|

시장보고서

상품코드

2063625

임상 지식 기반 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Clinical Knowledge-Based Platforms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

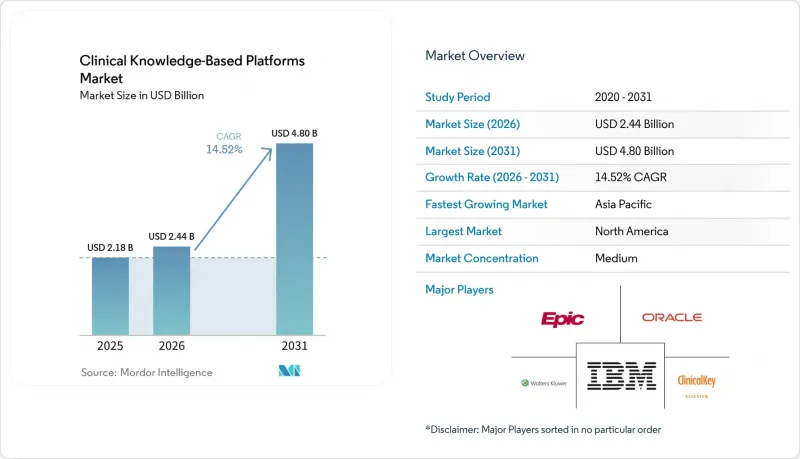

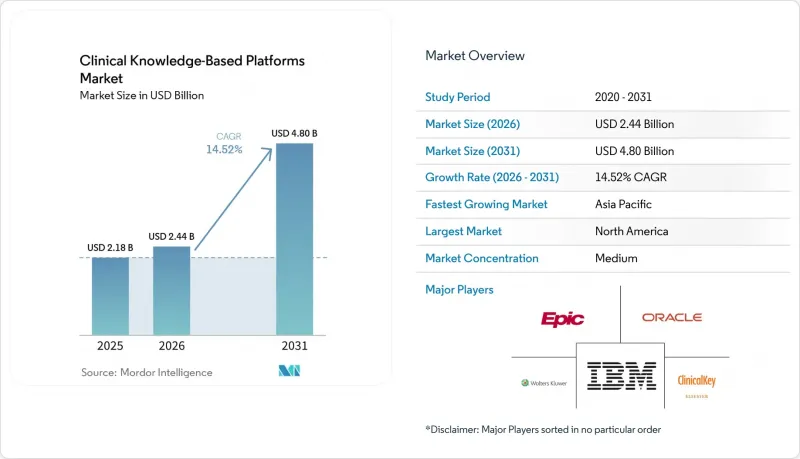

Mordor Intelligence에 의하면, 임상 지식 기반 플랫폼 시장 규모는 2025년에 21억 8,000만 달러로 평가되었습니다. 2026년에 24억 4,000만 달러에서 2031년까지 48억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 14.52%를 나타낼 것으로 전망됩니다.

본 보고서는 도입 모델(클라우드 기반, On-Premise형), 최종 사용자(병원 및 의료 시스템, 기타), 플랫폼 유형(증거 기반 참조 플랫폼, 임상 의사결정 지원 플랫폼, 기타) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 임상 지식 기반 플랫폼 시장 동향 및 인사이트

증거 기반 의료의 도입 확대

의료 시스템은 표준화된 진료 경로를 오더 세트에 반영함으로써 진료의 편차를 줄이고, 입원 일수를 단축하며, 진료 보수를 확보하고 있습니다. 아트로포스 헬스(Atropos Health)의 ‘알렉산드리아(Alexandria)’는 2025년까지 3,300만 건의 근거 자료를 선별하여, 임상의가 단 몇 초 만에 비교 유효성에 대한 답변을 도출할 수 있도록 했습니다. 가이드라인의 양이 수동 검토 능력을 초과하고 있기 때문에 이러한 변화를 가장 크게 체감하고 있는 분야는 종양학과 및 순환기내과입니다. 엘스비어는 2026년 2월, ClinicalKey AI를 300개 이상의 병원으로 확대하고 Epic 및 DrFirst와 통합함으로써, 처방 시 가이드라인 발췌문이 표시되도록 했습니다. 전문의 학회는 현재 그 권고 사항을 업무 흐름에 직접 반영하고 있으며, 이는 즉각적인 준수율 향상으로 이어지고 있습니다. 재입원에 대한 제재가 강화됨에 따라, 임상 지식 기반 플랫폼 시장은 단순한 옵션의 업그레이드가 아닌 업무상 필수 요건이 되고 있습니다.

임상 데이터량의 기하급수적 증가

메이요 클리닉의 APOLLO AI는 2025년까지 250억 건의 임상 사례를 수집하여, 수십 년에 걸친 종단적 기록으로 훈련된 기반 모델을 생성했습니다. 지속 혈당 모니터, 웨어러블 원격 측정, 유전체 패널을 통해 인간의 통합 능력을 뛰어넘는 테라바이트급 데이터가 쏟아져 나오고 있습니다. InterSystems IRIS for Health는 스탠포드 헬스케어의 ChatEHR을 지원하며, 상황에 맞는 기록과 동향을 실시간으로 수집하고 있습니다. 2026년 4월, 『Nature』지는 DxDirector-7B를 발표하며 14개 진료 분야에서 전문의 수준의 진단 정확도를 보여주었습니다. 그러나 파편화된 코딩 방식과 FHIR 도입 현황의 불일치로 인해, 특히 병원 통합이 아직 완료되지 않은 미국에서 여러 의료기관에 걸친 데이터 집계가 저해되고 있습니다.

기존 EHR과의 상호운용성 장벽

많은 병원에서는 여전히 HL7 v2 피드나 독자적인 사양의 데이터 모델이 사용되고 있습니다. 2026년 2월에 발표된 Oracle의 서너(Cerner) 클라우드 이전은 수년에 걸쳐 진행될 예정이므로, 이종 시스템이 혼재된 도입 기반이 그대로 남게 될 것입니다. 의미론적 불일치(“HbA1c” 대 “글리코헤모글로빈”)는 의사결정 지원의 정확도를 저하시킵니다. Smile CDR이나 InterSystems의 미들웨어는 형식 변환이 가능하지만, 처리 지연이 발생하고 유지보수 부담이 증가합니다. 충분한 IT 인력을 확보하지 못한 시설에서는 이러한 어댑터에 대한 패치 적용에 어려움을 겪고 있으며, 이로 인해 지방 및 지역 의료 현장에서 임상 지식 기반 플랫폼 시장 침투가 지연되고 있습니다.

부문별 분석

2025년, 클라우드 기반 부문은 12억 9,000만 달러를 기록하며 임상 지식 기반 플랫폼 시장의 59.38%를 차지해 On-Premise 수요를 크게 앞질렀습니다. Elastic Compute는 대규모 언어 모델에서 발생하는 추론 호출의 급증에 대응하며, 단일 테넌트 아키텍처는 HIPAA 및 GDPR(EU 개인정보보호규정)의 규정 준수 요건을 충족합니다. First Databank의 MedProof 서버는 로컬 설치 없이 하루에 수백만 건의 API 호출을 처리하는 멀티테넌트 클러스터를 운영하고 있습니다. Elsevier는 Azure를 활용하여 300개 이상의 병원에 1초 미만의 시간 내에 근거 자료를 검색할 수 있는 서비스를 제공합니다. 이러한 추세에 따라 클라우드 분야의 연평균 성장률(CAGR)은 15.54%에 달하고, On-Premise 분야의 성장률보다 2배 이상 높으며, 임상 지식 기반 플랫폼 시장 전체의 성장을 주도하고 있습니다.

데이터 주권에 관한 법령이나 에어갭 의무가 우선시되는 경우, 예를 들어 군이나 일부 중국 정부 산하 병원 등에서는 여전히 On-Premise 방식이 계속 사용되고 있습니다. Oracle의 하이브리드형 Cerner 로드맵에서는 정책이 허용하는 한도 내에서 기밀 기록을 로컬에 보관하면서 분석 기능을 클라우드로 이전하고 있습니다. 그러나 패치 적용, 용량 계획 수립, 컨텐츠 업데이트와 같은 작업이 사내 팀에 부담이 되면서, 신규 계약은 매니지드 클라우드나 프라이빗 클라우드 형태로 기울고 있습니다. 자동 갱신 서비스가 포함된 견고한 어플라이언스를 판매하는 벤더는 On-Premise 시장의 잔여 수요를 확보할 수 있겠지만, 장기적인 추세로는 클라우드의 확장이 우세합니다.

지역별 분석

북미는 거의 전역에 걸친 EHR 보급과 성과 기반 보상 페널티의 영향으로, 2025년 임상 지식 기반 플랫폼 시장 매출의 48.26%를 차지했습니다. CMS의 최종 규정은 지급 기관에 FHIR 인터페이스의 공개를 의무화하고 있으며, 이를 통해 API 중심공급업체들이 활성화되고 있습니다. Epic은 현재 175건의 생성형 AI 활용 사례를 개발 중이며, 이는 혁신 주기가 얼마나 빠르게 단축되고 있는지를 보여줍니다. First Databank의 MedProof 출시는 전환 비용을 절감하고, 기존 공급업체에 대한 종속성을 완화하고 있습니다. Epic, Oracle, Meditech 등 여러 시스템에 걸쳐 있는 공급업체의 다양성은 특히 소규모 병원 환경에서 통합의 복잡성을 가중시키고 도입 일정을 지연시키고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 16.44%로 성장을 지속하고, 있으며, 2031년까지 시장 점유율이 거의 두 배로 늘어날 전망입니다. 인도의 ‘아유슈만 바라트 디지털 미션’은 2025년까지 6억 8,000만 건의 건강 ID를 발급하고 26만 개 시설을 등록했습니다. 중국 국가의약품감독관리국(NMPA)은 2024년까지 170건 이상의 AI 의료기기를 승인하고, 현지 임상 추론 데이터 세트를 구축했습니다. 일본의 AI SaMD(소프트웨어 의료기기) 승인 절차와 한국의 ‘디지털 헬스케어법’은 원격의료의 적용 범위를 확대하고 있으며, 이에 따라 원격 모니터링 분야에서 클라우드 기반 CDS(임상 의사결정 지원)에 대한 수요가 증가하고 있습니다. 그러나 다양한 언어 및 데이터 현지화와 관련된 법적 규제로 인해 공급업체는 지역별 고유 온톨로지와 호스팅 영역을 구축할 수밖에 없게 되어, 비용 증가로 이어지고 있습니다.

유럽의 동향은 임상 의사결정 지원을 고위험 범주로 분류하고, 적합성 평가와 시판 후 조사를 의무화하는 EU AI법에 달려 있습니다. GDPR(EU 개인정보보호규정) 규정은 규정 준수 부담을 가중시키지만, 감사를 통과한 품질 관리 시스템을 갖춘 검증된 공급업체에 대한 구매자의 선호도를 높이고 있습니다. 영국 국민보건서비스(NHS)는 디지털 분류 및 원격 모니터링 성과와 연계된 가치 기반 계약을 시범적으로 도입하고 있습니다. 독일, 프랑스, 이탈리아는 2027년까지 ‘유럽 헬스 데이터 스페이스’를 통해 국경을 초월한 데이터의 유동성을 추구하고 있으며, 이를 통해 연합형 CDS 분석이 가능해질 것으로 보입니다. 중동 및 아프리카의 지출은 아직 초기 단계이지만, 사우디아라비아와 아랍에미리트(UAE)가 클라우드 헬스 인프라에 투자하고 있는 지역에서는 그 속도가 빨라지고 있습니다. 한편, 라틴아메리카는 거시경제의 변동으로 어려움을 겪고 있으며, 대규모 확장이 지연되고 있어 서비스 제공업체들은 설비 투자(Capex) 대신 구독형 SaaS로 전환하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the clinical knowledge-Based platforms market size is expected to be USD 2.18 billion in 2025, USD 2.44 billion in 2026, and reach USD 4.80 billion by 2031, growing at a CAGR of 14.52% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premises), End User (Hospitals and Health Systems, and Others), Platform Type (Evidence-Based Reference Platforms, Clinical Decision Support Platforms, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Clinical Knowledge-Based Platforms Market Trends and Insights

Escalating Adoption of Evidence-based Medicine

Health systems are locking standardized pathways into order sets to compress variation, shorten length of stay, and safeguard reimbursement. Atropos Health's Alexandria curated 33 million evidence artifacts by 2025, letting clinicians surface comparative-effectiveness answers in seconds. Oncology and cardiology services feel this shift most acutely because guideline volumes outpace manual review capacity. Elsevier extended ClinicalKey AI to more than 300 hospitals in February 2026, integrating with Epic and DrFirst so guideline snippets appear at prescribing time. Specialty societies now embed their recommendations directly into workflows, raising immediate adherence. As penalties for readmissions intensify, the Clinical Knowledge-Based Platforms market becomes an operational requirement rather than an optional upgrade.

Exponential Growth of Clinical Data Volumes

Mayo Clinic's APOLLO AI ingested 25 billion clinical events by 2025, producing foundation models trained on decades of longitudinal records.Continuous glucose monitors, wearable telemetry, and genomic panels pour terabytes of data that exceed human synthesis capacity. InterSystems IRIS for Health powers Stanford Health Care's ChatEHR, retrieving context-aware notes and trends in real time. In April 2026 Nature published DxDirector-7B, showing specialist-level diagnostic accuracy across 14 disciplines. Yet fragmented coding schemes and inconsistent FHIR adoption hamper multi-site aggregation, especially in the United States where hospital consolidation remains incomplete.

Interoperability Barriers with Legacy EHRs

Many hospitals still run HL7 v2 feeds and bespoke data models. Oracle's Cerner cloud transition announced February 2026 will unfold over years, leaving heterogeneous install bases in place. Semantic mismatches-"HbA1c" versus "glycated hemoglobin"-dilute decision-support accuracy. Middleware from Smile CDR and InterSystems can translate formats but adds latency and maintenance overhead. Facilities lacking robust IT staff struggle to keep these adapters patched, slowing Clinical Knowledge-Based Platforms market penetration in rural and community settings.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates to Reduce Medication Errors

- Expansion of Value-based Care Reimbursement Models

- Alert Fatigue and Clinician Trust Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud-based segment commanded USD 1.29 billion and 59.38% of the Clinical Knowledge-Based Platforms market in 2025, dwarfing on-premises demand. Elastic compute absorbs surges in inference calls from large language models, while single-tenant architectures satisfy HIPAA and GDPR compliance. First Databank's MedProof server runs multi-tenant clusters that handle millions of daily API calls without local installs. Elsevier leverages Azure to deliver sub-second evidence retrieval to more than 300 hospitals. These dynamics propel a 15.54% CAGR for cloud, more than double the on-premises clip, sustaining the broader Clinical Knowledge-Based Platforms market growth narrative.

On-premises deployments persist where data-sovereignty statutes or air-gap mandates prevail, such as military and some Chinese government hospitals. Oracle's hybrid Cerner roadmap keeps sensitive records local while shifting analytics to its cloud when policy permits. Yet patching, capacity planning, and content-update chores burden internal teams, tilting new contracts toward managed or private-cloud variants. Vendors marketing hardened appliances with bundled auto-update services will capture residual on-premises spend, but secular gravity favors cloud expansion.

Geography Analysis

North America contributed 48.26% of 2025 revenue to the Clinical Knowledge-Based Platforms market, buoyed by near-universal EHR penetration and outcome-based reimbursement penalties. The CMS Final Rule compels payers to open FHIR interfaces, stimulating API-centric vendors. Epic records 175 generative AI use cases under development, indicating how quickly innovation cycles shorten. First Databank's MedProof launch lowers switching costs, fragmenting incumbent lock-in. Vendor heterogeneity across systems such as Epic, Oracle, and Meditech increases integration complexity and slows implementation timelines, particularly in smaller hospital settings.

Asia-Pacific is on track for a 16.44% CAGR and will nearly double its share by 2031. India's Ayushman Bharat Digital Mission issued 680 million health IDs and registered 260,000 facilities by 2025. China's NMPA had cleared more than 170 AI medical devices by 2024, creating local clinical-reasoning datasets. Japan's AI SaMD pathway and South Korea's Digital Healthcare Act expand telemedicine codes, lifting demand for cloud CDS in remote monitoring. Diverse languages and data-localization statutes, however, force vendors to build region-specific ontologies and hosting zones, adding cost.

Europe's trajectory hinges on the EU AI Act that classifies clinical decision support as high-risk, mandating conformity assessments and post-market surveillance. GDPR rules elevate compliance overhead but reinforce buyer preference for established vendors with audited quality systems. NHS England pilots value-based contracts linked to digital triage and remote monitoring outcomes. Germany, France, and Italy seek cross-border data liquidity through the European Health Data Space by 2027, which should unlock federated CDS analytics. Middle East and Africa spend remains nascent but accelerates where Saudi Arabia and the UAE invest in cloud health infrastructure, while Latin America wrestles with macroeconomic volatility that delays large-scale rollouts, nudging providers toward subscription SaaS instead of capex.

List of Companies Covered in this Report:

- Ada Health

- BMJ Group

- Clinical Architecture

- EBSCO Information Services

- Elsevier (ClinicalKey)

- Epic Systems

- EvidenceCare

- First Databank

- IBM

- Infermedica

- InterSystems

- Isabel Healthcare

- Oracle

- Persivia

- Spok Holdings

- Thomson Reuters Cortellis

- VisualDx

- Wolters Kluwer Health

- Zynx Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Adoption of Evidence-based Medicine

- 4.2.2 Exponential Growth of Clinical Data Volumes

- 4.2.3 Regulatory Mandates to Reduce Medication Errors

- 4.2.4 Expansion of Value-based Care Reimbursement Models

- 4.2.5 Integration of Large Language Models into Platforms

- 4.2.6 FHIR-based API Marketplaces Enabling Plug-and-Play Services

- 4.3 Market Restraints

- 4.3.1 Interoperability Barriers with Legacy EHRs

- 4.3.2 Alert Fatigue and Clinician Trust Concerns

- 4.3.3 High Implementation Costs for Small Practices

- 4.3.4 IP Litigation Around Proprietary Clinical Algorithms

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Deployment Model

- 5.1.1 Cloud-based

- 5.1.2 On-premises

- 5.2 By End User

- 5.2.1 Hospitals and Health Systems

- 5.2.2 Ambulatory Care Centers

- 5.2.3 Academic and Research Institutes

- 5.2.4 Healthcare Payers

- 5.3 By Platform Type

- 5.3.1 Evidence-based Reference Platforms

- 5.3.2 Clinical Decision Support Platforms

- 5.3.3 Clinical Pathway Management Platforms

- 5.3.4 API-based Knowledge Services

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Ada Health

- 6.3.2 BMJ Group

- 6.3.3 Clinical Architecture

- 6.3.4 EBSCO Information Services

- 6.3.5 Elsevier (ClinicalKey)

- 6.3.6 Epic Systems Corporation

- 6.3.7 EvidenceCare

- 6.3.8 First Databank

- 6.3.9 IBM

- 6.3.10 Infermedica

- 6.3.11 InterSystems

- 6.3.12 Isabel Healthcare

- 6.3.13 Oracle

- 6.3.14 Persivia

- 6.3.15 Spok Holdings

- 6.3.16 Thomson Reuters Cortellis

- 6.3.17 VisualDx

- 6.3.18 Wolters Kluwer Health

- 6.3.19 Zynx Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment