|

시장보고서

상품코드

2063667

API 가시성 및 테스트 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)API Observability And Testing Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

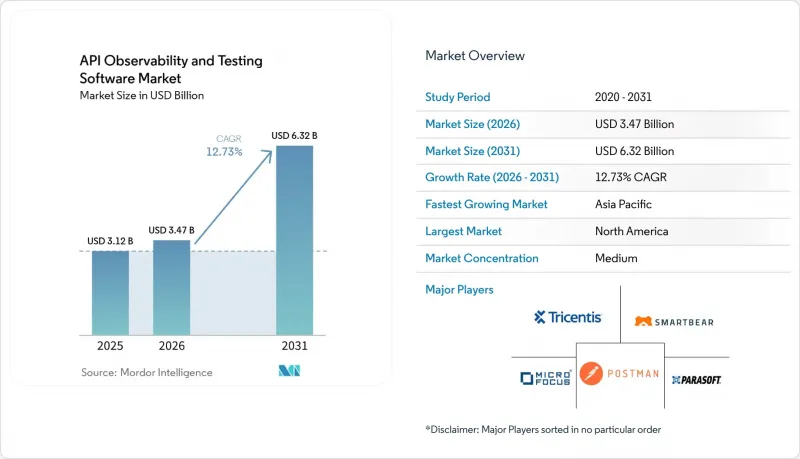

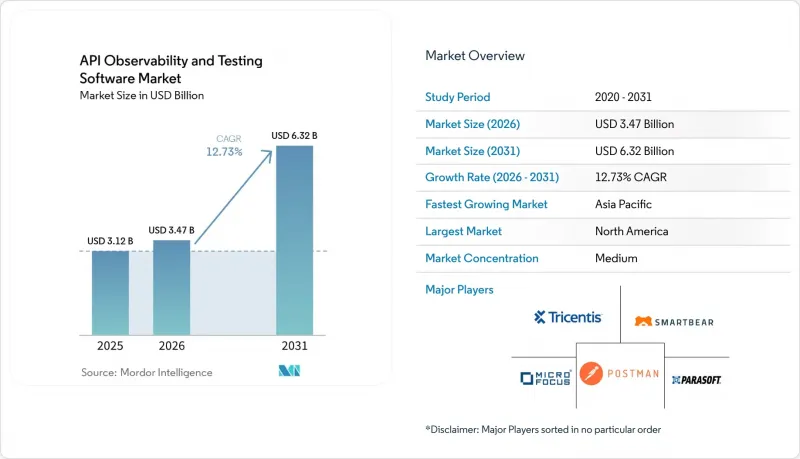

Mordor Intelligence에 의하면, API 가시성 및 테스트 소프트웨어 시장 규모는 2025년 31억 2,000만 달러로 평가되었습니다. 2026년에는 34억 7,000만 달러로 확대되어 2026-2031년 CAGR은 12.73%를 나타내, 2031년까지 63억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(솔루션 및 서비스), 도입 형태(클라우드 기반, On-Premise형 등), 조직 규모(대기업 및 중소기업), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어, 소매 및 전자상거래, 정부 기관, 제조업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 API 가시성 및 테스트 소프트웨어 시장 동향 및 인사이트

마이크로서비스 아키텍처의 도입 확대

조직은 모놀리식 아키텍처를 수백 개의 느슨하게 결합된 서비스로 분해했으며, 각 서비스는 여러 엔드포인트를 공개하고 있으므로 자동화된 계약 테스트, 스키마 검증, 분산 추적이 필요합니다. 단일 디지털 트랜잭션이 15-20개의 내부 API를 거치는 경우도 있어, 시스템의 복잡성과 상호 의존성이 증가하고 있습니다. 이를 관리하기 위해 개발팀은 서비스 메시 통합을 도입하여 지연 시간의 급격한 증가나 오류 연쇄를 실시간으로 감지하고 있습니다. 금융 서비스, 소매, 미디어 스트리밍 등의 업계에서는 시스템 가동 중단이 고객의 신뢰, 업무 연속성, 수익 창출에 직접적인 영향을 미치기 때문에 상세한 가시성이 필수적이라고 여겨집니다.

CI/CD 및 DevOps 파이프라인 가속화

DevSecOps 툴체인을 통해 하루에 여러 번 코드를 릴리스할 수 있게 되었으므로, API 테스트 주기는 몇 시간이 아닌 몇 분 이내에 완료되어야 합니다. 자동화된 회귀 테스트 모음, 계약 테스트 및 보안 스캔은 각 파이프라인 단계에서 필수적인 점검 단계로 기능하며, 프로덕션 환경에 배포하기 전에 파괴적인 변경 사항을 조기에 감지할 수 있도록 보장합니다. 이러한 변화를 통해 품질과 보안이 개발 라이프사이클에 직접 통합됩니다. 또한, 연방 정부 기관 및 국방 기관의 규정 준수 요건은本番 전 API 보안 검증에 실패한 배포를 금지함으로써 이러한 접근 방식을 강화하고 있으며, 지속적인 통합 및 배포 환경 내에서 견고하고 자동화된 테스트 프레임워크의 중요성을 더욱 부각시키고 있습니다.

레거시 시스템과의 통합의 복잡성

하이브리드 환경을 운영하는 기업은 메인프레임, 미들웨어, 클라우드 네이티브 서비스에 걸쳐 있는 REST, SOAP, GraphQL, gRPC의 페이로드를 관리해야 합니다. 이러한 이종 혼합 텔레메트리 데이터를 상호 연관시키기 위해 통합 플랫폼을 활용하는 경우는 극히 일부에 불과하며, 팀은 프로토콜별 모니터링 도구에 의존할 수밖에 없어, 그 결과 운영상의 오버헤드가 증가하고 평균 복구 시간(MTTR)이 길어지고 있습니다. 또한, 구식 COBOL 카피북의 데이터 구조를 최신 JSON 형식으로 변환할 때는 지연이나 새로운 장애 요인이 발생합니다. 이러한 복잡성으로 인해 전용 모니터링 파이프라인이 필요하게 되며, 관측 가능성이 더욱 파편화되어 엔드투엔드 성능 추적 및 사고 해결이 더욱 어려워집니다.

부문별 분석

2025년 API 가시성 및 테스트 소프트웨어 시장 매출에서 솔루션이 63.42%를 차지했으며, 이는 기업들이 DevOps 파이프라인에 통합된 플랫폼 주도형 도입을 강력히 선호하고 있음을 보여줍니다. 구매자들은 확장성, CI/CD 워크플로우와의 통합, 그리고 중앙 집중식 거버넌스를 우선시하고 있으며, 이로 인해 분산된 접근 방식보다 라이선스 기반 도구가 선호되고 있습니다. 이와 동시에, 서비스 부문은 테스트 케이스의 개발, 실행 및 지속적인 모니터링에 대한 아웃소싱 수요에 힘입어 연평균 성장률(CAGR) 13.57%로 성장하고 있습니다. 매니지드 서비스 제공업체는 컨설팅, 환경 프로비저닝, 규정 준수 모니터링을 구독 기반 모델로 통합하여 내부 리소스의 제약을 완화하고 있습니다. 예를 들어, Katalon은 2026년에 MSP 프로그램을 도입하여 AI로 생성된 테스트 라이브러리와 사전 구성된 배포 프레임워크를 통해 온보딩 기간을 단축하고 있습니다.

솔루션 생태계는 로우코드 플랫폼, 엔터프라이즈급 제품군, 오픈소스 도구와 같은 분야로 구조적으로 분할된 상태를 유지하고 있으며, 각 분야는 서로 다른 수준의 성숙도를 가진 사용자를 대상으로 하고 있습니다. 로우코드 환경은 기술적 지식이 없는 팀도 테스트를 설계하고 실행할 수 있게 함으로써 기술 격차를 해소하는 한편, IBM과 SmartBear의 엔터프라이즈 플랫폼은 거버넌스, 가시성, 라이프사이클 통합을 중시하고 있습니다. Postman과 같은 오픈소스 도구는 여전히 개발자들에게 입문용 도구로서의 역할을 수행하고 있지만, SLA에 기반한 지원 및 맞춤 설정을 제공하는 서비스 제공업체를 통해 점차 상용화가 진행되고 있습니다. 이러한 다층적인 생태계는 대기업과 중견 디지털 네이티브 기업 모두에서 도입이 확대되고 있으며, 이에 따라 시장 전체의 보급률과 지출이 증가하고 있습니다.

2025년에는 API 가시성 및 테스트 소프트웨어 시장 매출의 65.21%를 클라우드 기반 배포가 차지했으며, SaaS 소비 모델로의 구조적 전환에 힘입어 연평균 성장률(CAGR) 14.57%로 확대될 것으로 전망됩니다. 클라우드 네이티브 도구는 초기 하드웨어 투자 필요성을 없애고, 전 세계에 분산된 부하 테스트를 가능하게 하며, 가격 책정을 실제 API 사용량에 연동함으로써 비용 투명성을 높입니다. 그럼에도 불구하고, 금융 서비스, 의료, 국방 등 규제 대상 분야에서는 데이터 주권 및 규정 준수 요건으로 인해 현지에서의 실행이 의무화되어 있기 때문에 On-Premise 구축은 여전히 중요하게 여겨지고 있습니다. 기업이 워크로드를 분할하여 기능 테스트나 확장성 테스트를 클라우드에서 실행하는 한편, DORA나 FedRAMP 등의 프레임워크를 준수하기 위해 기밀 데이터 검증을 On-Premise에서 유지하는 하이브리드 모델이 주목을 받고 있습니다.

하이퍼스케일러와의 생태계 통합을 통해 클라우드 도입이 더욱 가속화되고 있습니다. AWS API Gateway, Azure API Management, Google Apigee 등의 서비스는 네이티브 통합 기능을 제공하여 인증을 효율화하고, 지연을 줄이며, 배포 파이프라인을 간소화합니다. 또한, IBM API Connect는 페더레이티드 런타임 모델을 통해 멀티클라우드 환경 전반에 걸친 통합 거버넌스를 실현함으로써 플랫폼에 대한 채택률을 높이고 있습니다. 구식 On-Premise 도구는 여전히 틈새 이용 사례에서 활용되고 있지만, 기업 소유 데이터센터의 지속적인 감소와 운영 비용(OpEx) 중심의 IT 지출 모델로의 광범위한 전환으로 인해, API 가시성 및 테스트 소프트웨어 시장에서 클라우드의 우위는 앞으로도 유지될 것으로 예측됩니다.

지역별 분석

2025년, 북미는 API 가시성 및 테스트 소프트웨어 시장 매출의 34.70%를 차지했습니다. 이는 DevOps의 성숙한 도입, 하이퍼스케일러의 높은 집중도, 그리고 API 품질 기준을 강화하는 ‘의료보험 상호운용성 및 책임법(HIPAA)’과 같은 엄격한 규제 체계에 힘입은 결과입니다. 연방 정부 기관들은 검증 요건을 확대하고 있으며, 캐나다의 금융 기관들은 오픈 뱅킹 인프라를 지속적으로 강화하고 있습니다. 그러나 대기업들이 공급업체 기반을 합리화함에 따라 벤더 통합이 진행되면서 성장세가 둔화되고 있습니다. 그럼에도 불구하고, 국방, 주 정부, 제조업 등 도입률이 낮은 분야에서는 특히 레거시 시스템이 API 중심 아키텍처로 전환됨에 따라 더 많은 기회가 생겨나고 있습니다.

아시아태평양은 디지털 인프라의 급속한 확대와 높은 API 거래량에 힘입어 연평균 성장률(CAGR) 13.72%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 2025년에 1,000억 건 이상의 거래를 처리한 인도의 Unified Payments Interface(UPI)는 API에 대한 의존도가 높음을 보여주고 있으며, 확장 가능한 클라우드 기반 테스트 솔루션의 필요성을 부각시키고 있습니다. 중국의 주권 클라우드 정책은 국내 공급업체를 우대하고 있지만, 국제적인 공급업체들도 현지화된 사업 전개나 합작 투자를 통해 시장에 진출하고 있습니다. 한편, 일본과 한국은 스마트 제조 이니셔티브에 API 검증을 포함시키고 있으며, 호주는 ‘소비자 데이터 권리(Consumer Data Right)’ 프레임워크 하에서 규정 준수를 추진하고 있습니다. 표준의 파편화와 현지화 요건은 실행의 복잡성을 초래하지만, 장기적인 수요를 뒷받침하고 있습니다.

유럽 시장 동향은 DORA(데이터 마이그레이션성 및 권리법)에 기반한 규제 집행과 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))과 관련된 엄격한 데이터 거버넌스 요건에 의해 형성되고 있습니다. 영국, 독일, 프랑스의 금융 기관들은 사이버 장애를 시뮬레이션하고 복구 SLA를 검증하기 위한 첨단 테스트 프레임워크에 투자하고 있습니다. 스위스와 북유럽 국가들은 국경을 초월한 결제 통합을 지원하고 있으며, 지연 시간에 민감한 API 테스트에 대한 수요가 증가하고 있습니다. 남미, 중동 및 아프리카는 절대적인 규모로 보면 여전히 작지만, SaaS 기반 가격 모델을 통해 성장하고 있습니다. 브라질의 Pix나 사우디아라비아의 디지털 정부 프로그램과 같은 노력들이 API 테스트의 지속적인 도입을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the aPI observability and testing software market size is expected to grow from USD 3.12 billion in 2025 to USD 3.47 billion in 2026 and is forecast to reach USD 6.32 billion by 2031 at 12.73% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud-Based, On-Premises, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Retail and E-Commerce, Government, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global API Observability And Testing Software Market Trends and Insights

Growing Adoption of Microservices Architectures

Organizations are decomposing monolithic architectures into hundreds of loosely coupled services, each exposing multiple endpoints that require automated contract testing, schema validation, and distributed tracing. A single digital transaction can traverse 15-20 internal APIs, increasing system complexity and interdependencies. To manage this, development teams deploy service mesh integrations to detect latency spikes and error cascades in real time. Industries such as financial services, retail, and media streaming consider deep observability essential, as system downtime directly impacts customer trust, operational continuity, and revenue generation.

Acceleration of CI/CD and DevOps Pipelines

DevSecOps toolchains enable multiple daily code releases, requiring API testing cycles to complete within minutes rather than hours. Automated regression suites, contract testing, and security scans function as mandatory checkpoints across each pipeline stage, ensuring early detection of breaking changes before production deployment. This shift embeds quality and security directly into the development lifecycle. Additionally, compliance mandates from federal and defense agencies reinforce this approach by prohibiting deployments that fail pre-production API security validations, increasing the criticality of robust, automated testing frameworks within continuous integration and delivery environments.

Integration Complexity with Legacy Systems

Enterprises operating hybrid environments must manage REST, SOAP, GraphQL, and gRPC payloads across mainframes, middleware, and cloud native services. Only a minority use a unified platform to correlate such heterogeneous telemetry, forcing teams to rely on protocol-specific monitoring tools that increase operational overhead and extend mean time to recovery. Additionally, translating legacy COBOL copybook data structures into modern JSON formats introduces latency and new failure points. These complexities require dedicated monitoring pipelines, further fragmenting observability and making end-to-end performance tracking and incident resolution more difficult.

Other drivers and restraints analyzed in the detailed report include:

- Rising API Security Incidents and Compliance Mandates

- Expansion of Cloud-Native and Serverless Workloads

- Shortage of Skilled API Test Engineer

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 63.42% of API Observability And Testing Software Market revenue in 2025, indicating strong enterprise preference for platform-led adoption embedded within DevOps pipelines. Buyers prioritize scalability, integration with CI/CD workflows, and centralized governance, which favors licensed tools over fragmented approaches. In parallel, the services segment is expanding at a 13.57% CAGR, driven by demand for outsourced test-case development, execution, and continuous monitoring. Managed service providers are consolidating consulting, environment provisioning, and compliance oversight into subscription-based models, reducing internal resource constraints. For instance, Katalon introduced its 2026 MSP Program, accelerating onboarding timelines through AI-generated test libraries and pre-configured deployment frameworks.

The solutions ecosystem remains structurally fragmented across low-code platforms, enterprise-grade suites, and open-source tools, each targeting distinct user maturity levels. Low-code environments address skill gaps by enabling non-technical teams to design and execute tests, while enterprise platforms from IBM and SmartBear emphasize governance, observability, and lifecycle integration. Open-source tools such as Postman continue to serve as entry points for developers, but are increasingly commercialized via service providers offering SLA-backed support and customization. This layered ecosystem is expanding adoption across both large enterprises and mid-market digital-native firms, thereby increasing overall market penetration and spend.

Cloud-based deployment accounted for 65.21% of API observability and testing software market revenue in 2025 and is projected to expand at a 14.57% CAGR, driven by structural shifts toward SaaS consumption models. Cloud-native tools remove the need for upfront hardware investment, enable globally distributed load testing, and align pricing with actual API usage volumes, improving cost transparency. Despite this, on-premises deployments remain relevant in regulated sectors such as financial services, healthcare, and defense, where data sovereignty and compliance requirements mandate localized execution. Hybrid models are gaining traction as enterprises split workloads, running functional and scalability tests in the cloud while retaining sensitive data validation on-site to comply with frameworks such as DORA and FedRAMP.

Ecosystem integration with hyperscalers is further accelerating cloud adoption. Services like AWS API Gateway, Azure API Management, and Google Apigee provide native integrations that streamline authentication, reduce latency, and simplify deployment pipelines. Additionally, IBM API Connect enables centralized governance across multi-cloud environments through a federated runtime model, increasing platform stickiness. While legacy on-premises tools persist in niche use cases, the ongoing decline of enterprise-owned data centers and a broader shift toward OpEx-driven IT spending models are expected to sustain cloud dominance in the API observability and testing software market.

Geography Analysis

North America accounted for 34.70% of the API observability and testing software market revenue in 2025, supported by mature DevOps adoption, high hyperscaler concentration, and strict regulatory frameworks such as the Health Insurance Portability and Accountability Act that elevate API quality standards. Federal agencies are expanding validation mandates, while Canadian financial institutions continue strengthening open-banking infrastructure. However, growth is moderating due to vendor consolidation as large enterprises rationalize supplier bases. Despite this, underpenetrated segments, including defense, state government, and industrial manufacturing, offer incremental opportunities, particularly as legacy systems transition to API-driven architectures.

Asia-Pacific is the fastest-growing region, with a 13.72% CAGR, driven by the rapid expansion of digital infrastructure and high API transaction volumes. India's Unified Payments Interface, which processed over 100 billion transactions in 2025, underscores the scale of API dependency, underscoring the need for scalable, cloud-based testing solutions. China's sovereign cloud policies favor domestic vendors, although international providers are entering through localized deployments and joint ventures. Meanwhile, Japan and South Korea are embedding API validation within smart manufacturing initiatives, and Australia is advancing compliance under its Consumer Data Right framework. Fragmentation in standards and localization requirements introduces execution complexity but sustains long-term demand.

Europe's market trajectory is shaped by regulatory enforcement under DORA and stringent data governance requirements linked to the General Data Protection Regulation. Financial institutions across the United Kingdom, Germany, and France are investing in advanced testing frameworks to simulate cyber disruptions and validate recovery SLAs. Switzerland and Nordic countries are supporting cross-border payment integration, increasing demand for latency-sensitive API testing. South America, the Middle East, and Africa remain smaller in absolute terms but are scaling through SaaS-based pricing models. Initiatives such as Brazil's Pix and Saudi Arabia's digital government programs are reinforcing sustained adoption of API testing.

- Postman, Inc.

- SmartBear Software, Inc.

- Tricentis GmbH

- Micro Focus International plc

- Parasoft Corporation

- Katalon, Inc.

- RapidAPI, Inc.

- Sauce Labs, Inc.

- IBM Corporation

- Oracle Corporation

- Google LLC (Apigee)

- Kong, Inc.

- MuleSoft LLC

- Axway Software SA

- WSO2, Inc.

- Broadcom, Inc. (Layer7)

- Tyk Technologies Ltd.

- Solo.io, Inc.

- Stoplight, Inc.

- Assertible, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.1.1 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Microservices Architectures

- 4.2.2 Acceleration of CI/CD and DevOps Pipelines

- 4.2.3 Rising API Security Incidents and Compliance Mandates

- 4.2.4 Expansion of Cloud-Native and Serverless Workloads

- 4.2.5 Low-Code and No-Code Test Automation Platforms

- 4.2.6 Per-Endpoint Pricing Models Driving SME Uptake

- 4.3 Market Restraints

- 4.3.1 Integration Complexity with Legacy Systems

- 4.3.2 Shortage of Skilled API Test Engineers

- 4.3.3 Observability Data Cost Inflation in Large-Scale Deployments

- 4.3.4 Tool-Sprawl Leading to Governance Challenges

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare

- 5.4.4 Retail and E-commerce

- 5.4.5 Government

- 5.4.6 Manufacturing

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Mexico

- 5.5.1.3 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Switzerland

- 5.5.2.7 Benelux

- 5.5.2.8 Russia

- 5.5.2.9 Nordics

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Argentina

- 5.5.4.2 Brazil

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Kingdom of Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Postman, Inc.

- 6.4.2 SmartBear Software, Inc.

- 6.4.3 Tricentis GmbH

- 6.4.4 Micro Focus International plc

- 6.4.5 Parasoft Corporation

- 6.4.6 Katalon, Inc.

- 6.4.7 RapidAPI, Inc.

- 6.4.8 Sauce Labs, Inc.

- 6.4.9 IBM Corporation

- 6.4.10 Oracle Corporation

- 6.4.11 Google LLC (Apigee)

- 6.4.12 Kong, Inc.

- 6.4.13 MuleSoft LLC

- 6.4.14 Axway Software SA

- 6.4.15 WSO2, Inc.

- 6.4.16 Broadcom, Inc. (Layer7)

- 6.4.17 Tyk Technologies Ltd.

- 6.4.18 Solo.io, Inc.

- 6.4.19 Stoplight, Inc.

- 6.4.20 Assertible, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment