maintaining key lubricity benchmarks.

In 2025, silicones accounted for 26.15% of revenue, driven by their unmatched thermal stability, ability to reduce surface energy, and tolerance to sterilization. However, silicone migration can disrupt downstream printing and adhesive bonding. This challenge has led formulators to limit cyclic siloxane content below emerging regulatory thresholds. By 2031, the market size for inorganic nano-additives in medical coatings will mark the segment's fastest CAGR at 14.98%. Silver nanoparticles, effective at sub-1 wt% loading, offer antimicrobial benefits, while zinc oxide nanoparticles, with their dual UV protection and antibacterial properties, are increasingly favored for wearable and implantable devices.

Geography Analysis

In 2025, North America accounted for 36.71% of global revenue, driven by high per-capita health spending, widespread adoption of interventional cardiology, and established regulatory pathways for Class III devices. The FDA's recognition of VHP sterilization and the EPA's EtO emission limits necessitate requalification budgets, benefiting established suppliers with robust R&D and regulatory teams. While Mexico's near-shoring surge increases its capacity for catheter and syringe assembly, the region continues to rely on imports of high-purity silanes and UV oligomers from the United States and Europe.

Europe held a significant market share in 2025, supported by Germany's manufacturing strength and the United Kingdom's med-tech hubs. However, the EU's MDR mandates on chemical characterization are extending validation timelines and increasing costs, creating challenges for SMEs. Germany's orthopedic implant sector is driving demand for antimicrobial nano-silver powders, while France's catheter industry is adopting UV-curable, solvent-free topcoats to align with the EU's Green Deal. The Asia-Pacific region is set to lead with the highest CAGR of 14.56% through 2031. China's regulatory reforms are accelerating device registrations and encouraging local sourcing of silicone fluids and nano-silver additives. In India, Production-Linked Incentives (PLI) are being utilized to establish lines for catheter and implant coatings, although challenges persist with supply-chain fragmentation for high-purity organosilanes. Meanwhile, ASEAN's Medical Device Directive is harmonizing labeling and performance testing, reducing costs for multi-country launches and expanding market opportunities for regional OEMs.

- Allnex Holding S.a r.l.

- Arkema S.A.

- Avient Corporation

- Biocoat

- BioCote Ltd.

- Clariant AG

- Covalon Technologies

- Covestro

- DuPont

- Elkem ASA

- Evonik Industries AG:

- Henkel

- Lubrizol

- Microban Products Company

- Mitsubishi Chemical Corp.

- Momentive Performance Materials Inc.

- SANITIZED AG

- Shamrock Technologies, Inc.

- Solvay SA

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Minimally Invasive Procedures Expand Catheter and Guidewire Volumes

- 4.2.2 Healthcare-Associated Infection (HAI) Burden

- 4.2.3 Shift To Waterborne and UV/EB-Curable Systems to Meet VOC/Sustainability Goals and Raise Line Productivity

- 4.2.4 Recognition Of VHP Sterilization Expands Modality Options Tightening Additive Compatibility Requirements

- 4.2.5 EtO Emissions Rule Drives Revalidation of Sterilization-Compatible Coating Chemistries and Additives

- 4.2.6 PFAS Restriction Trajectory Accelerates Reformulation Toward Silicone/Silane/Wax

- 4.3 Market Restraints

- 4.3.1 Stringent Biocompatibility and MDR/ISO 10993 Requirements Extend Time-To-Market and Raise Costs

- 4.3.2 Intravascular Particulate Shedding Scrutiny Elevates Coating Integrity Testing and Failure Risk

- 4.3.3 Sterilization Material Compatibility Limits Like VHP Packaging And Process Constraints Complicate Scaling

- 4.3.4 PFAS Substitution Risks Including Performance Tradeoffs Long Validations and Analytics Limits Slow Adoption

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Additive Function

- 5.1.1 Antimicrobial Additives

- 5.1.2 Slip/Lubricity Modifiers

- 5.1.3 Adhesion Promoters

- 5.1.4 Crosslinkers/Curing Agents

- 5.1.5 Photoinitiators/UV Stabilizers

- 5.1.6 Wetting/Flow/Leveling & Defoamers

- 5.1.7 Biocompatible Pigments/UV Absorbers

- 5.2 By Additive Chemistry

- 5.2.1 Silicones & Silicone Fluids

- 5.2.2 Organosilanes

- 5.2.3 Fluoropolymers/PTFE Micropowders

- 5.2.4 Polyurethane-based Additives

- 5.2.5 Acrylics/Methacrylates (UV)

- 5.2.6 Inorganic Nano-additives

- 5.2.7 Polyolefin Waxes & Specialty Biobased Polymers

- 5.3 By Formulation Type

- 5.3.1 Solvent-borne

- 5.3.2 Water-borne

- 5.3.3 100% Solids UV/EB-curable

- 5.3.4 Solventless Silicone Systems

- 5.4 By Application

- 5.4.1 Catheters & Guidewires

- 5.4.2 Syringes & Needles

- 5.4.3 Implantable Devices

- 5.4.4 Surgical Instruments & Electrosurgery

- 5.4.5 Diagnostics & Consumables

- 5.4.6 Wound Care & Dressings

- 5.5 By Substrate Material

- 5.5.1 Metals

- 5.5.1.1 Stainless steel

- 5.5.1.2 Nitinol

- 5.5.1.3 Titanium

- 5.5.2 Polymers

- 5.5.2.1 Polyolefins (PE, PP)

- 5.5.2.2 Polyurethanes/TPU, Pebax, Nylon

- 5.5.2.3 PEEK, PVC, PC

- 5.5.3 Elastomers

- 5.5.4 Glass & Composites

- 5.5.1 Metals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of APAC

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of MEA

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Allnex Holding S.a r.l.

- 6.3.2 Arkema S.A.

- 6.3.3 Avient Corporation

- 6.3.4 Biocoat

- 6.3.5 BioCote Ltd.

- 6.3.6 Clariant AG

- 6.3.7 Covalon Technologies Ltd.

- 6.3.8 Covestro AG

- 6.3.9 DuPont

- 6.3.10 Elkem ASA

- 6.3.11 Evonik Industries AG:

- 6.3.12 Henkel AG & Co. KGaA

- 6.3.13 Lubrizol Corporation

- 6.3.14 Microban Products Company

- 6.3.15 Mitsubishi Chemical Corp.

- 6.3.16 Momentive Performance Materials Inc.

- 6.3.17 SANITIZED AG

- 6.3.18 Shamrock Technologies, Inc.

- 6.3.19 Solvay SA

- 6.3.20 Wacker Chemie AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment