|

시장보고서

상품코드

2063699

스마트 매니지드 스위치 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Smart Managed Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

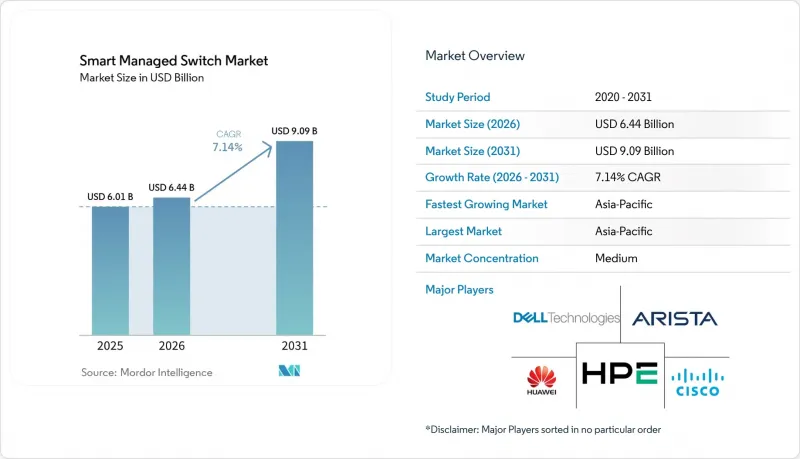

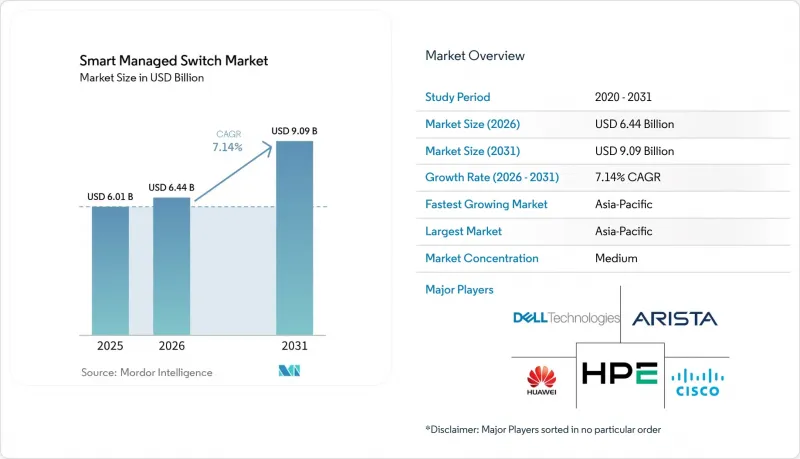

Mordor Intelligence에 의하면, 스마트 매니지드 스위치 시장 규모는 2025년 60억 1,000만 달러로 평가되었습니다. 2026년에는 64억 4,000만 달러로 확대되어 2031년까지 90억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 7.14%를 나타낼 전망입니다.

본 보고서는 포트 속도(기가비트 이더넷(10/100/1000 Mbps), 10기가비트 이더넷, 기타), 포트 수(2-8포트, 9-24포트, 기타), 관리 방식(클라우드 네이티브, On-Premise 네이티브, 기타), 최종 사용자 산업 규모(중소기업, 기타), 최종 사용자 산업(IT 및 통신, 소매, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 스마트 매니지드 스위치 시장 동향 및 인사이트

디스크리트 산업 및 공정 산업에서의 인더스트리 4.0 도입

디지털 트윈이나 예측 유지보수를 도입하는 제조업체들은 마이크로초 수준의 동기화를 저해하지 않으면서 결정론적인 트래픽 분리를 구현할 것을 네트워크 설계자들에게 요구하고 있습니다. 인도의 생산 연계형 인센티브(PLI) 프로그램은 전자기기 제조에 1조 4,600억 루피(197억 달러)를 배정하고, 네이티브 PROFINET, EtherNet/IP 및 OPC UA를 지원하는 매니지드 스위치를 필수로 하는 공장 투자를 촉진하고 있습니다. 록웰 오토메이션의 Stratix 시리즈는 Cisco IOS와 디바이스 레벨의 이중화 기능을 결합하여, 산업용 벤더가 엔터프라이즈 스위칭과 공장 현장의 내결함성을 어떻게 융합하고 있는지를 보여줍니다. 피닉스 콘택트의 IEC TS 60079-47 인증을 획득한 Ethernet-APL 스위치는 관리형 이더넷을 폭발 위험 구역 내 1km까지 확장하여 기존의 필드버스 게이트웨이를 불필요하게 만듭니다. 공장이 사후 대응형 유지보수에서 상태 모니터링형 유지보수로 전환되는 가운데, 비관리형 장치는 고주파수 센서 텔레메트리 처리량 및 세분화 요건을 충족할 수 없습니다.

PoE 지원 에지 디바이스의 보급

Wi-Fi 7 액세스 포인트는 포트당 47-51와트를 소비하기 때문에 PoE+에서 IEEE 802.3bt 하드웨어로 업그레이드해야 합니다. Wi-Fi 7은 2025년 3분기 기업용 AP 출하량의 31.1%를 차지했으며, 2028년까지 90%를 넘어설 것으로 전망됩니다. TP-Link의 Omada SG3218XP-M2는 2.5기가비트 이더넷 포트 16개를 갖추고 있으며, 240와트의 전력 공급 능력을 보유하고 있어, 중견 기업 구매자들이 고가의 가격 부담 없이 멀티기가비트 업링크를 확보할 수 있는 방법을 제시하고 있습니다. 무선 외에도 IP 감시 카메라와 엣지 AI 박스는 이더넷을 통해 전력과 데이터를 통합함으로써 배선을 줄일 수 있는 반면, 스위치에 열 부하가 집중됩니다. 개별 인젝터를 사용하지 않음으로써 절감되는 인건비는 도입 대수가 12대를 초과할 경우 15-20%의 하드웨어 비용 증가분을 상쇄합니다.

높은 초기 설비 투자(CapEx) : 비관리형 제품과의 비교

매니지드 스위치는 동급의 비매니지드 제품보다 40-60% 더 비쌉니다. 예를 들어, NETGEAR의 GS728TXUP의 정가는 1,552.49파운드(1,970달러)이지만, 비관리형 제품의 가격은 800달러 미만이며, 단일 지점 사용자의 경우 투자 회수 기간이 36개월을 초과합니다. AI 가속기에 대한 수요가 웨이퍼 생산 능력을 압박하고 있어, 부품 부족과 긴급 조달에 따른 할증 요금이 비용을 더욱 끌어올리고 있습니다. 신흥 지역의 가격에 민감한 구매자들은 초기 투자 비용을 절감하기 위해 하드웨어 수준의 QoS를 희생하고, 비관리형 하드웨어에 소프트웨어 오버레이를 결합한 방식을 종종 도입하고 있습니다.

부문별 분석

기가비트 이더넷용 스마트 매니지드 스위치 시장 규모가 전반적인 수요를 주도하고 있지만, 25/40 기가비트 옵션은 두 자릿수 성장률을 기록하며 확대되고 있습니다. 하이퍼스케일러들은 하나의 섀시에 800기가비트 이더넷 포트 576개를 탑재한 Arista의 7800R4 섀시에 주목하고 있습니다. 화웨이의 수냉식 51.2 Tbps 스위치는 열 부하를 절반으로 줄여, 캐비닛당 8대를 설치할 수 있게 해줍니다. 중규모 데이터센터에서는 여전히 10기가비트가 주류를 이루고 있지만, 가격 경쟁력이 있는 25기가비트 NIC의 등장으로 인해 오버구독으로 인한 문제는 완화되고 있습니다. GPU 워크로드에는 저지연 패브릭이 필요하기 때문에 100기가비트 이상의 플랫폼용 스마트 관리형 스위치 시장 점유율이 상승하고 있으며, 이러한 추세는 2025년 2분기 출하 대수가 3배로 증가한 사실로 입증되고 있습니다.

용도의 성장에 따라, 대역폭을 점진적으로 확장하는 것만으로는 더 이상 따라잡을 수 없게 되어, 리프레시 주기가 단축되고 있습니다. Ultra Ethernet Consortium의 무손실 기능 강화는 표준의 분열을 초래할 가능성이 있지만, AI 클러스터에서 결정론적 성능에 대한 수요를 부각시키고 있습니다. 각 벤더사는 외부 탭 없이 마이크로 버스트의 가시성을 제공하는 프로그래밍 가능한 ASIC 텔레메트리 파이프라인을 통해 차별화를 꾀하고 있습니다.

고정 포트 수가 9-24개인 모델은 지사 등의 요구를 충족시키고 있지만, Wi-Fi 7에서는 액세스 포인트 1대당 스위치 포트 1개가 필수이기 때문에 25-48포트 스마트 매니지드 스위치 시장 규모가 가장 빠르게 확대되고 있습니다. 익스트림 네트웍스의 4000 시리즈는 포트 수준에서 범용 ZTNA를 통합하여, 병원이나 은행이 스위치 자체에서 트래픽을 마이크로 부문화할 수 있도록 지원합니다.

피닉스 컨택트의 FL SWITCH 2608과 같은 견고한 2-8포트 유닛은 공간이 제한된 산업용 인클로저에 적합하며, 50-80%의 가격 프리미엄이 책정되어 있습니다. 48포트를 초과하는 규모의 경우, 가동 중인 라인 카드 업그레이드로 인해 추가 비용을 정당화할 수 있으므로 모듈형 섀시가 주류를 이루고 있습니다. 여러 유닛을 단일 관리 도메인으로 통합하는 인스턴트 스태킹은 펌웨어 관리 지점을 줄여주며, IT 팀이 수백 개의 통신실을 모니터링할 때 큰 이점을 제공합니다.

지역별 분석

아시아태평양은 2025년 매출의 3분의 1 이상을 창출하며, 지역별로는 가장 높은 연평균 성장률(CAGR)을 보였습니다. 1조 4,600억 루피(197억 달러) 규모의 인센티브에 힘입은 인도의 스마트 팩토리 구상이 OT-IT 융합 스위칭에 대한 수요를 견인하고 있습니다. 선전, 싱가포르, 시드니에서 화웨이가 ‘Xinghe AI Fabric 2.0’을 선보인 것은 하이퍼스케일화의 추세를 뒷받침하고 있습니다.

북미와 유럽에서는 판매 대수 증가세가 완만하지만, EU 규정 2023/826이 대기 전력을 2-7와트로 제한함에 따라 규정 준수를 위한 제품 교체가 이루어지고 있습니다. 중동 및 아프리카에서는 사우디아라비아의 HUMAIN 캠퍼스 등, 400기가비트 지원 패브릭을 지정하는 프로젝트가 소버린 클라우드 의무화를 호재로 삼고 있습니다.

남미에서는 Tecto사의 포르투알레그레에서 진행 중인 2억 레알(3,720만 달러) 규모의 건설 프로젝트를 포함해, 600억 달러 규모의 AI 데이터센터 설비 투자 혜택을 누리고 있습니다. 조달에 있어 우선순위는 지역에 따라 다릅니다. 서유럽 바이어들은 수십 년에 걸친 지원을 중시하여 다소 비싼 가격을 지불하는 반면, 아시아 고객들은 40-60%의 비용 절감을 실현하기 위해 신흥 공급업체와 거래할 때 수반되는 위험을 감수하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the smart managed switch market size is expected to increase from USD 6.01 billion in 2025 to USD 6.44 billion in 2026 and reach USD 9.09 billion by 2031, growing at a CAGR of 7.14% over 2026-2031.

This report is Segmented by Port Speed (Gigabit Ethernet [10/100/1000 Mbps], 10 Gigabit Ethernet, and More), Port Count (2-8 Ports, 9-24 Ports, and More), Management Method (Cloud-Native, On-Prem Native, and More), End-User Industry Size (Small and Medium Enterprises, and More), End-User Industry (IT and Telecom, Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Managed Switch Market Trends and Insights

Industry 4.0 Adoption in Discrete and Process Industries

Manufacturers embracing digital twins and predictive maintenance push network designers to enforce deterministic traffic segregation without sacrificing microsecond-level synchronization. India's Production-Linked Incentive program earmarked INR 1.46 trillion (USD 19.7 billion) to electronics manufacturing, catalyzing factory investments that mandate managed switches with native PROFINET, EtherNet/IP, and OPC UA support. Rockwell Automation's Stratix series blends Cisco IOS with Device Level Ring redundancy, showing how industrial vendors meld enterprise switching with plant-floor resilience. Phoenix Contact's Ethernet-APL switch, certified to IEC TS 60079-47, extends managed Ethernet 1 km into explosive zones, eliminating legacy fieldbus gateways. As factories migrate from reactive to condition-based maintenance, unmanaged devices fail to meet the throughput and segmentation demands of high-frequency sensor telemetry.

Proliferation of PoE-Enabled Edge Devices

Wi-Fi 7 access points consume 47-51 watts per port, forcing upgrades from PoE+ to IEEE 802.3bt hardware. Wi-Fi 7 accounted for 31.1% of enterprise AP shipments in Q3 2025 and will surpass 90% by 2028. TP-Link's Omada SG3218XP-M2 provides 16 ports of 2.5 Gigabit Ethernet and a 240-watt budget, showing how mid-market buyers secure multi-gigabit uplinks without premium pricing. Beyond wireless, IP surveillance cameras and edge AI boxes consolidate power and data over Ethernet, reducing cabling yet concentrating thermal load at the switch. Labor savings from avoiding separate injectors offset the 15-20% hardware premium once deployments exceed 12 endpoints.

High Initial CapEx Versus Unmanaged Alternatives

Managed switches cost 40-60% more than unmanaged equivalents. For example, NETGEAR's GS728TXUP lists at GBP 1,552.49 (USD 1,970) versus sub-USD 800 unmanaged peers, extending payback beyond 36 months for single-site users. Component shortages and expedited sourcing premiums inflate bills further as AI accelerator demand diverts wafer capacity. Price-sensitive buyers in emerging regions often deploy unmanaged hardware plus software overlays, trading hardware-level QoS for lower capital outlays.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Cloud-Managed Networking Platforms

- AI-Driven Intent-Based Switching for SMB Networks

- Skilled Workforce Shortage for Advanced Network Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Smart Managed Switch market size for Gigabit Ethernet led overall demand, yet 25/40 Gigabit options are accelerating at a double-digit clip. Hyperscalers gravitate to Arista's 7800R4 chassis, packing 576 ports of 800 Gigabit Ethernet in one frame. Huawei's liquid-cooled 51.2 Tbps switch halves thermal overhead, enabling eight units per cabinet. While 10 Gigabit remains prevalent in mid-tier data centers, price-parity 25 Gigabit NICs shrink oversubscription headaches. The Smart Managed Switch market share of 100 Gigabit and above platforms is rising as GPU workloads require low-latency fabrics, a trend underscored by shipments tripling in Q2 2025.

Refresh cycles compress because incremental bandwidth bumps can no longer match application growth. The Ultra Ethernet Consortium's lossless enhancements may splinter standards, but they underline demand for deterministic performance in AI clusters. Vendors differentiate through programmable ASIC telemetry pipelines that expose microburst visibility without external taps.

Fixed 9-24-port models satisfy branch offices, yet the Smart Managed Switch market size for 25-48-port devices is climbing fastest as Wi-Fi 7 mandates one switch port per access point. Extreme Networks' 4000 Series bundles Universal ZTNA at the port level, letting hospitals and banks micro-segment traffic on the switch itself.

Ruggedized 2-8-port units such as Phoenix Contact's FL SWITCH 2608 address tight industrial enclosures, commanding 50-80% price premiums. Above 48 ports, modular chassis prevail where in-service line-card upgrades justify higher cost. Instant stacking that collapses multiple units into one management domain reduces firmware touchpoints, a compelling benefit when IT teams supervise hundreds of closets.

Geography Analysis

Asia-Pacific generated over one-third of 2025 revenue and will post the fastest regional CAGR. India's smart factory initiatives, backed by INR 1.46 trillion (USD 19.7 billion) of incentives, push demand for converged OT-IT switching. Huawei's Xinghe AI Fabric 2.0 rollout in Shenzhen, Singapore, and Sydney underscores hyperscale momentum.

North America and Europe exhibit slower unit growth but trigger compliance-driven refreshes as EU Regulation 2023/826 caps standby power at 2-7 watts. The Middle East and Africa ride sovereign cloud mandates, with projects such as Saudi Arabia's HUMAIN campus specifying 400-Gigabit-ready fabrics.

South America benefits from USD 60 billion in AI data center capex, including Tecto's BRL 200 million (USD 37.2 million) Porto Alegre build. Procurement priorities diverge: Western buyers pay premiums for multi-decade support, whereas Asian customers accept emerging-vendor risk for 40-60% price savings.

- Cisco Systems Inc.

- Hewlett Packard Enterprise Company

- Juniper Networks Inc.

- Arista Networks Inc.

- Dell Technologies Inc.

- Extreme Networks Inc.

- Netgear Inc.

- TP-Link Technologies Co. Ltd.

- D-Link Corporation

- Ubiquiti Inc.

- Huawei Technologies Co. Ltd.

- ZTE Corporation

- Moxa Inc.

- Advantech Co. Ltd.

- Belden Inc.

- Phoenix Contact GmbH & Co. KG

- Siemens AG

- Rockwell Automation Inc.

- Schneider Electric SE

- ABB Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industry 4.0 Adoption in Discrete and Process Industries

- 4.2.2 Proliferation of PoE-Enabled Edge Devices

- 4.2.3 Rapid Expansion of Cloud-Managed Networking Platforms

- 4.2.4 AI-Driven Intent-Based Switching for SMB Networks

- 4.2.5 Wi-Fi 7 Multi-Gigabit Access Layer Upgrades

- 4.2.6 Energy-Efficiency Mandates and Incentives for ICT Equipment

- 4.3 Market Restraints

- 4.3.1 High Initial Capex Versus Unmanaged Alternatives

- 4.3.2 Skilled Workforce Shortage for Advanced Network Management

- 4.3.3 Semiconductor Supply-Chain Volatility

- 4.3.4 Vendor Lock-in from Proprietary Cloud Portals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Port Speed

- 5.1.1 Gigabit Ethernet (10/100/1000 Mbps)

- 5.1.2 10 Gigabit Ethernet

- 5.1.3 25/40 Gigabit Ethernet

- 5.1.4 100 Gigabit and Above

- 5.2 By Port Count

- 5.2.1 2-8 Ports

- 5.2.2 9-24 Ports

- 5.2.3 25-48 Ports

- 5.2.4 Above 48 Ports

- 5.3 By Management Method

- 5.3.1 Cloud-native

- 5.3.2 On-prem native

- 5.3.3 Hybrid

- 5.4 By End-User Industry Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End-User Industry

- 5.5.1 IT and Telecom

- 5.5.2 Healthcare

- 5.5.3 Retail

- 5.5.4 Government

- 5.5.5 Education

- 5.5.6 Other End-User industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Hewlett Packard Enterprise Company

- 6.4.3 Juniper Networks Inc.

- 6.4.4 Arista Networks Inc.

- 6.4.5 Dell Technologies Inc.

- 6.4.6 Extreme Networks Inc.

- 6.4.7 Netgear Inc.

- 6.4.8 TP-Link Technologies Co. Ltd.

- 6.4.9 D-Link Corporation

- 6.4.10 Ubiquiti Inc.

- 6.4.11 Huawei Technologies Co. Ltd.

- 6.4.12 ZTE Corporation

- 6.4.13 Moxa Inc.

- 6.4.14 Advantech Co. Ltd.

- 6.4.15 Belden Inc.

- 6.4.16 Phoenix Contact GmbH & Co. KG

- 6.4.17 Siemens AG

- 6.4.18 Rockwell Automation Inc.

- 6.4.19 Schneider Electric SE

- 6.4.20 ABB Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment