|

시장보고서

상품코드

2063604

혈압계 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sphygmomanometer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

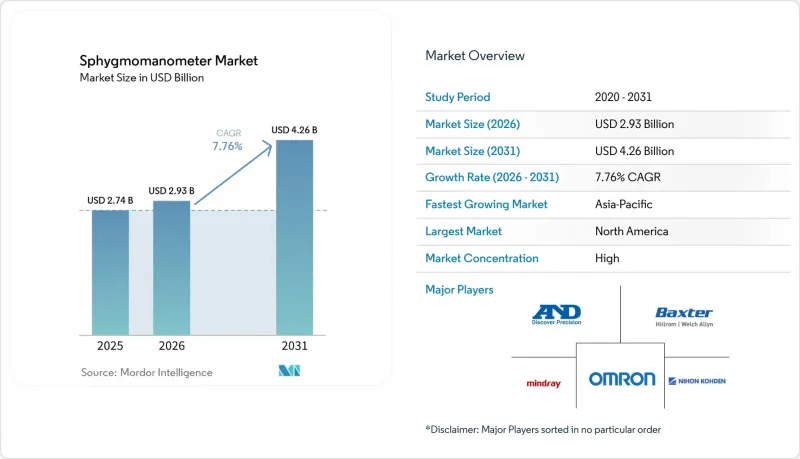

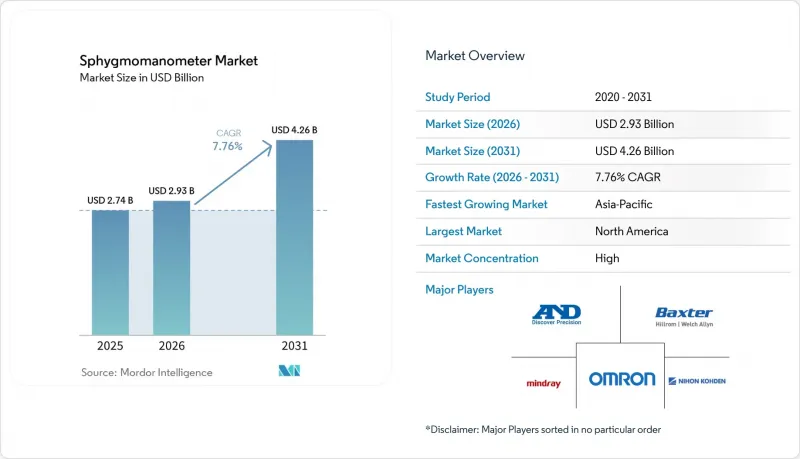

Mordor Intelligence에 의하면, 혈압계 시장 규모는 2025년 27억 4,000만 달러에서 2026년에는 29억 3,000만 달러로 확대되어 2031년까지 42억 6,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 7.76%로 성장할 전망입니다.

본 보고서는 제품 유형(수은식 혈압계, 아네로이드식 혈압계, 디지털식 혈압계), 작동 방식(수동, 자동, 반자동), 형태(휴대형, 고정형), 최종 사용자(병원 및 진료소, 재택치료, 기타), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 본 보고서에서는 상기 각 부문 시장 규모(달러)를 제시하고 있습니다.

세계 혈압계 시장 동향과 인사이트

고혈압 및 심혈관 질환 유병률 증가

세계보건기구(WHO)의 보고에 따르면, 2024년 현재 전 세계적으로 14억 명의 성인이 고혈압을 앓고 있는 반면, 미국 질병통제예방센터(CDC)의 기록에 따르면 미국 성인의 약 48%가 고혈압 진단 기준을 충족하고 있습니다. 이러한 유병률은 진단 확정 및 치료 조정을 위해 빈번한 측정이 이루어지도록 임상 지침이 변화함에 따라, 재택 모니터링 기기에 대한 수요로 직접 이어지고 있습니다. 2026년 2월 미국심장학회가 발표한 자료에 따르면, 미국 성인의 80% 가까이가 혈압 목표치를 초과하는 고혈압(HTN)을 앓고 있습니다. 이러한 역학적 동향은 주기적인 것이 아니라 구조적인 것으로, 아네로이드식 및 보급형 디지털 기기의 상품화로 인해 평균 판매 가격이 하락하고 있음에도 불구하고 안정적인 수요를 뒷받침하고 있습니다.

세계의 고령화와 만성 질환의 부담

65세 이상 세계 인구는 연평균 3.1%의 비율로 증가하고 있으며, 일본, 이탈리아, 독일에서는 연령 중앙값이 45세를 넘고 있습니다. 이러한 인구 동향은 고혈압 유병률과 상관관계가 있으며, 40-49세 연령층의 유병률은 약 30%인 반면, 70세 이상에서는 70%를 초과합니다. 이 고령층에서는 당뇨병, 만성 신장병, 심방세동 등의 동반 질환 비율도 높게 나타납니다. 이러한 질환들은 혈압 관리를 복잡하게 만들며, 투약량을 조절하는 동안 저혈압 발작을 방지하기 위해 빈번한 모니터링이 필요합니다. 만성 질환의 부담은 모니터링이 필요한 환자 수를 늘리는 ‘ 수요 증가 요인’인 동시에, 기능의 복잡화를 촉진하는 ‘기능 고도화 요인’으로도 작용하여 혈압계 시장 수요를 증가시키고 있습니다.

정확성에 대한 우려와 장비 검증 기준의 부재

정확도에 대한 우려와 표준화된 검증 프로토콜의 부재는 혈압계 시장에서 여전히 큰 제약 요인으로 작용하고 있습니다. 2026년 1월, 『Digital Health』지에 게재된 데이터에 따르면, 2023년 5월 15일 프라하의 체코 공과대학교 생체의공학부 윤리위원회가 실시한 연구에서 시중에 판매되고 있는 많은 기기가 적절한 임상 검증을 받지 않았으며, 500대 이상의 커프리스형 기기에 대해 표준화된 정확도 검증이 이루어지지 않았다고 보고되었습니다. 2024년 10월 『Hypertension』지에 게재된 기사에 따르면, 1946년 및 1947년부터 2023년 4월까지의 MEDLINE 및 EMBASE 문헌 검색 결과, 가정용 혈압계와 임상적 골드 스탠다드인 수은식 혈압계 사이에서 수축기 혈압 측정값에 10%-72%의 차이가 확인되었다고 보고되었습니다. 이러한 불일치에 더해, 세계적 검증 기준을 충분히 준수하지 못하고 있는 점이 기기의 신뢰성과 시장 보급을 계속해서 저해하고 있습니다.

부문별 분석

2025년에는 디지털 모델이 주류를 이루었고, 환경 규제로 인한 수은식 제품의 감소에 따라 혈압계 시장 점유율의 58.8%를 차지했습니다. 오므론 등 제조업체들은 연결형 혈압계, 모바일 앱, 원격 환자 모니터링 서비스를 통합함으로써 디지털 혈압계 생태계를 확대하고 있으며, 이를 통해 고혈압 관리가 개선되고 의료진이 실시간으로 환자를 모니터링할 수 있게 되었습니다. 동시에, AI를 활용한 고혈압 관리도 확산되고 있으며, 일상적인 혈압 측정 중에 심방세동(AFib)을 감지하거나 심혈관 위험을 평가하는 알고리즘이 탑재된 기기가 늘어나고 있습니다. 이러한 예측적·예방적 관리로의 전환에 따라, 가정용 혈압 측정 기기의 임상적 가치는 단순히 측정값을 제공하는 것을 넘어 더욱 높아지고 있습니다. 예를 들어, 2025년 10월, 오므론 헬스케어는 AI가 탑재된 심방세동 감지 기능이 있는 혈압계로 디지털 헬스 허브 재단이 주최한 ‘2025 디지털 헬스 어워드’에서 재택 건강 검진·모니터링 부문 최우수상을 수상했습니다.

2025년에는 측정 주기 중 커프가 자동으로 팽창함으로써 절차 시간이 단축되고 불편함이 줄어들었기 때문에 자동식 기기가 53.45%의 시장 점유율을 차지했습니다. 자동 혈압계 시장 규모는 2031년까지 연평균 성장률(CAGR) 7.96%로 확대될 것으로 전망됩니다. Beurer사의 BM 48은 커프가 팽창하기 전에 위치를 확인하여, 과거에 오경보를 유발했던 오류를 미연에 방지합니다. 반자동 혈압계는 주로 가격에 민감한 시장에서 여전히 자리를 잡고 있지만, 현재 시장 점유율은 10% 미만에 그치고 있습니다. 한편, 수동 청진 키트는 부정맥이나 소아용 등 틈새 시장을 겨냥한 제품으로 남아 있습니다.

지역별 분석

주요 지역 전반에서 심혈관 질환 및 생활습관병의 유병률이 증가하고 있으며, 이는 공중보건상 중요한 우려 사항으로 대두되고 있어 혈압계 등 진단·모니터링 기기 수요에 큰 영향을 미치고 있습니다. Heart &Stroke의 최신 ‘하트 먼스’ 보고서에 따르면, 심장병과 뇌졸중은 이전 추정치보다 훨씬 더 많은 사람들에게 영향을 미치고 있으며, 캐나다에서만 약 600만 명이 이러한 질환을 앓으며 살고 있습니다. 이는 고령화, 고혈압, 비만과 같은 생활습관상의 위험 요인에 기인한 북미 전역의 심혈관 질환 부담 증가를 반영하고 있습니다. 유병률 증가에 따라 정기적인 혈압 모니터링과 예방 의료에 대한 수요가 높아지고 있습니다.

2026년 4월 인도 『The India Practitioner』지에 보도된 바에 따르면, 인도 국립통계청이 실시한 최근 전국 조사에서 생활습관병의 급증 현상이 두드러지게 나타났으며, 현재 인구의 거의 절반이 고혈압, 심장병, 당뇨병 등의 심혈관 질환 및 대사성 질환을 앓고 있는 것으로 밝혀졌습니다. 심혈관 질환의 유병률은 2017-2018년의 16.7%에서 2025년에는 25.6%로 상승했으며, 대사·내분비 질환도 현저한 증가세를 보였습니다. 아시아태평양 전체에서 나타나는 이러한 급격한 증가는 혈압 및 관련 건강 상태에 대한 선별 검사와 모니터링 개선에 대한 강력한 필요성을 부각시키고 있습니다.

전반적으로, 북미 및 아시아태평양의 심혈관 질환 및 대사성 질환 부담 증가는 혈압계 시장의 지속적인 성장을 견인할 것으로 예측됩니다. 이는 질환의 관리와 예방에 있어 조기 진단과 정기적인 혈압 모니터링이 점점 더 중요해지고 있기 때문입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the sphygmomanometer market size is expected to increase from USD 2.74 billion in 2025 to USD 2.93 billion in 2026 and reach USD 4.26 billion by 2031, growing at a CAGR of 7.76% over 2026-2031.

This report is Segmented by Product Type (Mercury Sphygmomanometers, Aneroid Sphygmomanometers, and Digital Sphygmomanometers), by Operation (Manual, Automatic, and Semi-Automatic), by Modality (Portable and Bench-Top), by End User (Hospitals & Clinics, Homecare Settings, and Others), and by Geography (North America, Europe, Asia Pacific, and Others). The Report Offers the Value (USD) for the Above Segments.

Global Sphygmomanometer Market Trends and Insights

Rising Prevalence of Hypertension and Cardiovascular Diseases

The World Health Organization reported that 1.4 billion adults were living with hypertension globally in 2024, while the Centers for Disease Control and Prevention documented that approximately 48% of United States adults meet diagnostic thresholds for elevated blood pressure, a prevalence that translates directly into demand for home monitoring devices as clinical guidelines shift toward frequent measurement for diagnosis confirmation and treatment titration. As per the data reported by American College of Cardiology in February 2026, nearly 80% of United States Adults Have HTN Above BP Goals. This epidemiological trend is structural in nature rather than cyclical, supporting consistent unit demand even as average selling prices decline due to the commoditization of aneroid and entry-level digital devices.

Aging Global Population & Chronic-Disease Burden

The global population aged 65 and older is expanding at 3.1% annually, with Japan, Italy, and Germany exhibiting median ages above 45 years, demographics that correlate with hypertension incidence, which rises from approximately 30% in the 40-49 age cohort to over 70% in those aged 70 and above. This aging cohort also presents higher rates of comorbidities such as diabetes, chronic kidney disease, and atrial fibrillation, conditions that complicate blood pressure management and necessitate frequent monitoring to avoid hypotensive episodes during medication titration. The burden of chronic diseases acts as both a volume driver, bringing more patients into need of monitoring, and a driver of feature complexity, increasing demand within the sphygmomanometer market.

Accuracy Concerns & Lack of Device Validation Standards

Accuracy concerns and lack of standardized validation protocols remain a significant restraint in the sphygmomanometer market. As per the data published in Digital Health in January 2026, a study conducted by the Ethics Committee of the Faculty of Biomedical Engineering of the Czech Technical University in Prague on May 15, 2023, shows that many commercially available devices lack proper clinical validation, with over 500 cuffless devices reported without standardized accuracy verification. As per the article published in Hypertension in October 2024, a literature search of MEDLINE and EMBASE from 1946 and 1947, respectively, through April 2023, stated that discrepancies of 10%-72% in systolic readings have been observed between home monitors and mercury sphygmomanometers, the clinical gold standard. These inconsistencies, coupled with limited adherence to global validation standards, continue to hinder device reliability and market adoption.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Home-Based Blood-Pressure Monitoring Devices

- Expansion of Telehealth Reimbursement for Remote BP Monitoring

- Stringent Multi-Region Regulatory Approval Timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital models dominated in 2025, accounting for 58.8% of the sphygmomanometer market share as mercury options receded under environmental bans. Manufacturers such as Omron are expanding digital sphygmomanometer ecosystems by integrating connected BP monitors, mobile applications, and remote patient monitoring services, enabling improved hypertension management and real-time clinician oversight. At the same time, AI-enabled hypertension management is gaining momentum, with devices increasingly incorporating algorithms for AFib detection and cardiovascular risk assessment during routine blood pressure measurements. This shift toward predictive and preventive care is enhancing the clinical value of home BP monitoring devices beyond traditional readings. For instance, in October 2025, Omron Healthcare was recognized by the Digital Health Hub Foundation's 2025 Digital Health Awards as Best in Class in Home Health Diagnostics & Monitoring for its AI-powered AFib-detecting BP monitors.

Automatic units held 53.45% share in 2025, due to automated cuff inflation during measurement cycles that shorten procedure time and reduce discomfort. The sphygmomanometer market size for automatic devices is forecast to expand at 7.96% CAGR to 2031. Beurer's BM 48 checks cuff position before inflation, aborting errors that once generated false alarms. Semi-automatic monitors survive mainly in price-sensitive markets but now claim below 10% unit share, while manual auscultatory kits remain niche for arrhythmia or pediatric use.

Geography Analysis

The increasing prevalence of cardiovascular and lifestyle-related diseases across major regions is emerging as a key public health concern, significantly influencing the demand for diagnostic and monitoring devices such as sphygmomanometers. Heart disease and stroke are affecting a significantly larger population than previously estimated, with about 6 million people living with these conditions in Canada alone, according to Heart & Stroke's latest Heart Month report. This reflects a growing cardiovascular burden across North America, driven by aging populations and lifestyle risk factors such as hypertension and obesity. The rising prevalence is increasing the demand for regular blood pressure monitoring and preventive care.

A recent nationwide survey by the National Statistics Office reported in The India Practitioner in April 2026 in India highlights a sharp increase in lifestyle-related diseases, with nearly half the population now reporting cardiovascular and metabolic conditions such as hypertension, heart disease, and diabetes. Cardiovascular ailments rose from 16.7% in 2017-18 to 25.6% in 2025, while metabolic and endocrine disorders also showed a marked increase. This rapid escalation across the Asia Pacific region underscores a strong need for improved screening and monitoring of blood pressure and related health conditions.

Overall, the rising burden of cardiovascular and metabolic disorders in both North America and Asia Pacific is expected to drive sustained growth in the sphygmomanometer market, as early diagnosis and regular blood pressure monitoring become increasingly critical for disease management and prevention.

- A&D Company, Limited

- Aktiia SA

- Beurer

- Biobeat Technologies Ltd.

- Bosch + Sohn GmbH u. Co. KG

- Citizen Systems Japan Co., Ltd.

- Contec Medical Systems

- GE HealthCare Technologies Inc.

- Hillrom / Welch Allyn

- iHealth Labs, Inc.

- Jiangsu Yuyue Medical (Yuwell)

- Koninklijke Philips

- Microlife

- Mindray Bio-Medical Electronics Co., Ltd.

- Nanowear, Inc.

- Nihon Kohden

- Omron Healthcare Co., Ltd.

- Panasonic Healthcare

- Rossmax

- Rudolf Riester

- SunTech Medical, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Hypertension and Cardiovascular Diseases

- 4.2.2 Rapid Adoption of Home-based Blood-pressure Monitoring Devices

- 4.2.3 Aging Global Population & Chronic-disease Burden

- 4.2.4 Expansion of Telehealth Reimbursement for Remote BP Monitoring

- 4.2.5 AI-enabled Predictive Analytics in Digital Sphygmomanometers

- 4.2.6 Corporate Wellness & Insurance Programs Mandating BP Tracking

- 4.3 Market Restraints

- 4.3.1 Accuracy Concerns & Lack of Device Validation Standards

- 4.3.2 Stringent Multi-region Regulatory Approval Timelines

- 4.3.3 Data-privacy & Cybersecurity Risks in Connected Devices

- 4.3.4 Supply-chain Disruptions for Critical Electronic Components

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Mercury Sphygmomanometers

- 5.1.2 Aneroid Sphygmomanometers

- 5.1.3 Digital Sphygmomanometers

- 5.1.3.1 Standard Upper-Arm Digital

- 5.1.3.2 Wrist Digital

- 5.1.3.3 Wearable / Cuff-less

- 5.2 By Operation

- 5.2.1 Manual

- 5.2.2 Automatic

- 5.2.3 Semi-automatic

- 5.3 By Modality

- 5.3.1 Portable

- 5.3.2 Bench-top

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Homecare Settings

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Community Health Centers & Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves & Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-Level Overview, Market-Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.4.1 A&D Company, Limited

- 6.4.2 Aktiia SA

- 6.4.3 Beurer GmbH

- 6.4.4 Biobeat Technologies Ltd.

- 6.4.5 Bosch + Sohn GmbH u. Co. KG

- 6.4.6 Citizen Systems Japan Co., Ltd.

- 6.4.7 Contec Medical Systems Co., Ltd.

- 6.4.8 GE HealthCare Technologies Inc.

- 6.4.9 Hillrom / Welch Allyn

- 6.4.10 iHealth Labs, Inc.

- 6.4.11 Jiangsu Yuyue Medical (Yuwell)

- 6.4.12 Koninklijke Philips N.V.

- 6.4.13 Microlife Corporation

- 6.4.14 Mindray Bio-Medical Electronics Co., Ltd.

- 6.4.15 Nanowear, Inc.

- 6.4.16 Nihon Kohden Corporation

- 6.4.17 Omron Healthcare Co., Ltd.

- 6.4.18 Panasonic Healthcare Co., Ltd.

- 6.4.19 Rossmax International Ltd.

- 6.4.20 Rudolf Riester GmbH

- 6.4.21 SunTech Medical, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment