|

시장보고서

상품코드

2063652

액체 충전 하드 캡슐 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Liquid Filled Hard Capsules - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

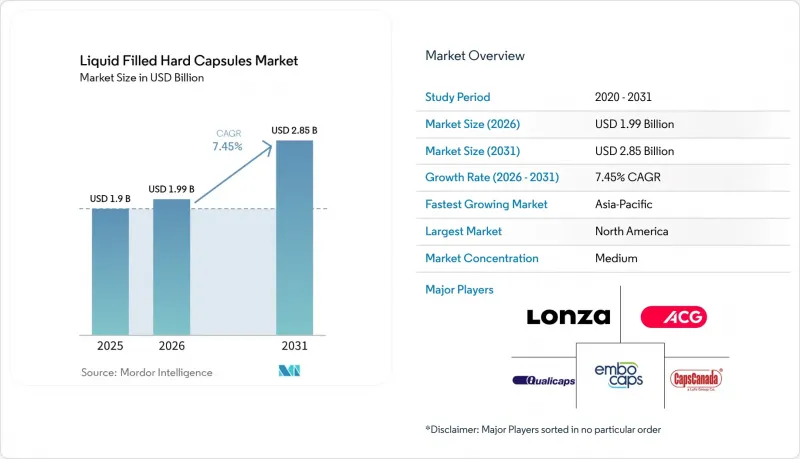

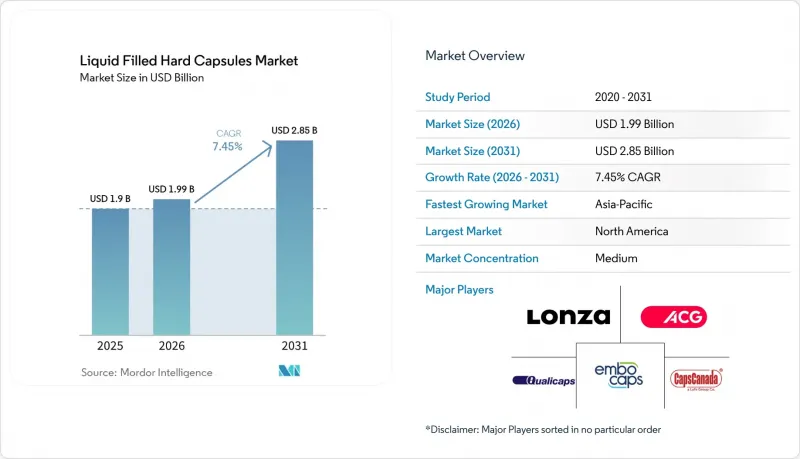

Mordor Intelligence에 의하면, 액체 충전 하드 캡슐 시장 규모는 2025년에 19억 달러, 2026년에 19억 9,000만 달러, 2031년까지 28억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 7.45%로 성장할 전망입니다.

본 보고서는 코팅 재료(젤라틴, HPMC, 풀루란/기타 셀룰로오스), 충전 상태(유성 액체, 현탁액, 반고체/핫멜트 충전 등), 밀봉 방법(밴딩, 락온리 등), 최종 용도(처방약, 일반의약품 등), 방출 프로파일(즉시 방출, 서방형), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 액체 충전 하드 캡슐 시장 동향 및 인사이트

수용성이 낮은 API의 생체이용률 향상이 액체 제형의 채택을 촉진

새로운 저분자 화합물 후보의 대부분은 수용성이 낮기 때문에 개발팀은 위장관 내에서의 용해성과 흡수성을 높이기 위해 SEDDS나 SMEDDS와 같은 지질 기반 액체 충전 전략을 채택하고 있습니다. 이러한 시스템은 오일과 계면활성제 및 보조 계면활성제를 조합함으로써, 장액과 접촉했을 때 자발적으로 미세한 에멀젼을 형성하여 계면적을 증가시키고, 보다 예측 가능한 흡수를 가능하게 합니다. 액체 충전 하드 캡슐 시장에서 이러한 접근 방식은 BCS 등급 II 및 IV 화합물의 약물 노출 변동성을 줄이려는 목적과 부합합니다. 이러한 화합물은 기존의 정제 형태로 투여될 경우, 혈장 농도 프로파일에 편차가 발생할 수 있습니다.

각 제조업체는 이러한 충전 내용물에 대해 가교 반응이나 습기로 인한 열화를 방지할 수 있는 캡슐 껍질을 선정함으로써, 보관 기간 내내 용해 동태의 일관성을 유지하고 있습니다. 규제 체계와 약전 기준은 액체 경구 제형에 대한 품질 설계(QbD)의 실천을 뒷받침하며, 이러한 캡슐 제형의 개발 및 규모 확대 과정의 예측 가능성을 높이고 있습니다. 그 결과, 액체 충전 하드 캡슐 시장은 용해성 제한으로 인한 노출 문제를 해소하기 위한 파이프라인 내 제형 개선 과정에서 더 큰 시장 점유율을 확보할 전망입니다.

뉴트라슈티컬 시장의 성장이 모든 소비자층에서 캡슐 수요를 견인하고 있습니다.

소비자들은 삼키기 쉽고 흡수가 빠르다고 인식되는 1회 투여 제제를 계속해서 선호하고 있으며, 이로 인해 소매 채널에서 오일, 비타민, 효소, 프로바이오틱스 캡슐 제제에 대한 수요가 증가하고 있습니다. 액체 충전 하드 캡슐 시장에서는 각 브랜드가 퓨전 씰이나 강화된 산소 차단 기능을 활용하여 오메가-3, 코엔자임 Q10, 특정 식물 성분 등 산화에 민감한 유효 성분을 보호하는 동시에, 무단 개봉 방지 기능도 강화하고 있습니다. 프로바이오틱스 및 효소 제제의 경우, 서방형 설계가 적용된 HPMC 캡슐을 사용하고 있습니다. 이를 통해 민감한 성분이 위 환경을 통과하여 장 내에서 방출되므로, 코팅 공정을 추가하지 않고도 효능에 대한 설득력을 높일 수 있습니다.

제조업체들이 콜라겐이나 다성분 블렌드 등의 카테고리에서 용량을 확대해 나가는 가운데, 소매 제품 라인의 포장 및 형태를 결정할 때는 1회 분량과 섭취의 편의성이 여전히 중요한 요소로 남아 있습니다. 이러한 사용자 중심의 특성 덕분에, 액체 충전 하드 캡슐 시장은 맛의 마스킹, 안정성, 클린 라벨 인증 등이 중요한 차별화 요소로 작용하는 성장 기회를 포착하고 있습니다. 뉴트라슈티컬 제품 포트폴리오가 다양화되는 가운데, 캡슐 껍질, 밀봉, 충전 분야의 전문 지식을 통합한 공급업체는 새로운 개념을 상온 보관이 가능한 SKU로 신속하게 구현할 수 있는 입장에 있습니다.

특수한 라벨 가공은 비용과 공정의 복잡성을 증가시킵니다.

액체 충전 방식에서는 용기 및 밀봉 시스템의 무결성을 확보하기 위해 밴딩이나 퓨전 씰이 필요한 경우가 많으며, 이로 인해 기존의 하드 캡슐에 비해 설비 투자 및 운영상의 부담이 증가할 가능성이 있습니다. 액체 충전 하드 캡슐 시장에서 기밀성이 뛰어난 연속적인 이음매를 형성하는 퓨전 시스템은 뛰어난 보호 성능을 제공하지만, 전용 설비, 검증 절차 및 작업자의 숙련도가 필요하기 때문에 모든 제조 시설이 이를 갖추고 있는 것은 아닙니다. 생산 라인이 고도화됨에 따라, 기업은 중량, 밀봉 상태, 외관이 사양을 충족하는지 실시간으로 보장하고, 인라인 제어 및 검사 공정의 유효성 검증을 수행해야 합니다. 이로 인해 품질 관리 부담이 커지고, 소량 생산이나 빈번한 SKU 전환 시 기술 이관에 시간이 더 소요될 가능성이 있습니다. 뛰어난 위조 방지 기능이나 산화 방지 기능을 원하는 후원 기업은 보존 기간이나 품질 면에서 이점을 얻을 수 있지만, 그 복잡성이 증가함에 따라 가격 경쟁이 치열한 프로그램에서는 부담이 될 가능성이 있습니다. 이러한 상충 관계는 액체 충전 하드 캡슐 시장 전체의 시설 전략 및 아웃소싱 선택에 영향을 미치고 있습니다.

부문별 분석

2025년 기준으로, 젤라틴 캡슐은 액체 충전 하드 캡슐 시장의 73.24% 점유율을 차지했습니다. 이는 성숙한 가공 인프라와 일반적인 유성 및 현탁액 충전재의 용해 거동이 충분히 이해되고 있다는 점에 기반을 두고 있습니다. 이러한 기존 기반을 바탕으로, 가교 반응을 유발할 가능성이 있는 첨가제의 화학적 성분을 배제한 제제에서 젤라틴은 대량 생산 프로그램의 핵심적인 위치를 계속 차지하고 있습니다. 후원 기업들은 확립된 젤라틴 공급망과의 연계 및 번들링 작업 흐름에 대한 현장 수준의 경험을 활용함으로써, 효율적인 적합성 평가를 중시하고 있습니다. HPMC는 알데히드에 의한 가교 반응에 대한 고유한 내성, 쉘의 낮은 수분 함량, 그리고 서방형 또는 개량된 방출 설계에 대한 적합성 덕분에 계속해서 빠르게 성장하고 있습니다. 이 모든 요소가 제제 설계의 자유도를 높여주고 있습니다. 비유전자변형, 할랄, 비건 등의 인증 범위 또한 HPMC가 많은 소비자용 제품 포트폴리오의 핵심이 되는 표시가 부착된 제품 시장 기회를 개척하는 데 기여하고 있습니다. 액체 충전 하드 캡슐 시장에서는 젤라틴의 규모의 경제성과 HPMC의 기능적 측면 및 표시상의 이점 사이의 역학 관계가 2031년까지 캡슐 껍질 선정에 계속 영향을 미칠 것으로 보입니다.

HPMC는 안정성과 예측 가능한 방출을 유지하기 위해, 젤라틴에서 이동하는 수분에 민감한 API, 프로바이오틱스, 효소 및 용매를 함유한 충전제가 증가함에 따라 2031년까지 연평균 성장률(CAGR) 8.51%를 나타낼 것으로 전망됩니다. 공급업체들은 pH에 영향을 받지 않는 용해성과 모든 액체 충전 형태에서 일관된 성능을 실현하기 위해 열 겔화 공정 및 고분자 공학의 발전에 투자해 왔습니다. 액체 충전 하드 캡슐 업계에서 이러한 기술력을 바탕으로, 제제 개발자는 소비자용 유통 채널에서 중요한 표시 내용을 유지하면서도 서방형 특성과 지질계 운반체를 결합한 제품을 설계할 수 있게 됩니다. 젤라틴은 여전히 안정된 중성 pH의 오일이나 단순한 현탁액에는 적합하기 때문에 포트폴리오 고유의 기준이 주요 구매업체들의 하이브리드 조달 전략을 계속해서 주도하고 있습니다. 시간이 지남에 따라, 규제 대상 제품에서 HPMC에 대한 신뢰도가 높아지고 인증된 공급처가 확대됨에 따라, 식물 유래 캡슐 껍질 시장 점유율이 점차 확대될 가능성이 있습니다.

2025년 기준으로, 유성 액체 충전은 액체 충전 하드 캡슐 시장 규모의 45.32%를 차지하고 있으며, 이는 용해되기 쉬운 비타민, 오일, 호르몬 제품에서 이 방식이 수행하는 핵심적인 역할을 반영하고 있습니다. 제조업체들은 공정의 간편함, 안정적인 사용 범위, 그리고 젤라틴 및 HPMC 캡슐 껍질과의 폭넓은 호환성 덕분에 여전히 유성 캐리어를 선호하고 있습니다. 원료의약품(API)에 대해 강력한 용해성이 요구되는 경우, 프로그램은 환자 간 변동 폭을 줄이면서 높은 노출량을 실현하도록 설계된 유화 시스템으로 전환되고 있습니다. 이는 보관 기간 동안 성능을 유지하기 위해 캡슐 껍질, 밀봉, 충전 과정을 일체적으로 조정해야 하기 때문에 액체 충전 하드 캡슐 시장에서 가장 큰 제형 혁신이 이루어지고 있는 분야입니다. 이와 동시에, 장비 제조업체들은 엄격한 가공 조건이 요구되는 핫필 및 고점도 시스템을 위해 처리 능력, 인라인 제어 및 온도 관리 기능을 개선해 왔습니다.

자가유화형 SEDDS/SMEDDS 시장은 2031년까지 연평균 성장률(CAGR) 9.85%를 기록하며 성장할 것으로 전망됩니다. 이는 지질 마이크로에멀젼이 용해되기 어려운 API의 용해성과 노출을 개선한다는 동료 심사를 거친 증거에 의해 뒷받침됩니다. 나노미터에서 서브마이크론 범위의 액적 크기를 제어할 수 있는 능력 덕분에 표면적이 증가하여, 투여 상태가 변동하는 조건에서도 일관된 흡수를 촉진합니다. 현탁액 및 핫멜트 제제는 유효 성분의 지용성이 낮거나 반고체 매트릭스가 효과적인 경우에 뚜렷한 역할을 수행하지만, 침전 및 열 프로파일을 관리하기 위해서는 견고한 공정 제어가 더욱 중요합니다. 개발 파이프라인이 복잡한 전달 목표로 진화함에 따라, 액체 충전 하드 캡슐 시장에서는 방출 제어와 용해 전략을 통합할 수 있는 유화 시스템 시장 점유율이 더욱 확대될 것입니다.

지역별 분석

북미는 2025년 기준 액체 충전 하드 캡슐 시장의 34.56%를 차지하고 있으며, 이는 강력한 제약사 기반, 확립된 캡슐 제조 체계, 그리고 경구 제형에 대한 성숙한 규제 시스템에 힘입은 결과입니다. 미국의 cGMP 요건과 용기 및 밀봉 시스템의 무결성에 대한 기대는 액체 충전 프로그램의 품질 및 문서화 관행을 표준화하는 데 기여하고 있습니다. 산화 안정성 및 라벨 표시 측면에서 프리미엄급 치료제나 소비자 제품을 뒷받침하는 프로젝트에서 퓨전 씰 및 HPMC 쉘을 적용한 캡슐의 사용이 증가하고 있습니다. 해당 지역에 도입된 고처리량 생산 라인은 처방약(Rx)과 일반의약품(OTC) 모두의 대량 생산을 뒷받침하고 있으며, 신제품 출시 및 제형 개선을 위한 생산 능력의 기반이 되고 있습니다. 이러한 생태계 덕분에 북미는 예측 기간 내내 영향력 있는 구매자 및 생산자로서의 지위를 유지할 것으로 보입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.32%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 예상되며, 이는 강력한 제조 역량과 의약품 및 영양 보조 식품 파이프라인 모두에서 프리미엄 씰 및 쉘 옵션의 채택 확대가 반영된 결과입니다. 지역 공급업체와 세계 다국적 기업들은 현지 및 수출 수요에 더 높은 수준의 무결성을 갖춘 형태로 대응하기 위해 생산 능력과 기술 역량을 확대되고 있습니다. 각 후원사가 생산 현지화와 설비 업그레이드를 추진하는 가운데, 주요 거점에서는 인라인 제어 기능을 갖춘 고속 생산 라인이 점차 보편화되고 있습니다. HPMC의 채택은 채식주의자 및 할랄 인증에 대한 수요가 증가함에 따라 늘어나고 있으며, 주요 시장의 소매 및 처방약(Rx) 분야에서의 활용 사례를 뒷받침하고 있습니다. 품질, 속도, 그리고 폭넓은 인증을 모두 갖춘 이 조합이 액체 충전 하드 캡슐 시장에서 해당 지역의 뛰어난 실적을 뒷받침하고 있습니다.

유럽에서는 액체 충전, 퓨전 씰, 그리고 첨단 방출 설계에 대해 검증된 공정을 갖춘 제조업체를 우대하는 엄격한 품질 기준 하에서 꾸준한 성장이 나타나고 있습니다. 활동 내용에는 제약 및 소비자 건강 분야 고객 모두를 지원하는 포장 및 통합 서비스 분야의 생산 능력 확충이 포함됩니다. HPMC의 채택은 수분 관리가 필요한 이용 사례나, 채식주의자 및 할랄 인증 표시를 확대하는 이용 사례에서 꾸준한 추세를 보이고 있습니다. 문서화, 추출물 및 용출물 시험, 공정 내 관리에 대한 엄격한 기준을 바탕으로, 유럽의 제조업체들은 복잡한 액체 충전 요구 사항을 충족하는 운영 모델을 구축해 왔습니다. 이를 통해 해당 지역은 규제 시장에서 유리한 입지를 유지하면서, 액체 충전 하드 캡슐 시장의 전 세계 공급 수요에도 대응하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the liquid filled hard capsules market size is projected to be USD 1.9 billion in 2025, USD 1.99 billion in 2026, and reach USD 2.85 billion by 2031, growing at a CAGR of 7.45% from 2026 to 2031.

This report is Segmented by Shell Material (Gelatin, HPMC, Pullulan/Other Cellulose), Filling State (Oil-Based Liquids, Suspensions, Semi-solid/Hot-melt Fills, and More), Sealing Method (Banding, Lock-Only, and More), End Use (Rx Pharmaceuticals, OTC, and More), Release Profile (Immediate Release, Modified Release), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Liquid Filled Hard Capsules Market Trends and Insights

Bioavailability Push For Poorly Soluble APIs Drives Liquid-Fill Adoption

A large share of new small-molecule candidates presents low aqueous solubility, which steers development teams toward lipid-based liquid-fill strategies such as SEDDS and SMEDDS to increase dissolution and absorption in the gastrointestinal tract. These systems combine oils with surfactants and co-surfactants to spontaneously form fine emulsions on contact with intestinal fluids, which increases interfacial area and supports more predictable uptake. In the liquid filled hard capsules market, this approach aligns with the objective of reducing variability in drug exposure for BCS Class II and IV compounds, which can otherwise show erratic plasma profiles when delivered as conventional tablets.

Manufacturers pair these fills with shell selections that avoid cross-linking and moisture-driven degradation so that dissolution kinetics remain consistent during shelf life. Regulatory frameworks and compendial standards reinforce quality-by-design practices for liquid oral dosage forms, improving the predictability of development and scale-up paths for these capsule formats. As a result, the liquid filled hard capsules market is positioned to capture a larger share of pipeline reformulations that target solubility-limited exposure.

Nutraceutical Growth Propels Capsule Demand Across Consumer Segments

Consumers continue to prefer single-dose formats that are easy to swallow with perceived faster uptake, which has lifted capsule-based delivery for oils, vitamins, enzymes, and probiotics in retail channels. In the liquid filled hard capsules market, brands are leveraging fusion sealing and enhanced oxygen barriers to protect oxidation-sensitive actives like omega-3, CoQ10, and certain botanicals while also enhancing tamper-evidence. Probiotic and enzyme formulations are adopting HPMC shells with delayed-release designs so that sensitive ingredients survive gastric conditions before releasing in the intestine, which strengthens efficacy positioning without adding a coating operation.

As manufacturers expand dose ranges for categories like collagen or multi-ingredient blends, portion sizes and ease of regimen adherence remain central to packaging and format decisions in retail lines. These user-centric attributes are helping the liquid filled hard capsules market capture growth opportunities where taste masking, stability, and clean-label shell certifications are key differentiators. As nutraceutical portfolios diversify, suppliers with integrated shell, sealing, and fill expertise are positioned to translate new concepts into shelf-stable SKUs at speed.

Specialized Sealing Adds Cost And Process Complexity

Liquid-filled formats often require banding or fusion sealing as part of container-closure integrity, which adds steps that can raise capital and operating burdens compared to conventional hard capsules. In the liquid filled hard capsules market, fusion systems that create hermetic, continuous seams deliver premium protection, yet they call for dedicated equipment, validation, and operator skill that not all sites maintain. As lines become more advanced, firms must validate in-line controls and inspection steps that ensure weight, seal integrity, and appearance meet specifications in real time. This escalates the quality management footprint, which can lengthen tech transfers for smaller batches or frequent SKU changeovers. Sponsors that need premium tamper-evidence and oxidative protection gain shelf-life and quality benefits, but the added complexity may weigh on programs where price competition is tight. The trade-off shapes facility strategies and outsourcing choices across the liquid filled hard capsules market.

Other drivers and restraints analyzed in the detailed report include:

- Advances In Liquid Dosing And Sealing Accuracy

- HPMC Adoption For Moisture-Sensitive And Vegetarian Formulations

- Excipient-Shell Interactions Demand Extensive Validation Protocols

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gelatin capsules held 73.24% of the liquid filled hard capsules market share in 2025, supported by mature processing infrastructure and well-understood dissolution behavior across common oil and suspension fills. This installed base keeps gelatin central to high-volume programs where formulations avoid excipient chemistries that could drive cross-linking. Sponsors value streamlined qualification when working with established gelatin supply networks and site-level experience in banding workflows. HPMC continues to expand faster because of inherent resistance to aldehyde-driven cross-linking, lower shell moisture, and its suitability for delayed or modified-release designs, all of which increase formulation headroom. Certification footprints that include non-GMO, halal, and vegan claims also help HPMC unlock labeled product opportunities that are central to many consumer portfolios. Within the liquid filled hard capsules market, the dynamic between gelatin's scale economics and HPMC's functional and labeling advantages will continue to shape shell selection decisions through 2031.

HPMC is projected to post an 8.51% CAGR through 2031 as more moisture-sensitive APIs, probiotics, enzymes, and solvent-containing fills shift away from gelatin to maintain stability and predictable release. Suppliers have invested in thermogelation processes and polymer-engineering advances that deliver pH-independent dissolution and consistent performance across liquid-fill modalities. In the liquid filled hard capsules industry, this capability lets formulators design products that combine delayed-release features with lipid vehicles while maintaining label claims that matter in consumer-facing channels. Gelatin remains a strong fit for stable, neutral-pH oils and simpler suspensions, so portfolio-specific criteria continue to drive hybrid procurement strategies at large buyers. Over time, rising comfort with HPMC in regulated products and the expansion of certified supply may gradually rebalance shares in favor of plant-based shells.

Oil-based liquid fills accounted for 45.32% of the liquid filled hard capsules market size in 2025, reflecting their central role in vitamins, oils, and hormone products where solubilization is straightforward. Operators continue to favor oil vehicles for their process simplicity, stable handling windows, and broad compatibility with both gelatin and HPMC shells. Where APIs demand stronger solubilization, programs migrate toward engineered emulsifying systems that deliver higher exposure with tighter inter-patient variability. This is where the liquid filled hard capsules market is seeing the greatest formulation innovation, because shell, seal, and fill must be tuned together to preserve performance across shelf life. In parallel, equipment providers have improved throughput, in-line control, and temperature management for hot fills and viscous systems that need tight processing windows.

Self-emulsifying SEDDS/SMEDDS are projected to grow at a 9.85% CAGR through 2031, reinforced by peer-reviewed evidence that lipid microemulsions improve solubilization and exposure for difficult APIs. The ability to target droplet sizes in the nano to submicron range increases interfacial area, which helps drive consistent absorption even under variable fed-state conditions. Suspension and hot-melt applications maintain clear roles where actives have low oil solubility or benefit from semi-solid matrices, yet they rely more heavily on robust process controls to manage sedimentation and thermal profiles. As pipelines evolve toward complex delivery goals, the liquid filled hard capsules market will keep allocating greater share to emulsifying systems that can integrate release control with solubilization strategies.

Geography Analysis

North America held 34.56% of the liquid filled hard capsules market in 2025, supported by a strong base of pharmaceutical sponsors, established capsule manufacturing, and mature regulatory systems for oral dosage forms. U.S. cGMP requirements and container-closure integrity expectations have helped standardize quality and documentation practices for liquid-fill programs. Capsules with fusion sealing and HPMC shells are increasing in projects where oxidative stability and label claims support premium therapies and consumer products. The region's installed base of high-throughput lines supports large-volume runs across both Rx and OTC, which anchors capacity for launches and reformulations. This ecosystem positions North America to remain an influential buyer and producer through the forecast window.

Asia-Pacific is projected to be the fastest-growing region at a 9.32% CAGR through 2031, reflecting strong manufacturing capability and increasing adoption of premium sealing and shell options in both pharmaceutical and nutraceutical pipelines. Regional suppliers and global multinationals are expanding capacity and technology stacks to serve local and export demand with higher integrity formats. As sponsors localize production and upgrade equipment, high-speed lines with in-line controls are becoming more common in leading hubs. HPMC adoption is rising alongside demand for vegetarian and halal certification, which supports retail and Rx use cases across major markets. This combination of quality, speed, and certification breadth supports the region's outperformance in the liquid filled hard capsules market.

Europe shows steady growth under rigorous quality standards that favor producers with validated processes for liquid fills, fusion sealing, and advanced release designs. Activity includes capacity additions in packaging and integrated services that support both pharma and consumer health customers. HPMC uptake is strong in use cases that require moisture management or expand labeled claims for vegetarian and halal preferences. With a high bar for documentation, extractables and leachables testing, and in-process controls, European manufacturers have built operating models that align with complex liquid-fill demands. This keeps the region well positioned in regulated markets while also serving global supply needs in the liquid filled hard capsules market.

- ACG Worldwide

- Aenova Group

- Ascendia Pharmaceutical Solutions

- Catalent, Inc

- CapsCanada

- Farmacapsulas

- HealthCaps India Ltd

- I.M.A. Industria Macchine Automatiche S.p.A.

- Lonza Group

- MG2 s.r.l.

- Qualicaps

- Roxlor LLC

- SaintyCo

- SEJONG PHARMATECH

- Sirio Pharma

- Suheung (EMBO CAPS)

- Sunil HealthCare Limited

- Syntegon Technology

- Vantage Nutrition

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Bioavailability Push for Poorly Soluble APIs (Lipid-Based Fills, SEDDS/SMEDDS)

- 4.2.2 Nutraceutical Growth and Capsule Preference

- 4.2.3 Advances in Liquid Dosing and Sealing Accuracy

- 4.2.4 HPMC Adoption for Moisture-Sensitive and Vegetarian Formulations

- 4.2.5 High-Throughput Capsule Machinery Enabling LFHC Scale-Up

- 4.2.6 Banding/Fusion Sealing Enabling Tamper-Evidence and Premiumization

- 4.3 Market Restraints

- 4.3.1 Specialized Sealing Adds Cost and Process Complexity

- 4.3.2 Excipient-Shell Compatibility and Regulatory Validation Burdens

- 4.3.3 Gelatin Supply and Cultural Constraints Create Volatility

- 4.3.4 Oxygen/Moisture Ingress Risk Without Advanced Sealing/Packaging

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Shell Material

- 5.1.1 Gelatin

- 5.1.2 HPMC

- 5.1.3 Pullulan / Other Cellulose

- 5.2 By Filling State

- 5.2.1 Oil-based liquids

- 5.2.2 Suspensions

- 5.2.3 Semi-solid / Hot-melt fills

- 5.2.4 Self-emulsifying (SEDDS/SMEDDS)

- 5.3 By Sealing Method

- 5.3.1 Banding

- 5.3.2 Fusion sealing / LEMS microspray

- 5.3.3 Lock-only

- 5.4 By End Use

- 5.4.1 Rx Pharmaceuticals

- 5.4.2 OTC

- 5.4.3 Nutraceuticals / Dietary Supplements

- 5.5 By Release Profile

- 5.5.1 Immediate Release

- 5.5.2 Modified Release (Sustained / Enteric)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 ACG

- 6.3.2 Aenova Group

- 6.3.3 Ascendia Pharmaceutical Solutions

- 6.3.4 Catalent, Inc

- 6.3.5 CapsCanada

- 6.3.6 Farmacapsulas

- 6.3.7 HealthCaps India Ltd

- 6.3.8 I.M.A. Industria Macchine Automatiche S.p.A.

- 6.3.9 Lonza

- 6.3.10 MG2 s.r.l.

- 6.3.11 Qualicaps

- 6.3.12 Roxlor LLC

- 6.3.13 SaintyCo

- 6.3.14 SEJONG PHARMATECH

- 6.3.15 Sirio Pharma

- 6.3.16 Suheung (EMBO CAPS)

- 6.3.17 Sunil HealthCare Limited

- 6.3.18 Syntegon Technology GmbH

- 6.3.19 Vantage Nutrition

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment