|

시장보고서

상품코드

2063663

구성 관리 데이터베이스(CMDB) 및 IT 디스커버리 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Configuration Management Database (CMDB) And IT Discovery Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

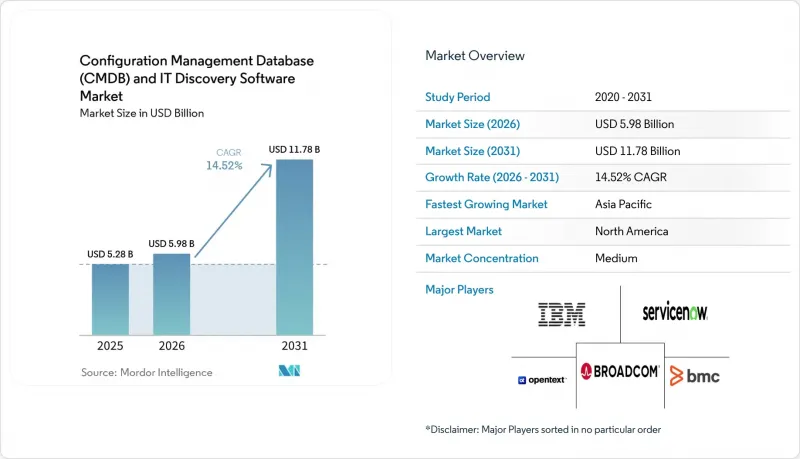

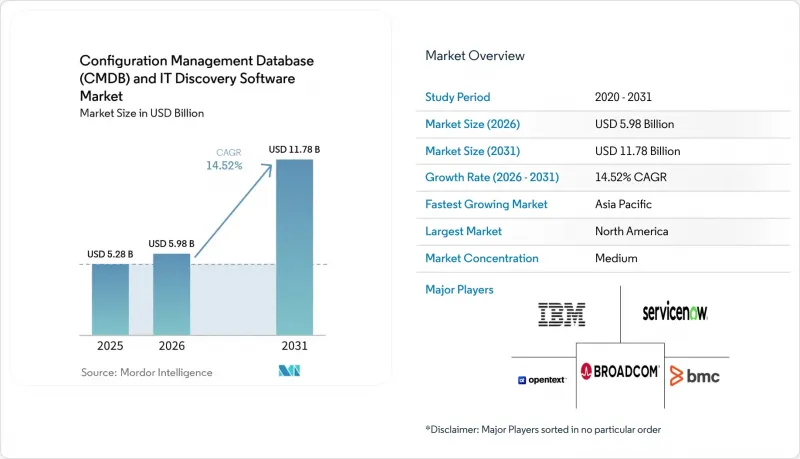

Mordor Intelligence에 의하면, 구성 관리 데이터베이스(CMDB) 및 IT 디스커버리 소프트웨어 시장 규모는 2025년에 52억 8,000만 달러로 평가되었습니다. 2026년에 59억 8,000만 달러에서 2031년까지 117억 8,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 14.52%를 나타낼 것으로 전망됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 방식(On-Premise, 클라우드, 하이브리드), 조직 규모(대기업, 중소기업), 용도(IT 운영, 보안 및 규정 준수 등), 산업 분야(BFSI 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 구성 관리 데이터베이스(CMDB) 및 IT 디스커버리 소프트웨어 시장 동향 및 인사이트

에이전트 없는 클라우드 디스커버리 솔루션으로의 전환이 가속화되고 있습니다.

에이전트리스 디스커버리는 수천 개의 엔드포인트, 특히 수명이 짧은 클라우드 인스턴스에서 소프트웨어를 배포하고, 패치를 적용하며, 보안 조치를 수행하는 데 따르는 부하를 피할 수 있기 때문에 에이전트 기반 스캔을 점차 대체하고 있습니다. ServiceNow의 Yokohama 릴리스는 AWS, Microsoft Azure 및 Google Cloud의 API에서 직접 구성 메타데이터를 가져와, 검색 지연 시간을 몇 시간에서 몇 분으로 단축합니다. 보안 팀은 읽기 전용 자격 증명을 사용하여 프로덕션 시스템의 권한을 최소화하는 에이전트 없는 방식을 선호합니다. IBM이 Confluent의 Apache Kafka 이벤트 스트림을 통합함에 따라, 구성 관리 데이터베이스(CMDB) 및 IT 디스커버리 소프트웨어 시장 플랫폼은 배치 스캔을 기다릴 필요 없이 실시간 구성 이벤트를 수집할 수 있게 됩니다. 멀티 클라우드 전략이 보편화됨에 따라, 클라우드별 에이전트 없이도 서로 다른 환경에 분산된 자산을 상호 연관시킬 수 있는 능력은 이제 필수 불가결한 요소가 되었습니다.

AI를 활용한 종속 관계 매핑과 예측 분석의 통합

머신러닝 모델은 네트워크 흐름, 로그 텔레메트리, 인시던트 이력을 분석하여 구성 요소 간의 관계를 추론함으로써, 수동으로 수행하던 토폴로지 유지 관리를 대폭 줄여줍니다. BMC Helix 25.2에서는 HelixGPT Insight Finder와 Post Mortem Analyzer가 추가되었습니다. 이 기능들은 CMDB 데이터를 활용하여 서비스 상태의 이상을 감지하고, 토폴로지 업데이트를 권장합니다. ServiceNow의 Now Assist는 데이터 입력 시 속성을 제안함으로써 데이터 품질을 향상시킵니다. ENISA는 NIS2의 적용 대상 사업자에게 있어 자동화된 의존성 매핑이 필수적이라고 강조하고 있습니다. 알고리즘이 성숙해짐에 따라, CMDB의 영향 분석은 정적 테이블에서 연쇄적인 장애 위험을 정량화하는 확률적 그래프로 전환되고 있습니다.

기업 규모 도입에 따른 높은 비용과 복잡성

통합 미들웨어, 데이터 정제 및 직원 교육 비용을 고려할 때, 전 세계 CMDB 도입 프로젝트에서는 예산을 최대 100%까지 초과하는 것이 일상화되어 있습니다. 포춘 500대 기업의 프로젝트에서는 3년 동안 1,000만 미달러를 초과하는 경우도 있어, 중견 기업의 구매자에게는 충격적인 금액이 됩니다. 업계 고유의 자산에 맞추어 ServiceNow의 데이터 모델을 맞춤 설정하거나, 여러 디스커버리 도구에서 중복되는 항목을 조정하거나, 합병 후 CMDB를 통합하는 작업은 도입 기간을 수년이나 연장시킬 가능성이 있습니다. ISO 20000은 개요 수준의 지침만을 제공하기 때문에 기업은 독자적인 청사진을 수립할 수밖에 없으며, 그 결과 비용과 위험이 증가합니다.

부문별 분석

서비스 매출은 연평균 14.92%라는 견실한 성장률을 기록하며 확대되고 있으며, 이는 구성 관리 데이터베이스(CMDB) 및 IT 디스커버리 소프트웨어 시장 전체의 성장률을 상회하고 있습니다. 이러한 성장은 레거시 데이터를 표준화된 스키마에 매핑하고, 중복 레코드를 조정하며, 복잡한 하이브리드 클라우드 환경 전반에 걸쳐 디스커버리 피드를 통합하는 등 중요한 요구 사항을 해결하기 위해 조직들이 컨설팅 회사에 점점 더 의존하고 있기 때문입니다. 소프트웨어 라이선스, 인프라, 지속적인 관리를 결합한 관리형 CMDB-as-a-Service(MaaS) 서비스는 종합적인 솔루션을 필요로 하지만 자원이 제한적인 구매자들 사이에서 지지를 얻고 있습니다. 2025년 매출 중 소프트웨어가 71.45%를 차지했지만, 지속적인 서비스에 대한 의존도가 높아지고 있는 점이 플랫폼 업데이트 결정에 영향을 미치는 중요한 요인이 되고 있으며, 이는 벤더 락인 전략을 더욱 공고히 하고 있습니다.

또한, 전문 서비스 부문은 통합에 대한 수요 증가를 활용하여 부가가치가 더 높은 솔루션을 제공합니다. 예를 들어, BMC Helix의 에이전트 기반 AI는 인시던트 레코드에서 직접 Microsoft Teams의 Swarm 세션을 시작하고, CMDB(구성 관리 데이터베이스)의 컨텍스트를 협업 워크플로에 원활하게 통합합니다. 이 기능을 통해 운영 효율이 향상되고, 사고 해결 시간이 단축됩니다. 또한, 각 벤더사는 CMDB의 정확도 지표와 직접 연동되는 성과 기반 가격 모델 등 혁신적인 가격 전략을 채택하고 있습니다. 이러한 모델은 성과 위험을 제공업체 측으로 이전함으로써, 제공업체가 더 높은 품질의 서비스를 제공하도록 동기를 부여하는 동시에, 경쟁이 치열해지는 시장 상황에서 차별화를 꾀할 수 있게 해줍니다. 가격 책정을 측정 가능한 성과와 연계함으로써, 공급업체는 고객의 위험을 줄일 뿐만 아니라 시장에서 자사의 가치 제안을 강화하는 데에도 기여하게 됩니다.

2025년에는 구성 관리 데이터베이스(CMDB) 및 IT 디스커버리 소프트웨어 시장 점유율 중 클라우드 도입이 46.83%를 차지했으며, 2031년까지 15.12%의 성장률이 예상됩니다. 이러한 도입은 전환이나 인수합병(M&A)으로 인한 수요 급증 시기 등 수요가 높아지는 기간에 유연하게 확장할 수 있다는 점에서 점점 더 선호되고 있으며, 동시에 조직의 시스템에 대한 패치 적용 및 업그레이드 부담을 줄여주고 있습니다. 하이브리드 도입 모델은 기밀 데이터를 On-Premise 저장소에 남겨두면서도 퍼블릭 워크로드를 위해 클라우드의 검색 기능을 활용할 수 있기 때문에 규제 대상 기업들 사이에서 지지를 얻고 있습니다. 그러나 On-Premise 도입은 국방 및 정보 기관 등의 분야에서는 여전히 일반적이지만, 클라우드 기반 솔루션에 비해 시장 점유율을 서서히 잃어가고 있습니다.

ServiceNow의 FedRAMP High 인증 및 Autonomous Workforce 솔루션 도입은 연방 정부 부문에서 안전한 SaaS CMDB에 대한 수요가 증가하고 있음을 여실히 보여주고 있습니다. 마찬가지로, 유럽 사이버보안 기관(ENISA)은 보안 조치가 마련된 클라우드 처리에 관한 지침을 발표했으며, 이는 유럽 전역에서 하이브리드 클라우드 모델의 도입을 촉진하고 있습니다. 현재 구매자들은 AWS, Azure, Google Cloud, PrivateStack 등의 플랫폼 간에 원활하게 통합되는 멀티클라우드 감지 기능을 기대하고 있습니다. 조직이 IT 생태계에서 유연성과 상호운용성을 우선시함에 따라, 이러한 기대감으로 인해 벤더 종속성에 대한 용인 수준은 낮아지고 있습니다.

지역별 분석

북미는 ITIL의 조기 도입, 엄격한 규제 요건, 그리고 해당 지역공급업체 집중도가 높은 점 등으로 인해 2025년 매출의 38.23%를 차지했습니다. 미국에서는 은행들이 연방준비제도이사회가 규정한 종합적인 자산 목록 관리 의무를 준수하기 위해 CMDB 솔루션 도입을 가속화하고 있습니다. 한편, 캐나다 공공 부문에서는 디지털 정부 플랫폼의 보안과 효율성을 높이기 위해 자산 관리 시스템의 업그레이드를 적극적으로 추진하고 있습니다. 멕시코에서는 수출에 주력하는 제조업체들이 국제 무역 기준을 준수하고 업무 효율성을 확보하기 위해, 운영 기술 자산을 효과적으로 관리·감시하는 수단으로 CMDB를 활용하는 사례가 증가하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 15.36%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 인도에서는 디지털 정부 추진의 일환으로 부처 간 자산 가시화가 의무화되어 있으며, 일본에서는 CMDB 데이터와 산업용 IoT 분석을 결합하여 플랜트의 가동률을 최적화하고 있습니다. 중국은 자국이 주도하는 기술 스택을 중시하고 있으며, 데이터 현지화 규정을 준수하는 국내 CMDB 솔루션의 제공을 촉진하고 있습니다. 모바일 우선 방식을 채택한 한국의 노동력은 현장 기술자에게 최적화된 CMDB 인터페이스를 원하고 있습니다. 지역적 다양성이 클라우드의 확장성과 데이터 보관 요건 준수를 조화시키는 하이브리드 아키텍처의 도입을 촉진하고 있습니다.

DORA와 NIS2가 유럽 시장을 형성하고 있습니다. 은행 및 중요 인프라 사업자는 실시간 자산 목록과 의존 관계 지도를 유지해야 하며, 이것이 불변의 감사 추적을 필요로 하는 요인으로 작용하고 있습니다. 영국, 독일, 프랑스는 성숙한 제조업 및 금융 부문의 뒷받침을 받아 도입을 주도하고 있습니다. 남미, 중동 및 아프리카는 여전히 개발도상국이지만, 브라질이 은행의 사이버 보안 규제를 강화하고, 걸프 국가들이 자동 감지에 의존하는 스마트 시티 인프라를 구축함에 따라 그 성장세는 가속화되고 있습니다. 이러한 지역이 성숙해짐에 따라, 구성 관리 데이터베이스(CMDB) 및 IT 디스커버리 소프트웨어 시장에서는 규제의 미묘한 차이에 대응하기 위한 지역 밀착형 파트너십이 부상할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the configuration management database (CMDB) and IT Discovery Software market size is projected to be USD 5.28 billion in 2025, USD 5.98 billion in 2026, and reach USD 11.78 billion by 2031, growing at a CAGR of 14.52% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises), Application (IT Operations, Security and Compliance, and More), Industry Vertical (BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Configuration Management Database (CMDB) And IT Discovery Software Market Trends and Insights

Accelerating Shift to Agentless Cloud Discovery Solutions

Agentless discovery is displacing agent-based scanning because it bypasses the overhead of deploying, patching, and securing software on thousands of endpoints, especially short-lived cloud instances. ServiceNow's Yokohama release harvests configuration metadata directly from AWS, Microsoft Azure, and Google Cloud APIs, shrinking discovery latency from hours to minutes. Security teams favor agentless methods that use read-only credentials, minimizing production-system privileges. IBM's integration of Confluent's Apache Kafka event streams enables Configuration Management Database (CMDB) and IT Discovery Software market platforms to ingest real-time configuration events rather than waiting for batch scans. As multi-cloud strategies proliferate, the ability to correlate assets across heterogeneous environments without per-cloud agents is becoming non-negotiable.

Integration of AI-Powered Dependency Mapping and Predictive Analytics

Machine-learning models now infer relationships among configuration items by analyzing network flow, log telemetry, and incident histories, sharply reducing manual topology maintenance. BMC Helix 25.2 added HelixGPT Insight Finder and Post Mortem Analyzer, which consume CMDB data to surface service-health anomalies and recommend topology updates. ServiceNow's Now Assist suggests attributes during data entry, improving data quality. ENISA highlights automated dependency mapping as critical for NIS2-covered operators. As algorithms mature, CMDB impact analysis is transitioning from static tables to probabilistic graphs that quantify cascading-failure risk.

High Cost and Complexity of Enterprise-Scale Implementations

Global CMDB rollouts routinely exceed budgets by up to 100% once integration middleware, data cleansing, and staff training are factored in. Fortune 500 programs can surpass USD 10 million over three years, creating sticker shock for mid-market buyers. Customizing ServiceNow's data model for sector-specific assets, reconciling duplicate items from multiple discovery tools, and federating CMDBs after mergers can extend timelines by years. ISO 20000 provides only high-level guidance, forcing enterprises to develop bespoke blueprints that increase costs and risks.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for Real-Time Configuration Audit Trails

- Convergence of ITAM, FinOps and ESG Reporting Requirements

- Persistent Data Quality and Normalization Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is expanding at a robust 14.92% annual growth rate, outpacing the overall Configuration Management Database (CMDB) and IT Discovery Software markets. This growth is driven by organizations increasingly relying on consultancies to address critical needs such as mapping legacy data to standardized schemas, reconciling duplicate records, and integrating discovery feeds across complex hybrid cloud environments. Managed CMDB-as-a-service offerings, which combine software licenses, infrastructure, and ongoing stewardship, are gaining traction among resource-constrained buyers who seek comprehensive solutions. While software still accounted for 71.45% of the projected 2025 income, the growing reliance on recurring services is now a key factor influencing platform renewal decisions, further solidifying vendor lock-in strategies.

Additionally, professional services are leveraging the increasing demand for integrations to deliver more value-added solutions. For instance, BMC Helix's agentic AI initiates Microsoft Teams swarming sessions directly from incident records, seamlessly embedding CMDB (Configuration Management Database) context into collaboration workflows. This capability enhances operational efficiency and improves incident resolution times. Furthermore, vendors are adopting innovative pricing strategies, such as outcome-based pricing models tied directly to CMDB accuracy metrics. These models transfer performance risks to the providers, incentivizing them to deliver higher-quality services while simultaneously enabling them to stand out in an increasingly competitive market landscape. By aligning pricing with measurable outcomes, vendors not only mitigate risks for their clients but also reinforce their value proposition in the market.

Cloud implementations accounted for 46.83% of the Configuration Management Database (CMDB) and IT Discovery Software market share in 2025, with projections indicating a 15.12% growth rate through 2031. These implementations are increasingly preferred for their ability to scale elastically during periods of high demand, such as during migrations or mergers and acquisitions (M&A) surges, while also relieving organizations of the burden of patching and upgrading systems. Hybrid deployment models are gaining traction among regulated entities, as they allow sensitive data to remain in on-premises repositories while leveraging cloud discovery capabilities for public workloads. However, on-premises installations, while still prevalent in sectors like defense and intelligence, are gradually losing market share in comparison to cloud-based solutions.

ServiceNow's FedRAMP High authorization and the introduction of its Autonomous Workforce solution highlight the growing demand for secure SaaS CMDBs within the federal sector. Similarly, the European Union Agency for Cybersecurity (ENISA) has issued guidance on cloud processing with safeguards, which is driving the adoption of hybrid cloud models across Europe. Buyers now expect multi-cloud discovery capabilities that seamlessly integrate across platforms such as AWS, Azure, Google Cloud, and private stacks. This expectation is reducing tolerance for vendor lock-in, as organizations prioritize flexibility and interoperability in their IT ecosystems.

Geography Analysis

North America captured 38.23% of 2025 revenue due to early ITIL adoption, stringent regulatory requirements, and a high concentration of vendors in the region. In the United States, banks are expediting the implementation of CMDB solutions to comply with Federal Reserve mandates for maintaining comprehensive asset inventories. Meanwhile, Canada's public sector is actively upgrading its asset management systems to enhance the security and efficiency of its digital government platforms. In Mexico, manufacturers focused on exports are increasingly leveraging CMDBs to manage and monitor their operational technology estates effectively, ensuring compliance with international trade standards and operational efficiency.

Asia-Pacific is the fastest-growing region, with a 15.36% CAGR. India's digital-government push mandates asset visibility across ministries, while Japan couples CMDB data with industrial IoT analytics to optimize plant uptime. China emphasizes sovereign technology stacks, spurring domestic CMDB offerings that comply with data-localization rules. South Korea's mobile-first workforce demands CMDB interfaces optimized for field technicians. Regional diversity drives uptake of hybrid architectures that balance cloud scale with residency compliance.

DORA and NIS2 shape Europe's market. Banks and critical infrastructure operators must maintain real-time inventories and dependency maps, which are driving demand for immutable audit trails. The United Kingdom, Germany, and France lead adoption, supported by mature manufacturing and finance sectors. South America, the Middle East, and Africa remain nascent but accelerating as Brazil tightens bank cybersecurity rules and Gulf nations deploy smart-city infrastructure that relies on automated discovery. As these regions mature, the Configuration Management Database (CMDB) and IT Discovery Software market will see localized partnerships emerge to navigate regulatory nuance.

- ServiceNow, Inc.

- BMC Software, Inc.

- International Business Machines Corporation

- OpenText Corporation

- Broadcom Inc.

- Ivanti, Inc.

- Flexera Software LLC

- Device42, Inc.

- SolarWinds Corporation

- Zoho Corporation Pvt. Ltd. (ManageEngine)

- Atlassian Corporation

- Freshworks Inc.

- Cherwell Software, LLC

- USU Software AG

- Matrix42 AG

- Snow Software AB

- Lansweeper NV

- SysAid Ltd.

- Quest Software Inc.

- Cloudaware Inc.

- Armis Security, Inc.

- Spiceworks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Shift to Agentless Cloud Discovery Solutions

- 4.2.2 Integration of AI-Powered Dependency Mapping and Predictive Analytics

- 4.2.3 Regulatory Mandates for Real-Time Configuration Audit Trails

- 4.2.4 Convergence of ITAM, FinOps and ESG Reporting Requirements

- 4.2.5 Rising Cybersecurity Threats Driving Asset Visibility Demand

- 4.2.6 Vendor Consolidation Enabling End-to-End ITSM Platforms

- 4.3 Market Restraints

- 4.3.1 High Cost and Complexity of Enterprise-Scale Implementations

- 4.3.2 Persistent Data Quality and Normalization Challenges

- 4.3.3 Skills Shortage in ITAM and Configuration Governance

- 4.3.4 Security Concerns Around Cloud-Hosted Configuration Data

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Consulting and Advisory

- 5.1.2.2 Integration and Deployment

- 5.1.2.3 Support and Maintenance

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 IT Operations and Service Management (ITSM)

- 5.4.2 Security, Risk and Compliance

- 5.4.3 Asset and Configuration Management

- 5.4.4 Other Applications

- 5.5 By Industry Vertical

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing

- 5.5.5 Government and Public Sector

- 5.5.6 Retail and Consumer Goods

- 5.5.7 Energy and Utilities

- 5.5.8 Other Industry Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ServiceNow, Inc.

- 6.4.2 BMC Software, Inc.

- 6.4.3 International Business Machines Corporation

- 6.4.4 OpenText Corporation

- 6.4.5 Broadcom Inc.

- 6.4.6 Ivanti, Inc.

- 6.4.7 Flexera Software LLC

- 6.4.8 Device42, Inc.

- 6.4.9 SolarWinds Corporation

- 6.4.10 Zoho Corporation Pvt. Ltd. (ManageEngine)

- 6.4.11 Atlassian Corporation

- 6.4.12 Freshworks Inc.

- 6.4.13 Cherwell Software, LLC

- 6.4.14 USU Software AG

- 6.4.15 Matrix42 AG

- 6.4.16 Snow Software AB

- 6.4.17 Lansweeper NV

- 6.4.18 SysAid Ltd.

- 6.4.19 Quest Software Inc.

- 6.4.20 Cloudaware Inc.

- 6.4.21 Armis Security, Inc.

- 6.4.22 Spiceworks, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment