|

시장보고서

상품코드

2063609

흡수성 임플란트 디바이스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Absorbable Nasal Implant Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

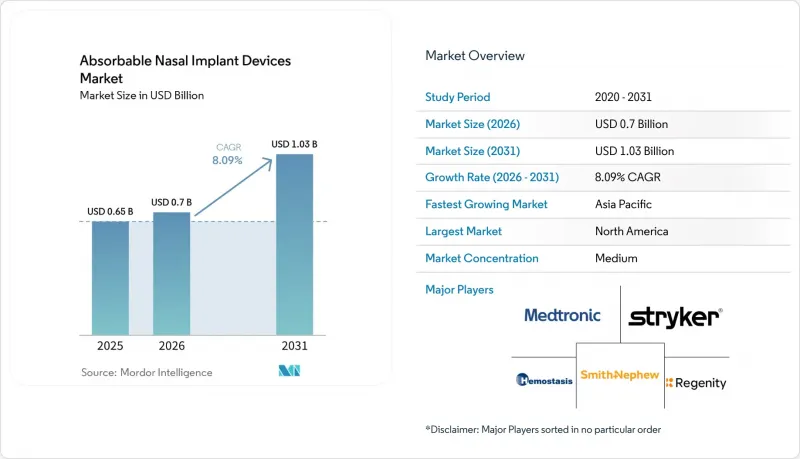

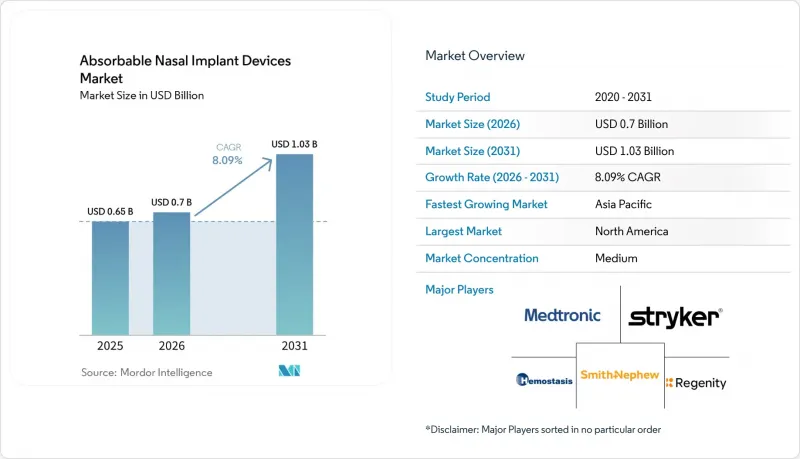

Mordor Intelligence에 의하면, 흡수성 비강 임플란트 디바이스 시장 규모는 2025년 6억 5,000만 달러, 2026년 7억 달러에서 2031년까지 10억 3,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.09%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(흡수성 비강 드레싱, 약물 방출형 부비동 임플란트, 흡수성 비강 판막 지지 임플란트 등), 용도(기능적 내시경 부비동 수술 후, 코피 관리 등), 최종 사용자(병원, 외래수술센터(ASC) 등) 및 지역(유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 흡수성 비강 임플란트 기기 시장 동향 및 인사이트

만성 부비동염(CRD)의 유병률 상승과 수술 건수 증가가 부비동 내 드레싱 및 임플란트에 대한 수요를 뒷받침하고 있습니다.

만성 부비동염 유병률 증가와 안정적인 부비동 수술 건수는 병원 및 외래 환경 모두에서 기기의 지속적인 사용을 뒷받침하고 있습니다. 내시경 부비동 수술 후 관리의 핵심 목표는 수술 후 염증을 조절하고 개구부의 개존성을 유지하는 것이며, 이에 따라 약물 방출형 및 비약물형 흡수성 임플란트가 수술 후 관리에 있어 일상적으로 고려되고 있습니다. 미국에서 실시된 임상 및 보험사 검토 요약에 따르면, 모메타손 방출형 임플란트를 삽입할 경우 수술 후 중재가 감소하는 것으로 보고되었으며, 이는 외과의사들이 이를 채택하는 데 있어 데이터에 기반한 근거를 뒷받침하고 있습니다.

전문 학회는 특정 비과 시술에 있어 진료소 및 외래 진료의 워크플로우가 수행하는 역할을 강조하고 있으며, 이에 따라 흡수성 임플란트를 사용할 수 있는 시술 장소가 확대되고 있습니다. 흡수성 비강 임플란트 기기 시장이 성숙해짐에 따라, 임상의들은 재발성 폴립 환자군에서 재수술 위험을 줄이기 위해 부비동 내 임플란트와 최적화된 국소 스테로이드 요법을 병행하고 있습니다. 이러한 안정적인 시술 환경이 예측 기간 동안 흡수성 비강 임플란트 기기 시장에 예측 가능한 수요를 지속시키는 요인 중 하나입니다.

진료소/ASC(외래수술센터(ASC))에서의 비과 치료로의 전환에 따라, 진료소 내 임플란트 및 드레싱 사용이 증가

저침습 기술과 국소 마취를 통해 환자의 편안함을 유지하면서 치료 기간을 단축할 수 있기 때문에 외래 및 진료소에서의 비과 치료 비중이 확대되고 있습니다. SINUVA는 진료소에서 내시경 하에 삽입하는 것이 적응증이며, 90일 동안 국소적으로 플루오로메타손을 방출하므로, 진료소에서는 수술실 예약이나 전신 마취 없이도 재발성 용종의 치료를 진행할 수 있습니다. 비판막 재건에 관한 CPT 코드 30468에 따른 청구 기준이 명확해짐에 따라, 점막하 측벽 임플란트의 청구 가능 경로가 정의되어, 클리닉에서 시행하는 판막 지지술에 대한 불확실성이 완화됩니다. 부비동 수술 및 관련 임플란트의 의료적 필요성 기준을 정의하는 보험사 측의 개정으로 인해, 의료기관은 의료기기를 활용한 치료 계획에 대한 문서화 및 보험 적용 범위에 대한 기대치에 대해 보다 명확한 전망을 얻을 수 있게 되었습니다.

간편한 원패스 삽입을 목적으로 하며, 제거가 필요 없는 생체 흡수성 기기 등 진료소 사용에 최적화된 새로운 임플란트는 워크플로우의 예측 가능성을 높이고, 바쁜 이비인후과 진료에서 후속 관리의 부담을 줄여줍니다. 따라서 생체 흡수성 비강 임플란트 기기 시장은 해당 기기를 활용한 시술 프로토콜이 시간적·비용적 측면에서 뚜렷한 이점을 제공하는 외래 및 클리닉 환경으로 적절한 증례가 전환됨에 따라 혜택을 볼 수 있는 위치에 있습니다.

보험사가 비중개 임플란트 및 약물 방출 스텐트를 ‘임상시험 단계’로 규정하는 방침으로 인해 보험 적용이 제한됨

2026년 민간 보험사의 정책에 따르면, 표본 크기가 작고, 추적 조사의 한계가 있으며, 표준 국소 스테로이드 요법과의 직접적인 비교가 부족하다는 이유로 약물 방출형 부비동 임플란트를 ‘임상시험 단계’로 분류하고 있으며, 이로 인해 미국의 주요 보험 플랜에서 보험 적용이 제한되고 있습니다. 이와 유사한 추세는 비중격 폐쇄증에 사용되는 흡수성 외측 비강 임플란트에도 영향을 미치고 있으며, 임상 연구에서 증상 개선 효과가 입증되었음에도 불구하고 일부 보험 계획에서는 이 기술을 ‘임상시험 단계’로 분류하고 있어, 환자들의 접근이 복잡해지고 이용 확대가 저해되고 있습니다. ‘임상시험 중’이라는 분류는 많은 기업 주도형 보험 플랜에서 보장 대상에서 제외되는 요인이 되어, 비용을 환자에게 전가하고 있습니다. 그 결과, 수술 패키지 이외의 분야에서 도입 확대를 검토하고 있는 클리닉의 경우, 경제적 부담이 커지고 있습니다. 또한, 다른 보험 플랜에서는 흡수성 비강 임플란트와 비판막을 대상으로 한 고주파 치료 모두에 대해 ‘임상시험 중’이라는 상태를 유지하고 있으며, 추적 조사 중 탈락이나 다른 구조적 수술과의 직접적인 비교가 부족하다는 한계를 강조하고 있습니다.

정책 환경은 여전히 유동적이며, 의료기기 제조업체는 각 보험 상품의 급여 기준에 부합하는 방식으로 증거 부족 문제를 해소하기 위해, 결과 조사 및 보험사에 대한 인식 제고 활동에 투자해야 합니다. 이러한 상황의 편차로 인해, 외과의사들의 관심과 실제 임상에서 좋은 결과가 나타나고 있음에도 불구하고, 흡수성 비강 임플란트 시장의 단기적인 성장은 둔화되고 있습니다.

부문별 분석

2025년에는 약물 방출형 부비동 임플란트가 흡수성 비강 임플란트 기기 시장 점유율 33.60%를 차지할 것으로 예상되며, 흡수성 비강 밸브 지지 임플란트는 2026년부터 2031년까지 연평균 성장률(CAGR) 10.86%로 성장할 것으로 전망됩니다. 이는 수술 후 염증 조절에 있어 국소 코르티코스테로이드 투여에 대한 임상의들의 강한 신뢰를 반영한 것입니다. 지불 주체의 의사결정을 위해 정리된 증거에 따르면, 스테로이드 방출 장치는 비약물 대조군에 비해 수술 후 중재 및 전신 스테로이드 사용을 감소시키는 것으로 나타났으며, 이는 부비동 수술 후 주요 보조 요법으로서의 역할을 뒷받침하고 있습니다. PROPEL 시리즈는 생체 흡수성 스캐폴드를 통해 모메타손 플루에이트를 방출하는 제품으로, 수술 후 초기 치유 단계에 맞추어 설계된 용출 프로파일을 상세하게 기재한 첨부 문서를 갖추고 있으며, 이는 수술 후 1개월 동안의 임상적 유용성을 입증하고 있습니다. 진료소에서 시행되는 모메타손 방출 임플란트는 과거 수술 후 비용종이 재발한 환자를 대상으로 하며, 특정 적격 환자에게 90일 동안 국소 스테로이드를 공급함으로써 재수술을 연기하거나 피할 수 있게 해줍니다.

비약물성 흡수성 드레싱은 여전히 비중격 성형술, 코 성형술 및 부비동 수술에 필수적이며, 외과의사는 치유 전망에 맞추어 분해 일정을 선택함으로써 환자의 불편함과 진료소의 업무 부담을 줄이고 있습니다. 생체흡수성 스페이서 및 비중격 스프린트는 천공 복구나 복잡한 재건 수술 시 피부 이식 부위의 피복 등 보다 전문적인 요구를 충족시켜 주며, 틈새 적응증 분야에서 사례별 고가 책정을 뒷받침하고 있습니다. 중국과 인도에서공급 현지화는 규격에 부합하는 흡수성 드레싱의 세계 공급 체계를 강화하고 있으며, 이를 통해 물류 혼란으로부터 보호받을 뿐만 아니라, 가격에 민감한 시장의 공립 및 사립 병원들이 서비스 제공 비용을 매력적인 수준으로 유지할 수 있게 해주고 있습니다.

지역별 분석

북미는 2025년에 41.80%의 점유율을 차지했습니다. 이는 특정 적응증에 있어 지불 주체의 대응에 차이가 있음에도 불구하고, 수술실이나 클리닉에서의 프로토콜이 표준화되어 있고 기기 사용이 정착되었기 때문입니다. 미국 내 외래 진료 지급 기준이 개정되면서 의료기기를 많이 사용하는 부비동 수술이 정의됨에 따라, 의료 기관은 번들 내에서 임플란트 사용을 계획하기가 더 쉬워졌으며, 병원 및 외래수술센터(ASC)에서의 지속적인 도입이 촉진되고 있습니다. 과거 수술 후 재발성 용종에 대한 진료소 내 삽입 등 특정 임상 시나리오에 대한 코딩 및 보험 적용 범위의 명확화는 시설 기반 진료팀에게 해당 이용 사례에 대한 청구 예측 가능성을 높여주고 있습니다. 전문 학회 및 보험사의 정책 업데이트는 외과 의사와 관리자가 수술 후 계획을 수립하는 데 지침이 되며, 흡수성 비강 임플란트 기기 시장의 꾸준한 수요를 뒷받침하고 있습니다. 코딩, 훈련 및 결과 데이터가 통합됨에 따라, 해당 지역의 임상 리더는 환자의 편안함과 재수술 위험 감소를 최우선으로 하는 표준화된 치료 경로에 스테로이드 방출형 및 흡수성 구조 장치를 지속적으로 도입하고 있습니다.

유럽에서는 성숙한 규제 환경과 프로토콜을 대규모로 표준화할 수 있는 이비인후과 센터의 견고한 기반에 힘입어, 확고한 보급이 진행되고 있습니다. 유럽 전역에서의 제품 출시는 흡수성 3등급 의료기기의 안전성과 시판 후 조사를 우선시하는 조화로운 규제 체제 하에서 진행되고 있으며, 이는 장기적인 치료 결과를 추적하고자 하는 의료진의 기대와 부합합니다. 프랑스, 영국, 이탈리아, 스페인 등 주요 시장에는 약물 방출형 및 비약물형 흡수성 임플란트 모두에 정통한 경험이 풍부한 이비인후과 전문의가 다수 재직하고 있으며, 이것이 의료기기를 활용한 수술 후 관리의 꾸준한 확장을 뒷받침하고 있습니다. 학술 기관과 임상 시설 간의 협력을 통해 연구자 주도 조사, 외과 의사의 연수 및 임상 감사가 촉진됨에 따라, 적절한 대상 집단에서 증상을 관리하고 재수술을 줄이는 데 있어 흡수성 임플란트의 역할이 강화되고 있습니다. 이러한 환경 속에서 흡수성 비강 임플란트 시장은 공립병원과 민간병원을 불문하고 일관된 치료 성과를 중시하는 엄격한 조달 체계와 외과 의사 주도의 프로토콜을 통해 발전하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 국내 생산 및 이비인후과 인프라 확충을 통해 접근성과 가격 경쟁력이 향상되어 2031년까지 연평균 성장률(CAGR)이 12.24%를 나타낼 것으로 전망됩니다. 중국과 인도의 인증 제조업체들은 지역 시장 및 수출 시장에 흡수성 드레싱 및 관련 제품을 공급하고 있으며, 이를 통해 물류 위험이 감소하고 공공 부문의 경쟁력 있는 가격 조달이 뒷받침되고 있습니다. 2·3급 도시에서 이비인후과(ENT) 진료 체계가 확충됨에 따라 흡수성 드레싱에 대한 수요가 증가하는 한편, 증가하는 중산층을 대상으로 하는 민간 클리닉에서 진료소 사용에 최적화된 임플란트의 도입이 촉진되고 있습니다. 가처분 소득과 환자의 인식이 높아짐에 따라, 이비인후과 의료진은 편안함, 후속 처치의 감소, 그리고 증상 관리를 위한 국소 요법을 중시하는 수술 후 및 진료소 내 프로토콜에 흡수성 임플란트를 도입하고 있습니다. 따라서 흡수성 비강 임플란트 시장은 북미와 유럽에서의 꾸준한 보급을 보완하는 아시아태평양의 판매량 증가의 혜택을 받고 있으며, 현지 구매력과 의료 모델에 맞추어 고가의 약물 방출형 임플란트와 비용 대비 효과가 높은 흡수성 드레싱 간의 균형이 잘 잡혀 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the absorbable nasal implant devices market size is projected to expand from USD 0.65 billion in 2025 and USD 0.7 billion in 2026 to USD 1.03 billion by 2031, registering a CAGR of 8.09% between 2026 to 2031.

This report is Segmented by Product Type (Absorbable Nasal Dressings, Drug-Eluting Sinus Implants, Absorbable Nasal Valve Support Implants, and More), Application (Post-Functional Endoscopic Sinus Surgery, Epistaxis Management, and More), End User (Hospitals, Ambulatory Surgery Centers, and More), and Geography (Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Absorbable Nasal Implant Devices Market Trends and Insights

Rising CRD Prevalence And Surgical Volumes Sustain Demand For In-Sinus Dressings And Implants

The growing prevalence of chronic rhinosinusitis and stable sinus surgery volumes support consistent device utilization in both hospital and ambulatory settings. Postoperative inflammation control and ostial patency maintenance are central goals of care after endoscopic sinus procedures, which have kept drug-eluting and non-drug absorbable implants in routine consideration for postoperative management. Evidence summaries from U.S. clinical and payer reviews report reductions in postoperative interventions when mometasone-eluting implants are placed, which reinforces a data-driven rationale for surgeon adoption.

Specialty societies highlight the role of office-based and ambulatory workflows for select rhinology interventions, which expands the procedural sites where absorbable implants can be used. As the absorbable nasal implant devices market matures, clinicians are combining in-sinus implants with optimized topical steroid regimens to lower revision risk in recurrent polyp cohorts. This steady procedural backdrop helps the absorbable nasal implant devices market sustain predictable demand through the forecast period.

Shift To Office/ASC Rhinology Increases Adoption Of In-Office Implants And Dressings

Ambulatory and office settings are gaining share in rhinology because minimally invasive techniques and local anesthesia can compress care timelines while maintaining patient comfort. SINUVA is indicated for in-office endoscopic placement and delivers mometasone furoate locally over 90 days, which allows clinics to treat recurrent polyps without an operating-room slot or general anesthesia. Coding clarity through CPT 30468 for nasal valve repair defines a billable pathway for submucosal lateral wall implants, which reduces uncertainty for clinic-based valve support procedures. Payer updates that define medical-necessity criteria for sinus surgery and related implants give facilities a clearer view of documentation and coverage expectations for device-enabled care plans.

New office-optimized implants, such as bioabsorbable devices designed for simple one-pass placement and no removal, improve workflow predictability and reduce follow-up burden for busy ENT practices. The Absorbable nasal implant devices market is therefore positioned to benefit from the migration of appropriate cases to outpatient and clinic settings where device-enabled protocols have clear time and cost advantages.

Payer Policies Labeling Nasal Valve Implants/Drug Eluting Stents Investigational Limit Coverage

Commercial payer policies in 2026 classify drug-eluting sinus implants as investigational, citing small sample sizes, limited follow-up, and a lack of direct comparisons against standard topical steroid therapy, which restricts coverage in key U.S. plans. The same dynamic affects absorbable lateral nasal implants for valve collapse, where several plans categorize the technology as investigational even as clinical studies show symptomatic benefit, which complicates patient access and suppresses utilization growth. Investigational labeling drives benefit exclusions in many employer-sponsored plans and shifts costs to patients, which in turn dampens the economics for clinics contemplating broader adoption outside surgical bundles. Other plans maintain investigational status for both absorbable nasal implants and radiofrequency procedures targeted at the nasal valve, emphasizing limitations such as loss to follow-up and lack of head-to-head comparisons with other structural surgeries.

The policy environment remains fluid, which requires device manufacturers to invest in outcomes research and payer education that addresses evidence gaps in a way that aligns with each plan's coverage criteria. This variability slows near-term growth in the absorbable nasal implant devices market despite surgeon interest and supportive real-world experiences.

Other drivers and restraints analyzed in the detailed report include:

- Clinical Evidence For Steroid-Eluting And Valve-Support Implants Improves Outcomes And Reduces Revisions

- Established Coding (E.G., CPT 30468) And Device Approvals Enable Procedure Standardization

- Adverse Events/Foreign-Body Reactions And Extrusion Risks Necessitate Careful Selection

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drug-eluting sinus implants captured 33.60% of absorbable nasal implant devices market share in 2025 and absorbable nasal valve support implants are projected to grow at a 10.86% CAGR from 2026 through 2031, reflecting strong clinician confidence in local corticosteroid delivery for postoperative inflammation control. Evidence summarized for payer decisions shows that steroid-eluting devices reduce postoperative interventions and systemic steroid use compared to non-drug controls, which reinforces their role as core adjuncts after sinus surgery. The PROPEL family delivers mometasone furoate via a bioabsorbable scaffold and has labeling that details elution profiles designed for early healing phases, which anchors clinical utility in the first month after surgery. In-office mometasone-eluting implants target patients with recurrent nasal polyps after prior surgery, providing a 90-day local steroid source to defer or avoid revision procedures for select candidates.

Nondrug absorbable dressings remain essential for septoplasty, rhinoplasty, and sinus procedures where surgeons select degradation timelines that match healing expectations to reduce discomfort and clinic workload. Bioabsorbable spacers and septal splints meet more specialized needs like perforation repair or donor-site coverage in complex reconstructions, which supports premium pricing per case in niche indications. Supply localization in China and India strengthens global availability of compliant absorbable dressings, which protects against logistics shocks and keeps cost-to-serve attractive for public and private hospitals in price-sensitive markets.

Geography Analysis

North America held 41.80% in 2025 as operating-room and clinic-based protocols normalize device use despite payer variability for select indications. U.S. outpatient payment updates that define device-intensive sinus procedures help facilities plan implant utilization within bundles, which supports continued adoption in hospitals and ASCs. Coding and coverage clarity for defined clinical scenarios, including in-office placement for recurrent polyps after prior surgery, supports claims predictability in targeted use cases for facility-based care teams. Specialty societies and payer policy updates provide guardrails that surgeons and administrators use to shape postoperative plans, which support steady demand in the absorbable nasal implant devices market. As coding, training, and outcomes data converge, clinical leaders in the region continue to integrate steroid-eluting and absorbable structural devices into standardized pathways that prioritize patient comfort and reduced revision risk.

Europe demonstrates solid adoption supported by a mature regulatory environment and a strong base of ENT centers that can standardize protocols at scale. Pan-European launches proceed under harmonized regulations that prioritize safety and post-market surveillance for absorbable Class III devices, which aligns with provider expectations for long-term outcomes tracking. Leading markets such as France, the United Kingdom, Italy, and Spain provide an installed base of experienced rhinologists who are familiar with both drug-eluting and nondrug absorbable options, which supports methodical expansion of device-enabled postoperative care. Collaboration across academic and clinical sites supports investigator-initiated research, surgeon training, and clinical audits that reinforce the role of absorbable implants in symptom control and revision reduction in appropriate cohorts. In this environment, the absorbable nasal implant devices market advances through disciplined procurement and surgeon-led protocols that emphasize consistent outcomes across public and private hospitals.

Asia-Pacific is the fastest-growing region with a projected 12.24% CAGR through 2031 as domestic manufacturing and expanding ENT infrastructure increase availability and affordability. Certified manufacturers in China and India supply absorbable dressings and related products to regional and export markets, which reduces logistics risk and supports public-sector procurement at competitive price points. ENT capacity expansion in tier-2 and tier-3 cities drives demand for absorbable dressings and supports adoption of office-optimized implants in private clinics that serve growing middle-income populations. As disposable income and patient awareness rise, ENT providers integrate absorbable implants into postoperative and in-office protocols that emphasize comfort, fewer follow-up procedures, and local therapy for symptom control. The Absorbable nasal implant devices market therefore benefits from volume growth in Asia-Pacific that complements steady adoption in North America and Europe, balancing premium drug-eluting implants with cost-effective absorbable dressings to match local purchasing power and care models.

- Abbott Laboratories

- Aegis Lifesciences

- Boston Scientific

- Conmed

- Cook Group

- GELITA

- Globus Medical

- Hemostasis

- INNOVIA MEDICAL

- Karl Storz

- Lyra Therapeutics

- Mascia Brunelli S.p.a.

- Medtronic

- Meril Life Sciences

- Regenity

- Smiths Group

- Stryker

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising CRD Prevalence and Surgical Volumes Sustain Demand for In-Sinus Dressings and Implants

- 4.2.2 Shift to Office/ASC Rhinology Increases Adoption of In-Office Implants and Dressings

- 4.2.3 Clinical Evidence for Steroid-Eluting and Valve-Support Implants Improves Outcomes and Reduces Revisions

- 4.2.4 Established Coding (E.G., CPT30468) and Device Approvals Enable Procedure Standardization

- 4.2.5 Six-Month Programmable Drug-Eluting Platforms (Next-Gen Implants) Expand Addressable Pool

- 4.2.6 Supply Localization in Asia And India for Absorbable Dressings Lowers Cost-To-Serve

- 4.3 Market Restraints

- 4.3.1 Payer Policies Labeling Nasal Valve Implants/Drug-Eluting Stents Investigational Limit Coverage

- 4.3.2 Adverse Events/Foreign-Body Reactions and Extrusion Risks Necessitate Careful Selection

- 4.3.3 Biologics for CRSWNP Shift Some Candidates Away from Implant-Based Therapy

- 4.3.4 Office/ASC Reimbursement Variability and Lack of Device-Intensive Status Pressure Margins

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Values, USD)

- 5.1 By Product Type

- 5.1.1 Absorbable Nasal Dressings

- 5.1.2 Drug-eluting Sinus Implants

- 5.1.3 Absorbable Nasal Valve Support Implants

- 5.1.4 Absorbable Sinonasal Spacers

- 5.1.5 Others (Bioabsorbable Sinonasal Repair Grafts, Absorbable Septal Splints etc.)

- 5.2 By Application

- 5.2.1 Post-Functional Endoscopic Sinus Surgery

- 5.2.2 Epistaxis Management

- 5.2.3 CRS with Nasal Polyps Drug Delivery

- 5.2.4 Nasal Valve Collapse Support

- 5.2.5 Septal Perforation / Donor-site Repair

- 5.2.6 Others (Post-Traumatic Repair, Iatrogenic Sinonasal Repair)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers (ASCs)

- 5.3.3 Specialty Clinics

- 5.3.4 Others (Academic Institues, Research Institutes)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 Aegis Lifesciences

- 6.3.3 Boston Scientific Corporation

- 6.3.4 Conmed Corporation

- 6.3.5 Cook Medical

- 6.3.6 GELITA

- 6.3.7 Globus Medical, Inc.

- 6.3.8 Hemostasis LLC

- 6.3.9 INNOVIA MEDICAL

- 6.3.10 Karl Storz

- 6.3.11 Lyra Therapeutics

- 6.3.12 Mascia Brunelli S.p.a.

- 6.3.13 Medtronic

- 6.3.14 Meril Life Sciences

- 6.3.15 Regenity

- 6.3.16 Smith+Nephew

- 6.3.17 Stryker

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment