|

시장보고서

상품코드

2063661

자율형 IT 운영 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Autonomous IT Operations - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

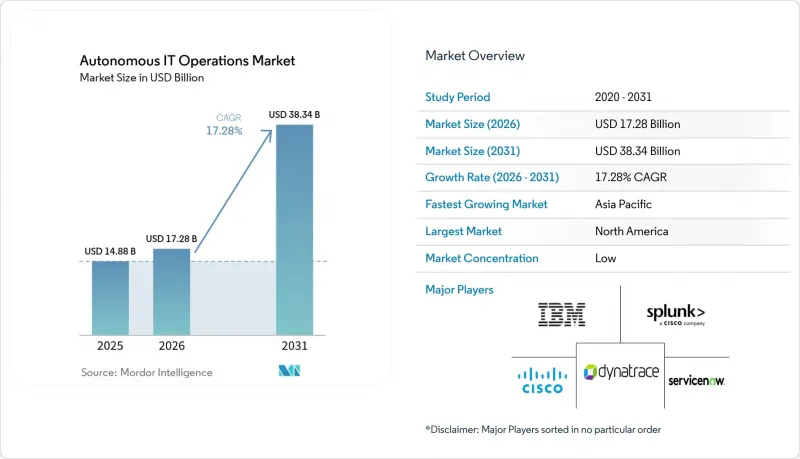

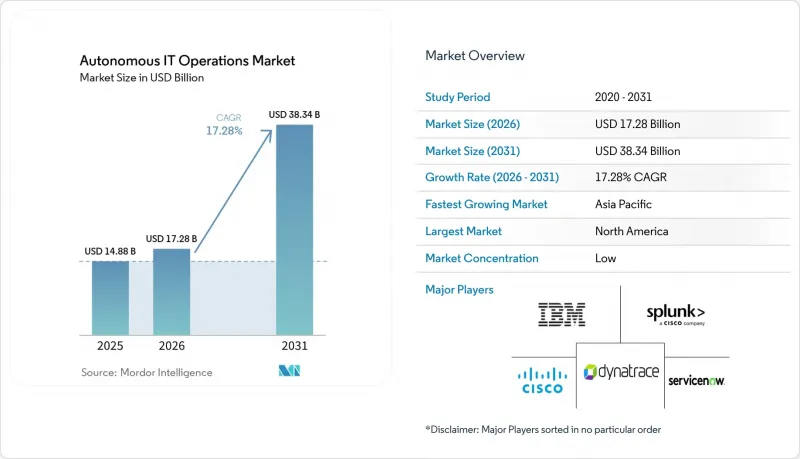

Mordor Intelligence에 의하면, 자율형 IT 운영 시장 규모는 2025년 148억 8,000만 달러에서 2026년에는 172억 8,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 17.28%로 성장을 지속하여, 2031년까지 383억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(플랫폼, 서비스(자문 서비스 등)), 도입 형태(On-Premise, 클라우드, 하이브리드), 조직 규모(대기업, 중소기업), 용도(용도 성능 관리 등), 업종(IT 및 통신, BFSI 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 자율형 IT 운영 시장 동향과 인사이트

IT 텔레메트리 데이터의 폭발적인 증가가 AI 상관 분석을 촉진

클라우드 네이티브 마이크로서비스는 트랜잭션당 수천 건의 이벤트를 생성하여, 기존의 규칙 기반 모니터링 시스템으로는 처리할 수 없는 페타바이트 규모의 가시성 파이프라인을 만들어내고 있습니다. 이러한 파이프라인은 방대한 양의 데이터를 생성하지만, 기존 방식으로는 이를 효과적으로 관리하거나 분석하기 어렵습니다. 이 과제를 해결하기 위해 AI 기반 상관관계 분석 엔진이 중요한 해결책으로 등장했습니다. 이 엔진은 이 압도적인 데이터 흐름을 몇 초 이내에 실용적인 근본 원인에 대한 인사이트로 압축할 수 있습니다. 이러한 첨단 플랫폼은 매일 수조 건의 종속성을 처리하도록 설계되어 있어, 문제를 신속하게 파악하고 해결할 수 있도록 보장합니다. 예를 들어, 소매업이나 전자상거래 사업자들은 계절적 판매 성수기 등 수요가 집중되는 기간에 발생할 수 있는 지연의 급증을 예측하고 이를 완화하기 위해 이러한 AI 기반 엔진을 점점 더 많이 활용하고 있습니다. 사후 대응형 알림에서 예측적 시정 조치로 전환함으로써, 기업은 업무 효율을 높이고 고객 경험을 개선하며, 중요한 상황에서도 원활한 서비스 제공을 유지할 수 있습니다.

하이브리드 및 멀티 클라우드 아키텍처 도입 확대

워크로드는 On-Premise 데이터센터, 퍼블릭 클라우드, 엣지 거점에 걸쳐 분포되어 있어, 수동 런북이나 기존의 모니터링 도구만으로는 효과적으로 메울 수 없는 심각한 가시성 격차가 발생하고 있습니다. 이러한 격차는 워크로드가 여러 플랫폼과 인프라에 걸쳐 실행되는 현대 IT 환경의 복잡성과 다양성에서 기인합니다. 자율형 IT 운영 플랫폼은 이기종 환경 전반에 걸쳐 텔레메트리 데이터를 통합함으로써 이러한 과제를 해결하며, 워크로드의 위치와 관계없이 원활하고 통일된 정책 적용을 가능하게 합니다. 이 기능을 통해 On-Premise, 클라우드, 엣지 등 어떤 환경에서든 일관된 관리와 규정 준수가 보장됩니다. 또한, 유럽 및 중동 등 지역에서의 소버린 클라우드 추진이 자율적인 엣지 운영 도입을 뒷받침하고 있습니다. 이러한 노력은 데이터 주권과 보안을 최우선으로 하며, 운영 효율성과 지역 규제 준수를 유지하면서 데이터 유출을 최소화하는 엣지 솔루션의 도입을 촉진하고 있습니다.

기존 IT 스택과의 통합에 따른 복잡성

메인프레임, 독점 데이터베이스 및 맞춤형 미들웨어에는 대개 최신 측정 기능이 탑재되어 있지 않기 때문에 기업은 모니터링 및 데이터 수집을 위해 추가 에이전트를 도입할 수밖에 없습니다. 그러나 이러한 에이전트는 지연 시간을 늘리고 유지보수 비용을 증가시켜 운영상의 비효율을 초래합니다. 레거시 시스템이 주류를 이루는 브라운필드 환경에서는 최신 솔루션의 도입 주기가 1년 이상 걸리기도 합니다. 이러한 지연은 호환성을 확보하기 위해 팀이 텔레메트리 커넥터 개조, 레거시 시스템 통합, 그리고 서로 다른 데이터 형식의 정규화 작업을 진행하는 과정에서 발생합니다. 하이브리드 디스커버리 엔진을 제공하는 벤더들은 이러한 과제에 대한 해결책을 제시하고 있습니다. 이러한 엔진은 SNMP 기반 장치와 Kubernetes 클러스터를 매핑할 수 있으며, 자산 탐색을 자동화하고 통합 시 수작업 부담을 줄임으로써 프로세스를 효율화합니다.

부문별 분석

2025년, 자율형 IT 운영 시장 점유율 중 73.12%를 플랫폼 부문이 차지했습니다. 이는 조직이 개별 도구를 통합하여 로그, 메트릭, 트레이스, 이벤트를 수집할 수 있는 통합 엔진으로 만들었기 때문입니다. 서비스 부문은 복잡한 도입 과정을 간소화하는 자문, 통합 및 관리형 운영 패키지에 힘입어 성장세를 이어가고 있습니다. 2026년부터 2031년까지, 기업들이 외부 전문 지식을 통해 보다 신속한 가치 실현(Time-to-Value)을 추구하는 가운데, 서비스 부문은 연평균 성장률(CAGR) 18.28%를 기록하며 플랫폼 부문을 앞지를 것으로 예측됩니다. 벤더들이 플랫폼 라이선스와 관리형 서비스를 세트로 판매하는 사례가 늘어나고 있으며, 이로 인해 조달 주기가 단축되고 사용량 급증도 완화되고 있습니다.

지속적인 최적화에 대한 수요가 증가함에 따라, 유지보수 계약은 공급업체가 계절적 트래픽 패턴을 바탕으로 상관 알고리즘을 재조정하는 선제적인 계약으로 변화하고 있습니다. 대형 인프라 제공업체가 기존 환경에 AIOps를 통합한 이후, 교차 판매 기회는 두 배로 증가했으며, 플랫폼의 유지율을 높이는 동시에 서비스 수익을 끌어올리고 있습니다. 미션 크리티컬한 워크로드를 중단하지 않고 현대화를 추진하려는 기존 설비를 보유한 제조업체나 공공기관에게 있어, 컨설턴트가 주도하는 텔레메트리 설계는 매우 중요해지고 있습니다.

2025년 시점에서 자율형 IT 운영 시장 점유율 대부분(52.24%)은 On-Premise 도입이 차지하고 있었습니다. 이는 의료 및 금융 서비스 업계의 엄격한 데이터 거주 요건과 규정 준수 요건 때문입니다. 이러한 업계에서는 기밀 데이터를 통제된 환경 내에 보관하고 엄격한 규제 체계를 준수하기 위해 On-Premise 솔루션을 우선적으로 채택하고 있습니다. 그러나 중소기업(SME)이 막대한 초기 투자가 필요 없는 구독형 모델을 점점 더 많이 도입함에 따라, 클라우드 도입은 2031년까지 연평균 성장률(CAGR) 17.88%로 확대될 것으로 전망됩니다. 이러한 변화를 통해 중소기업은 물리적 인프라 유지에 따른 재정적 부담 없이 고도의 IT 운영 기능을 활용할 수 있게 됩니다. 하이브리드 토폴로지가 선호되는 솔루션으로 부상함에 따라, 조직은 기밀성이 높은 상관 분석 워크로드를 On-Premise에 유지하면서, 버스트 분석에는 퍼블릭 클라우드 플랫폼의 확장성과 비용 효율성을 활용할 수 있게 됩니다.

엣지 컴퓨팅은 공장이나 소매점 등의 운영 환경에 경량 상관 분석 엔진을 통합함으로써, 이 생태계에 새로운 계층을 추가합니다. 이러한 환경에서는 실시간 의사 결정에 있어 밀리초 단위로 측정되는 초저지연이 필수적입니다. 최근 플랫폼 업데이트를 통해 핫 데이터를 즉시 액세스할 수 있도록 로컬에 저장하고, 웜 데이터는 비용 효율성을 높이기 위해 클라우드 오브젝트 스토어에 저장하는 계층형 스토리지 솔루션이 통합됨에 따라, 조직은 성능과 비용을 모두 최적화할 수 있게 되었습니다. 또한, ISO/IEC 27001과 같은 인증 프레임워크는 하이브리드 환경 전체를 포괄하도록 적용 범위를 확대하고 있으며, 기업이 On-Premise, 클라우드, 엣지 환경 전반에 걸쳐 통일된 보안 접근 방식을 채택하도록 뒷받침하고 있습니다. 이러한 종합적인 관점을 통해 조직은 하이브리드 및 엣지 컴퓨팅 솔루션의 유연성과 확장성을 활용하면서도 강력한 보안 기준을 유지할 수 있게 됩니다.

지역별 분석

2025년, 북미는 자율형 IT 운영 시장의 32.78%를 차지했습니다. 이는 해당 지역의 하이퍼스케일러 집중도가 높고, 탄탄한 DevOps 인재 풀에 힘입은 결과입니다. 미국은 선진적인 IT 인프라와 자동화 기술의 광범위한 도입을 통해 시장을 선도하고 있습니다. 한편, 캐나다의 디지털 전환에 대한 집중과 멕시코에서 업무 효율화를 위한 클라우드 플랫폼에 대한 의존도 증가는 해당 지역의 우위를 더욱 공고히 하고 있습니다. 그럼에도 불구하고, 아시아태평양은 연평균 성장률(CAGR) 19.21%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 중국, 인도 및 동남아시아 국가 등은 기존 시스템을 건너뛰고, 그린필드 방식의 클라우드 구축을 채택하고 있습니다. 중국에서는 엄격한 데이터 현지화 법에 따라 국내 벤더들이 주권형 클라우드를 위해 최적화된 솔루션을 개발해야 하는 상황에 놓여 있습니다. 한편, 인도의 주요 IT 서비스 기업들은 운영 효율성을 높이기 위해 AIOps를 관리형 서비스 포트폴리오에 통합하고 있습니다.

유럽의 자율형 IT 운영 시장은 GDPR(EU 개인정보보호규정) 및 EU AI법과 같은 엄격한 규제 체제에 힘입어 견조한 성장세를 보이고 있습니다. 이러한 규제로 인해 공급업체는 모델의 계보 및 투명성과 같은 기능을 도입해야 하며, 이를 통해 규정 준수를 확보하고 기업 간 신뢰를 구축하고 있습니다. 중동에서는 스마트 시티 플랫폼에 막대한 투자가 이루어지고 있으며, 엄격한 서비스 수준 목표를 유지하기 위해 자율형 IT 운영에 크게 의존하고 있습니다. 마찬가지로, 남미에서는 통신 네트워크의 현대화가 진행되고 있으며, 5G 네트워크 슬라이싱의 복잡성을 관리하기 위해 AIOps가 도입되고 있습니다. 이러한 발전 덕분에 해당 지역에서는 네트워크 효율을 높이고 운영 비용을 절감할 수 있게 되었습니다.

아프리카는 자율형 IT 운영의 도입이 아직 초기 단계에 있지만, 큰 성장 잠재력을 지니고 있습니다. 이 지역의 이동통신 사업자들은 외딴 지역이나 서비스가 미치지 않는 지역에 걸쳐 있는 방대한 기지국 네트워크의 자동화를 추진하며, 현장 직원에 대한 의존도를 최소화하려고 하고 있습니다. 이러한 자동화로 인해 운영상의 과제가 해결되고, 해당 지역에서의 서비스 제공이 개선될 것으로 기대됩니다. 자율형 IT 운영 분야에 대한 수요가 지속적으로 증가하는 가운데, 아프리카 등 일부 지역은 시장의 향후 성장에 있어 더욱 중요한 역할을 하게 될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the autonomous IT operations market size is expected to grow from USD 14.88 billion in 2025 to USD 17.28 billion in 2026 and is forecast to reach USD 38.34 billion by 2031 at 17.28% CAGR over 2026-2031.

This report is Segmented by Component (Platform, and Services (Advisory Services, and More)), Deployment Mode (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Application Performance Management, and More), Industry Vertical (IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Autonomous IT Operations Market Trends and Insights

Explosion of IT Telemetry Volumes Driving AI Correlation

Cloud-native microservices generate thousands of events per transaction, creating petabyte-scale observability pipelines that overwhelm traditional rules-based monitoring systems. These pipelines produce an immense volume of data that is challenging to manage and analyze effectively using conventional methods. To address this, AI-driven correlation engines have emerged as a critical solution, capable of condensing this overwhelming data torrent into actionable root-cause insights within seconds. These advanced platforms are designed to process trillions of dependencies daily, ensuring rapid identification and resolution of issues. For instance, retail and e-commerce operators increasingly rely on these AI-powered engines to anticipate and mitigate latency spikes during high-demand periods, such as seasonal sales peaks. By transitioning from reactive alerting to predictive remediation, businesses can enhance operational efficiency, improve customer experiences, and maintain seamless service delivery during critical times.

Rising Adoption of Hybrid and Multi-Cloud Architectures

Workloads span on-premise data centers, public clouds, and edge locations, creating significant visibility gaps that manual runbooks and traditional monitoring tools cannot effectively bridge. These gaps arise from the complexity and diversity of modern IT environments, where workloads run across multiple platforms and infrastructures. Autonomous IT operations platforms address this challenge by federating telemetry across heterogeneous estates, enabling seamless, unified policy enforcement regardless of workload location. This capability ensures consistent management and compliance across all environments, whether on-premise, in the cloud, or at the edge. Additionally, sovereign-cloud initiatives in regions such as Europe and the Middle East are driving the adoption of autonomous edge operations. These initiatives prioritize data sovereignty and security, encouraging the implementation of edge solutions that minimize data egress while maintaining operational efficiency and compliance with regional regulations.

Integration Complexity with Legacy IT Stacks

Mainframes, proprietary databases, and custom middleware often lack modern instrumentation, which forces enterprises to deploy additional agents to enable monitoring and data collection. These agents, however, increase latency and add to maintenance costs, creating operational inefficiencies. In brownfield environments, where legacy systems dominate, adoption cycles for modern solutions can extend beyond a year. This delay occurs as teams work to retrofit telemetry connectors, integrate legacy systems, and normalize disparate data formats to ensure compatibility. Vendors offering hybrid discovery engines provide a solution to these challenges. These engines can map SNMP-based devices alongside Kubernetes clusters, streamlining the process by automating asset discovery and reducing manual effort during integration.

Other drivers and restraints analyzed in the detailed report include:

- Need to Reduce Mean Time to Resolution and Downtime Costs

- Generative AI Copilots Improving AIOps Usability

- Shortage of AIOps-Skilled Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The platform segment accounted for 73.12% of the autonomous IT operations market share in 2025, as organizations consolidated point tools into unified engines capable of ingesting logs, metrics, traces, and events. The services segment is gaining momentum, driven by advisory, integration, and managed-operations packages that simplify complex deployments. During 2026-2031, services are projected to outpace platforms at 18.28% CAGR as enterprises seek faster time-to-value through external expertise. Vendors increasingly bundle platform licenses with managed services, shortening procurement cycles and smoothing consumption spikes.

The growing demand for continuous optimization is reshaping maintenance contracts into proactive engagements in which vendors retune correlation algorithms based on seasonal traffic patterns. Cross-selling opportunities have multiplied since large infrastructure providers integrated AIOps into existing estates, reinforcing platform stickiness while boosting services revenue. Consultant-led telemetry design has become pivotal for brownfield manufacturers and public agencies looking to modernize without disrupting mission-critical workloads.

On-premises installations accounted for the majority of the autonomous IT operations market share, at 52.24%, in 2025, due to strict data-residency and compliance requirements in healthcare and financial services. These industries prioritize on-premises solutions to ensure sensitive data remains within controlled environments and to adhere to stringent regulatory frameworks. Cloud deployments, however, are forecast to expand at a compound annual growth rate (CAGR) of 17.88% through 2031, as small and medium-sized enterprises (SMEs) increasingly adopt subscription-based models that eliminate the need for significant upfront capital expenditure. This shift allows SMEs to access advanced IT operations capabilities without the financial burden of maintaining physical infrastructure. Hybrid topologies are emerging as a preferred solution, enabling organizations to keep sensitive correlation workloads on-premises while leveraging the scalability and cost-efficiency of public cloud platforms for burst analytics.

Edge computing introduces an additional layer to this ecosystem by embedding lightweight correlation engines within operational environments such as factories and retail stores, where ultra-low latency, often measured in milliseconds, is critical for real-time decision-making. Recent platform updates that incorporate tiered storage solutions, storing hot data locally for immediate access and warm data in cloud object stores for cost efficiency, are helping organizations optimize both performance and expenses. Furthermore, certification frameworks like ISO/IEC 27001 are increasingly expanding their coverage to encompass entire hybrid estates, encouraging businesses to adopt a unified security approach across on-premises, cloud, and edge environments. This holistic view ensures that organizations can maintain robust security standards while benefiting from the flexibility and scalability of hybrid and edge computing solutions.

Geography Analysis

North America accounted for 32.78% of the autonomous IT operations market share in 2025, driven by the region's high concentration of hyperscalers and a robust DevOps talent pool. The United States leads the market with its advanced IT infrastructure and widespread adoption of automation technologies. Meanwhile, Canada's focus on digital transformation and Mexico's growing reliance on cloud platforms for operational efficiency further bolsters the region's dominance. Despite this, the Asia-Pacific region is expected to be the fastest-growing region, with a projected CAGR of 19.21%. Countries like China, India, and those in Southeast Asia are bypassing legacy systems and adopting greenfield cloud builds. In China, stringent data-localization laws are pushing domestic vendors to develop solutions optimized for sovereign clouds, while India's IT services giants are integrating AIOps into their managed services portfolios to enhance operational efficiency.

Europe's growth in the autonomous IT operations market remains steady, supported by strict regulatory frameworks such as GDPR and the EU AI Act. These regulations require vendors to incorporate features such as model lineage and transparency, thereby ensuring compliance and fostering trust among enterprises. The Middle East is making significant investments in smart-city platforms, which rely heavily on autonomous IT operations to maintain stringent service-level objectives. Similarly, South America is witnessing modernization in its telecom networks, with AIOps being adopted to manage the complexities of 5G network slicing. These advancements are enabling the region to improve network efficiency and reduce operational costs.

Africa, while still in the early stages of adopting autonomous IT operations, has considerable growth potential. The region's mobile operators are increasingly automating their extensive tower estates, which often span remote and underserved areas, to minimize the need for on-site staff. This shift toward automation is expected to address operational challenges and improve service delivery in the region. As global demand for autonomous IT operations continues to rise, regionssuch ase Africa are likely to play a more significant role in the market's future growth.

- International Business Machines Corporation

- Dynatrace, Inc.

- Splunk Inc.

- Cisco Systems, Inc.

- Datadog, Inc.

- Broadcom Inc.

- ServiceNow, Inc.

- BMC Software, Inc.

- Micro Focus International plc

- Elastic N.V.

- ScienceLogic, Inc.

- Moogsoft, Inc.

- BigPanda, Inc.

- LogicMonitor, Inc.

- SolarWinds Corporation

- New Relic, Inc.

- PagerDuty, Inc.

- Aisera, Inc.

- Resolve Systems, LLC

- OpsRamp, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of IT Telemetry Volumes Driving AI Correlation

- 4.2.2 Rising Adoption of Hybrid and Multi-Cloud Architectures

- 4.2.3 Need to Reduce Mean Time to Resolution and Downtime Costs

- 4.2.4 Generative AI Copilots Improving AIOps Usability

- 4.2.5 Data-Sovereignty Rules Fueling Autonomous Edge Operations

- 4.2.6 ESG-Linked Green Ops Mandates for Energy Optimisation

- 4.3 Market Restraints

- 4.3.1 Integration Complexity with Legacy IT Stacks

- 4.3.2 Shortage of AIOps-Skilled Professionals

- 4.3.3 AI Model Auditability under Emerging Regulations

- 4.3.4 Vendor Lock-In from Proprietary Correlation Engines

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.1.2.1 Advisory Services

- 5.1.2.2 Integration and Implementation Services

- 5.1.2.3 Support and Maintenance Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Application Performance Management

- 5.4.2 Infrastructure Management

- 5.4.3 Network and Security Management

- 5.4.4 Real-Time Analytics and Event Correlation

- 5.4.5 IT Service Management Automation

- 5.5 By Industry Vertical

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Retail and eCommerce

- 5.5.5 Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other Industry Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 International Business Machines Corporation

- 6.4.2 Dynatrace, Inc.

- 6.4.3 Splunk Inc.

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Datadog, Inc.

- 6.4.6 Broadcom Inc.

- 6.4.7 ServiceNow, Inc.

- 6.4.8 BMC Software, Inc.

- 6.4.9 Micro Focus International plc

- 6.4.10 Elastic N.V.

- 6.4.11 ScienceLogic, Inc.

- 6.4.12 Moogsoft, Inc.

- 6.4.13 BigPanda, Inc.

- 6.4.14 LogicMonitor, Inc.

- 6.4.15 SolarWinds Corporation

- 6.4.16 New Relic, Inc.

- 6.4.17 PagerDuty, Inc.

- 6.4.18 Aisera, Inc.

- 6.4.19 Resolve Systems, LLC

- 6.4.20 OpsRamp, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment