|

시장보고서

상품코드

2063611

실험실 온도 제어 장치 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Laboratory Temperature Control Units - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

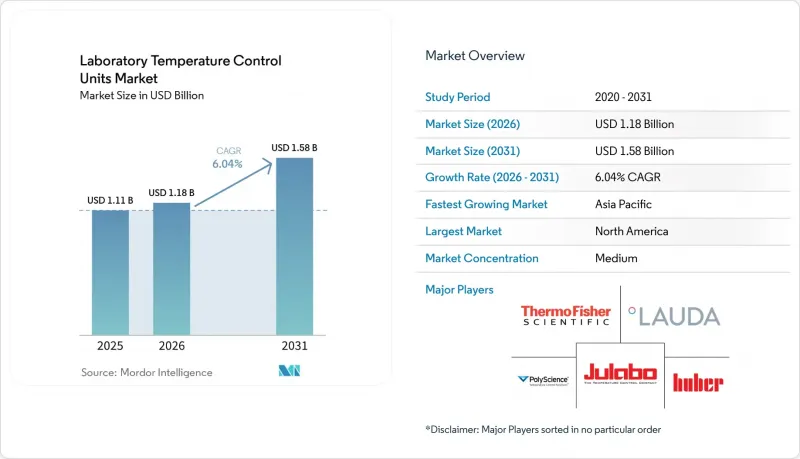

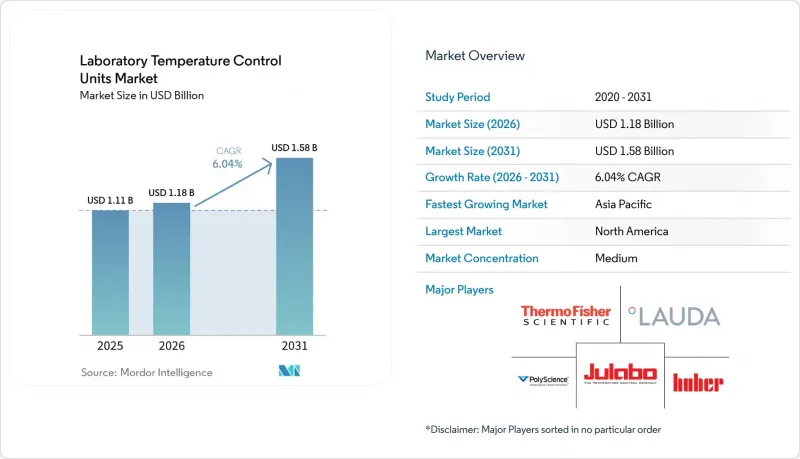

실험실 온도 제어 장치 시장 규모는 2025년 11억 1,000만 달러로 평가되었습니다. 2026년 11억 8,000만 달러에서 2031년까지 15억 8,000만 달러로 확대되어 2026년부터 2031년까지 사이에 CAGR6.04%를 나타낼 것으로 예측됩니다.

본 보고서는 제품별(순환식 칠러 등), 냉각 기술별(공랭식 등), 온도 범위별(-40°C 이하 등), 용량별(0.5kW 미만, 기타), 최종 사용자(제약·바이오기술, 기타), 용도(분석 기기용, 기타), 폼 팩터, 유통 채널 및 지역별로 분류되어 있습니다. 시장 전망은 달러 기준입니다.

세계의 실험실 온도 제어 장치 시장 동향 및 인사이트

제약·바이오기술 분야의 연구 개발이 활발해짐에 따라 정밀 온도 제어에 대한 수요가 증가하고 있습니다.

파이프라인의 압박과 특허 만료에 대한 우려로 인해, 바이오의약품 기업들은 2026년에 실험실 설비 투자를 유지하거나 확대할 수밖에 없으며, 그 결과 고부가가치 분석법을 엄격한 허용 범위 내에 유지하기 위해 필요한 정밀 냉각 및 가열 시스템의 도입 대수가 증가하고 있습니다. 조사 대상이 된 연구개발(R&D) 담당자들은 2025년 실험실 현대화를 통해 처리 능력과 오류율이 개선될 것이라고 강조하고 있으며, 이러한 우선순위는 현재 규제 대상 실험실의 데이터 무결성을 보호하기 위해 보다 엄격한 설정값 제어와 검증된 데이터 로깅을 요구하는 조달 사양으로 이어지고 있습니다. 자금이 바이오의약품, 세포 치료, 차세대 치료법으로 유입됨에 따라, 냉각 요건은 기존 워크플로우보다 더 좁은 반응 속도 및 안정성 범위를 충족하기 위한 동적 온도 제어 방식으로 전환되고 있으며, 이로 인해 실험실용 온도 제어 장치 시장에서 프리미엄 제품의 채택이 확대되고 있습니다. 2025년과 2026년에 중국에서 체결된 경영진 간 제휴를 통해 거래 규모가 신규 실험실 및 분석 핵심 시설을 확장하는 거점으로 이동함에 따라, 아시아태평양 허브 내 온도 제어 시스템의 잠재적 도입 기반이 확대되고 있습니다.

인도의 ‘Bio SHAKTI’ 계획에 따른 5년간 약 10억 8,000만 달러 규모의 예산 배정은 국립 의약품 교육 연구 기관, 임상시험 시설 및 바이오시밀러 생산 능력의 업그레이드가 2026년에 본격화됨에 따라 실행되고 있으며, 이에 따라 합성, 검증, 스테이징 각 워크플로우에서 재순환식 칠러, 냉장 서큘레이터 및 워터배스에 대한 수요가 증가하고 있습니다. 이러한 일련의 노력으로 인해 실험실당 설치 밀도가 높아지면서, 실험실 온도 제어 장치(TCU) 시장의 교체 주기가 연장될 것입니다.

APAC 지역의 실험실 건설 및 장비 도입에 따라 TCU 도입 대수가 증가

중국의 의약품 생산액은 2025년 3.6% 증가한 데 비해, 2026년에는 6.6% 증가했습니다. 이에 따라 자본 예산이 바이오의약품 중심의 파이프라인에 중점을 두게 되면서, 연구개발(R&D)부터 품질관리(QC)에 이르는 각 공정에서 온도 제어에 대한 수요가 증가하고 있습니다. 대만의 산업기술연구원은 2026년 2월에 12인치 반도체 시범 생산 라인의 착공을 시작하여 2027년 말 완공을 목표로 하고 있습니다. 이에 따라 0.1°C 미만의 안정성이 요구되는 리소그래피, 에칭, 계측 장비 분야의 정밀 냉각 수요가 확대될 것입니다. 2026년에는 알켐(Alkem)의 우자인(Ujjain) 제제 공장 및 루핀(Lupin)의 다바사(Dabhasa)에 있는 펩타이드 생산 능력 확충 등, 인도에서 여러 확장 프로젝트가 진행 중이며, 검증 완료된 스위트 내 여러 반응기의 열 부하를 관리하기 위해 중앙 집중식 또는 모듈식 온도 제어 아키텍처가 도입되고 있습니다.

아시아태평양(APAC)에서 분석 장비의 도입이 확대됨에 따라, 디지털 제어를 통합하고 경보 알림을 위해 네트워크에 연결할 수 있는 소형 칠러에 대한 현장 수요도 증가하고 있으며, 이에 따라 실험실용 온도 제어 장치 시장의 진입 기회가 확대되고 있습니다. 상하이, 쑤저우, 하이데라바드, 신주 등 각 클러스터에서 클린룸과 장비의 밀도가 높아지고 있으며, 이에 따라 사이트당 TCU 도입률이 향상되고 있습니다. 제약 및 반도체 프로젝트가 혼재되어 있는 상황에서 APAC 지역의 통합 업체가 사양을 세계 검증 기준에 부합하도록 조정함에 따라, 규정 준수 대응 장치의 리드타임이 단축되어 실험실용 온도 제어 장치 시장의 도입 대수 성장률이 상승하고 있습니다.

새로운 F가스/GWP 규제로 인한 규정 준수 비용 및 재설계

자연 냉매로의 전환에 따라 가연성 및 고압 설계 요건이 부과됨에 따라, 중소용량 유닛의 경우 비용과 복잡성이 증가하여 소규모 공급업체의 이익률이 압박받고 있습니다. A3 냉매 사용이 제한된 실험 시설에서는 환기 시스템이나 안전 인터록을 설계하거나, 설치 면적과 전력 소비를 여전히 복잡하게 만드는 대안을 선택해야 하기 때문에 이로 인해 일부 전환이 지연되고 있습니다. 미국 환경보호청(EPA)은 2025년 9월, 안전 기준의 시행 시기와 성능 측면의 격차로 인해 특정 용도의 경우 규정 준수 유예 기간이 필요하다고 지적했습니다. 이는 정밀 기기 분야에서 여전히 해결 과정에 있는 설계상의 복잡성을 뒷받침하는 것입니다. 2025년부터 2026년에 걸친 유럽의 지침 및 업계 동향은 할당량 축소와 높은 GWP 냉매에 대한 새로운 금지 조치로 인해 유지보수 비용이 상승하고, 일부 기존 설비가 사용 불가능해질 것임을 시사하고 있습니다. 이로 인해 기기 폐기 결정은 앞당겨지겠지만, 구매자가 선택지를 검토하는 과정에서 단기적인 구매가 미뤄질 가능성이 있습니다.

지역별로 여러 SKU를 인증해야 하고, 가장 엄격한 기준을 적용하는 플랫폼에 통합해야 한다는 점은 시장 출시 속도를 늦추고 공급업체의 파이프라인에 부담을 줄 수 있습니다. 이러한 요인들로 인해 2026년 수주량은 일부 위축될 전망이지만, 실험실 온도 제어 장치 시장 전체에서 규제를 준수하는 대체 제품에 대한 수요가 중기적으로 필요하다는 사실은 변함이 없습니다.

부문별 분석

2025년, 순환식 칠러는 실험실 온도 제어 장치 시장 규모의 22.45%를 차지했습니다. 이는 품질 관리(QC) 실험실, 수탁 시험, 그리고 폐쇄 루프 안정성 및 검증된 로깅이 필요한 계측 기기군의 연속 가동 수요에 힘입은 결과입니다. 이 장비들은 물-글리콜 또는 실리콘 오일을 외부 열교환기를 통해 순환시켜, 광범위한 용량 범위를 높은 안정성으로 커버하며, 규제된 워크플로우나 표준화된 시설에 적합합니다. 냉각·가열 서큘레이터는 발열체와 증기 압축 냉각 방식을 결합한 것으로, 1회 운전 중에 주변 온도 및 주변 온도 이하의 설정값을 통과하는 프로토콜을 지원합니다. 가열 서큘레이터는 주변 온도 이상의 용도로 사용되며, 주변 온도 이하의 제어가 필요하지 않은 증발, 증류 및 재킷이 부착된 용기의 공정에서 여전히 수요가 있습니다. 수욕조 및 진동 수욕조는 익숙한 조작성과 저렴한 가격이라는 장점 덕분에 세포 배양, 반응 속도 측정 및 용출 시험에 일반적으로 사용되고 있습니다.

반응 열량 측정, 파일럿 스케일 공정 및 반도체 개발 분야에서는 안전성과 수율 향상을 위해 급격한 온도 상승과 정밀한 오버슈트 제어가 필수적이기 때문에 고동적 범위 온도 제어 시스템 시장은 2031년까지 연평균 성장률(CAGR) 8.85%로 확대될 것으로 전망됩니다. 실험실 온도 제어 장치 시장은 실험실 정보 시스템 및 건물 관리 대시보드와 연동되는 컨트롤러의 개선 덕분에 계속해서 혜택을 보고 있습니다. 각 공급업체는 GMP 환경에서의 가동 시간 보장을 뒷받침하는 다점 센서, 이중화 회로 및 경보 로직을 탑재하고 있습니다. 제품 로드맵에서는 천연 냉매의 채택과 에너지 소비 및 정상 상태의 안정성 간의 균형을 맞추어 인증 시험을 통과하기 위한 인버터 구동 압축기가 강조되고 있습니다.

2025년에는 설치가 간편하고 건물의 배관이나 냉수 루프 없이도 가동할 수 있다는 장점 덕분에 공랭식 시스템이 실험실 온도 제어 장치 시장의 46.22%를 차지하며 1위를 유지했습니다. 수냉식 칠러는 실내의 열 부하를 줄여주며, 대부분의 경우 더 높은 성능 계수(COP)를 달성하지만, 건물과의 통합 및 수처리 시스템이 필요하기 때문에 일부 시설에서는 이러한 설비를 갖추고 있지 않은 경우가 있습니다. 마이크로플루이딕스공학, 칩 상의 장기, 생세포 이미징 분야에서는 진동이 없고 냉매를 사용하지 않는 작동 방식과 정밀한 설정점 제어가 활용되기 때문에 열전식 또는 펠티에식 플랫폼 시장은 연평균 성장률(CAGR) 8.03%로 성장할 것으로 전망됩니다. 극저온 및 CO₂ 보조 시스템은 동결건조나 동결보존 시 -80°C 이하의 초저온 요구 사항을 충족하며, 일반적인 실험실 냉각보다는 특정 프로토콜에 특화되어 있습니다. 하이브리드 방식은 유지보수가 복잡하고 공간 요구 사항이 많기 때문에 실험실에서는 여전히 드물게 사용됩니다. 도입 곡선을 살펴보면, 저부하 영역에서는 열전식 방식이 확대되고, 고부하 영역에서는 공랭식 및 수랭식 플랫폼이 대응하는 등 서로를 보완하는 역할을 확인할 수 있습니다.

팬 및 압축기 제어 기술의 발전으로 인해 다양한 주변 환경에서도 안정성을 유지하면서 계절별 효율이 향상되고 있습니다. 이더넷 및 RS232를 지원하는 컨트롤러 옵션과 데이터 로깅 기능은 감사 추적 및 경보 라우팅을 지원하며, 규제가 엄격한 환경에서 중요합니다. 반도체 및 이미징 연구실에서는 진동과 음향 아티팩트를 줄여주는 저소음 성능이 중요시되고 있으며, 이에 따라 적응형 팬을 탑재한 고품질 공랭식 유닛에 대한 수요가 증가하고 있습니다. 중앙 플랜트의 루프가 설치된 곳에서는 에너지 효율과 열 관리 측면에서 수냉식 유닛이 여전히 유력한 선택지로 남아 있습니다. 각 공급업체들이 자연 냉매로의 전환을 완료함에 따라, 성능 특성은 안정성 지표를 중심으로 더욱 엄격해질 것입니다. 이러한 일련의 변화로 인해, 실험실 온도 제어 장치 시장에서는 용량, 소음, 설치 면적, 통합성 등의 측면에서 용도에 대한 적합성이 계속해서 중요하게 여겨질 것입니다.

0-+100°C의 온도 범위는 2025년 수요의 39.80%를 차지했습니다. 이는 대부분의 분석 장비, 세포 배양 및 재킷이 장착된 반응기가 적정한 안정성을 목표로 이 범위 내에서 가동되고 있기 때문입니다. 바이오프로세스 및 재료 실험실에서 초저온 냉동고, 동결 건조, 환경 시험이 확대됨에 따라, -40°C 이하의 시스템 시장은 2031년까지 연평균 성장률(CAGR) 9.39%로 성장할 것으로 전망됩니다. 다단 냉동 및 CO₂ 캐스케이드 전략은 저온 성능 목표를 유지하면서 EU의 이행 규정을 충족하기 위해 기존의 혼합 냉매를 점차 대체하고 있습니다. 상온 부근의 온도 제어는 제약 및 환경 시험 분야에서 검출기 냉각, 컬럼 오븐, 용출 시험조의 주요 이용 사례로 계속해서 자리 잡고 있습니다. 상온 이하부터 고온 영역에 이르는 광범위한 온도 범위에서는 여전히 냉각형 또는 가열형 서큘레이터가 선호되고 있습니다. ICH 안정성 시험 및 검증 프로토콜 준수에 따라, 품질 관리(QC) 환경에서의 감사 대응을 지원하는 로깅 및 제어 기능에 대한 수요가 증가하고 있습니다.

100°C를 초과하는 온도 범위에서는 오일 냉각식 순환기가 고온 설정점에서 안정성이 요구되는 재료 및 폴리머 공정을 가능하게 합니다. 이 분야에서는 오버슈트를 줄이고, 안전성과 데이터 품질을 위해 온도 상승 추종성을 향상시키는 제어 알고리즘이 유용합니다. 점점 더 많은 프로토콜이 상온 이하와 상온 이상의 가열을 결합하는 방식으로 전환됨에 따라, 구매자들은 광범위한 범위를 포괄하고 높은 안정성을 갖춘 플랫폼으로 통합하는 경향을 보이고 있습니다. 각 공급업체들이 재설계를 완료하고 안전 측면을 고려함에 따라, 자연 냉매 플랫폼은 이러한 범주의 더 많은 분야로 확대되고 있습니다. 장비 교체 후 워크플로우 재인증이 필요한 실험실에서는 검증 키트와 교정 서비스가 구매 결정에 영향을 미치고 있습니다. 이러한 동향에 따라 실험실 온도 제어 장치 시장에서는 활발한 교체 및 업그레이드 추세가 지속되고 있습니다.

지역별 분석

2025년 북미는 실험실 온도 제어 장치 시장 규모의 34.82%를 차지했습니다. 이는 규제 대상인 제약 사업, 주요 연구 대학의 장비군, 그리고 가동 시간 보장 및 서비스 계약에 대한 수요를 높이는 검증된 워크플로우에 힘입은 결과입니다. 칠러에 관한 에너지 및 성능 규제로 인해 가변 속도 구성 요소와 판형 열교환기를 갖춘 고효율 장비에 대한 투자가 집중되고 있으며, 이는 캐나다와 미국의 조달 문서와 일치합니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 10.48%를 나타낼 것으로 예측되며, 이는 정밀 냉각 시스템 도입 대수를 늘리는 제약 및 반도체 생산 능력 확대를 반영한 것입니다. 2026년 중국의 제약 생산 증가와 고부가가치 바이오의약품으로의 광범위한 전환은 연구개발(R&D)부터 품질관리(QC)에 이르기까지 수요를 강화할 것입니다. 대만에서는 2026년 ITRI 시범 라인과 2025년 리가쿠 계측 센터의 개소에 따라, 계측 및 공정 연구 개발 분야에서 정밀한 온도 제어에 대한 수요가 확대될 것입니다. 인도에서는 2026년 알켐(Alkem) 및 루핀(Lupin) 등의 프로젝트를 포함한 생산 확대에 따라, 검증된 제품군에 집중형 및 모듈식 TCU 아키텍처가 도입됨에 따라, 사용 현장 수요와 플랜트 통합형 수요 모두 증가할 것입니다.

유럽에서는 도입 기반이 성숙해 있지만, 냉매에 대한 엄격한 규제로 인해 가능한 한 R-290, R-744 및 고체 열 제어 기술로의 신속한 전환이 요구되고 있습니다. EU의 F가스 규제에서는 2027년과 2032년에 용량에 따른 단기 금지 조치가 설정되어 있으며, 이에 따라 규정을 준수하는 시스템으로의 재설계 및 조달 전환이 가속화되고 있습니다. 이러한 환경에서는 천연 냉매를 활용한 제품 포트폴리오와 검증된 지원 체계를 갖춘 공급업체가 유리한 입지를 차지하게 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the laboratory temperature control units market size is projected to expand from USD 1.11 billion in 2025 and USD 1.18 billion in 2026 to USD 1.58 billion by 2031, registering a CAGR of 6.04% between 2026 to 2031.

This report is Segmented by Product (Recirculating Chillers, and More), Cooling Technology (Air-Cooled, and More), Temperature Range (Below -40 °C, and More), Capacity (<0. 5 KW, and More), End User (Pharmaceuticals & Biotechnology, and More), Application (Analytical Instruments Support, and More), Form Factor, Distribution Channel, and Geography. Market Forecasts in Value USD.

Global Laboratory Temperature Control Units Market Trends and Insights

Pharma And Biotech R&D Intensification Boosts Precision Thermal Control Demand

Pipeline pressure and patent cliffs are forcing biopharma to maintain or raise laboratory capital spending in 2026, which increases the installed base of precision cooling and heating systems needed to keep high-value assays within tight tolerances. Surveyed R&D leaders highlighted throughput and error-rate gains from lab modernization in 2025, and those priorities now cascade into procurement specifications that call for tighter setpoint control and validated data logging that protect data integrity in regulated labs. As capital flows to biologics, cell therapy, and next-generation modalities, cooling requirements shift toward dynamic temperature control for reaction kinetics and stability windows that are narrower than legacy workflows, which expands premium adoption in the Laboratory Temperature Control Units market. Executive partnerships in China during 2025 and 2026 redirected deal value to sites that are scaling new labs and analytical cores, which expands the addressable installed base for thermal control in APAC hubs.

India's Bio SHAKTI allocation of approximately USD 1.08 billion over five years is being executed in 2026 as upgrades to National Institutes of Pharmaceutical Education and Research, clinical trial sites, and biosimilar capacity come online, which raises demand for recirculating chillers, refrigerated circulators, and water baths across synthesis, validation, and staging workflows. This set of actions lifts specification density per lab and expands refresh cycles in the laboratory temperature control units market.

APAC Lab Build-Out And Instrument Installs Expand Installed Base For TCUs

China's pharmaceutical production rose 6.6% in 2026 compared to 3.6% in 2025, which aligns capital budgets with more biopharma-oriented pipelines that intensify temperature control needs at each step from R&D to QC. Taiwan's Industrial Technology Research Institute broke ground on a 12-inch semiconductor pilot line in February 2026 with completion targeted by end-2027, which expands precision cooling demand around lithography, etch, and metrology tools that require sub-0.1 °C stability. Multiple Indian expansions in 2026, including Alkem's formulations site at Ujjain and Lupin's peptide capacity at Dabhasa, are embedding centralized or modular temperature control architectures to manage multi-reactor thermal loads in validated suites.

A growing base of analytical instruments in APAC is also raising point-of-use demand for compact chillers that integrate over digital controls and can be networked for alarms, which broadens entry points for the laboratory temperature control units market. Cleanroom and instrument density are increasing across Shanghai, Suzhou, Hyderabad, and Hsinchu clusters, which supports higher per-site TCU penetration. That mix of pharma and semiconductor projects narrows lead times for compliant units as APAC integrators synchronize specifications to global validation standards, which raises the installed base growth rate in the laboratory temperature control units market.

Compliance Costs And Redesigns Driven By New F Gas/GWP Limits

Transitioning to natural refrigerants imposes flammability or high-pressure design requirements that add cost and complexity to small and mid-capacity units, which erodes margins for vendors without scale. Laboratory campuses with restrictions on A3 refrigerants must either engineer ventilation and safety interlocks or opt for alternatives that still complicate footprint and power, which slows some conversions. The EPA noted in September 2025 that certain applications required compliance extensions due to safety-standard timing and performance gaps, which confirms the engineering complexity still being resolved for precision categories. European guidance and industry notes from 2025 through 2026 signaled that tightening quotas and new bans on high-GWP refrigerants would raise servicing costs and strand some installed equipment, which accelerates end-of-life decisions but can delay near-term purchases as buyers evaluate options.

The need to qualify multiple SKUs by region or converge on the strictest platform reduces speed to market, which can compress vendor pipelines. These factors temper some 2026 ordering but do not change the medium-term need for compliant replacements across the laboratory temperature control units market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift To Low GWP Refrigerants Accelerates Product Refresh And Retrofits

- Lab Sustainability, Energy And Water Efficiency Standards Replace Single Pass Cooling With Recirculating Systems

- Total Cost Of Ownership Constraints In Constrained Lab Spaces

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recirculating chillers commanded 22.45% of the laboratory temperature control units market size in 2025, driven by continuous-duty use in QC labs, contract testing, and instrument clusters that require closed-loop stability and validated logging. These units circulate water-glycol or silicone oil to external heat exchangers and cover broad capacity ranges with tight stability, which aligns with regulated workflows and standardized facilities. Refrigerated or heating circulators combine heater elements with vapor-compression cooling, which supports protocols that pass through ambient and sub-ambient setpoints during one run. Heating circulators serve applications above ambient and remain attractive in evaporation, distillation, and jacketed vessel workflows that do not require sub-ambient control. Water baths and shaking water baths are common in cell culture, kinetics, and dissolution testing based on familiarity and ease of use at lower price points.

Highly dynamic temperature control systems are projected to grow at an 8.85% CAGR through 2031 as reaction calorimetry, pilot-scale processing, and semiconductor development lean on fast ramps and precise overshoot control for safety and yield. The laboratory temperature control units market continues to benefit from controller improvements that integrate with laboratory information systems and building management dashboards. Vendors are embedding multi-point sensors, redundant circuits, and alarm logic that support uptime guarantees in GMP environments. Product roadmaps highlight natural-refrigerant adoption and inverter-driven compressors that balance energy use with steady-state stability to pass qualification tests.

Air-cooled systems led with 46.22% of laboratory temperature control units market share in 2025, supported by simple installation and the ability to operate without building plumbing or chilled-water loops. Water-cooled chillers reduce in-room heat load and often deliver higher coefficients of performance, but they require building integration and treatment regimes that some sites lack. Thermoelectric or Peltier platforms are set to grow at an 8.03% CAGR as microfluidics, organ-on-chip, and live-cell imaging benefit from vibration-free and refrigerant-free operation with precise setpoint control. Cryogenic and CO2-assisted systems serve ultra-low-temperature needs below -80 °C in freeze-drying and cryopreservation, which keeps them focused on specific protocols rather than general lab cooling. Hybrid approaches are still rare in labs due to maintenance complexity and space requirements. The adoption curve shows complementary roles as thermoelectric expands at the low end and air- or water-cooled platforms handle higher loads.

Advances in fan and compressor control improve seasonal efficiency while maintaining stability under varied ambient conditions. Controller options with Ethernet or RS232 and data logging support audit trails and alarm routing, which matters in regulated environments. Semiconductor and imaging labs prize low-noise profiles that reduce vibration and acoustic artifacts, which reinforces demand for premium air-cooled units with adaptive fans. Where central plant loops exist, water-cooled units remain compelling due to energy efficiency and heat management. As vendors complete natural-refrigerant conversions, performance characteristics will continue to tighten around stability metrics. This set of changes keeps the laboratory temperature control units market focused on application fit across capacity, noise, footprint, and integration.

The 0 to +100 °C band accounted for 39.80% of 2025 demand as most analytical instruments, cell culture, and jacketed reactors operate in that span with moderate stability goals. Systems below -40 °C are forecast to expand at a 9.39% CAGR through 2031 as ultra-low-temperature freezers, freeze-drying, and environmental testing scale in bioprocessing and materials labs. Multi-stage refrigeration and CO2 cascade strategies are displacing legacy blends to meet EU transition rules while sustaining low-temperature performance targets. Near-ambient control remains the dominant use case for detector cooling, column ovens, and dissolution baths across pharmaceutical and environmental testing. Wider spans that move from sub-ambient to elevated temperatures continue to back refrigerated or heating circulators. Compliance with ICH stability and validation protocols drives demand for logging and control features that support audit readiness in QC environments.

Above +100 °C, oil-based circulators enable materials and polymer processes that require stability at elevated setpoints. This area benefits from control algorithms that reduce overshoot and improve ramp tracking for safety and data quality. As more protocols combine sub-ambient segments with heating above ambient, buyers often consolidate on platforms that span a wider range with strong stability. Natural-refrigerant platforms are expanding into more of these categories as vendors complete redesigns and address safety considerations. Validation kits and calibration services influence purchase decisions in labs that must re-qualify workflows after equipment changes. These trends sustain a strong replacement and upgrade cadence in the laboratory temperature control units market.

Geography Analysis

North America captured 34.82% of the laboratory temperature control units market size in 2025, driven by regulated pharmaceutical operations, instrument clusters across leading research universities, and validated workflows that raise demand for uptime guarantees and service contracts. Energy and performance rules for chillers concentrate spend on efficient units with variable-speed components and plate heat exchangers, which align with procurement documents in Canada and the United States.

Asia-Pacific is projected to record a 10.48% CAGR through 2031, reflecting pharmaceutical and semiconductor capacity expansions that multiply the installed base for precision cooling. China's 2026 production gains in pharmaceuticals and a broader reorientation to higher-value biopharma reinforce demand from R&D to QC. Taiwan's ITRI pilot line in 2026 and Rigaku's metrology center in 2025 expand demand for tight temperature control in metrology and process R&D. India's manufacturing expansions in 2026, including Alkem and Lupin projects, incorporate centralized and modular TCU architectures in validated suites, which raises both point-of-use and plant-integrated demand.

Europe maintains a mature installed base but faces binding refrigerant rules that push rapid transitions to R-290, R-744, and solid-state thermal control where feasible. The EU F-Gas pathways set near-term bans in 2027 and 2032 by capacity, which accelerates redesigns and procurement shifts to compliant systems. That environment rewards suppliers with natural-refrigerant portfolios and established validation support.

- Applied Thermal Control

- ATS Automation Tooling Systems Inc.

- Avantor

- BUCHI

- Cole-Parmer

- Eaton

- EURODIFROID

- Filtrine

- FRYKA Refrigeration Technology

- Grant Instruments

- Haskris

- Heidolph Instruments

- IKA

- JULABO GmbH

- LabTech S.r.l.

- LAUDA

- Peter Huber Kaltemaschinenbau SE

- PolyScience

- Thermo Fisher Scientific

- Yamato Scientific co., ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pharma and Biotech R&D Intensification Boosts Precision Thermal Control Demand

- 4.2.2 APAC Lab Build-Out And Instrument Installs Expand Installed Base For TCUs

- 4.2.3 Regulatory Shift To Low-GWP Refrigerants Accelerates Product Refresh And Retrofits

- 4.2.4 Lab Sustainability: Energy And Water Efficiency Standards Replace Single-Pass Cooling With Recirculating Systems

- 4.2.5 Rising Cooling Needs For Analytical Instruments (LC/GC-MS, EM) With Higher Throughput And Uptime

- 4.2.6 Thermoelectric/Peltier Control Adoption In Microfluidics, Organ-On-Chip, And Live-Cell Imaging

- 4.3 Market Restraints

- 4.3.1 Compliance Costs And Redesigns Driven By New F-Gas/GWP Limits

- 4.3.2 Total Cost Of Ownership Constraints (Power, Heat Load, Noise) In Constrained Lab Spaces

- 4.3.3 Migration To Central Plant/Closed Loops In New Labs Reduces Some Benchtop Chiller Demand

- 4.3.4 Technician Certification And Low-GWP Refrigerant Servicing Complexity

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Recirculating Chillers

- 5.1.2 Refrigerated/Heating Circulators

- 5.1.3 Heating Circulators

- 5.1.4 Highly Dynamic Temperature Control Systems

- 5.1.5 Laboratory Temperature Controllers

- 5.1.6 Water Baths & Shaking Water Baths

- 5.1.7 Others (Micro-temperature Control Units, Reactor Temperature Control Units, etc.)

- 5.2 By Cooling Technology

- 5.2.1 Air-cooled

- 5.2.2 Water-cooled

- 5.2.3 Thermoelectric (Peltier)

- 5.2.4 Cryogenic/LN2 or CO2-assisted

- 5.2.5 Others (Hybrid vapor-compression, Absorption Cooling Systems)

- 5.3 By Temperature Range

- 5.3.1 Below -40 °C

- 5.3.2 -40 to -20 °C

- 5.3.3 -20 to 0 °C

- 5.3.4 0 to +100 °C

- 5.3.5 Others (+ 100 to +300 °C, Above +300 °C)

- 5.4 By Capacity

- 5.4.1 < 0.5 kW

- 5.4.2 0.5 - 2 kW

- 5.4.3 2 - 5 kW

- 5.4.4 > 5 kW

- 5.5 By End User

- 5.5.1 Pharmaceuticals & Biotechnology

- 5.5.2 Academic & Research Institutes

- 5.5.3 Clinical & Diagnostics

- 5.5.4 Others (CROs, CDMOs)

- 5.6 By Application

- 5.6.1 Analytical Instruments Support (LC/GC-MS, NMR, EM)

- 5.6.2 Lab Reactors & Process Development

- 5.6.3 Sample Conditioning & Thermal Testing

- 5.6.4 Bioprocessing & Cold-Chain Labs

- 5.6.5 Microfluidics & Live-cell Imaging

- 5.6.6 Others (Reagent Preparation & Storage Conditioning, Vaccine Development & Formulation Testing)

- 5.7 By Form Factor

- 5.7.1 Benchtop

- 5.7.2 Floor-standing

- 5.7.3 Rack-mounted

- 5.7.4 Integrated/OEM Modules

- 5.7.5 Others (Under-counter Units, Portable)

- 5.8 By Distribution Channel

- 5.8.1 Direct Sales

- 5.8.2 Distributors

- 5.8.3 e-Commerce

- 5.9 By Geography

- 5.9.1 North America

- 5.9.1.1 United States

- 5.9.1.2 Canada

- 5.9.1.3 Mexico

- 5.9.2 Europe

- 5.9.2.1 Germany

- 5.9.2.2 United Kingdom

- 5.9.2.3 France

- 5.9.2.4 Italy

- 5.9.2.5 Spain

- 5.9.2.6 Rest of Europe

- 5.9.3 Asia-Pacific

- 5.9.3.1 China

- 5.9.3.2 India

- 5.9.3.3 Japan

- 5.9.3.4 Australia

- 5.9.3.5 South Korea

- 5.9.3.6 Rest of Asia-Pacific

- 5.9.4 Middle East and Africa

- 5.9.4.1 GCC

- 5.9.4.2 South Africa

- 5.9.4.3 Rest of Middle East and Africa

- 5.9.5 South America

- 5.9.5.1 Brazil

- 5.9.5.2 Argentina

- 5.9.5.3 Rest of South America

- 5.9.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Applied Thermal Control

- 6.3.2 ATS Automation Tooling Systems Inc.

- 6.3.3 Avantor, Inc.

- 6.3.4 BUCHI

- 6.3.5 Cole-Parmer Instrument Company, LLC

- 6.3.6 Eaton

- 6.3.7 EURODIFROID

- 6.3.8 Filtrine

- 6.3.9 FRYKA Refrigeration Technology

- 6.3.10 Grant Instruments

- 6.3.11 Haskris

- 6.3.12 Heidolph Instruments

- 6.3.13 IKA

- 6.3.14 JULABO GmbH

- 6.3.15 LabTech S.r.l.

- 6.3.16 LAUDA

- 6.3.17 Peter Huber Kaltemaschinenbau SE

- 6.3.18 PolyScience

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Yamato Scientific co., ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment