|

시장보고서

상품코드

2063691

헬스케어 분야 빅데이터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Big Data In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

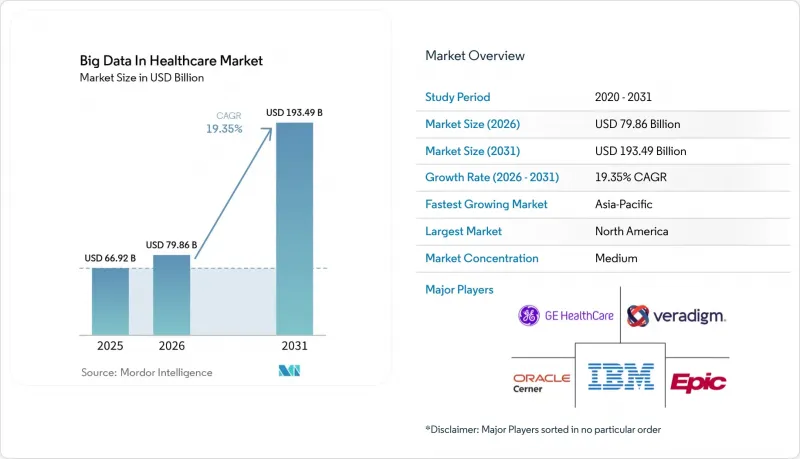

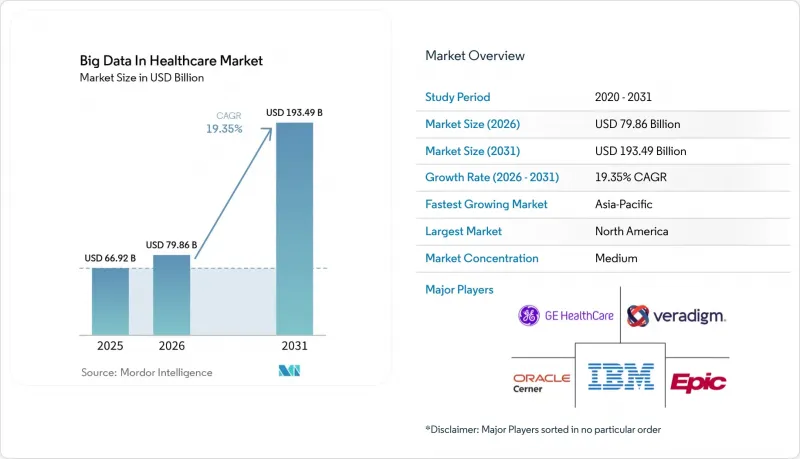

Mordor Intelligence에 의하면, 헬스케어 분야 빅데이터 시장 규모는 2025년 669억 2,000만 달러로 평가되었습니다. 2026년 798억 6,000만 달러에서 2031년까지 1,934억 9,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 19.35%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어, 서비스), 배포 방식(On-Premise, 클라우드), 분석 유형(기술적 분석, 예측 분석, 처방적 분석), 용도(재무 분석 등), 최종 사용자(의료 제공업체 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 헬스케어 분야 빅데이터 시장 동향 및 인사이트

집단 건강 관리용 분석 솔루션에 대한 수요 증가

집단 건강 전략에서는 위험을 예측하고 자원을 배분하기 위해 사회적 결정 요인과 임상 데이터를 결합하는 경향이 강해지고 있습니다. 고급 분석 기술을 도입한 의료 제공업체들은 재입원율을 낮추고 실질적인 비용 절감을 실현하고 있으며, 이는 2030년까지 모든 종량제 급여 수급자가 가치 기반 계약에 참여하도록 하겠다는 메디케어·메디케이드 서비스 센터(CMS)의 목표와 부합합니다. 리얼 월드 에비던스(RWE) 플랫폼은 보험 청구 데이터, 전자 건강 기록(EHR), 유전체 프로파일을 통합하여 조기 개입의 지침이 되는 개인 맞춤형 위험 점수를 산출합니다. 미국에서는 통합 의료 네트워크(IDN) 전반에 걸쳐 도입이 널리 진행되고 있으며, 유럽의 보험사들도 유럽 건강 데이터 전략(EHDS)의 목표 달성을 위해 유사한 도구를 활용하고 있습니다.

의료 관리 및 전략 최적화를 위한 비즈니스 인텔리전스의 필요성 증가

병원들은 이익률 압박과 관리 업무의 복잡화에 직면해 있습니다. 최신 비즈니스 인텔리전스 제품군은 수익 주기 지표와 운영 및 임상 지표를 통합하여 성과 격차를 실시간으로 시각화합니다. AI 기반 청구 거절 관리 모듈은 청구 데이터 수정을 자동화하여, 미국의 대규모 의료 시스템에서 평균 지급 기간을 단축함으로써 환자 치료에 투자할 자금을 확보하고 있습니다. 롤링 예측 및 시나리오 모델링은 경영진이 변동하는 상환율, 인력 부족, 공급망 혼란에 대응하는 데 도움이 됩니다. 여러 시설을 보유한 의료 시스템은 엔터프라이즈 대시보드를 통해 각 거점 간에 표준화할 수 있는 모범 사례를 시각화할 수 있기 때문에 가장 큰 혜택을 보고 있습니다.

기밀성이 높은 환자 의료 데이터와 관련된 보안상의 우려

2024년에는 3,100만 명 이상의 미국인이 의료 정보 유출 피해를 입었습니다. 2025년에 제안된 HIPAA 보안 개정안에서는 엄격한 자산 목록 및 사고 대응 계획의 수립이 의무화되어 있어, 분석 시스템 도입에 복잡성을 더하고 있습니다. 동형 암호화는 암호화된 데이터에 대한 연산을 가능하게 하지만, 지연이나 통합상의 장벽을 초래하여 프로젝트 진행을 늦추고 있습니다. 기관 간 공동 조사에서는 데이터 공유의 이점과 법적 위험 사이의 균형을 맞추는 데 어려움을 겪고 있으며, 일부 파트너는 공동 분석 이니셔티브의 범위를 축소하려는 경향을 보이고 있습니다.

부문별 분석

서비스 부문은 2025년에 헬스케어 분야 빅데이터 시장의 56.25%를 차지했으며, 기업들이 컨설팅, 통합 및 관리형 운영을 외부에 위탁함에 따라 연평균 성장률(CAGR) 21.45%를 나타낼 것으로 전망됩니다. 많은 의료 시스템에서는 데이터 거버넌스 및 보안에 관한 사내 전문 인력이 부족하기 때문에 클라우드 아키텍처 설계, 데이터 흐름 매핑, 그리고 규정 준수를 전문 업체에 위탁하고 있습니다. 또한, 서비스 부문은 플랫폼 유지보수와 성능 최적화를 결합한 다년 계약 형태의 관리형 분석 계약으로부터도 혜택을 보고 있습니다.

소프트웨어 시장 점유율은 낮지만, 플랫폼 공급업체는 서비스 파트너와 협력하여 도입을 가속화하고, 의료 제공업체가 가치를 실현하기까지 걸리는 시간을 단축하고 있습니다. 서비스 분야의 성장은 헬스케어 분야 빅데이터 시장에서 임상적 인사이트와 데이터 사이언스, 사이버 보안을 융합한 다분야에 걸친 팀이 필요함을 보여주고 있습니다. 의료 제공업체들은 재입원율 감소 및 수익 주기 개선과 컨설팅 비용을 연계하는 성과 기반 서비스 수준 계약을 협상하고 있습니다. 여러 병원에 걸쳐 진행되는 연합 학습(Federated Learning)과 같은 고급 활용 사례가 등장함에 따라, 전문적인 알고리즘 큐레이션 서비스에 대한 수요가 증가하고 있습니다.

2025년 기준 헬스케어 분야 빅데이터 시장 규모에서 On-Premise 도입이 60.95%를 차지했습니다. 이는 많은 의료 기관이 보호 대상인 의료 정보(PHI)에 대한 물리적 관리 권한을 유지하고 있었기 때문입니다. 그러나 각 하이퍼스케일러 기업들이 의료 전용 보안 도구 및 규정 준수 인증에 대한 투자를 확대함에 따라, 클라우드 도입은 2031년까지 연평균 성장률(CAGR) 23.95%로 확대될 것으로 전망됩니다. 의료 기관에서는 AI 및 고성능 컴퓨팅(HPC) 워크로드를 클라우드 클러스터로 이전하는 추세가 강해지고 있으며, 이를 통해 제공되는 탄력적인 확장 기능 덕분에 계산 부하가 높은 유전체 분석 및 영상 분석이 지원되고 있습니다.

클라우드의 보급은 설비 투자를 운영비로 전환하는 구독 모델로의 전환을 반영하고 있으며, 이는 예산에 제약이 있는 병원에게 매력적인 특징입니다. 마이크로소프트와 엔비디아는 의료 분야에 최적화된 턴키 AI 스택을 통해 협력하고 있으며, 의료 시스템이 모델 훈련을 보안이 확보된 데이터센터로 오프로드할 수 있도록 지원하고 있습니다. 대규모 이미지 아카이브가 여전히 로컬 이미지 아카이브 시스템에 존재하는 순환기내과나 영상의학과에서는 하이브리드 모델이 계속 유지되고 있지만, 데이터 계층화 정책에 따라 오래된 검사 데이터는 비용이 더 저렴한 클라우드 오브젝트 스토리지로 이전되고 있습니다.

지역별 분석

북미는 EHR 도입이 성숙 단계에 접어들었고 연방 정부의 상호운용성 정책에 힘입어, 2025년에도 45.10%의 점유율을 차지하며 최대 지역 시장으로 자리매김했습니다. 2024년 연방 FHIR 실행 계획안은 각 기관의 구현 가이드 표준화를 목표로 하며, 의료 제공업체, 보험사, 공중보건 기관 간의 원활한 데이터 흐름을 촉진하고 있습니다. 미국의 의료 시스템은 HIPAA 규정을 준수하면서 분석 기능을 현대화하기 위해 클라우드 공급업체를 활용하고 있습니다. 캐나다는 ‘인포웨이(Infoway)’ 이니셔티브를 통해 전국적인 의료 데이터 통합을 추진하고 있으며, 멕시코는 만성 질환의 부담을 관리하기 위해 디지털 역학에 투자하고 있습니다.

유럽도 이에 뒤를 따르고 있습니다. 유럽 헬스 데이터 스페이스(European Health Data Space)의 추진으로 활기를 띠고 있으며, 안전한 2차 데이터 활용을 가능하게 함으로써 향후 10년 동안 EU 전체에서 110억 유로(129억 달러)의 비용 절감이 예상됩니다. 독일의 ‘병원 미래법(Hospital Future Act)’에 따르면, 분석 기능 구축을 포함한 병원 IT 시스템 현대화에 40억 유로(47억 달러)가 배정되었습니다. 영국은 NHS 연합 데이터 플랫폼을 확장하여 트러스트(의료권) 간의 데이터 세트를 통합하고 있습니다. 프랑스, 이탈리아, 스페인은 AI 대응을 중시하는 전국적인 전자건강기록(EHR) 확대 정책을 시행하고 있습니다. 2028년까지 유럽 건강 데이터 공간(EHDS)은 조사 및 공중보건 프로그램을 가속화할 수 있는 국경을 초월한 데이터 공유 체계를 구축할 예정입니다.

아시아태평양은 헬스케어 분야 빅데이터 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지의 연평균 성장률(CAGR)은 20.10%로 전망됩니다. 중국은 각 성의 의료 정보 교환 시스템을 국가 인프라에 통합하여 공중보건 비상사태에 대한 예측 모델링을 지원하고 있습니다. 인도의 ‘아유슈만 바라트 디지털 미션’은 공공 및 민간 시설 전반에 걸쳐 환자 데이터를 연계하는 독자적인 건강 식별자를 확립했습니다. 일본은 급속한 고령화 사회에 대응하기 위해 AI를 활용한 고령자 돌봄 모니터링을 시범적으로 도입하고 있습니다. 호주는 제3자에 의한 분석 혁신을 촉진하기 위해 ‘My Health Record’의 API를 공개하고 있으며, 한국은 ‘Bio-Vision 2030’ 로드맵에 따라 클라우드 기반 유전체 분석에 자금을 지원하고 있습니다. 다양한 인구 구성과 질병 양상에 따라, 대도시터 외딴 섬에 이르기까지 대응할 수 있는 유연한 분석 프레임워크에 대한 수요가 생겨나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the big data in healthcare market size is projected to expand from USD 66.92 billion in 2025 and USD 79.86 billion in 2026 to USD 193.49 billion by 2031, registering a CAGR of 19.35% between 2026 to 2031.

This report is Segmented by Component (Software, Services), Deployment (On-Premise, Cloud), Analytics Type (Descriptive Analytics, Predictive Analytics, Prescriptive Analytics), Application (Financial Analytics, and More), End User (Healthcare Providers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Big Data In Healthcare Market Trends and Insights

Increase in Demand for Analytics Solutions for Population Health Management

Population health strategies increasingly combine social determinants with clinical data to predict risk and allocate resources. Providers deploying advanced analytics have lowered readmission rates and demonstrated material cost savings, aligning with the Centers for Medicare & Medicaid Services' target that all fee-for-service beneficiaries join value-based arrangements by 2030. Real-world evidence platforms merge claims, electronic health records, and genomic profiles to create individualized risk scores that guide early interventions. Uptake is widespread across integrated delivery networks in the United States, while European payers use similar tools to meet EHDS objectives.

Rising Need for Business Intelligence to Optimise Health Administration & Strategy

Hospitals face tight margins and growing administrative complexity. Modern business intelligence suites integrate revenue-cycle metrics with operational and clinical indicators to highlight performance gaps in real time. AI-based denial management modules automate claim edits and have shortened average payment windows for large US systems, freeing cash for patient care investments. Rolling forecasts and scenario modeling help executives navigate shifting reimbursement rates, workforce constraints, and supply chain disruptions. Multi-facility systems benefit the most because enterprise dashboards surface best practices that can be standardized across locations.

Security Concerns Related to Sensitive Patient Medical Data

More than 31 million Americans were affected by healthcare breaches in 2024. Proposed 2025 HIPAA security updates mandate rigorous asset inventories and incident response plans, adding complexity to analytics rollouts. Homomorphic encryption allows computation on encrypted data but introduces latency and integration hurdles that slow projects. Cross-institution research collaborations struggle to reconcile data-sharing benefits with legal exposure, leading some partners to narrow the scope of joint analytics initiatives.

Other drivers and restraints analyzed in the detailed report include:

- Mandates for Value-Based Care Reimbursement

- Expanding Adoption of Real-Time Remote-Patient-Monitoring Data Streams

- High Cost of Implementation and Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The services segment held 56.25% of the big data in healthcare market share in 2025 and is forecast to grow at 21.45% CAGR as organizations outsource consulting, integration, and managed operations. Many health systems lack internal skill sets in data governance and security, so they contract specialized vendors to design cloud architectures, map data flows, and ensure regulatory compliance. The services segment also benefits from multi-year managed analytics contracts that bundle platform maintenance with performance optimization.

Despite software's smaller share, platform vendors collaborate with service partners to accelerate deployments, improving time to value for providers. Growth in services underscores the big data in healthcare market's need for multidisciplinary teams that combine clinical insight with data science and cybersecurity. Providers negotiate outcome-based service level agreements that align consulting fees with readmission reductions or revenue-cycle improvements. As advanced use cases emerge, such as federated learning across multiple hospitals, demand for specialized algorithm-curation services is rising.

On-premise deployments accounted for 60.95% of the big data in healthcare market size in 2025 because many institutions retained physical control over protected health information. However, cloud deployments are projected to grow at 23.95% CAGR through 2031 as hyperscalers invest in healthcare-specific security tooling and compliance attestations. Providers increasingly migrate AI and high-performance computing workloads to cloud clusters where elastic scaling supports computationally intensive genomics and imaging analyses.

Cloud uptake also reflects the shift to subscription models that convert capital outlays into operating expenses, a feature attractive to budget-constrained hospitals. Microsoft and NVIDIA collaborate on turnkey AI stacks optimized for healthcare, encouraging health systems to offload model training to secure data centers. Hybrid models persist in cardiology and radiology departments where large imaging archives still reside on local picture archiving systems, yet data-tiering policies push older studies to cheaper cloud object storage.

Geography Analysis

North America remained the largest regional market with 45.10% share in 2025, supported by mature EHR adoption and federal interoperability policies. The 2024 Draft Federal FHIR Action Plan aims to standardize implementation guides across agencies, encouraging seamless data flow among providers, payers, and public health bodies. US health systems engage cloud vendors to modernize analytics while balancing HIPAA obligations. Canada advances national health data integration through its Infoway initiatives, and Mexico invests in digital epidemiology to manage chronic disease burdens.

Europe follows closely, energized by the European Health Data Space that is expected to save the bloc EUR 11 (USD 12.9) billion over ten years by enabling secure secondary data use. Germany's Hospital Future Act allocates EUR 4 (USD 4.7) billion to modernize hospital IT systems, including analytics readiness. The United Kingdom scales its NHS Federated Data Platform to unify datasets across trusts. France, Italy, and Spain implement national electronic health record expansion, emphasizing AI readiness. By 2028 the EHDS will create cross-border data-sharing pathways that accelerate research and population health programs.

Asia-Pacific is the fastest growing big data in healthcare market region, projected at a 20.10% CAGR through 2031. China integrates provincial health information exchanges into a national backbone that supports predictive modeling for public health emergencies. India's Ayushman Bharat Digital Mission establishes a unique health identifier that links patient data across public and private facilities. Japan pilots AI-driven eldercare monitoring as it contends with a rapidly aging population. Australia publishes My Health Record APIs to encourage third-party analytics innovations, and South Korea funds cloud-based genomic analysis under its Bio-Vision 2030 roadmap. Diverse demographics and disease profiles create demand for flexible analytics frameworks that can scale from megacities to remote islands.

- Veradigm Inc.

- Amazon Web Services Inc.

- Apixio Inc.

- Dell

- Epic Systems

- Exl Service

- Flatiron Health

- GE Healthcare

- Health Catalyst

- Health Fidelity

- Innovaccer

- IBM

- MedeAnalytics

- Optum

- Oracle

- Palantir Technologies Inc.

- Koninklijke Philips

- SAS Institute

- Siemens Healthineers

- Truven Health Analytics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Demand for Analytics Solutions for Population Health Management

- 4.2.2 Rising Need for Business Intelligence to Optimize Health Administration & Strategy

- 4.2.3 Mandates for Value-Based Care Reimbursement

- 4.2.4 Expanding Adoption of Real-Time Remote-Patient-Monitoring Data Streams

- 4.2.5 Integration of Multi-Omics Datasets into Clinical Decision Support

- 4.2.6 Emergence of Hospital-At-Home Models Generating Rich Home-Based Data

- 4.3 Market Restraints

- 4.3.1 Security Concerns Related to Sensitive Patient Medical Data

- 4.3.2 High Cost of Implementation and Deployment

- 4.3.3 Fragmented Data Standards Hindering Interoperability

- 4.3.4 Limited AI Explainability Raising Clinical-Liability Risk

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By Analytics Type

- 5.3.1 Descriptive Analytics

- 5.3.2 Predictive Analytics

- 5.3.3 Prescriptive Analytics

- 5.4 By Application

- 5.4.1 Financial Analytics

- 5.4.2 Clinical Data Analytics

- 5.4.3 Operational Analytics

- 5.4.4 Population Health Analytics

- 5.5 By End User

- 5.5.1 Healthcare Providers

- 5.5.2 Healthcare Payers

- 5.5.3 Pharma & Biotechnology Companies

- 5.5.4 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Veradigm Inc.

- 6.3.2 Amazon Web Services Inc.

- 6.3.3 Apixio Inc.

- 6.3.4 Dell Technologies Inc.

- 6.3.5 Epic Systems Corporation

- 6.3.6 ExlService Holdings Inc.

- 6.3.7 Flatiron Health

- 6.3.8 GE HealthCare

- 6.3.9 Health Catalyst Inc.

- 6.3.10 Health Fidelity Inc.

- 6.3.11 Innovaccer Inc.

- 6.3.12 International Business Machines Corporation (IBM)

- 6.3.13 MedeAnalytics Inc.

- 6.3.14 Optum Inc.

- 6.3.15 Oracle Corporation

- 6.3.16 Palantir Technologies Inc.

- 6.3.17 Philips Healthcare

- 6.3.18 SAS Institute Inc.

- 6.3.19 Siemens Healthineers AG

- 6.3.20 Truven Health Analytics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment