|

시장보고서

상품코드

2063626

대용량 네뷸라이저 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Large Volume Nebulizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

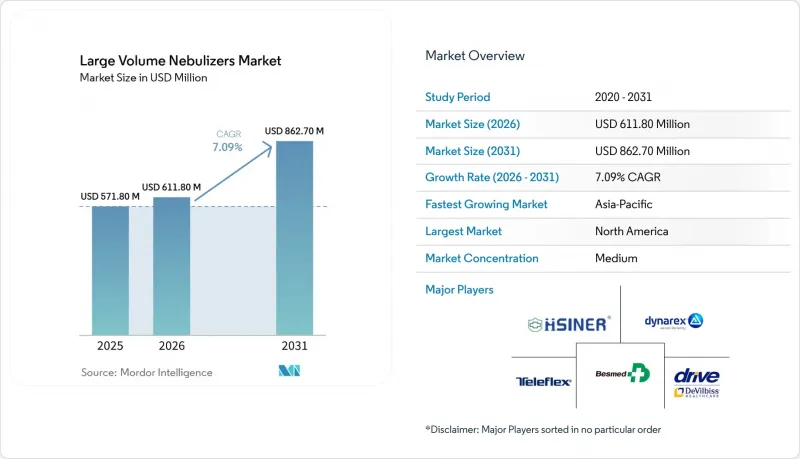

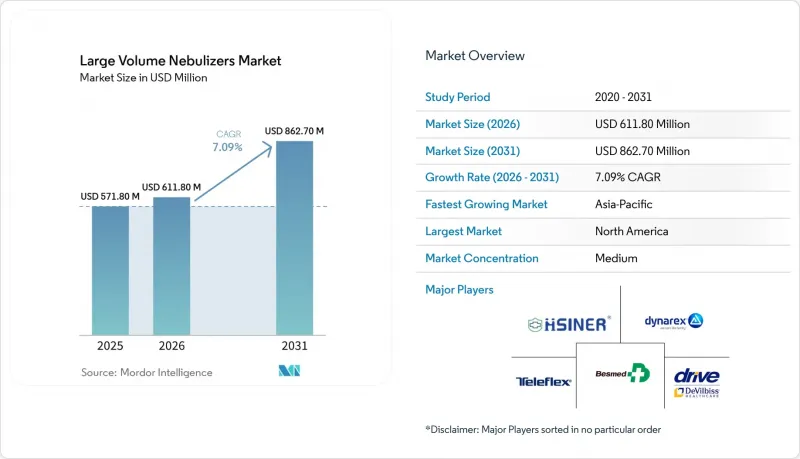

Mordor Intelligence에 의하면, 대용량 네뷸라이저 시장 규모는 2025년 5억 7,180만 달러에서 2026년에는 6억 1,180만 달러로 확대되어 2026년부터 2031년까지 CAGR 7.09%로 성장을 지속하여, 2031년까지 8억 6,270만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형(제트/벤츄리식 LVN, 지속 투여용 LVN 등), 제품 구성(사전 충전된 멸균 리저버식 LVN, 리필 가능/빈 LVN), 리저버 용량(200-300ml 등), 용도(산소 요법용 가습 등), 최종 사용자(병원 등), 지역(북미 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 대용량 네뷸라이저 시장 동향 및 인사이트

급성기 의료 분야의 산소 가습 프로토콜과 지속 에어로졸 요법이 LVN에 대한 안정적인 수요를 견인하고 있습니다.

미국 호흡기 치료 협회의 지침에 따르면, 4 L/분을 초과하는 산소 유량에 대한 가습이 권장됩니다. 이에 따라 응급실 및 병동에서 저산소혈증 환자를 관리하는 데 있어 대용량 네뷸라이저(LVN)의 도입이 확대되고 있습니다. 2026년 연구에서 알부테롤을 10-15mg/h로 투여하는 지속적 기관지 확장제 투여 프로토콜이 간헐적 투여보다 더 뛰어난 효과를 보였으며, 소아 응급실 체류 기간을 13% 단축시키는 것으로 입증되었습니다. 일부 중환자실(ICU)에서는 진동 메쉬 기술이 도입되어 있지만, 다른 병동에서는 예산 제약으로 인해, 특히 장비가 이미 설치되어 있는 관계로 1차 가습에는 제트식 LVN에 계속 의존하고 있습니다. 지속적 에어로졸 요법이 입원율을 낮춘다는 증거가 점점 더 늘어나고 있는 것은 성인 병동에서 LVN을 상시 배치해야 할 필요성을 더욱 확고히 하고 있습니다.

저·중소득 국가(LMICs)에서 산소 접근성 확대가 가습 및 네뷸라이제이션 도입 기반을 확대

세계보건기구(WHO)의 ‘2024년 국가 산소 공급 확대 프레임워크’는 저·중소득 국가(LMICs)에서 압력 스윙 흡착(PSA) 플랜트 및 관련 부속품의 조달을 추진하고 있습니다. 유니세프의 ‘Plant in a Box’ 이니셔티브는 2024년까지 21개국에서 57기의 PSA 시스템을 도입하는 데 성공했으며, 2025년까지 130기로 확대하는 것을 목표로 하고 있습니다. 각 시스템은 최대 100병상을 수용할 수 있습니다. 병원에서 산소 공급을 확대함에 따라, 점막 손상을 방지하기 위해 산소 유량을 가습해야 할 필요성도 동시에 대두되고 있으며, 이로 인해 대용량 네뷸라이저에 대한 수요가 크게 증가하고 있습니다. 『랜싯』 위원회 보고서는 LMICs 환자 중 70%가 여전히 산소 공급을 받지 못하고 있음을 지적하며, 시장의 잠재력을 부각시키고 있습니다. 또한, 세계 ‘옥시젠 얼라이언스’가 40억 달러의 자금 지원을 약속함에 따라 LVN의 판매 전망이 더욱 밝아지고 있습니다.

중환자실(ICU)에서의 약물 투여에 있어, 진동 메쉬식 네뷸라이저는 LVN보다 뛰어난 성능을 발휘합니다.

진동 메쉬 방식 시스템은 삽관 환자에게 연속 제트 방식 LVN에 비해 1.4배에서 3.6배 더 높은 흡입 투여량을 제공합니다. 이러한 시스템은 더 미세한 입자를 생성하고, 잔류량을 최소화하며, 압축 가스의 흐름을 차단함으로써 인공호흡기의 트리거 작동이 더욱 원활하게 이루어지도록 보장합니다. 진동 메쉬 방식 시스템의 단가는 일회용 제트 방식 LVN의 3배에서 5배에 달하지만, 많은 3차 의료 기관의 중환자실(ICU)에는 이 비용을 감당할 수 있는 예산 여유가 있습니다.

부문별 분석

2025년 대용량 네뷸라이저 시장의 매출액 중 63.18%를 제트식 또는 벤츄리식 LVN이 차지했습니다. 이러한 제품들은 심플한 설계, 저렴한 비용, 그리고 벽면용 압축 가스 공급구와의 호환성 덕분에 계속해서 처방집에 채택되고 있습니다. 병원에서는 고유량 산소 회로를 통한 가습, 표준 산소 포트를 통한 간헐적인 약물 투여에 이를 활용하고 있습니다. 대용량 네뷸라이저 시장의 초음파식 기기 시장 규모는 현재 작지만, 장기 요양 의료진이 거의 소음이 없는 작동과 미세한 에어로졸을 제공하는 압전 변환기를 선호함에 따라 연평균 성장률(CAGR) 8.60%로 확대되고 있습니다.

초음파식 모델은 수면 방해를 최소화하고, 야간에도 치료의 연속성을 유지하고자 하는 의료진에게 특히 매력적입니다. B&B;Medical사의 헬리오크스포트를 통합한 HOPE 플랫폼 등의 제품 출시는 차별화 전략을 더욱 부각시키고 있습니다. 그 결과, 구매 담당자들은 스텝다운 병동에서 이러한 프리미엄 장비에 대한 예산 배정을 점차 늘리고 있습니다. 제트식 네뷸라이저는 환자 수가 많은 성인 병동에서 비용 대비 효과가 높기 때문에 앞으로도 주류를 이룰 것으로 보이지만, 2031년에 이르기까지 초음파식 기기의 도입이 확대됨에 따라 그 시장 점유율은 서서히 감소할 것으로 보입니다.

리필 가능한 병은 2025년 매출의 72.81%를 차지하고 있으며, 이는 오랜 구매 습관과 병원에서 조달한 멸균수를 사용할 수 있는 유연성을 반영한 것입니다. 그러나 오염된 세척용 병과 관련된 집단 감염이 발생함에 따라 감시가 더욱 엄격해지고 있습니다. 대용량 네뷸라이저용 프리필드 리저버 시장 규모는 급속히 확대되고 있으며, 2031년까지의 연평균 성장률(CAGR)은 8.37%로 예측됩니다.

작업 시간 및 동작 분석에 따르면, 간호사는 한 번의 준비 작업당 1분 이상을 절약할 수 있으며, 이는 각 교대 근무 중 다수의 환자를 돌보는 과정에서 누적됩니다. 감염 예방 위원회는 리콜 발생 시 추적 가능성을 확보하기 위해 밀봉 포장을 권장하고 있습니다. 이에 대응하여 공급업체들은 무단 개봉 방지 캡이나 레이저 각인을 통한 로트 코드를 도입하고 있으며, 이러한 기능들은 현재 병원의 입찰 사양서에 포함되어 있습니다. 그 결과, 재충전 가능한 제품 시장 점유율은 꾸준히 감소할 것으로 예상되지만, 저·중소득 국가(LMICs)의 예산에 민감한 병원에서는 당분간 이러한 제품을 계속 사용할 가능성이 높을 것으로 보입니다.

지역별 분석

2025년, 북미는 중환자실(ICU)의 충실한 시설, 확립된 의료 프로토콜, 그리고 견조한 의료비 지출에 힘입어 대용량 네뷸라이저 시장에서 42.16%라는 압도적인 점유율을 차지했습니다. 해당 지역에서는 고유량 비강 캐뉼라 장치의 보급으로 인해 여러 과제에 직면해 있지만, 최근 발생한 클래스 I 무균수 리콜로 인해 소매 시장의 선호도가 고부가가치 프리필드 리저버로 이동하면서 시술 건수 감소분을 부분적으로 상쇄하고 있습니다. 캐나다와 멕시코 양국은 지방 병원 개보수 및 산소 파이프라인 정비에 연방 자금을 투입하고 있으며, 가습용 액세서리의 필요성을 강조하고 있습니다. 또한, 2024년 10월 CMS가 발표한 규정에 따라 요양 시설에서의 호흡 요법 보험 적용 범위가 확대됨에 따라 일회용 LVN의 사용이 더욱 촉진되고 있습니다.

아시아태평양은 급속한 성장 궤도에 올라 있으며, 8.44%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 이러한 성장은 중국의 ‘건강 중국 2030’이나 인도의 ‘아유슈만 바라트’ 프로그램과 같은 이니셔티브에 힘입은 산소 생산 분야에 대한 공공 투자가 주된 원동력이 되고 있습니다. 중국이 2024년부터 2026년까지 수립한 1조 2,000억 위안(약 1,700억 달러) 규모의 야심 찬 의료 인프라 예산에는 PSA 플랜트에 대한 투자가 포함되어 있으며, 이것이 LVN의 공동 구매를 촉진하고 있습니다. 한편, 인도는 2027년도 예산에서 응급 의료기기에 대한 예산을 67.66% 대폭 증액하여, 가습 장치에 대한 새로운 입찰의 길을 열었습니다. 동남아시아에서는 각국의 보건부가 부속품 세트를 활용하고 있어, 지방 병원에서 대용량 네뷸라이저의 보급이 더욱 확대되고 있습니다.

유럽, 일본, 한국, 호주 등 성숙한 하위 시장에서는 판매량의 급증이라기보다는 지속가능성에 관한 규제와 감염 방지 정책에 힘입어 기기 교체 수요가 증가하고 있습니다. 유럽에서는 불소계 가스에 대한 유럽연합(EU)의 규제로 인해 정량 분무 흡입기(pMDI)에서 네뷸라이저로의 전환이 가속화되고 있으며, 이는 간접적으로 LVN의 판매를 촉진하고 있습니다. 그러나 고유량 비강 캐뉼라(HFNC)의 보급으로 인해 중환자실(ICU)에서의 잠재적 매출 증가는 제한적입니다. 중동에서는 최근 발표된 걸프협력회의(GCC)의 산소 자급자족을 위한 노력이 이 신흥 지역 수요 증가를 보여주고 있습니다. 국내 PSA 플랜트의 가동이 시작됨에 따라, 2026년 이후 하류 의료기기 출하가 증가할 것으로 예측됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the large volume nebulizers market size is expected to grow from USD 571.80 million in 2025 to USD 611.80 million in 2026 and is forecast to reach USD 862.70 million by 2031 at 7.09% CAGR over 2026-2031.

This report is Segmented by Type (Jet/Venturi LVNs, Continuous Medication LVNs, and More), Product Configuration (Prefilled Sterile Reservoir LVNs, Refillable/Empty LVNs), Reservoir Capacity (200-300 ML, and More), Application (Oxygen Therapy Humidification, and More), End User (Hospitals, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Large Volume Nebulizers Market Trends and Insights

Oxygen Humidification Protocols and Continuous Aerosol Therapy in Acute Care Drive Steady LVN Demand

Guidelines from the American Association for Respiratory Care recommend humidifying oxygen flows exceeding 4 L/min. This has linked the adoption of large volume nebulizers (LVNs) to the management of hypoxemic patients in emergency departments and wards. A 2026 trial demonstrated that continuous bronchodilator protocols, administering 10-15 mg/h of albuterol, outperformed intermittent dosing, leading to a 13% reduction in pediatric emergency department stays. While some intensive care units (ICUs) are adopting vibrating-mesh technology, budget constraints in other wards keep them reliant on jet LVNs for primary humidification, especially since the equipment is already in place. Mounting evidence that continuous aerosol therapy reduces admission rates further solidifies the routine stocking of LVNs in adult units.

Oxygen Access Scale-Up in LMICs Expands Installed Base for Humidification/Nebulization

The World Health Organization's 2024 National Oxygen Scale-Up Framework has driven the procurement of pressure-swing adsorption (PSA) plants and their accessories across low- and middle-income countries (LMICs). UNICEF's "Plant in a Box" initiative successfully deployed 57 PSA systems across 21 countries by 2024, with ambitions for 130 by 2025, each capable of servicing up to 100 beds. As hospitals expand their oxygen supply, they concurrently need to humidify these flows to avert mucosal injuries, significantly boosting the demand for large volume nebulizers. A Lancet Commission highlighted that 70% of patients in LMICs still lack access to supplemental oxygen, underscoring the market's potential.Additionally, the Global Oxygen Alliance's funding commitments of USD 4 billion further bolster the sales outlook for LVNs.

Vibrating-Mesh Nebulizers Outperform LVNs in ICU Drug Delivery

Vibrating-mesh systems deliver 1.4 to 3.6 times higher inhaled doses compared to continuous jet LVNs for intubated patients. These systems produce finer particles, leave minimal residual volume, and eliminate compressed-gas flow, ensuring smoother ventilator triggering. Although the unit price of vibrating-mesh systems is three to five times higher than disposable jet LVNs, many tertiary ICUs have the budget flexibility to absorb this cost.

Other drivers and restraints analyzed in the detailed report include:

- Consolidation Among Leading OEMs/Brands Improves Global Distribution and Contracting

- Shift Toward Single-Patient-Use and Prefilled Sterile Reservoirs for Infection Control

- Post-Pandemic Guidelines Limit LVN Usage in Certain Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Jet or venturi LVNs accounted for 63.18% of 2025 revenue in the large volume nebulizers market. Their straightforward design, low cost, and compatibility with wall-outlet compressed gas ensure their continued inclusion in formularies. Hospitals utilize them for humidification in high-flow oxygen circuits and for intermittent drug delivery through standard oxygen ports. While the market size for ultrasonic devices in large volume nebulizers is currently smaller, it is expanding at an 8.60% CAGR due to the preference of long-term care clinicians for piezoelectric transducers, which provide near-silent operation and finer aerosols.

Ultrasonic models are particularly appealing to staff aiming to minimize sleep disruptions and maintain therapy continuity overnight. Product launches, such as B&B Medical's HOPE platform with an integrated heliox port, highlight differentiation strategies. Consequently, purchasing managers are gradually allocating budgets for these premium devices in step-down units. Jet LVNs are expected to remain prevalent due to their cost-effectiveness in high-volume adult wards, but the adoption of ultrasonic devices will incrementally reduce their market share through 2031.

Refillable bottles represented 72.81% of 2025 sales, reflecting long-standing purchasing habits and the flexibility to use hospital-sourced sterile water. However, outbreaks associated with contaminated rinse bottles have increased scrutiny. The market size for prefilled reservoirs in large volume nebulizers is growing rapidly, with an 8.37% CAGR projected through 2031.

Time-motion studies confirm that nurses save over a minute per setup, which accumulates across numerous patients during each shift. Infection-prevention committees favor sealed packaging for traceability in the event of recalls. Suppliers have responded by introducing tamper-evident caps and laser-etched lot codes, features now included in hospital tender specifications. As a result, forecasts indicate a steady decline in the share of refillables, although budget-conscious hospitals in LMICs are likely to continue using them for the foreseeable future.

Geography Analysis

In 2025, North America commanded a dominant 42.16% share of the large volume nebulizers market, supported by its dense ICU capacities, established medical protocols, and robust healthcare spending. While the region faces challenges due to the widespread adoption of high-flow nasal cannula devices, a recent Class I sterile-water recall has shifted retail preferences toward higher-value prefilled reservoirs, partially offsetting the decline in procedure counts. Both Canada and Mexico are allocating federal funds to upgrade rural hospitals and establish oxygen pipelines, emphasizing the need for humidification accessories. Additionally, a rule from CMS in October 2024 enhances reimbursements for respiratory therapy in skilled-nursing facilities, further encouraging the use of single-patient-use LVNs.

Asia-Pacific is on a rapid growth trajectory, boasting the fastest CAGR of 8.44%. This expansion is largely driven by public investments in oxygen generation, supported by initiatives like China's "Healthy China 2030" and India's "Ayushman Bharat" program. China's ambitious healthcare infrastructure budget of CNY 1.2 trillion (approximately USD 170 billion) for 2024-2026 includes investments in PSA plants, driving co-purchases of LVNs. Meanwhile, India has significantly increased its fiscal 2027 budget for critical-care equipment by 67.66%, paving the way for new tenders on humidification devices. In Southeast Asia, health ministries are leveraging bundled accessory kits, further enhancing the penetration of large volume nebulizers in district hospitals.

Regions like Europe, Japan, South Korea, and Australia, being mature sub-markets, are experiencing upgrades driven by sustainability mandates and infection-control policies, rather than a surge in volume. In Europe, regulations from the European Union concerning fluorinated gases are accelerating the transition from pMDIs to nebulizers, indirectly boosting LVN sales. However, the growth of HFNCs limits potential gains in ICUs. In the Middle East, the recently announced Gulf Cooperation Council's initiative for oxygen self-sufficiency indicates rising demand in this emerging cluster. With domestic PSA plants coming online, they are expected to stimulate downstream device shipments starting in 2026.

- Amsino International, Inc.

- B&B Medical Technologies Inc.

- Besmed Health Business Corp

- Drive DeVilbiss Healthcare GmbH

- Dynarex

- GaleMed Corporation

- Global Healthcare Group

- HSINER Co., Ltd.

- Intersurgical Ltd.

- Protec Somar Industria e Comercio Ltda.

- SunMed Group Holdings, LLC

- Teleflex

- U.P. Medical Salter

- Unitec Hospitalar Ltda.

- VADI Medical Technology Co., Ltd.

- Ventcare Medical

- WestPrime Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Oxygen Humidification Protocols and Continuous Aerosol Therapy in Acute Care Drive Steady LVN Demand

- 4.2.2 Oxygen Access Scale-Up in LMICs Expands Installed Base for Humidification/Nebulization

- 4.2.3 Consolidation Among Leading OEMs/Brands Improves Global Distribution and Contracting

- 4.2.4 Shift Toward Single-Patient-Use and Prefilled Sterile Reservoirs for Infection Control

- 4.2.5 Workforce Efficiency and Bedside Workflow Simplification Favor Prefilled LVNs

- 4.2.6 Policy Headwinds on Propellants (E.G., F-Gas Quotas) Nudge Hospitals Toward Non-pMDI Delivery

- 4.3 Market Restraints

- 4.3.1 ICU Shift to Vibrating Mesh Nebulizers Reduces LVN Use for Ventilated Drug Delivery

- 4.3.2 Aerosol-Generating Procedure (AGP) Precautions Constrain LVN Use in Some Settings

- 4.3.3 Sterile Water/Saline Supply Disruptions and Recalls Periodically Limit LVN Availability

- 4.3.4 High-Flow Heated Humidification and HFNC Substitute LVN-Based Humidification

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Jet/venturi LVNs

- 5.1.2 Continuous medication LVNs

- 5.1.3 Ultrasonic LVNs

- 5.2 By Product Configuration

- 5.2.1 Prefilled sterile reservoir LVNs

- 5.2.2 Refillable/empty LVNs (with clinician-provided water)

- 5.3 By Reservoir Capacity

- 5.3.1 200-300 mL

- 5.3.2 400-600 mL

- 5.3.3 750-1100 mL

- 5.4 By Application

- 5.4.1 Oxygen therapy humidification (wards/ED/ICU)

- 5.4.2 Continuous bronchodilator therapy

- 5.4.3 Sputum induction/airway hydration

- 5.5 By End User

- 5.5.1 Hospitals (ICU/ED/wards)

- 5.5.2 Long-term care facilities

- 5.5.3 Ambulatory/outpatient clinics

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Amsino International, Inc.

- 6.3.2 B&B Medical Technologies Inc.

- 6.3.3 Besmed Health Business Corp

- 6.3.4 Drive DeVilbiss Healthcare GmbH

- 6.3.5 Dynarex Corporation

- 6.3.6 GaleMed Corporation

- 6.3.7 Global Healthcare Group

- 6.3.8 HSINER Co., Ltd.

- 6.3.9 Intersurgical Ltd.

- 6.3.10 Protec Somar Industria e Comercio Ltda.

- 6.3.11 SunMed Group Holdings, LLC

- 6.3.12 Teleflex Incorporated

- 6.3.13 U.P. Medical Salter

- 6.3.14 Unitec Hospitalar Ltda.

- 6.3.15 VADI Medical Technology Co., Ltd.

- 6.3.16 Ventcare Medical

- 6.3.17 WestPrime Systems, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment