|

시장보고서

상품코드

2063681

신생아 및 산전 진단 기기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Neonatal And Prenatal Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

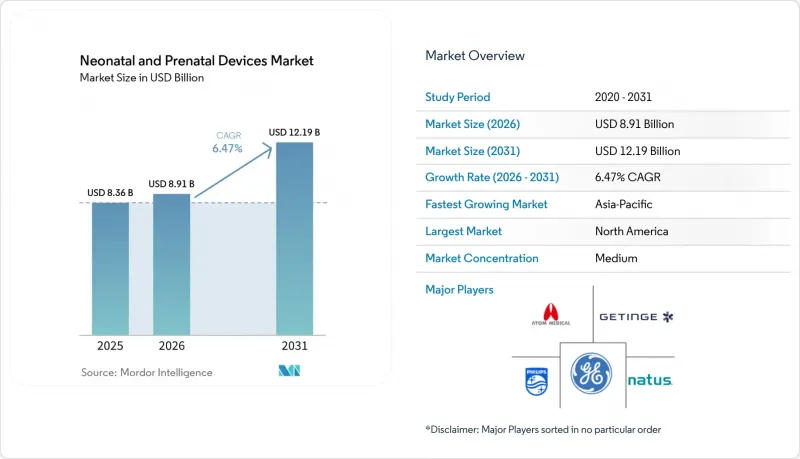

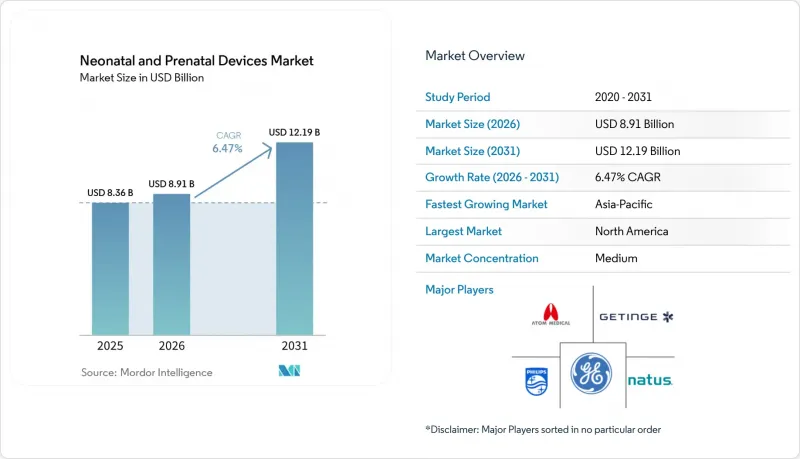

Mordor Intelligence에 의하면, 신생아 및 산전 진단 기기 시장 규모는 2025년 83억 6,000만 달러로 평가되었습니다. 2026년 89억 1,000만 달러에서 2031년까지 121억 9,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 6.47%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(산전·태아용 기기, 신생아용 기기), 기술(침습적 모니터링, 비침습적 모니터링), 최종 사용자(병원, 산부인과·전문 클리닉, 기타) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 신생아 및 산전 진단 기기 시장 동향 및 인사이트

조산 발생률 증가

조산율이 높은 수준을 유지함에 따라 신생아 및 주산기 의료기기 시장은 구조적인 수요 압박에 지속적으로 직면하고 있습니다. 미국의 자료에 따르면, 2023년 조산 건수는 37만 3,902건이며, 흑인 영아(14.7%)와 아메리카 원주민 또는 알래스카 원주민 영아(12.4%)에서 여전히 가장 높은 비율을 보였습니다. 단태 임신에 비해 조산 확률이 7배나 높은 다태 임신은 불임 치료 증가에 따라 관련 기기 수요를 더욱 확대시키고 있습니다. 따라서 병원에서는 수동 관찰보다 더 조기에 패혈증이나 괴사성 장염을 감지할 수 있는 첨단 신생아 인큐베이터, 인공호흡기, 예측 분석 시스템에 대한 투자를 가속화하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 선진국에서는 총 출생 수가 정체되어 있음에도 불구하고 생명 유지 장치 수요는 견조한 추세를 보이고 있습니다.

고위험 임신 및 산전 선별 검사 건수 증가

대부분의 선진국에서 임산부의 연령이 높아지면서 고위험 임신으로 분류되는 비율이 증가하고 있으며, 이는 정교한 산전 영상 진단에 대한 수요를 촉진하고 있습니다. 2023년, 40세 이상 여성의 조산율은 14.6%에 달했고, 전국 평균을 크게 상회했습니다. AI를 활용한 초음파 검사에서는 현재 신경관 결손증의 95%를 검출할 수 있으며, 머신러닝을 통한 분류 알고리즘은 테스트 데이터셋에서 71.5%의 진단 정확도를 달성하고 있습니다. 원격 초음파 진단을 통해 전문의가 지역 클리닉을 지원할 수 있게 되면서 임상 현장에서의 도입이 가속화되고 있으며, 2023년에 76.1%까지 낮아진 임신 초기 산전 관리 수진율 격차를 해소하고 있습니다. 웨어러블 임산부 모니터는 심박수, 혈중 산소 농도, 활동량 센서를 결합하여 흡연 및 임신성 당뇨병의 위험을 실시간으로 관리합니다. 디지털 케어 패스웨이는 치료 성과를 저해하지 않으면서 불필요한 내원을 줄이고, 시스템 비용을 절감하는 동시에, 연결형 산전 기기에 대한 보험사의 보험금 지급을 촉진합니다.

선진국의 출산율 감소

세계의 총 특수 출생률은 2050년까지 1.83, 2010년까지 1.59로 떨어질 것으로 예측되며, 이는 인구 대체 수준을 크게 밑도는 수치입니다. 이로 인해 가장 부유한 국가들의 신생아 및 산전 진단 기기 시장의 잠재적 대상 규모가 축소될 것입니다. 미국에서는 2023년에 출생 수가 2% 감소했고, 일반 합계 특수 출생률이 3% 하락한 것으로 보고되었습니다. 산부인과 병동의 폐쇄로 인해 접근성 문제가 더욱 심각해지고 있습니다. 200곳 이상의 지방 병원이 분만 서비스를 중단함에 따라, 230만 명의 여성이 ‘산부인과 의료 사막’에 방치되어 있습니다. 사회경제적 요인?결혼 연령의 상승, 고등교육의 보급, 육아비 급등이 계속해서 출생 수를 억제하고 있으며, 프랑스, 한국, 싱가포르에서 시행되고 있는 정책적 인센티브의 효과도 제한적인 수준에 그치고 있습니다. 출생 수의 절대적 감소로 인해, 공급업체들은 선진 지역에서의 수익 성장을 유지하기 위해 첨단 의료기기 및 부수적인 재택 모니터링 서비스로 사업을 전환할 수밖에 없게 되었습니다.

부문별 분석

신생아용 의료기기 매출액은 2031년까지 연평균 성장률(CAGR) 9.53%로 증가할 것으로 예상되며, 2025년에는 산전·태아용 의료기기가 신생아 및 산전 진단 기기 시장의 62.88%를 차지했음에도 불구하고, 산전·태아용 카테고리를 상회하는 성장이 전망됩니다. 인큐베이터와 관련된 신생아 및 산전 진단 기기 시장 규모는 가장 빠르게 확대되고 있습니다. 이는 병원이 기존 모델보다 비용이 몇 분의 1 수준이면서도 ISO 온도 안정성 기준을 충족하는 휴대용 배터리 구동 장치로 교체하고 있기 때문입니다. 방글라데시의 자원이 부족한 시설에서는 2만 대의 부족에 직면해 있으며, 약 250파운드 무게의 소형 시스템은 조달 장벽을 낮추고 정부의 입찰을 촉진하고 있습니다. 광선 치료 시스템에는 전력 소비를 60% 줄여주는 장수명 LED가 채택되어 있어, 전력망에서 멀리 떨어진 진료소에서의 도입이 촉진되고 있습니다. 인공호흡 플랫폼에는 예측 알고리즘이 내장되어 있어, 기존의 경보 시스템보다 몇 분 더 빨리 호흡 곤란을 감지할 수 있으므로, 산소 포화도가 위험한 임계치까지 떨어지기 전에 의료진이 개입할 수 있게 됩니다.

산전·태아용 기기는 여전히 신생아 및 산전 진단 기기 시장의 매출에서 가장 큰 비중을 차지하고 있지만, 3차 의료기관에서의 보급률이 이미 높기 때문에 그 성장 속도는 완만합니다. GE 헬스케어의 ‘Voluson Signature’ 시리즈로 대표되는 AI 강화형 초음파 진단 장치는 진단 정확도를 저하시키지 않으면서 스캔부터 보고서를 작성하는 데 걸리는 시간을 최대 40% 단축합니다. 태아용 MRI는 초음파 검사 결과가 명확하지 않은 경우 중추신경계 이상을 발견하는 데 있어 그 역할이 확대되고 있으며, 규모는 작지만 고부가가치의 하위 시장을 형성하고 있습니다. 원격 태아 맥박 산소 측정기는 원격 의료 포털과 연동되어 산부인과 의사가 고위험 임신을 원격으로 모니터링할 수 있게 해줍니다. 이는 임산부의 2.3%가 산전 관리를 받지 못하는 지역에서 매우 귀중한 것입니다. 그러나 시장의 성숙과 병원 예산의 부족으로 인해 신생아 의료용 기기에 비해 성장세가 둔화되고 있으며, 공급업체들은 연구개발 자원을 산후 관리 분야에 집중하고 있습니다.

지역별 분석

북미는 2025년에 전 세계 매출의 36.88%를 차지했으며, 대규모 신생아 집중치료실(NICU)의 보급, 종합적인 민간 보험 적용 범위, 그리고 지속적인 혁신을 뒷받침하는 규제 환경의 지지를 받고 있습니다. 그러나 연간 2%의 출생률 감소라는 구조적인 역풍이 불고 있으며, 200곳 이상의 지방 병원이 분만실을 폐쇄함에 따라 대도시권 이외 지역에서의 접근성이 제한되고 있습니다. 캐나다의 단일 지불자 제도에서는 여전히 고가의 장비가 도입되고 있지만, 예산 제약으로 인해 교체 주기가 길어지고 있습니다. 멕시코의 사회보장 병원에서는 비용과 환자 중증도 증가 사이의 균형을 고려하여 중저가형 모니터를 도입하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.84%로 확대될 것으로 예상되며, 신생아 및 산전 진단 기기 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 중국만 해도 신생아 의료 인프라에 수십억 위안(人民元)을 투자하고 있는 반면, 인도의 생산 연계형 인센티브 제도로 인해 장비 조립이 국내로 이전되면서 입고 비용이 낮아지고 있습니다. 일본과 한국의 병원에서는 고령화되는 임상 인력을 관리하기 위해 AI 영상 진단을 도입하고 있으며, 출생률 증가세가 주춤함에도 불구하고 프리미엄 부문의 성장은 지속되고 있습니다. 인도네시아와 베트남을 포함한 동남아시아 국가들에서는 민관협력(PPP) 모델을 바탕으로 새로운 산모·신생아 병원이 개설되고 있으며, 기능과 가격의 균형이 잘 잡힌 중급 수준의 신생아 인큐베이터와 모니터가 수입되고 있습니다.

유럽에서는 의료기기 규정(MDR)의 시행 시한이 다가옴에 따라, 신규 사업 확대보다 규정 준수에 대한 투자가 우선시되고 있어, 진전은 보다 착실한 속도로 이루어지고 있습니다. 다만, 통일된 규정에 따라 AI 기반 소프트웨어의 EU 전역에서의 출시 절차가 간소화되었습니다. 중동 및 아프리카 및 남미는 여전히 개발도상국이지만, 모바일 우선 인프라 덕분에 유선 네트워크의 기존 비용을 부담하지 않고도 클라우드 연결 기기로 비약적으로 전환할 수 있어 전략적으로 중요한 지역입니다. 이 지역들에서는 휴대용 인큐베이터와 태양광 발전식 모니터에 대한 수요가 가장 높으며, 이는 절약형 혁신의 세계적 중요성이 입증되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the neonatal and prenatal devices market size is projected to expand from USD 8.36 billion in 2025 and USD 8.91 billion in 2026 to USD 12.19 billion by 2031, registering a CAGR of 6.47% between 2026 to 2031.

This report is Segmented by Product Type (Prenatal and Fetal Equipment, and Neonatal Equipment), Technology (Invasive Monitoring, and Non-Invasive Monitoring), End User (Hospitals, Maternity & Specialty Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Neonatal And Prenatal Devices Market Trends and Insights

Rising Incidence of Preterm Births

Persistently high preterm delivery rates keep the neonatal and prenatal devices market under structural demand pressure. United States data show 373,902 preterm births in 2023, and rates remain highest among Black infants at 14.7% and American Indian or Alaska Native infants at 12.4%. Multiple pregnancies, which are seven times more likely to be preterm than singleton pregnancies, amplify equipment needs as fertility treatments rise. Hospitals, therefore, accelerate investment in advanced incubators, ventilators, and predictive analytics that can flag sepsis or necrotizing enterocolitis earlier than manual observation. Together, these factors translate into steady volume for life-support devices even as overall birth totals plateau in developed economies.

Growth in High-Risk Pregnancy & Prenatal Screening Volumes

Maternal age is rising in most high-income nations, lifting the proportion of pregnancies classified as high-risk and fueling demand for sophisticated prenatal imaging. Women aged 40 and older experienced 14.6% preterm birth rates in 2023, well above the national average. AI-based ultrasound now detects 95% of neural tube defects, while machine-learning classification algorithms reach 71.5% diagnostic accuracy in test datasets. Clinical uptake accelerates because remote ultrasound reviews allow specialists to serve community clinics, closing the gap created by the fall in first-trimester prenatal care coverage to 76.1% in 2023. Wearable maternal monitors combine heart-rate, blood-oxygen, and activity sensors to manage smoking and gestational diabetes risks in real time. Digital care pathways reduce unnecessary in-person visits without compromising outcomes, lowering system costs, and encouraging payer reimbursement for connected prenatal devices.

Declining Birth Rates in Developed Economies

Global fertility is projected to slide to 1.83 by 2050 and 1.59 by 2010, well below the replacement rate, cutting the underlying volume addressable by the neonatal and prenatal devices market in the wealthiest countries. The United States reported a 2% birth decline and 3% drop in the general fertility rate during 2023. Maternity unit closures compound access problems; more than 200 rural hospitals shut labor-and-delivery services, leaving 2.3 million women in "maternity care deserts". Socioeconomic factors-delayed marriage, higher education, and childcare expenses-continue to suppress birth numbers, and policy incentives have shown only modest success in France, South Korea, and Singapore. Lower absolute births mean suppliers must pivot toward higher acuity equipment and ancillary home monitoring services to sustain revenue growth in developed regions.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of NICU Capacity in Emerging Markets

- AI-Enabled Remote Neonatal Monitoring Adoption in Home Settings

- High Capital Cost & Reimbursement Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Neonatal equipment revenue is expected to rise at a 9.53% CAGR through 2031, outstripping the prenatal and fetal category, even though prenatal devices held 62.88% of the neonatal and prenatal devices market in 2025. The neonatal and prenatal devices market size tied to incubators grows fastest because hospitals upgrade to portable, battery-powered units that cost a fraction of traditional models yet meet ISO temperature stability standards. Low-resource facilities in Bangladesh confront a 20,000-unit gap, and compact systems priced around GBP 250 reduce procurement barriers and stimulate government tenders. Phototherapy systems adopt longer-lasting LEDs that cut power consumption 60%, encouraging adoption in off-grid clinics. Ventilation platforms integrate predictive algorithms that flag respiratory distress minutes earlier than conventional alarms, which helps caregivers intervene before oxygen saturation drops to critical thresholds.

Prenatal and fetal equipment, while still the most significant contributor to the neonatal and prenatal devices market revenue, advances at a slower pace because penetration is already high among tertiary care centers. AI-enhanced ultrasound, typified by GE HealthCare's Voluson Signature line, reduces scan-to-report time by up to 40% without compromising diagnostic accuracy. Fetal MRI expands its role in central-nervous-system anomaly detection when ultrasound findings are inconclusive, creating a smaller but higher value subsegment. Remote fetal pulse oximeters link to telehealth portals so that obstetricians can watch high-risk pregnancies from afar, which is valuable in regions where 2.3% of mothers receive no prenatal care. However, market maturity and tightening hospital budgets temper growth relative to neonatology-focused devices, driving suppliers to focus R&D resources on postnatal applications.

Geography Analysis

North America commanded 36.88% of global revenue in 2025, anchored by large NICU footprints, robust private insurance coverage, and a regulatory environment that favors continuous innovation. Yet structural headwinds arise from a 2% annual birth decline, and more than 200 rural hospitals have shuttered labor wards, restricting access outside metro centers. Canada's single-payer model continues to buy premium equipment, but constrained budgets lengthen replacement cycles. Mexico's social-security hospitals adopt mid-range monitors as they balance cost and rising acuity.

Asia-Pacific is projected to expand at a 8.84% CAGR through 2031, making it the fastest-growing region within the neonatal and prenatal devices market. China alone commits billions of renminbi to neonatal infrastructure, while India's production-linked incentive scheme shifts device assembly onshore, lowering landed costs. Japanese and South Korean hospitals pursue AI imaging to manage aging clinical workforces, ensuring that premium segments continue to grow despite stagnant birth volumes. Southeast Asian nations, including Indonesia and Vietnam, open new maternal-child hospitals under public-private-partnership models, importing mid-tier incubators and monitors that balance feature sets with price.

Europe advances at a steadier clip as Medical Device Regulation deadlines prioritize compliance spending over green-field expansion, though unified rules simplify pan-EU launches for AI-driven software. Middle East and Africa, along with South America, remain nascent but strategically important because mobile-first infrastructure enables leapfrogging to cloud-connected devices without the legacy cost of wired networks. Portable incubators and solar-powered monitors see highest traction in these geographies, validating the global relevance of frugal innovation.

- GE Healthcare

- Koninklijke Philips

- Dragerwerk

- Atom Medical

- Natus Medical

- Getinge

- Masimo

- Medtronic

- Vyaire Medical

- Phoenix Medical Systems

- Fanem Ltda

- Fisher & Paykel Healthcare

- Siemens Healthineers

- Beckton Dickinson

- Smiths Group

- Hamilton Medical

- Mindray Bio-Medical Electronics

- Nihon Kohden

- Edward Lifesciences

- Butterfly Network, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Rising Incidence of Preterm Births

- 4.1.2 Growth in High-Risk Pregnancy & Prenatal Screening Volumes

- 4.1.3 Expansion of NICU Capacity in Emerging Markets

- 4.1.4 Government-Supported Universal Fetal Monitoring Programs

- 4.1.5 AI-Enabled Remote Neonatal Monitoring Adoption in Home Settings

- 4.1.6 Development of Low-Cost Portable Incubators for Off-Grid Clinics

- 4.2 Market Restraints

- 4.2.1 Declining Birth Rates in Developed Economies

- 4.2.2 High Capital Cost & Reimbursement Hurdles

- 4.2.3 Limited Skilled Neonatal Care Staff in Rural Hospitals

- 4.2.4 Supply-Chain Disruptions for Critical Electronic Components

- 4.3 Technological Outlook

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of Substitutes

- 4.4.4 Intensity of Competitive Rivalry

- 4.4.5 Threat of New Entrants

- 4.5 Regulatory Landscape

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Prenatal & Fetal Equipment

- 5.1.1.1 Ultrasound & Ultrasonography Devices

- 5.1.1.2 Fetal Doppler

- 5.1.1.3 Fetal MRI

- 5.1.1.4 Fetal Heart Monitors

- 5.1.1.5 Fetal Pulse Oximeters

- 5.1.1.6 Other Prenatal & Fetal Equipment

- 5.1.2 Neonatal Equipment

- 5.1.2.1 Incubators

- 5.1.2.2 Neonatal Monitoring Devices

- 5.1.2.3 Phototherapy Equipment

- 5.1.2.4 Respiratory Assistance & Monitoring Devices

- 5.1.2.5 Other Neonatal Care Equipment

- 5.1.1 Prenatal & Fetal Equipment

- 5.2 By Technology

- 5.2.1 Invasive Monitoring

- 5.2.2 Non-Invasive Monitoring

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Maternity & Specialty Clinics

- 5.3.3 Home & Remote Care Settings

- 5.3.4 Ambulatory Surgical Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 GE Healthcare

- 6.3.2 Koninklijke Philips NV

- 6.3.3 Dragerwerk AG & Co. KGaA

- 6.3.4 Atom Medical Corporation

- 6.3.5 Natus Medical Incorporated

- 6.3.6 Getinge AB

- 6.3.7 Masimo Corporation

- 6.3.8 Medtronic

- 6.3.9 Vyaire Medical

- 6.3.10 Phoenix Medical Systems Pvt. Ltd

- 6.3.11 Fanem Ltda

- 6.3.12 Fisher & Paykel Healthcare

- 6.3.13 Siemens Healthineers

- 6.3.14 Becton, Dickinson and Company

- 6.3.15 Smiths Medical (ICU Medical)

- 6.3.16 Hamilton Medical AG

- 6.3.17 Mindray Bio-Medical Electronics

- 6.3.18 Nihon Kohden Corporation

- 6.3.19 Edwards Lifesciences

- 6.3.20 Butterfly Network, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment