|

시장보고서

상품코드

2063636

진통 안약 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Demulcent Eye Drops - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

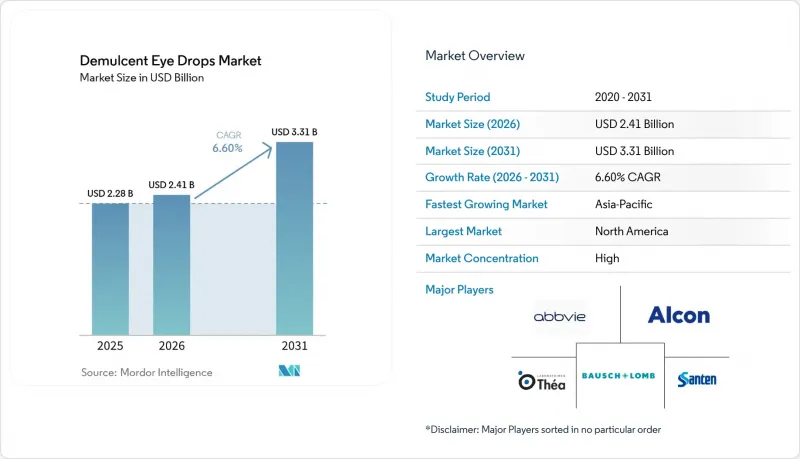

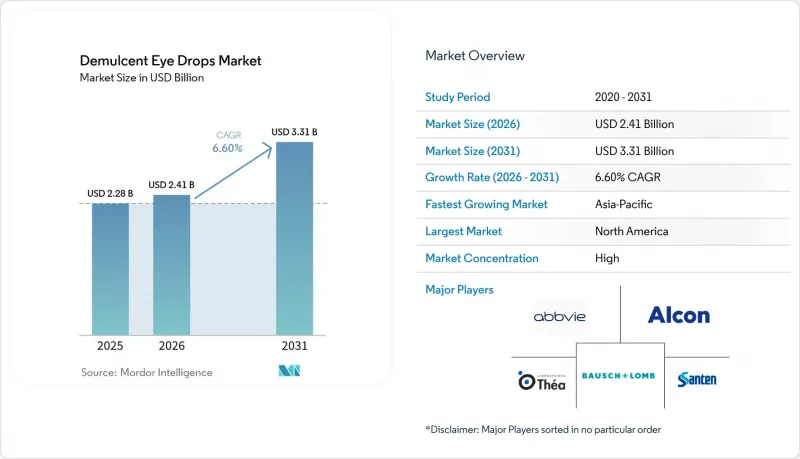

Mordor Intelligence에 의하면, 진통 안약 시장 규모는 2025년 22억 8,000만 달러로 평가되었습니다. 2026년에는 24억 1,000만 달러로 확대되어 2031년까지 33억 1,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.60%를 나타낼 전망입니다.

본 보고서는 유효 성분(글리세린/PEG/PG계 진정제, 셀룰로오스 유도체 등), 제형(방부제 함유 다회 투여용, 방부제 무첨가 단회 투여용, 방부제 무첨가 다회 투여용(MDPF)), 유통 채널(소매 약국, 병원 약국, 온라인 채널 등) 및 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 진통 안약 시장 동향 및 인사이트

고령화와 장시간의 화면 사용으로 인해 안구건조증 발병 빈도와 윤활 안약 사용이 증가하고 있습니다.

고령화와 디지털 라이프스타일의 확산으로 인해, 윤활 안약의 대상 사용자층은 기존의 고령층을 넘어 확대되고 있습니다. 미국에서는 2026년에 4,950만 명의 성인이 시력 장애를 보고했으며, 그중 380만 명은 중증 장애를 앓고 있습니다. 이는 일상적인 증상 완화를 위해 손쉽게 구할 수 있는 치료법에 대한 의존이 지속되고 있음을 보여줍니다. 한국의 인구 통계 자료에 따르면, 지난 5년간 안구건조증 유병률은 8.88%였으며, 여성과 고령층에서 더 높은 비율을 보였는데, 이는 국민건강보험제도 하의 보조 치료 과정에서 윤활제가 수행하는 역할을 뒷받침하고 있습니다. 스크린 노출이 증가함에 따라 젊은 층이 수요에 기여하는 비중이 커지고 있으며, 미국의 조사 결과에 따르면 10대 청소년의 절반이 하루 4시간 이상 학교 밖에서 스크린을 사용하는 것으로 나타났고, 이는 눈 깜빡임 빈도를 감소시키고 눈물막의 안정성을 해칠 수 있는 관련 건강 스트레스 요인으로 보고되고 있습니다. 전 세계 스크린 사용과 건강에 관한 평가에 따르면, Z세대의 일일 스크린 사용 시간은 9시간에 달하며, 과도한 사용은 디지털 눈의 피로 발생률 증가와 관련이 있습니다. 한편, 동아시아 지역의 높은 고도 근시 유병률은 안구 표면에 가해지는 부담을 증가시켜 윤활제 사용을 늘리고 있습니다. 전문 기관들도 아직 해결되지 않은 과제를 강조하고 있으며, 최근 교육 파트너십에서는 안구건조증 증상의 심각성과 지속적인 가정 내 관리의 중요성이 강조되고 있습니다.

방부제 무첨가 제품, 특히 다회 투여용 방부제 무첨가(MDPF) 병으로의 급속한 전환

방부제를 사용하지 않는 다회 투여 방식은 벤잘코늄 클로라이드 및 관련 약제로 인한 불편함과 장기적인 안구 위험을 해소하는 동시에, 1회 투여용 바이알 특유의 취급상의 번거로움을 다시 초래하지 않습니다. 최신 용기에는 일방향 밸브, 밀폐형 필터 시스템 또는 접이식 내부 저장소가 적용되어 있어, 화학 방부제를 사용하지 않고도 개봉 후 수개월 동안 무균 상태를 유지하며, 치료 순응도를 높이는 빈번한 일상적 사용을 가능하게 합니다. 2024년 이후 출시되는 제품들은 이 분야로 결정적으로 전환되고 있으며, 비타민이 강화되고 항산화 시스템이 탑재된 방부제 무첨가 다회용 제품도 포함되어 있어, 주요 체인점 및 온라인 마켓플레이스에서 소매 시장 내 입지를 확대되고 있습니다.

유럽의 임상 실무 지침 및 진료 지침에서는 만성 사용자에 대해 각막의 건강을 보호하기 위해 방부제가 포함되지 않은 요법을 권장하고 있으며, 이는 장기 사용을 위한 MDPF(다회 투여용) 형식으로의 분류 구성을 뒷받침하고 있습니다. 2023년의 오염 사고 및 2026년의 시정 조치를 계기로 강화된 무균성 감시 체계는 제조업체의 무균성 보증에 대한 기대치를 더욱 엄격하게 함으로써, 규제 지침을 이러한 포장 선택과 더욱 일치시키게 되었습니다. 이에 반해, 진통 안약 시장에서는 무균 충전 및 포장 기술에 대한 투자를 확대하고, 가격대에 관계없이 MDPF 제품공급을 늘리고 있습니다.

무균성 및 품질 관련 사고 증가로 인해 규정 준수, 시험 및 리콜 위험이 높아지고 있습니다.

업계는 오염과 관련된 집단 감염 및 이에 따른 무균성 보장 기준을 강화한 규제 당국의 조치로 인해 더욱 엄격한 감시를 받고 있습니다. 2026년 3월, 규제 당국은 310만 병 이상의 제품에 대해 무균성 보증이 불충분하다고 지적하며, 사전 경고에도 불구하고 일부 시설에서 미생물 관리상의 결함이 지속되고 있다는 우려를 표명했습니다. 2023년 초, 여러 주에 걸쳐 집단 감염이 발생하여 중상자와 사망자가 발생한 것을 계기로, OTC(일반의약품) 안약의 제조 및 검사 주기에 대한 광범위한 재검토가 이루어졌습니다. 이러한 영향들이 복합적으로 작용함에 따라, 무균 설비에 대한 투자 증가, 환경 모니터링 강화, 그리고 시장 출시까지의 기간을 연장시키는 제3자 무균성 감사 의무화가 진행되고 있습니다. 중소기업이나 일부 수탁 제조업체의 경우, 이러한 설비 갱신은 부담이 되고 있으며, 제품 포트폴리오의 합리화나 출시 지연으로 이어질 가능성이 있습니다. 따라서 진통 안약 시장은 규정 준수에 따른 비용을 상쇄하고 생산 규모를 유지할 수 있는 무균 제조 및 품질 관리 시스템이 확립된 기존 기업들에게 유리한 상황이 되고 있습니다.

부문별 분석

셀룰로오스 유도체는 2025년에 33.63%의 시장 점유율을 차지했으며, 이는 광범위한 도입 실적, 1회 투여당 낮은 비용, 그리고 약국 재고 구성에서 일관된 채택을 반영한 것입니다. 건성안용 안약 시장은 중등도 증상군을 대상으로 한 일상적인 증상 완화 및 익숙한 질감과 예측 가능한 사용감을 선호하는 사용자를 위해 계속해서 이러한 고분자에 의존하고 있습니다. 고점도 카르복시메틸셀룰로오스는 야간용이나 중증 건조증 치료 시 안구 표면에서의 체류 시간을 연장할 수 있는 반면, 하이드록시프로파일메틸셀룰로오스는 투여 후 즉각적인 효과를 원하는 사용자에게 적합합니다. 나트륨 히알루론산은 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 9.24%로 성장하고 있습니다. 이는 고분자량 등급이 마찰을 줄이고, 수분을 효과적으로 유지하며, 상피의 안정성을 지원함으로써, 범용 폴리머에 비해 착용감 면에서 우월함을 느끼게 하기 때문입니다. 미국 제품 라벨의 공개 정보에 따르면, 제네릭 CMC 제제조차도 비활성 첨가제로 히알루론산을 포함하는 경우가 많은데, 이는 시장이 HA 특유의 윤활성과 컨디셔닝 특성을 선호하고 있음을 보여줍니다. 한국에서는 처방 경향을 볼 때, 민감한 눈에 대한 1회용 히알루론산 제제의 사용이 두드러지며, 이는 임상의들이 오랫동안 중시해 온 ‘방부제 무첨가’ 투여 형태와 일치합니다.

현재 진통 안약 시장에서는 트레할로스나 HP-구아와 같은 생체 모방성 첨가제가 조합되어, 기본적인 윤활 작용을 넘어 쾌적성을 높이고, 증발성 안구건조증이나 표면 스트레스에 대처하고 있습니다. 유중수형 에멀젼이나 무수 제제는 지질층을 안정화시키고 눈물의 증발을 늦춤으로써 마이봄선 기능 부전 치료에서 그 역할을 확대하고 있으며, 이는 수성 성분에 중점을 둔 약제를 보완하는 역할을 합니다. 독일의 임상 지침에서는 건조감에는 히알루론산을, 자극이나 표면의 미세 손상에는 판테놀을 권장하고 있으며, 일상적인 증상 완화를 위해 성분을 최우선으로 고려하는 접근 방식을 제시하고 있습니다. 아시아 지역 각 기업의 파이프라인에서는 고농도 분비 촉진제 및 보조적 진정제 요법과 통합 가능한 차세대 약물이 중시되고 있으며, 이는 예측 기간 동안 해당 카테고리 시장 깊이를 유지하는 데 기여하고 있습니다. 진통 안약 업계는 셀룰로오스 계열 제품이 형성한 판매량 기반과, 접근성을 저해하지 않으면서 카테고리 전체의 가치를 강화하는 히알루론산 계열 프리미엄 제품 간의 균형을 맞추는 위치에 있습니다.

지역별 분석

2025년에는 임상의, 보험사, 소매업체가 일반의약품(OTC) 및 처방전 기반 형태의 무방부제 제품에 대한 접근성 확대에 주력한 결과, 북미가 36.47%의 점유율을 차지했습니다. 미국에서는 인구 통계에 따르면 수천만 명의 성인이 시각 장애를 호소하고 있으며, 이는 윤활제를 통해 간편하게 일상적인 증상 완화를 원하는 소비자층이 매우 광범위함을 보여줍니다. 2023년과 2026년에 발생한 리콜은 무균 기준에 대한 대중의 인식을 높이고, 제조업체에 대한 더 엄격한 감시를 촉발했습니다. 이러한 추세는 무균 라인의 효과가 입증된 확고한 브랜드에 힘을 실어줄 것입니다. 이 지역의 주요 기업들의 확장 투자는 국내 공급의 신뢰성과 방부제 무첨가 제품 라인의 생산 능력 확대에 대한 지속적인 노력을 보여주고 있습니다. 진통 안약 시장은 제품 처방 및 포장에서 프리미엄화 추세를 계속해서 반영하고 있으며, 전국의 소매점과 온라인 쇼핑몰에서 널리 판매되고 있습니다.

아시아태평양에서는 고령화, 도시형 생활 방식, 그리고 화면 노출 증가로 인해 증상의 심각도와 빈도가 높아지고 있어, 2031년까지 연평균 성장률(CAGR) 9.34%를 나타낼 것으로 전망됩니다. 중국의 대규모 제조 프로젝트는 2027년까지 무균 생산 능력을 대폭 확대할 계획이며, 이는 방부제가 첨가되지 않은 매일 사용형 안약에 대한 국내 수요 증가에 맞추어 생산 체계를 구축하기 위한 것입니다. 한국 전역의 데이터에 따르면, 특히 여성과 고령층에서 안구건조증 유병률이 증가하고 있으며, 이로 인해 임상 현장에서 방부제가 첨가되지 않은 1회용 히알루론산 점안제의 사용이 확대되고 있습니다. 인도에서는 콘택트렌즈의 보급 확대와 도시 지역의 대기질 문제로 인해 안구 표면에 가해지는 부담이 커지고 있으며, 대량 소비를 전제로 한 가격대의 일상용 윤활제 제품에 대한 수요가 증가하고 있습니다. 일본의 지침에 따르면, 민감한 눈이나 만성 증상에 대한 치료 시 방부제가 함유되지 않은 히알루론산 점안제의 사용이 권장되고 있으며, 이러한 진료 체계는 다양한 이용 사례에서 MDPF(마이크로도즈 프레셉트 포뮬레이션) 및 일회용 제품의 채택을 뒷받침하고 있습니다. 진통 안약 시장은 가격대에 따라 자주 사용하는 소비자에 대응하는 포장 기술의 발전과 판매량 증가 사이의 균형을 맞출 준비가 되어 있습니다.

유럽에서는 성숙한 수요와 방부제 무첨가 시스템 및 특수 제형 분야의 지속적인 혁신이 균형을 이루고 있습니다. 독일의 임상 지침에서는 안구건조증에는 히알루론산을, 자극에는 판테놀을 권장하는 한편, 특히 제품을 자주 사용하는 사용자의 경우 방부제의 장기 사용에 주의를 당부하고 있으며, 이것이 무방부제 제품 시장 점유율 유지를 뒷받침하고 있습니다. 의료 제도에 따라 안구건조증 치료를 보험 적용 대상인지, 아니면 OTC(일반의약품)로 분류할지가 달라지며, 그 결과 약국 주도의 판매와 의사의 처방에 따른 구성 비율에 차이가 발생하고 있습니다. 유럽 내 포트폴리오 확대 전략에는 5개 주요 시장에서 현지 안과 제품 라인업을 확충하고, 안구건조증 및 관련 치료에 대한 접근성을 높이는 인수가 포함되어 있으며, 규모 확대와 유통 효율 향상을 목표로 한 통합 계획이 수립되어 있습니다. 또한, 안약 시장에서는 일상적인 윤활 및 편안함 관리를 보완하는 질환 수정 요법을 추진하기 위한 지역 내 조사 제휴도 긍정적인 요인으로 작용하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 장기적인 증상 관리에 적합한 무방부제 제품 라인, 생체 모방성 첨가제 및 투여 형태에 대한 견고한 기반이 마련되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the demulcent eye drops market size is expected to increase from USD 2.28 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.31 billion by 2031, growing at a CAGR of 6.60% over 2026-2031.

This report is Segmented by Active Ingredient (Glycerin/PEG/PG Demulcents, Cellulose Derivatives, and More), Formulation (Preserved Multi-Dose, Preservative-Free Unit-Dose, Preservative-Free Multi-Dose MDPF), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Channels, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Demulcent Eye Drops Market Trends and Insights

Aging Populations and Prolonged Screen-time Intensify Dry Eye Episodes and Lubricant Drop Usage

An aging base and digital lifestyles expand the addressable user pool for lubricating drops beyond the traditional senior cohort. In the United States, 49.5 million adults reported vision difficulty in 2026, including 3.8 million with severe trouble, which signals sustained reliance on accessible therapies for daily symptom relief. Population data from South Korea indicate an 8.88% dry-eye prevalence over five years with higher rates among women and older adults, reinforcing the role of demulcents in supportive care pathways in universal coverage settings. Younger cohorts are contributing more to demand as screen exposure rises, with U.S. survey findings showing half of teens record 4 or more hours of non-school screen time per day and report associated health stressors that can reduce blink frequency and disrupt tear film stability. Global screen health assessments place Gen Z daily exposure at 9 hours and link heavy use to higher digital eye strain incidence, while high myopia prevalence figures in East Asia compound ocular surface stressors that increase lubricant use. Professional organizations also highlight unmet burden, with recent education partnerships underscoring the scale of dry-eye symptoms and the role of consistent at-home care.

Rapid Shift to Preservative-free Formats, Notably Multi-dose Preservative-free (MDPF) Bottles

Preservative-free multi-dose designs address the discomfort and long-term ocular risk associated with benzalkonium chloride and related agents, without reintroducing handling friction tied to unit-dose vials. Modern containers deploy one-way valves, closed-system filters, or collapsible inner reservoirs that maintain sterility for months after opening without chemical preservatives and enable frequent daily use patterns that support adherence. Product launches since 2024 have moved decisively into this space, including preservative-free multi-dose offerings with vitamin enrichment and antioxidant systems that broaden positioning at retail across major chains and online marketplaces.

European clinical practice content and clinic guidance favor preservative-free regimens for chronic users to protect corneal integrity, which nudges category mix toward MDPF formats for long-term use. Heightened sterility oversight after 2023 contamination events and follow-on actions in 2026 has further aligned regulatory signals with these packaging choices by tightening expectations on manufacturers' assurance of sterility. The demulcent eye drops market has responded with greater investment in aseptic filling and packaging technologies that scale MDPF availability across price points.

Heightened Sterility/Quality Incidents Elevate Compliance, Testing, and Recall Risks

The industry faces tighter oversight following contamination-linked outbreaks and subsequent enforcement actions that raised the bar on sterility assurance. In March 2026 regulators flagged over 3.1 million bottles for lack of sterility assurance, reinforcing concerns that some facilities had persistent microbiological control gaps despite prior warnings. Earlier in 2023, multi-state outbreaks caused severe injuries and fatalities, which catalyzed a wide review of OTC eye drop manufacturing and inspection cycles. The combined effect has been higher capital spending on aseptic equipment, more robust environmental monitoring, and mandatory third-party sterility audits that lengthen time-to-market. Smaller firms and some contract manufacturers face strain from these upgrades, which can lead to portfolio rationalization or delayed launches. The demulcent eye drops market therefore tilts toward incumbents with validated sterile production and quality systems that can absorb compliance overhead and maintain scale.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Online/Omnichannel Pharmacy and DTC Fulfillment for OTC Eye Lubricants

- Rising Contact Lens Wear and Post-procedure Ocular Surface Care Increase Drop Intensity

- Limited Head-to-head Superiority, Brand Switching and Private-label Pressure Commoditize

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cellulose derivatives held 33.63% share in 2025, reflecting a wide installed base, low per-dose cost, and consistent inclusion across pharmacy assortments. The demulcent eye drops market continues to rely on these polymers for day-to-day relief in moderate symptom clusters and for users who prefer familiar textures and predictable handling. Higher-viscosity carboxymethylcellulose can increase residence time on the ocular surface for overnight or severe-dryness regimens, while hydroxypropyl methylcellulose suits users who need clarity for immediate activity after dosing. Sodium hyaluronate is accelerating at 9.24% CAGR over 2026-2031 as high molecular weight grades lower friction, bind water effectively, and support epithelial stability, creating perceived comfort advantages over commodity polymers. Disclosures in U.S. product labels indicate that even generic CMC formulations often include hyaluronate as an inactive excipient, a signal of how the market prefers lubricity and conditioning characteristics associated with HA. In South Korea, prescribing patterns show strong use of single-use hyaluronate for sensitive eyes, aligning with long-standing clinician emphasis on preservative-free delivery.

The demulcent eye drops market now layers biomimetic excipients such as trehalose and HP-guar to extend comfort and address evaporative dryness and surface stress beyond basic lubrication. Oil-in-water emulsions and water-free vehicles are expanding roles in meibomian gland dysfunction as they stabilize the lipid layer and slow tear evaporation, which complements aqueous-focused agents. Guidelines in German practice literature recommend hyaluronic acid for dryness sensations and panthenol for irritation or surface micro-injury, pointing to an ingredient-first approach for daily relief. Company pipelines in Asia emphasize higher-concentration secretagogues and next-generation agents that can integrate with supportive demulcent regimens, and this supports continued category depth through the forecast period. he demulcent eye drops industry is positioned to balance cellulose-based volume anchors with hyaluronate-led premium tiers that reinforce overall category value without disrupting access.

Geography Analysis

North America accounted for 36.47% share in 2025 as clinicians, payers, and retailers converged on wider access to preservative-free options across OTC and prescription-adjacent formats. In the United States, population statistics show that tens of millions of adults report vision difficulty, which underscores the large base of consumers who seek accessible daily relief through lubricants. Recalls in 2023 and again in 2026 heightened public awareness of sterility standards and catalyzed more robust oversight of manufacturers, a trend that supports established brands with validated aseptic lines. Expansion investments by leading companies in the region point to ongoing commitment to domestic supply reliability and scaled throughput capacity for preservative-free lines. The demulcent eye drops market continues to reflect premiumization in product formulation and packaging with extensive presence across national retail and e-commerce.

Asia-Pacific is expected to deliver a 9.34% CAGR through 2031 as older demographics, urban lifestyles, and higher screen exposure elevate symptom intensity and frequency. Large-scale manufacturing projects in China are timed to bring substantial sterile capacity online by 2027, which aligns production with rising domestic demand for preservative-free daily-use drops. South Korea's nationwide data show elevated dry-eye prevalence, particularly among women and older age groups, which supports the use of preservative-free single-use hyaluronate in clinical practice. In India, contact-lens growth and urban air quality challenges amplify ocular surface stress and expand the need for daily lubrication products in volume-led price tiers. Japan's guidance encourages preservative-free hyaluronate in sensitive or chronic regimens, and this practice structure complements the adoption of MDPF and single-use lines across use cases. The demulcent eye drops market is prepared to balance volume growth with packaging advances that serve high-frequency users across tiered price points.

Europe balances mature demand with continued innovation in preservative-free systems and specialized formulations. Clinical guidance in Germany recommends hyaluronic acid for dryness and panthenol for irritation while cautioning against prolonged use of preservatives, especially in frequent users, which supports continued share for preservative-free ranges. Health systems differ in how they route dry-eye therapies across reimbursement channels and OTC, which results in varied mix between pharmacy-led sales and clinician-directed prescribing. Portfolio moves in Europe include acquisitions that expand local ophthalmology offerings across five major markets and broaden access to dry eye and related therapies, with integration plans aimed at improving scale and distribution efficiency. The demulcent eye drops market also benefits from research partnerships in the region designed to advance disease-modifying approaches that complement daily lubrication and comfort regimens. Together, these drivers create a stable foundation for preservative-free lines, biomimetic excipients, and dosing configurations that better match long-term symptom management.

- Abbvie

- AFT Pharmaceuticals

- Alcon

- Bausch + Lomb

- Bayer

- The Cooper Companies

- I-MED Pharma inc.

- Laboratoires Thea

- Menicon

- OASIS Medical

- OCuSOFT

- Prestige Consumer Healthcare

- Reckitt

- ROHTO Pharmaceutical Co.,Ltd.

- Santen Pharmaceuticals

- SEED Co., Ltd.

- Sentiss

- Similasan Corporation

- URSAPHARM Arzneimittel GmbH

- VISUfarma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Populations and Prolonged Screen-time Intensify Dry Eye Episodes and Lubricant Drop Usage

- 4.2.2 Rapid Shift to Preservative-free Formats, Notably Multi-dose Preservative-free (MDPF) Bottles

- 4.2.3 Expansion of Online/Omnichannel Pharmacy and DTC Fulfillment for OTC Eye Lubricants

- 4.2.4 Rising Contact Lens Wear and Post-procedure Ocular Surface Care Increase Drop Intensity

- 4.2.5 PF multi-dose Bottle Designs (one-way valve/filters) Reduce Contamination Fears and Boost Daily Use

- 4.2.6 Biomimetic Excipients (HA/trehalose/HP-Guar) Enable Premiumization and Regimen Bundling

- 4.3 Market Restraints

- 4.3.1 Heightened Sterility/Quality Incidents Elevate Compliance, Testing, and Recall Risks

- 4.3.2 Limited Head-to-head Superiority; Brand Switching and Private-label Pressure Commoditize

- 4.3.3 Trade/tariff Shocks and GMP Upgrades Inflate COGS for Demulcents and Packaging

- 4.3.4 Capital-intensive Aseptic Filling and PF Packaging Slow Smaller Entrants and Launches

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Active Ingredient

- 5.1.1 Glycerin / PEG / PG demulcents

- 5.1.2 Cellulose derivatives

- 5.1.3 Sodium hyaluronate (HA)

- 5.1.4 Oil-based Emulsion Tears

- 5.1.5 Polyvinyl Alcohol / Povidone

- 5.1.6 Dextran 70 Combinations

- 5.2 By Formulation

- 5.2.1 Preserved multi-dose

- 5.2.2 Preservative-free unit-dose (vials)

- 5.2.3 Preservative-free multi-dose (MDPF)

- 5.3 By Distribution Channel

- 5.3.1 Retail Pharmacies

- 5.3.2 Hospital Pharmacies

- 5.3.3 Online Channels

- 5.3.4 Ophthalmic & Optical Stores

- 5.3.5 Supermarkets & Hypermarkets

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AbbVie (Allergan)

- 6.3.2 AFT Pharmaceuticals

- 6.3.3 Alcon

- 6.3.4 Bausch + Lomb

- 6.3.5 Bayer AG

- 6.3.6 CooperVision

- 6.3.7 I-MED Pharma inc.

- 6.3.8 Laboratoires Thea

- 6.3.9 Menicon

- 6.3.10 OASIS Medical

- 6.3.11 OCuSOFT

- 6.3.12 Prestige Consumer Healthcare Inc.

- 6.3.13 Reckitt

- 6.3.14 ROHTO Pharmaceutical Co.,Ltd.

- 6.3.15 Santen Pharmaceutical Co., Ltd.

- 6.3.16 SEED Co., Ltd.

- 6.3.17 Sentiss

- 6.3.18 Similasan Corporation

- 6.3.19 URSAPHARM Arzneimittel GmbH

- 6.3.20 VISUfarma

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment