|

시장보고서

상품코드

2063603

히드로코르티손 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Hydrocortisone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

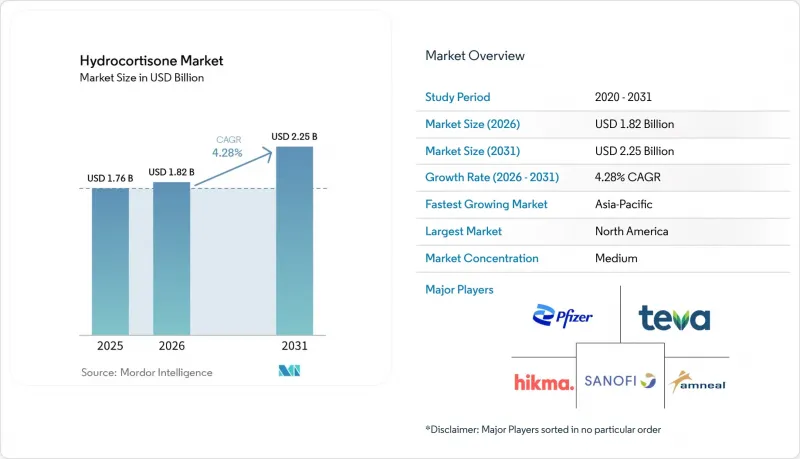

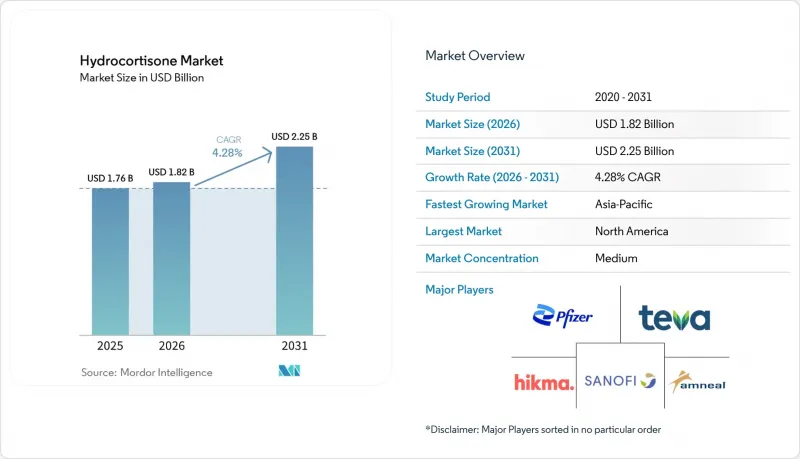

Mordor Intelligence에 의하면, 히드로코르티손 시장 규모는 2025년 17억 6,000만 달러, 2026년 18억 2,000만 달러에서 2031년까지 22억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 4.28%를 나타낼 것으로 예측됩니다.

본 보고서는 투여 경로(외용, 경구, 기타), 처방 유형(일반의약품(OTC), 처방약(Rx)), 유통 채널(병원 약국, 소매 약국, 온라인 약국), 적응증(피부과, 소화기계, 기타) 및 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 본 보고서에서는 상기 각 부문 시장 규모(달러)를 제시하고 있습니다.

세계 히드로코르티손 시장 동향 및 분석

WHO 필수 의약품 목록에 등재됨으로써 기본적인 수요와 처방집 등재가 보장됩니다.

2025년 9월에 재확인된 제24차 WHO 필수의약품 모델 목록에 히드로코르티손이 등재됨에 따라, 소득 수준에 관계없이 각국의 조달 및 공적 처방집에서 우선순위가 보장되고 있으며, 이를 통해 입찰 주도 환경 하에서 발생하는 급격한 대체로 인한 영향으로부터 히드로코르티손 시장을 안정시키고 있습니다. 2025년 제10판 WHO 소아용 필수의약품 모델 목록은 1mg/mL 경구액, 경구 과립제, 주사제를 포함한 보다 광범위한 소아용 제형을 규정함으로써, 소아의 대체 수요에 공급을 맞추는 동시에, 기존에는 복약 순응도를 저하시켰던 투여량 조정에 따른 대응 부담을 줄이고 있습니다. 아프리카 및 기타 지역의 국가 목록도 이러한 도입을 반영하고 있으며, 1차 의료 기관부터 3차 의료 기관에 이르기까지공급을 확보하고, 경구용 및 주사용 제제 모두에 대해 지속적인 기준 공급량을 강화하고 있습니다. 2026년에 진행 중인 WHO 전문가 위원회의 재검토를 통해, 중복되는 치료법에 대한 경쟁 장벽은 여전히 유지되고 있습니다. 그러나 히드로코르티손의 생리적 보충으로서의 역할과 응급 상황에서의 중요성을 고려할 때, 단기적으로는 목록에서 제외될 위험은 낮을 것으로 보입니다. 이러한 상황은 접근성을 높이는 동시에 공식 유통 채널에서의 가격 결정력을 억제하고 있어, 히드로코르티손 시장에 예측 가능하면서도 비용에 민감한 기반을 형성하고 있습니다.

OTC를 통한 접근성 확보로 자가 관리 및 소매 및 온라인 약국에 대한 접근성이 확대됩니다.

0.5-1% 농도의 일반의약품(OTC) 히드로코르티손은 의사의 진찰 없이도 경미한 피부 질환을 일상적으로 자가 관리할 수 있게 해주며, 2025년 처방약 부문에서 가장 큰 시장 점유율을 차지할 뿐만 아니라, 소비자가 원하는 ‘번거로움 없는 접근성’이라는 선호에도 부합합니다. 이러한 요인들이 복합적으로 작용하여 소매 및 디지털 채널 전반에 걸친 판매량의 견조한 성장세를 뒷받침하고 있습니다. 2025년 1월에 발효되는 미국 FDA의 ‘비처방약 사용에 관한 추가 조건’ 체계에 따라, 특정 OTC 의약품에 대해 기술을 활용한 자가 선택이 가능해집니다. 이는 안전한 자가 관리 과정을 지원하고, 그렇지 않았다면 치료를 미루고 있었을 소비자층의 구매 전환을 촉진할 가능성이 있습니다. 다만, 외용 스테로이드의 금단 위험에 대한 소비자의 인식이 높아지고 있는 것이 성장의 걸림돌이 되고 있으며, 일부 사용자들은 비스테로이드계 제품을 선호하는 추세입니다. 그럼에도 불구하고, 접근성이 뛰어난 일반의약품(OTC)은 경미한 염증에 대한 1차 치료의 기반으로서 여전히 중요한 역할을 하고 있습니다.

제네릭 의약품의 가격 압박과 치열한 경쟁이 이익률을 압박하고 있습니다.

히드로코르티손은 여러 제약사에 의해 경구제, 외용제, 주사제 등 다양한 제형으로 제조되고 있으며, 이로 인해 경쟁이 심화되면서 성숙한 적응증 분야에서 판매량을 크게 늘리지 못한 채 모든 유통 채널에 걸쳐 거래 마진을 압박하고 있습니다. 공급망에서 발생한 사건은 특정 제형의 취약점을 여실히 드러내고 있습니다. 영국에서는 2025년에 미리 조제된 히드로코르티손 주사액의 부족이 예상에 따라, 키트 조립에 적합한 소듐 코하박산 주사용 분말로 대체할 것을 권장했습니다. 이로 인해 구급 키트의 비축량은 유지되었지만, 단일 공급업체에 대한 의존 위험이 부각되었습니다. 이러한 환경 속에서 히드로코르티손 시장은 판매량은 안정적이지만 가격에 민감한 상태가 지속되고 있으며, 각 제약사는 수익성을 지키기 위해 틈새 시장에서 수익성이 높은 제제를 점점 더 우선시하고 있습니다.

부문별 분석

피부과 분야에서 일반의약품 및 처방약에 대한 수요가 증가함에 따라, 2025년 매출의 54.68%를 국소 투여제가 차지했습니다. 한편, 소아용 제품은 정확한 투여를 가능하게 하고 보호자에 의한 투여량 편차를 줄여주기 때문에 경구 제제는 2031년까지 연평균 성장률(CAGR) 5.98%로 가장 빠르게 성장할 것으로 예측됩니다. 이러한 추세는 예측 기간 동안 히드로코르티손 시장 규모 전망을 뒷받침하는 요인이 될 것입니다. 5세 이상 환자를 대상으로 한 Eton사의 경구용 액제 ‘KHINDIVI’는 2025년 5월 FDA 승인을 획득하고, 전문 약국의 지원을 받아 출시되었습니다. 이는 과립제 ‘ALKINDI SPRINKLE’을 보완하는 것으로, 임상적으로 정확한 투여가 중요한 환자군에서 투여 정확도를 높여줍니다. KHINDIVI의 첨부문서에서는 첨가제의 위험성으로 인해 5세 미만의 소아는 사용 대상에서 제외되어 있어, 이에 따라 적응증 대상이 제한되기는 하지만, 히드로코르티손 시장에서 연령에 따른 제제 개발에 대한 임상적 근거를 더욱 확고히 하고 있습니다. WHO의 EMLc 2025에는 정제 외에도 경구용 액제 및 과립제가 포함되어 있으며, 필수 의약품 목록이 조달을 주도하는 시장에서 소아 환자들의 접근성 확대를 위한 정책적 기반을 제공합니다.

외용 히드로코르티손은 경증 염증성 피부 질환의 1차 치료제로서 여전히 주류를 이루고 있으며, 이는 OTC(일반의약품)로서의 접근성, 환자의 익숙함, 그리고 단기 사용 시 위험-이익 프로파일이 양호하여 민감한 부위에 최저 용량 요법을 적용할 때 임상의가 느끼는 신뢰감에 힘입은 바 큽니다. 직장 투여는 소화기 계통을 표적으로 하는 투여 방법으로 자리매김하고 있으며, 크리스토콧(Cristocot)사의 차세대 90mg 히드로코르티손 아세테이트 좌약은 FDA 심사 결정 단계에 진입했고, 신약허가신청(NDA) 접수 시 공개된 3상 임상시험 결과에서 관해 효과를 보고함으로써 원위부 궤양성 대장염의 치료 옵션을 확대되고 있습니다. 투여 경로에 관계없이 히드로코르티손 업계는 국소 적응증에서의 유효성을 유지하면서 전신 노출을 최소화하는 투여법 개선에 투자를 집중하고 있으며, 이는 제네릭 의약품이 주류를 이루는 시장에서 지속적인 틈새 시장을 확보하기 위한 전략입니다. 응급 의료에 초점을 맞춘 투여 도구(임상 현장 외에서의 신속한 투여를 간소화하기 위한 노력을 포함)는 안전성과 부신 위기 대비가 동시에 중시되고 있음을 반영합니다. 이처럼 확고히 자리 잡은 외용제 분야의 리더십과 부상하고 있는 경구 정밀 투여 기술의 결합으로, 임상적 요구가 다양해지는 가운데 병원 및 재택치료 분야 모두에서 히드로코르티손 시장의 기반이 강화되고 있습니다.

OTC 제품은 경미한 증상에 대해 신속하고 번거롭지 않은 접근을 가능하게 함으로써, 2025년 매출의 57.88%를 차지했습니다. 그럼에도 불구하고, 소아과, 궤양성 대장염, 중환자 치료 분야에서 전문 의약품의 확대에 따라 처방전 경로는 2031년까지 연평균 성장률(CAGR) 6.34%로 더욱 빠르게 성장할 것으로 예상되며, 이러한 요인들이 복합적으로 작용하여 히드로코르티손 시장을 다각화하고 있습니다. 소아용 솔루션에 대한 전문적인 유통 경로와 본인 부담금 경감 프로그램은 복약 순응도의 장벽을 낮추고, 처방약(Rx)인 히드로코르티손을 단순한 일반 의약품이 아닌 정밀한 치료 도구로 자리매김하는 데 기여하고 있으며, 이것이 일반의약품(OTC)과의 성장 격차를 뒷받침하고 있습니다. 처방약 전용 주사제는 중환자실(ICU)이나 응급실에서 처치에 따라 사용되기 때문에 일반의약품(OTC)으로 대체되는 영향은 적으며, 프로토콜 준수 측면에서는 처방약 목록에 등재되는 것과 일관성을 우선시하기 때문입니다. OTC 히드로코르티손은 편의성, 합리적인 가격, 그리고 제품에 대한 폭넓은 인지도 덕분에 자가 관리형 피부과 치료의 주축으로 자리매김하고 있습니다. 이러한 특징들은 외용 스테로이드의 금단 증상에 대한 임상적 우려가 커지는 상황 속에서도 판매량 면에서의 우위를 공고히 하고 있습니다. 이와 동시에, 처방약 유통 채널은 의사의 감독이나 일반의약품 형태로는 재현할 수 없는 정확한 투여가 필요한 제제 및 적응증을 통해 가치를 창출하고 있으며, 이는 가격대나 의료 현장을 막론하고 히드로코르티손 시장의 균형을 유지하고 있습니다. 예측 기간 동안, 차별화된 처방약 제품과 병원 주도형 용도는 소비자의 심리적 변동에 덜 영향을 받는 임상적 틈새 시장을 공략하고 있기 때문에 더 빠른 성장세를 유지할 것입니다. 한편, OTC는 경미한 염증 증상을 보이는 폭넓은 계층을 계속해서 흡수해 나갈 것입니다.

지역별 분석

2025년에는 소아용 정밀 투여 기술이 성숙기에 접어들고 병원 프로토콜이 확고해짐에 따라, 북미가 매출의 38.34%를 차지했습니다. 한편, 아시아태평양은 2031년까지 연평균 성장률(CAGR) 5.21%로 가장 높은 성장률을 보일 것으로 예상되며, 이러한 양극화된 양상이 상환, 접근성, 유통 채널의 성숙도 측면에서 히드로코르티손 시장을 형성하고 있습니다. 미국 및 캐나다의 의료 제도에서는 부신 위기나 쇼크 관리 시 응급 처치를 위해 주사용 히드로코르티손이 병원 처방집에 등재되어 있습니다. 소아 부신 기능 부전은 필요에 따라 액제나 조제 제제를 포함한 만성적인 히드로코르티손 보충 요법으로 관리되며, 표준 약국 및 조제 경로를 통해 지원되고 있기 때문에 이 질환을 앓고 있는 환자들에게는 지속적인 처방 수요가 발생하고 있습니다. 디지털 약국의 확대와 당일 배송을 통한 물류 발전으로 환자 및 간병인에게 더욱 편리한 접근성이 확대되고 있는 반면, 임상 단체와 규제 당국은 적절한 외용 스테로이드 사용을 보장하기 위해 안전성 관련 정보를 지속적으로 업데이트하고 있습니다. 북미의 히드로코르티손 시장은 염증성 장 질환, 특히 궤양성 대장염에 대한 코르티코스테로이드 제제의 지속적인 혁신에 의해 형성되고 있습니다. 예를 들어, 2026년 4월 『MJH Life Sciences』지에 게재된 기사에 따르면, FDA가 직장 궤양성 대장염을 대상으로 한 차세대 히드로코르티손 아세테이트 좌약에 대한 신약 승인 신청(NDA)을 접수한 것은 만성 소화기 질환에서 전신성 부작용을 줄이면서 효능을 향상시키는 표적을 좁힌 국소 작용형 치료법에 대한 수요가 높아지고 있다는 중요한 요인을 부각시키고 있습니다. 전반적으로, 첨단 직장용 코르티코스테로이드 전달 시스템에 대한 규제 당국의 지원 확대와 효과적인 국소성 궤양성 대장염 치료법에 대한 미충족 의료 수요가 북미 히드로코르티손 시장의 주요 성장 요인이 될 것으로 예측됩니다.

아시아태평양의 성장은 도시화의 진전, 소매 및 병원 현장에서의 제네릭 히드로코르티손 보급, 그리고 약국의 전자상거래 및 원격 약국 서비스의 급속한 확산을 반영하고 있으며, 이러한 요인들이 결합되어 부신 기능 대체 요법과 같은 만성 질환에 대한 지속적인 관리를 강화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the hydrocortisone market size is projected to expand from USD 1.76 billion in 2025 and USD 1.82 billion in 2026 to USD 2.25 billion by 2031, registering a CAGR of 4.28% between 2026 to 2031.

This report is Segmented by Route of Administration (Topical, Oral, and Others), by Prescription Type (Over-The-Counter (OTC), Prescription (Rx)), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), by Indication (Dermatology, Gastrointestinal, and Others), and by Geography (North America, Europe, Asia-Pacific, and Others). The Report Offers the Value (USD) for the Above Segments.

Global Hydrocortisone Market Trends and Insights

WHO Essential Medicines Status Ensures Baseline Demand and Formulary Inclusion

Hydrocortisone's presence on the 24th WHO Model List of Essential Medicines, reaffirmed in September 2025, secures priority in national procurement and public formularies across income levels, which stabilizes the hydrocortisone market against abrupt displacement in tender-driven settings. The 10th WHO Model List of Essential Medicines for Children in 2025 codified broader pediatric coverage, including oral liquid 1 mg/mL, oral granules, and injectables, aligning supply with pediatric replacement needs and mitigating dosing workarounds that previously eroded adherence. Country lists in Africa and other regions mirror these inclusions, anchoring availability from primary care posts to tertiary hospitals and reinforcing sustained baseline volumes for both oral and parenteral formats. Ongoing WHO Expert Committee reviews in 2026 keep the competitive bar active for overlapping therapies. Yet, hydrocortisone's physiologic replacement role and emergency-use relevance make removal risk low in the near term. This status enhances access while constraining pricing power in public channels, which shapes a predictable but cost-sensitive foundation for the hydrocortisone market.

OTC Availability Enables Self-Care and Retail/E-Pharmacy Access Expansion

OTC hydrocortisone at 0.5-1% strength enables routine self-management of minor dermatoses without physician visits, supporting the largest 2025 prescription-type share and aligning with consumer preference for low-friction access, which together reinforce volume resilience across retail and digital channels. The United States FDA's Additional Conditions for Nonprescription Use framework, effective in January 2025, allows technology-enabled self-selection for certain OTC medicines, which supports safe self-care journeys and can lift conversion among consumers who otherwise defer treatment. Growth is moderated by rising consumer awareness of topical steroid withdrawal risks, which encourages some users to prefer non-steroidal options, but convenient OTC access still anchors front-line care for mild inflammation.

Generic Price Pressure and Intense Competition Compress Margins

Hydrocortisone is widely produced across oral, topical, and parenteral forms by many manufacturers, which intensifies price competition and narrows transaction margins across channels without significantly lifting unit volumes in mature indications. Supply-chain events underscore fragility in certain presentations, as the United Kingdom signaled shortages of pre-mixed hydrocortisone injection in 2025and advised substitution with sodium succinate powder for injection that is suitable for kit assembly, which preserved emergency-kit readiness but highlighted single-supplier risk. In this environment, the hydrocortisone market remains volume-stable but price-sensitive, and manufacturers increasingly prioritize niche, margin-protected formulations to defend profitability.

Other drivers and restraints analyzed in the detailed report include:

- Guideline-Backed Use in Vasopressor-Refractory Septic Shock Sustains Parenteral Demand

- Pediatric-Specific Approvals Enhance Access and Drive Oral Segment Growth

- Adverse Effects and Steroid-Phobia/TSW Reduce Adherence and Appropriate Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Topical administration accounted for 54.68% of 2025 revenue on the strength of OTC and prescription use in dermatology, while oral formulations are projected to grow fastest at 5.98% CAGR through 2031 as pediatric-specific products enable precise dosing and reduce caregiver variability, a dynamic that supports the hydrocortisone market size outlook through the forecast period. Eton's KHINDIVI oral solution for patients aged 5 and older received FDA approval in May 2025 and launched with specialty pharmacy support, complementing ALKINDI SPRINKLE granules and improving dosing accuracy in a population where precision is clinically important. The KHINDIVI label excludes children under 5 due to excipient risks, which narrows its on-label reach but reinforces the clinical rationale for age-tailored formulations within the hydrocortisone market. WHO EMLc 2025 includes oral liquids and granules alongside tablets, providing a policy foundation for broader pediatric access in markets where essential medicines lists steer procurement.

Topical hydrocortisone continues to dominate front-line management of mild inflammatory dermatoses, supported by OTC access, patient familiarity, and clinician comfort with lowest-potency regimens in sensitive areas where risk-benefit profiles are favorable for limited durations. Rectal delivery is positioned for targeted gastrointestinal use, where Cristcot's next-generation 90 mg hydrocortisone acetate suppository progressed to an FDA decision and reported remission benefits in Phase 3 results disclosed at NDA acceptance, expanding options for distal ulcerative colitis. Across modalities, the hydrocortisone industry is concentrating investment in delivery improvements that minimize systemic exposure while preserving efficacy for localized indications, a strategy aimed at creating durable niches inside a generics-heavy field. Emergency-focused delivery tools, including efforts to simplify rapid dosing outside clinical settings, reflect parallel emphasis on safety and readiness for adrenal crisis. This mix of entrenched topical leadership and rising oral precision dosing strengthens the hydrocortisone market's footing across hospital and home settings as clinical needs diversify

OTC products accounted for a 57.88% of 2025 revenue by enabling rapid, low-friction access for mild symptoms. Still, prescription pathways are projected to grow faster at 6.34% CAGR through 2031 as specialized formulations expand care in pediatrics, ulcerative colitis, and critical care, which together diversify the hydrocortisone market. Specialty distribution and copay programs around pediatric solutions help reduce barriers to adherence and position Rx hydrocortisone as a precision tool rather than a commodity choice, which underpins the growth gap with OTC. Rx-only parenteral presentations are insulated from OTC substitution because they are procedure-based in ICUs and emergency departments, where protocol adherence prioritizes on-formulary availability and consistency. OTC hydrocortisone remains a cornerstone in self-managed dermatology due to convenience, cost access, and widespread product familiarity, features that reinforce volume leadership even as clinical vigilance around topical steroid withdrawal rises. In parallel, Rx channels capture value through formulations and indications that require physician supervision or precise dosing that cannot be replicated in over-the-counter formats, which balances the hydrocortisone market across price tiers and care settings. Over the forecast, differentiated Rx products and hospital-driven uses maintain faster growth as they address clinical niches that are less exposed to consumer sentiment swings. At the same time, OTC continues to absorb the broad base of minor inflammatory presentations.

Geography Analysis

North America held 38.34% of revenue in 2025 as pediatric precision dosing matured and hospital protocols remained firmly embedded, while Asia Pacific is projected to deliver the fastest CAGR at 5.21% through 2031, a two-speed pattern that shapes the hydrocortisone market across reimbursement, access, and channel maturity. The United States and Canadian healthcare systems maintain injectable hydrocortisone in hospital formularies for emergency use in adrenal crisis and shock management. Pediatric adrenal insufficiency is managed with chronic hydrocortisone replacement, including liquid and compounded formulations when needed, supported through standard pharmacy and compounding channels, resulting in ongoing prescription requirements in affected patients. Digital pharmacy expansion and same-day logistics widen convenient access for patients and caregivers, while clinical groups and regulators continue to update safety communications to ensure appropriate topical steroid use. The North American hydrocortisone market is being shaped by ongoing innovation in corticosteroid formulations for inflammatory bowel diseases, particularly ulcerative colitis. For instance, as per the article published in MJH Life Sciences in April 2026, the FDA's acceptance of an NDA for a next-generation hydrocortisone acetate suppository for ulcerative colitis of the rectum highlights a key driver rising demand for targeted, locally acting therapies that improve efficacy while reducing systemic side effects in chronic GI conditions. Overall, increasing regulatory support for advanced rectal corticosteroid delivery systems and the unmet need for effective localized ulcerative colitis treatments are expected to be major growth drivers for the North America hydrocortisone market.

Asia Pacific's growth reflects rising urbanization, penetration of generic hydrocortisone across retail and hospital settings, and rapid adoption of pharmacy e-commerce and telepharmacy services that together strengthen continuity of care for chronic needs like adrenal replacement.

List of Companies Covered in this Report:

- Amneal Pharmaceuticals

- ANI Pharmaceuticals

- BluePoint Laboratories

- Chartwell RX, LLC

- Cipla

- Hikma Pharmaceuticals

- Medrock Pharmacy LLC

- Perrigo Company

- Pfizer

- Sandoz Group

- Sanofi

- Taro Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries

- Trifecta Pharmaceuticals USA, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 WHO Essential Medicines Status Ensures Baseline Demand and Formulary Inclusion

- 4.2.2 OTC Availability (0.5-1%) Enables Self-care and Retail/e-pharmacy Access Expansion

- 4.2.3 Guideline-backed Use in Vasopressor-refractory Septic Shock (parenteral demand)

- 4.2.4 Emergency Adrenal Crisis Protocols Mandate Hydrocortisone Kits and Rapid Dosing

- 4.2.5 Pediatric-specific Approvals (Oral Granules/Solution) for Adrenal Insufficiency

- 4.2.6 Endocrine Tapering/Stress-dose Guidance Favors Hydrocortisone in GIAI Management

- 4.3 Market Restraints

- 4.3.1 Adverse Effects and Steroid-phobia/TSW Reduce Adherence and Appropriate Use

- 4.3.2 Generic Price Pressure and Intense Competition Compress Margins

- 4.3.3 Steroid-sparing Biologics/JAK Inhibitors Displace Use in Select Indications

- 4.3.4 Pediatric Sepsis Guidance Limits Routine Hydrocortisone; Retail Curbs on Misuse

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Route of Administration

- 5.1.1 Topical

- 5.1.2 Oral

- 5.1.3 Others (Rectal, Parenteral, etc.)

- 5.2 By Prescription Type

- 5.2.1 Over-the-Counter (OTC)

- 5.2.2 Prescription (Rx)

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Indication

- 5.4.1 Dermatology

- 5.4.2 Gastrointestinal

- 5.4.3 Others (Ophthalmic, Allergic reacttions, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Amneal Pharmaceuticals, Inc.

- 6.4.2 ANI Pharmaceuticals, Inc.

- 6.4.3 BluePoint Laboratories

- 6.4.4 Chartwell RX, LLC

- 6.4.5 Cipla Ltd.

- 6.4.6 Hikma Pharmaceuticals PLC

- 6.4.7 Medrock Pharmacy LLC

- 6.4.8 Perrigo Company plc

- 6.4.9 Pfizer Inc.

- 6.4.10 Sandoz

- 6.4.11 Sanofi

- 6.4.12 Taro Pharmaceutical Industries Ltd.

- 6.4.13 Teva Pharmaceutical Industries Ltd.

- 6.4.14 Trifecta Pharmaceuticals USA, LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment