|

시장보고서

상품코드

2063680

가금류 헬스케어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Poultry Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

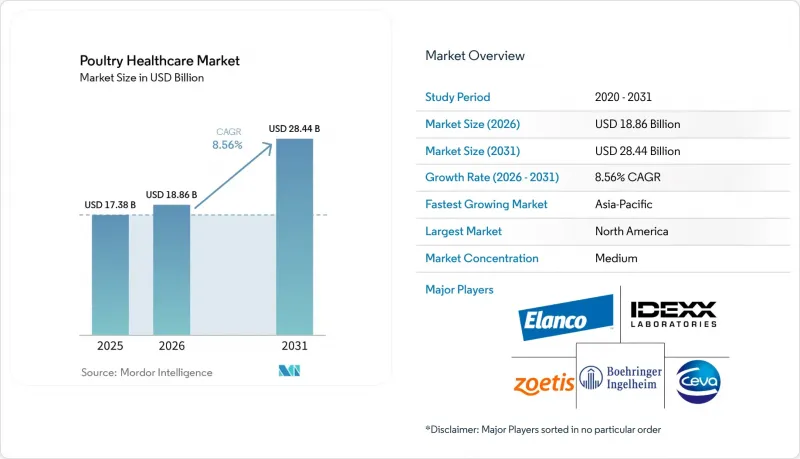

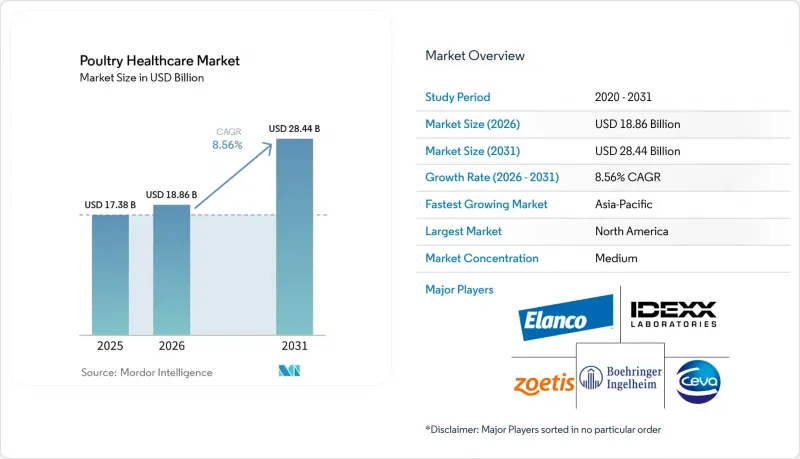

Mordor Intelligence에 의하면, 가금류 헬스케어 시장 규모는 2025년에 173억 8,000만 달러로 평가되었습니다. 2026년 188억 6,000만 달러에서 2031년까지 284억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.56%를 나타낼 전망입니다.

본 보고서는 제품 유형(백신, 구충제, 항감염제 등), 동물 유형(육계, 산란계, 종계 등), 투여 경로(경구, 비경구 등), 질환 유형(바이러스성 질환, 세균성 질환 등), 최종 사용자(상업용 가금류 등) 및 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 가금류 헬스케어 시장 동향 및 인사이트

신흥국에서의 상업용 육계 생산의 급속한 집약화

중국에서는 2024년에 76억 마리의 육계가 도축되었으며, 인도에서는 2024년부터 2025년까지의 기간 동안 53억 마리가 도축되었습니다. 이로 인해 비육 기간이 단축되면서 병원체로 인한 부담이 커지고 있습니다. 사육 밀도가 높아짐에 따라, 통합형 생산자들은 호흡기 및 장 감염증을 조기에 검출할 수 있는 다가 백신이나 진단법으로 전환해야 할 필요에 직면해 있습니다. 브라질에서는 2024년에 69억 마리의 닭이 살처분되었으며, 조류인플루엔자가 발생하지 않은 국가의 수입업체들이 시장에 계속 접근할 수 있도록 하기 위해 생물안전 조치를 강화해야 했습니다. 아르헨티나에서는 2023년부터 2025년에 걸쳐 생산 능력이 12% 증가함에 따라 수의사 네트워크에 부담이 가중되었고, 서비스 범위 부족 문제가 드러났습니다. 이로 인해 턴키 방식의 예방접종 계약에 대한 수요가 증가했습니다. 베트남과 태국에서는 환경 제어형 닭장으로의 전환이 진행되고 있으며, 이로 인해 사망률은 낮아지고 있지만, 질병 발생 시 발생하는 경제적 비용은 증가하고 있습니다. 이 때문에 예방용 생물학적 제제에 대한 지출이 증가하고 있습니다.

정부 보조금을 통한 가금류 백신 접종 프로그램 확대

인도의 ‘국가 동물 질병 대책 프로그램’은 2024년에 4억 5,000만 달러를 편성하여, 가정용 및 준상업용 가금류에 대한 조류 인플루엔자 및 뉴캐슬병 백신 비용을 부담했습니다. 인도네시아도 2025년에 이에 이어 새로운 콜드체인 허브를 통해 2억 회분의 뉴캐슬병 백신을 배포했습니다. 필리핀은 세바 산테 아니마르(Seba Sainte Animal)사와 제휴하여, 고온 기후에서도 효과를 보장할 수 있는 지역 냉동고 설치를 추진하고 있습니다. 아프리카 연합에서는 열안정성 제제를 활용한 시범 사업을 통해 전력 소비가 많은 냉장 설비에 대한 의존도를 낮추고 있습니다. 보조금 제도 덕분에 제조업체의 잠재 고객 기반이 확대되면서, 정기 예방접종이 각국의 수의학 규정에 점차 정착되고 있습니다.

조류 인플루엔자 백신용 주요 항원공급 부족

2024년부터 2025년에 걸쳐 발생한 H5N1 유행으로 인해 2025년 4월까지 미국에서 1억 6,862만 마리의 가금류가 살처분되었으나, 계란 유래 백신 제조 시설은 생산 규모를 확대하는 데 18개월이 소요되기 때문에 항원 공급 능력이 이를 따라가지 못했습니다. 2025년 2월에 시작된 미국 농무부(USDA)의 10억 달러 규모 프로그램은 6개월 만에 생산 능력을 확대할 수 있는 세포 배양주에 자금을 지원하고 있지만, 본격적인 생산 체제가 갖춰지는 것은 2027년 하반기가 될 전망입니다. 유럽은 2024년 유행 당시 브라질과 인도로부터 제한된 양의 백신을 확보했으나, 이는 지역 간 상호 의존 관계를 여실히 드러냈습니다. 인간용 팬데믹 인플루엔자 백신과의 기질 경쟁이 공급 부족을 악화시켜, 생산자들에게 막대한 비용이 드는 가금류 살처분을 강요할 뿐만 아니라, 하류 의료 제품 소비의 위축을 초래하고 있습니다.

부문별 분석

2025년, 백신은 47.12%라는 최대 점유율을 유지했습니다. 이는 뉴캐슬병, 전염성 기관지염, 조류 인플루엔자에 대한 의무 예방접종이 뒷받침하고 있습니다. 프로바이오틱스와 프리바이오틱스는 대형 소매업체들이 항생제를 사용하지 않은 닭고기를 요구하고 있으며, 동료 심사를 거친 연구에서 바실러스 균주가 살모넬라균 수를 최대 60%까지 감소시킨다는 사실이 입증됨에 따라, 2031년까지 연평균 8.79%의 성장률이 예상됩니다. 항감염제는 규제 당국이 의학적으로 중요한 분자의 사용을 제한함에 따라 시장 점유율이 줄어들고 있지만, 기생충 구제제는 이온포어와 백신을 번갈아 사용하는 셔틀 프로그램을 통해 판매량을 유지하고 있습니다. 진단 분야는 긍정적인 요소입니다. IDEXX사의 H5, H7, H9를 대상으로 한 2시간 멀티플렉스 PCR은 신속한 군 격리를 필요로 하는 통합 농가(양계 농가)들 사이에서 지지를 넓혀가고 있습니다.

2차적 영향은 발효 기술과 현장 시험을 통한 검증에 집중되어 있습니다. 상업 환경에서 균주별 고유 데이터를 제공할 수 있는 공급업체들이, 과거에는 범용 항생제 공급업체들이 차지하고 있던 유통 시장을 점차 확보해 나가고 있습니다. 사료 첨가제 제조업체와 대형 백신 제조업체 간의 교차 라이선싱은 장내 환경 개선 솔루션과 예방접종 프로토콜을 결합하는 수단으로 부상하고 있으며, 통합 생산자의 조달 과정을 원활하게 하고 있습니다.

2025년에는 육계가 매출의 63.34%를 차지했으며, 이는 전 세계적으로 연간 1,000억 마리가 넘는 병아리가 공급된다는 사실을 반영합니다. 그 다음으로 산란계가 뒤를 잇고 있으며, 번식계는 마릿수는 적지만 2031년까지 연평균 성장률(CAGR) 8.91%로 급성장하고 있습니다. 통합형 양계업자들은 부화율이 1포인트 상승할 때마다 하류 단계의 육계 생산량이 수백만 마리 증가한다는 사실을 인식하고 있으며, 이에 따라 마이코플라스마, ILT, 산란 정지 증후군을 예방하는 프리미엄 백신 접종 일정의 도입이 정당화됩니다.

2024년 미국에서 발생한 메타뉴모바이러스로 인한 감염 확산으로 부화율이 15% 하락하고 8,000만 달러 상당의 병아리 손실이 발생함에 따라, 번식용 닭이 생식기 병원체에 대해 취약하다는 사실이 여실히 드러났습니다. 이러한 사태에 따라, 생약독화 종계용 백신의 도입이 급속히 진행되었으며, 조부모 닭 농장에 대한 생물안전성 감사가 강화되었습니다. 현재, 통합형 양계 기업들은 종계 건강을 단순한 비용 항목이 아닌 이익을 창출하는 원천으로 간주하고, 취급 횟수를 최소화하며, 더 오랜 기간 유효한 복합 항원의 개발을 위해 연구 개발을 추진하고 있습니다.

지역별 분석

2025년에는 북미가 매출의 39.76%를 차지했습니다. 이는 미국의 90억 마리에 달하는 육계 사육군과 캐나다의 수출 지향형 가공업체들에 의해 뒷받침된 것입니다. 2025년 2월 FDA가 조에티스의 H5N1 백신을 조건부로 승인함에 따라, 축산 농가들은 가축을 도살하는 대신 백신 접종을 실시할 수 있게 되었으며, 만약 H5N1이 풍토병화된다면 연간 5억 달러의 비용 절감이 예상됩니다. 사료비 급등과 노동력 부족으로 인해 고가의 생물학적 제제의 도입은 주춤하고 있으며, 구매자들은 투자 회수 기간이 짧은 솔루션으로 눈을 돌리고 있습니다.

아시아태평양은 중국의 76억 마리 육계 생산량과 인도의 정부 자금 지원 백신 접종 이니셔티브에 힘입어, 2031년까지 연평균 성장률(CAGR) 9.34%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 인도네시아에서 진행 중인 2억 회분 백신 접종 캠페인과 베트남에서 상업화된 닭 사육 시설로의 전환이 가금류 헬스케어 시장을 확대시키고 있습니다. 대체품의 위협은 여전히 존재하며, 기업들은 블록체인 라벨 도입을 추진하고 있지만, 지역적 규모의 확대가 규정 준수 문제의 복잡성을 상회하고 있습니다.

유럽, 중동 및 아프리카, 남미가 합쳐서 전 세계 매출의 나머지 부분을 차지하고 있습니다. 예방적 항생제 사용을 금지하는 유럽의 규제로 인해 프로바이오틱스의 보급과 자가 제조 백신 신청이 가속화되었으며, 이는 2022년부터 2025년에 걸쳐 크게 증가했습니다. 브라질의 69억 마리에 달하는 도축량은 조류인플루엔자 비발생 지역을 조건으로 하는 수입국의 요구를 충족시키기 위한 백신 접종 비용을 뒷받침하고 있습니다. 아르헨티나 페소의 평가절하는 생산 능력 확대를 촉진했지만, 수의학 분야의 병목 현상을 드러내기도 했습니다. 수자원이 부족한 GCC 국가들은 가금류의 대부분을 수입하고 있지만, 생물안전 대책이 마련된 실내 양계장에 대한 투자를 확대하고 있으며, 할랄 원료 감사 기준을 충족하는 고효능 백신을 위한 틈새 시장을 개척하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the poultry healthcare market size was valued at USD 17.38 billion in 2025 and is estimated to grow from USD 18.86 billion in 2026 to reach USD 28.44 billion by 2031, at a CAGR of 8.56% during the forecast period (2026-2031).

This report is Segmented by Product Type (Vaccines, Parasiticides, Anti-Infectives, and More), Animal Type (Broilers, Layers, Breeders, and Others), Route of Administration (Oral, Parenteral, and More), Disease Type (Viral Disease, Bacterial Diseases, and More) End Users (Commercial Poultry, and More) and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Poultry Healthcare Market Trends and Insights

Rapid Intensification of Commercial Broiler Production in Emerging Economies

China processed 7.6 billion broilers in 2024, and India turned out 5.3 billion birds across the 2024-2025 cycle, compressing grow-out times and heightening pathogen pressure. Higher stocking densities are pushing integrators toward multivalent vaccines and diagnostics that detect respiratory and enteric infections early. Brazil's 6.9 billion chicken slaughter in 2024 required biosecure upgrades to retain market access to influenza-free importers. Argentina's 12% capacity hike between 2023 and 2025 strained veterinary networks, exposing coverage gaps that spurred demand for turnkey immunization contracts. Vietnam and Thailand are pivoting to environmentally controlled houses, trimming mortality yet amplifying the economic cost of any outbreak, which reinforces spending on preventive biologics.

Expansion of Government-Subsidized Poultry Vaccination Programs

India's National Animal Disease Control Programme earmarked USD 450 million in 2024 to underwrite avian-influenza and Newcastle-disease vaccines for backyard and semi-commercial flocks. Indonesia followed in 2025 with 200 million Newcastle-disease doses distributed through new cold-chain hubs. The Philippines partnered with Ceva Sante Animale to locate regional freezers that ensure potency in hot climates. African Union pilots with thermostable formulations are cutting reliance on electricity-intensive refrigeration. Subsidies are enlarging the addressable base for manufacturers and embedding routine immunization into national veterinary codes.

Supply Shortages of Critical Antigens for Avian-Influenza Vaccines

The 2024-2025 H5N1 episode forced depopulation of 168.62 million U.S. birds by April 2025, yet antigen capacity lagged because egg-based plants need 18 months to scale. A USD 1 billion USDA program launched in February 2025 is funding cell-culture lines that ramp in six months, though full output will not materialize until late 2027. Europe diverted limited doses from Brazil and India during its 2024 outbreak, underscoring trans-regional interdependence. Competition with human pandemic-influenza vaccines for the same substrates exacerbates scarcity, forcing producers into costly culling and shrinking downstream health-product consumption.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Demand for Antibiotic-Free "No-ABF" Value Chains

- Acceleration of Digital Flock-Health Monitoring Platforms

- Escalating Counterfeit Biologics Trade in South-East Asia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vaccines retained a 47.12% lion's share in 2025, anchored by compulsory Newcastle disease, infectious bronchitis, and avian influenza immunizations. Probiotics and prebiotics are charting an 8.79% annual rise to 2031 as large retailers demand antibiotic-free birds and peer-reviewed trials show Bacillus strains cutting Salmonella counts by up to 60%. Anti-infectives are losing ground where regulators curb medically important molecules, while parasiticides sustain volume through shuttle programs that rotate ionophores with vaccines. Diagnostics is a bright spot; IDEXX's two-hour multiplex PCR for H5, H7, and H9 is gaining traction among integrators seeking rapid flock segregation.

Second-order effects center on fermentation expertise and field-trial validation: suppliers that can provide strain-specific data in commercial settings are capturing distribution slots once held by generic antibiotic vendors. Cross-licensing between feed-additive firms and vaccine majors is emerging as a route to bundle gut-health solutions with immunization protocols, smoothing procurement for integrators.

Broilers delivered 63.34% revenue in 2025, reflecting annual placements exceeding 100 billion birds worldwide. Layers follow, but breeders, although fewer in headcount, are racing ahead at an 8.91% CAGR to 2031. Integrators recognize that every 1-point uptick in hatchability lifts downstream broiler volume by millions of chicks, justifying premium vaccination schedules covering Mycoplasma, ILT, and egg-drop syndrome.

Breeder sensitivity to reproductive pathogens was highlighted when a 2024 United States metapneumovirus flare cut hatch rates 15%, costing USD 80 million in lost chicks. The fallout prompted rapid uptake of live-attenuated breeder vaccines and reinforced biosecurity audits at grandparent farms. Integrators now view breeder health as a profit-center rather than a cost line item, directing R&D toward longer-lasting, combined antigens that minimize handlings.

Geography Analysis

North America accounted for 39.76% revenue in 2025, supported by the United States' 9 billion broiler flock and Canada's export-oriented processors. FDA's conditional clearance of Zoetis' H5N1 vaccine in February 2025 lets producers vaccinate rather than depopulate, with potential savings of USD 500 million annually if endemic status emerges. High feed costs and labor scarcity temper the adoption of premium biologics, steering buyers toward solutions with tight payback metrics.

Asia-Pacific is the fastest-advancing region at 9.34% CAGR to 2031, powered by China's 7.6 billion broiler output and India's government-funded vaccination initiatives. Indonesia's 200 million-dose campaign and Vietnam's transition to commercialized barns are enlarging the poultry healthcare market. Counterfeit threats persist, prompting firms to embed blockchain labels, yet regional scale outweighs compliance complexity.

Europe, the Middle East & Africa, and South America jointly supply the balance of global receipts. European regulation banning prophylactic antibiotics has accelerated probiotic penetration and autogenous vaccine filings, which rose significantly between 2022 and 2025. Brazil's 6.9 billion-bird slaughter volume underpins vaccination spend to satisfy influenza-free importers. Argentine peso devaluation spurred a capacity hike but uncovered veterinary bottlenecks. Water-scarce GCC states import most poultry yet are investing in biosecure indoor farms, opening niches for high-efficacy vaccines that qualify under Halal ingredient audits.

- Anicon Laboratories

- Avivagen

- Bimeda

- Biochek

- Boehringer Ingelheim

- Ceva Sante Animale

- Dechra Pharmaceuticals

- Elanco

- Hester Biosciences

- Hipra

- Huvepharma

- IDEXX

- Indovax

- Megacor Diagnostik

- Merck

- Phibro Animal Health

- Provet Pharma

- Thermo Fisher Scientific

- Venky's India Ltd.

- Virbac

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Intensification of Commercial Broiler Production in Emerging Economies

- 4.2.2 Expansion of Government-Subsidized Poultry Vaccination Programs

- 4.2.3 Growth In Demand for Antibiotic-Free "No-ABF" Value Chains

- 4.2.4 Acceleration of Digital Flock-Health Monitoring Platforms

- 4.2.5 Development of Next-Gen Vector Vaccines Targeting Multiple Serotypes

- 4.2.6 ESG-Driven Retail Sourcing Mandates for Animal-Welfare Certification

- 4.3 Market Restraints

- 4.3.1 Supply Shortages of Critical Antigens for Avian-Influenza Vaccines

- 4.3.2 Escalating Counterfeit Biologics Trade in South-East Asia

- 4.3.3 Regulatory Delays for Novel Feed Additive Approvals in the EU

- 4.3.4 Consolidation Of Integrators Squeezing Margins of Health-Product Vendors

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Vaccines

- 5.1.2 Parasiticides

- 5.1.3 Anti-infectives

- 5.1.4 Probiotics & Prebiotics

- 5.1.5 Diagnostics Kits & Reagents

- 5.2 By Animal Type

- 5.2.1 Broilers

- 5.2.2 Layers

- 5.2.3 Breeders

- 5.2.4 Others

- 5.3 By Administration Route

- 5.3.1 Oral

- 5.3.2 Parenteral

- 5.3.3 Topical

- 5.3.4 Spray / Aerosol

- 5.4 By Disease Type

- 5.4.1 Viral Disease

- 5.4.2 Bacterial Diseases

- 5.4.3 Parasitic Diseases

- 5.4.4 Fungal Diseases

- 5.5 By End Users

- 5.5.1 Commercial Poultry

- 5.5.2 Backyard Poultry

- 5.5.3 Veterinary clinic

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Anicon Laboratories

- 6.3.2 Avivagen

- 6.3.3 Bimeda

- 6.3.4 Biochek

- 6.3.5 Boehringer Ingelheim Vetmedica

- 6.3.6 Ceva Sante Animale

- 6.3.7 Dechra Pharmaceuticals

- 6.3.8 Elanco Animal Health

- 6.3.9 Hester Biosciences

- 6.3.10 HIPRA

- 6.3.11 Huvepharma

- 6.3.12 IDEXX Laboratories

- 6.3.13 Indovax

- 6.3.14 Megacor Diagnostik

- 6.3.15 Merck Animal Health

- 6.3.16 Phibro Animal Health

- 6.3.17 Provet Pharma

- 6.3.18 Thermo Fisher Scientific

- 6.3.19 Venky's India Ltd.

- 6.3.20 Virbac

- 6.3.21 Zoetis Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment