|

시장보고서

상품코드

2063726

만성 림프구성 백혈병 치료제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Chronic Lymphocytic Leukemia Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

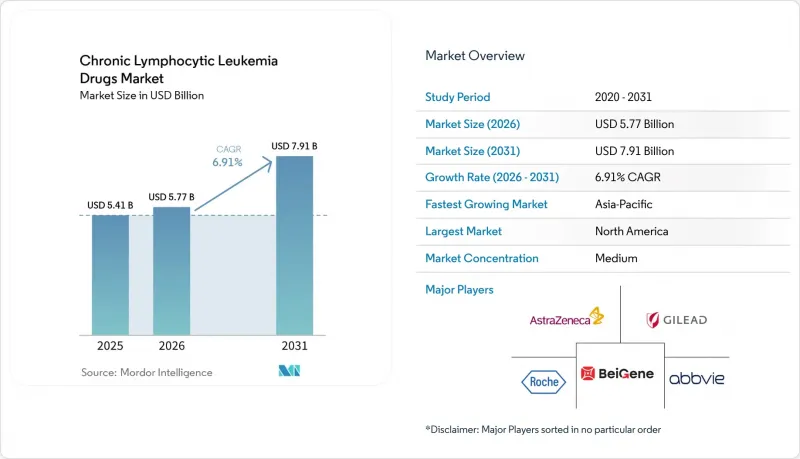

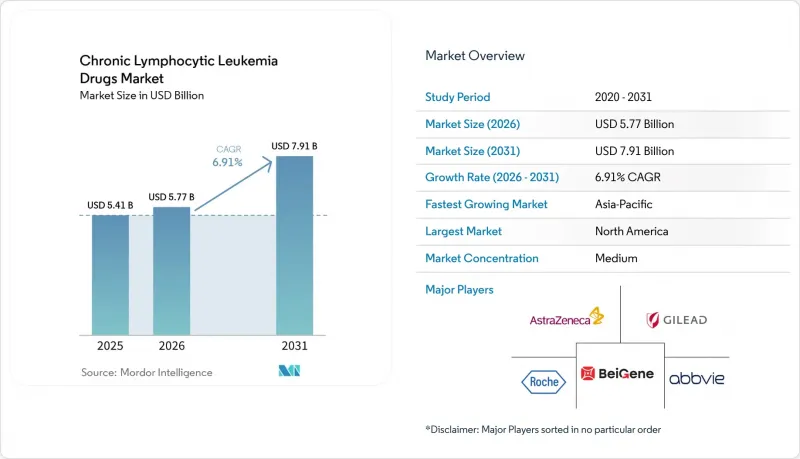

Mordor Intelligence에 의하면, 만성 림프구성 백혈병 치료제 시장 규모는 2025년에 54억 1,000만 달러, 2026년에 57억 7,000만 달러, 2031년까지 79억 1,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 6.91%로 성장할 것으로 전망됩니다.

본 보고서는 투여 경로(경구, 비경구, 기타), 치료법(표적 치료, 화학 요법, 면역 요법 등), 약물 분류(BTK 억제제, BCL-2 억제제 등), 치료 단계(1차 치료, 2차 치료 등), 유통 채널(병원, 전문 클리닉 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 만성 림프구성 백혈병 치료제 시장 동향 및 인사이트

전 세계 CLL 유병률 증가와 급속한 고령화

세계 확진자 수는 계속 증가하고 있으며, 2025년에는 미국에서 2만 3,690건의 신규 확진 사례가 발생할 것으로 예측됩니다. 진단 시 중앙값이 70세인 점을 고려할 때, 이 질환은 고령화 사회와 밀접한 관련이 있으며, 생존율이 89%를 초과함에 따라 CLL은 수십 년에 걸친 관리가 필요한 만성 질환입니다. 한때 발병률이 낮았던 아시아 국가들에서도, 선별 검사의 개선과 인구 구조의 고령화에 따라 현재는 더욱 급속한 증가세가 나타나고 있습니다. 이러한 역학적 경향에 따라 표적 치료제나 병용 요법의 대상이 되는 환자층이 확대되면서, 만성 림프구성 백혈병 치료제 시장은 성장하고 있습니다.

차세대 BTK, BCL-2, PI3K 억제제 파이프라인 확대

필트부르티닙 등의 비공유 결합형 BTK 억제제는 BTK 억제제 치료 경험이 있는 환자에서 81.6%의 반응률을 보인 반면, 손로토크라크스 등의 차세대 BCL-2 억제제는 자누부르티닙과의 병용 요법을 통해 97%의 반응률을 보였습니다. 현재 연구가 진행 중인 BTK 분해제는 억제가 아닌 새로운 제거 기전을 도입하고 있습니다. 규제 당국은 브레이크스루 프로그램 및 패스트트랙 프로그램을 통해 이러한 후보 약물의 승인 절차를 가속화하고 있으며, 이로 인해 개발 기간이 단축되면서 만성 림프구성 백혈병 치료제 시장의 경쟁이 치열해지고 있습니다.

특허를 취득한 신약 및 병용 요법의 높은 비용

CAR-T 치료의 환자 1인당 비용이 100만 달러에 육박한다는 점은 가장 부유한 의료 제도를 제외하고는 모든 제도에서 보험 적용의 과제가 되고 있습니다. 또한, 고정 기간의 2제 병용 요법의 경우에도 2020년대 후반 특허 만료 시까지 제네릭 의약품으로 전환할 수 없는 경우, 예산에 부담을 줄 가능성이 있습니다. 가치 기반 계약에 관한 협상은 여전히 고르지 못한 상태이며, 가격에 민감한 지역의 접근이 지연되면서 세계 성장 곡선의 일부가 둔화되고 있습니다.

부문별 분석

경구용 제제는 2025년 만성 림프구성 백혈병 치료제 시장 점유율의 61.65%를 차지하고 있으며, 이는 환자들의 재택 투여 선호도와 의료기관의 비용 절감에 대한 지불 주체의 관심을 반영하고 있습니다. 메디케어 파트 D의 적용 범위 확대와 2025년 본인부담 상한액 도입으로 인해 미국 내 사용이 촉진되는 한편, 일본과 독일에서도 아카라부티닙 및 자누부티닙의 승인 이후 경구용 제제의 도입이 가속화되고 있는 것으로 보고되고 있습니다. 경구용 BTK 및 BCL-2 억제제가 이러한 증가세를 뒷받침하고 있으며, 새로운 1일 1회 투여 제제와 전적으로 경구로 투여되는 병용 요법이 이러한 추세를 더욱 공고히 하고 있습니다. CD20 항체의 경우, 특히 도입 요법 단계에서는 비경구 투여법이 여전히 중요하지만, 그 상대적 중요성은 계속해서 감소하고 있습니다. 앞으로 피하 투여형 CD20 치료제나 경구용 PI3K 후보 약물이 사용 경향을 더욱 변화시킬 가능성이 있습니다. 만성 림프구성 백혈병 치료제 시장에서 경구용 제품 시장 규모는 2031년까지 연평균 성장률(CAGR) 9.18%로 확대될 것으로 예상되며, 이는 시장 전체의 성장률을 상회하여 경구 투여가 혁신의 주요 플랫폼으로서의 입지를 공고히할 것으로 보입니다.

종양 용해 위험이 높은 경우, 입원 환자에 대한 베네토클락스 투여 확대에 있어 병원 내 투여가 여전히 일정한 비중을 차지하고 있지만, 지침 개정과 원격의료 도구의 보급으로 인해 현재는 외래 치료나 완전한 원격 치료 프로토콜도 가능해졌습니다. 이러한 유연성은 보험사에게 매력적이며, 복잡한 세포 치료를 위한 병상을 확보함으로써 병원에서 재택 치료로의 전환 추세를 뒷받침하고 있습니다. 이처럼 경구용 제제는 복약 순응도를 높이고, 지방 지역의 접근성을 확대하며, 만성 림프구성 백혈병 치료제 시장의 지리적 확장을 뒷받침하고 있습니다. 이에 대응하여 제약사는 복약 일정을 간소화하는 환자 지원 프로그램과 블리스터 포장을 도입함으로써, 다양한 헬스케어 환경에서 제품의 보급을 더욱 촉진하고 있습니다.

표적 치료가 매출의 대부분을 차지하며, 2025년에는 48.92%를 나타낼 것으로 예측됩니다. 이는 BTK 및 BCL-2 억제제가 기존의 화학면역요법을 대체했기 때문입니다. 영국에서 진행된 FLAIR 임상시험의 5년간 데이터는 FCR과 비교했을 때 이부르티닙·베네토클락스가 더 우수한 무진행 생존 기간(PFS)을 보인다는 사실을 입증하고 있으며, 이는 전 세계 지침의 개정을 가속화하고 있습니다. 세포 치료 시장은 기저 수준이 낮고, BTK 및 BCL-2 억제제 모두에 반응하지 않은 환자를 대상으로 한 최초의 리소카브타제네 마랄루셀(lisocabtagene maraleucel)의 승인을 발판으로 연평균 성장률(CAGR) 10.44%를 기록하며 성장할 것으로 전망됩니다. 이 결과는 새로운 치료 경로를 개척하고, CAR-T 플랫폼을 보다 광범위한 조기 치료 단계에서 평가할 수 있는 기반을 마련했으나, 제조 과정의 복잡성과 비용은 여전히 걸림돌로 남아 있습니다.

CD20 항체를 이용한 면역요법은 여전히 핵심적인 역할을 담당하고 있으며, 특히 오비누츠주맙은 베네토클락스와의 시너지 효과를 통해 MRD 검출률 90% 이상을 달성하는 고정 기간 요법을 실현하고 있습니다. 화학요법의 적응증은 특정 세포유전학적 프로파일이나 자원이 제한된 환경으로 점차 좁혀지고 있습니다. 진단 기술의 발전과 더불어 이러한 진전에 힘입어, 만성 림프구성 백혈병(CLL) 치료제 시장은 기존의 장기 유지 요법 패러다임에서 벗어나, 치료 효과의 깊이와 무치료 기간을 더욱 중시하는 정밀하고 치료 성과 중심의 치료 모델로 지속적으로 전환되고 있습니다.

지역별 분석

북미는 FDA의 조기 승인, 성숙한 보험 적용, 그리고 혈액학 센터의 긴밀한 네트워크에 힘입어 계속해서 전 세계 매출의 38.12%를 차지하고 있습니다. 2025년에 도입될 메디케어의 2,000달러 상한제 덕분에 경구용 약물의 비용 대비 효과가 현저히 향상되었으며, MD 앤더슨 등 여러 학술 기관들이 실제 임상 현장에서의 보급을 가속화할 주요 임상시험을 주도하고 있습니다. 캐나다 역시 주 차원의 보상 제도의 지원을 받아, 유사한 진료 양상을 보이고 있습니다. 한편, 멕시코에서는 진료 지침의 통일과 조달 절차의 정비가 가속화되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.05%를 기록하며 가장 높은 성장세를 보일 것으로 전망됩니다. 일본에서는 2024년에 아카라부르티닙이 1차 치료제로 승인되고, 중국에서는 자누부르티닙이 다중 적응증 승인을 받아, 고령화가 진행되고 있는 양국의 인구에게 최신 치료 옵션이 제공될 것입니다. 중국의 혁신적인 기업들은 BCL-2 및 BTK를 표적으로 하는 파이프라인을 확대하고, 세계적 기준을 재정의할 가능성이 있는 경쟁력 있는 가격 책정을 시도하고 있습니다. 호주와 한국은 기간 한정의 베네토클락스 병용 요법을 신속하게 보험 적용한 반면, 인도는 비용 절감을 위해 유세포 분석기의 처리 능력을 확대하고 현지 생산 가능성을 모색하고 있습니다.

유럽에서는 EMA(유럽의약품청)의 중앙 심사 절차와, 지불 주체에 의한 심사를 효율화하는 공동 임상 평가 시범 사업을 통해 꾸준한 진전을 이어가고 있습니다. 독일과 영국에서는 이미 MRD(잔존 병변)에 기반한 치료 중단 기준이 도입되어 있으며, 기간 제한이 있는 치료 요법이 경제적으로 유리한 선택지로 자리 잡아가고 있습니다. 바이오시밀러는 CD20 표적 치료제의 비용을 절감하고, 보다 폭넓은 병용 요법을 가능하게 하고 있습니다. 중동 및 아프리카에서는 진단 지원 보조금 및 다국적 기업과의 제휴를 통해 검사 시설이 갖춰지고 있지만, 여전히 높은 정가가 걸림돌로 작용하고 있습니다. 남미에서는 브라질과 아르헨티나를 중심으로 민간 보험의 확대와 국가 처방집의 개정을 통해 의료 접근성이 점차 개선되고 있지만, 환율 변동이 절대적인 성장을 저해하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the chronic lymphocytic leukemia drugs market size is projected to be USD 5.41 billion in 2025, USD 5.77 billion in 2026, and reach USD 7.91 billion by 2031, growing at a CAGR of 6.91% from 2026 to 2031.

This report is Segmented by Route of Administration (Oral, Parenteral, and Others), Therapy Type (Targeted Therapy, Chemotherapy, Immunotherapy, and More), Drug Class (BTK Inhibitors, BCL-2 Inhibitors and More), Line of Therapy (First-Line, Second-Line and More), Distribution Channel (Hospitals, Specialty Clinics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Chronic Lymphocytic Leukemia Drugs Market Trends and Insights

Rise in Global CLL Prevalence and Rapidly Ageing Population

Worldwide diagnoses continue to climb, with 23,690 new US cases expected in 2025. The median diagnosis age of 70 aligns the disease with aging societies, and survival exceeding 89% turns CLL into a chronic condition that requires decades of management. Asian nations, once showing lower incidence, now report faster growth as screening improves and demographic profiles tilt older. These epidemiologic patterns enlarge the chronic lymphocytic leukemia drugs market by widening the pool of patients eligible for targeted agents and combination regimens.

Expanding Pipeline of Next-Gen BTK, BCL-2 and PI3K Inhibitors

Non-covalent BTK molecules, such as pirtobrutinib, post 81.6% responses in BTK-experienced patients, while next-generation BCL-2 assets, like sonrotoclax, post 97% responses when paired with zanubrutinib. BTK degraders, now under investigation, introduce a new removal mechanism rather than inhibition. Regulators accelerate these candidates through breakthrough and fast-track programs, compressing timelines and intensifying competition within the chronic lymphocytic leukemia drugs market.

High Cost of Patented Novel Agents and Combination Regimens

CAR-T therapy pricing near USD 1 million per patient challenges reimbursement in all but the wealthiest systems. Fixed-duration doublets can also strain budgets where generic substitutions are unavailable until late-decade patent cliffs. Negotiations over value-based contracts remain uneven, delaying access in price-sensitive regions and tempering part of the global growth curve.

Other drivers and restraints analyzed in the detailed report include:

- Improved Diagnostic Accuracy Via Flow-Cytometry and NGS Panels

- Favourable Reimbursement for Oral Targeted Therapies

- Grade ≥3 Adverse Events Driving Early Discontinuations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oral agents held 61.65% of the 2025 chronic lymphocytic leukemia drugs market share, reflecting patient preference for home dosing and payer interest in reduced facility bills. Broader Medicare Part D coverage and the 2025 copay cap reinforce utilisation in the United States, while Japan and Germany also report faster oral uptake post-approval of acalabrutinib and zanubrutinib. Oral BTK and BCL-2 inhibitors underpin this rise, and new once-daily or all-oral combinations further consolidate the trend. Parenteral regimens remain critical for CD20 antibodies, particularly during induction phases; however, their relative importance continues to decline. Looking ahead, subcutaneous CD20 products and oral PI3K candidates may further tilt usage. The chronic lymphocytic leukemia drugs market size for oral products is forecast to rise at a 9.18% CAGR through 2031, outpacing overall growth and cementing oral delivery as the primary platform for innovation.

Hospital administration keeps a foothold for inpatient venetoclax ramp-ups when tumor-lysis risk is high, but updated guidelines and telehealth tools now allow day-clinic or fully remote protocols. That flexibility attracts payers and frees capacity for complex cellular therapies, reinforcing the hospital-to-home migration trend. Oral agents thus improve adherence and widen access in rural areas, supporting the chronic lymphocytic leukemia drugs market's geographic expansion. Manufacturers respond with patient-support programs and blister packaging that simplify dosing schedules, further enhancing uptake across diverse healthcare settings.

Targeted therapy dominated revenue, accounting for 48.92% in 2025, as BTK and BCL-2 inhibitors displaced conventional chemoimmunotherapy. Five-year data from the U.K. FLAIR study confirm superior progression-free survival for ibrutinib-venetoclax over FCR, accelerating global guideline revisions. Cellular therapy, despite a low base, is projected to expand at a 10.44% CAGR, buoyed by the first-in-class approval of lisocabtagene maraleucel for patients failing both BTK and BCL-2 inhibitors. This result creates a rescue pathway and positions CAR-T platforms for broader earlier-line evaluations, though manufacturing complexity and cost remain hurdles.

Immunotherapy with CD20 antibodies retains an anchoring role, especially obinutuzumab, whose synergy with venetoclax delivers fixed-duration regimens that achieve undetectable MRD rates above 90%. The relevance of chemotherapy narrows to select cytogenetic profiles or resource-limited settings. Combined with diagnostic advances, these developments continue to shift the chronic lymphocytic leukemia drugs market toward precision, outcome-driven care models, where depth of response and treatment-free interval carry greater weight than classical long-term maintenance paradigms.

Geography Analysis

North America continues to control 38.12% of global revenue, underpinned by early FDA clearances, mature insurance coverage and dense networks of haematology centres. The 2025 USD 2,000 Medicare cap markedly improves affordability of oral agents, and multiple academic hubs such as MD Anderson lead pivotal trials that hasten real-world uptake. Canada follows similar practice patterns, supported by provincial reimbursement, while Mexico accelerates guideline harmonisation and procurement pathways.

Asia-Pacific is set to log the fastest 9.05% CAGR through 2031. Japan's 2024 first-line acalabrutinib approval and China's multi-indication green light for zanubrutinib supply large ageing populations with modern options. Chinese innovators expand BCL-2 and BTK pipelines and test competitive pricing that may reshape global benchmarks. Australia and South Korea rapidly reimburse fixed-duration venetoclax doublets, while India scales flow-cytometry capacity and explores local manufacture to temper cost.

Europe maintains steady advance through the EMA's centralised pathway and joint clinical-assessment pilots that streamline payer reviews. Germany and the United Kingdom already implement MRD-guided stop rules, reinforcing time-limited regimens as economic winners. Biosimilars cut CD20 costs, enabling broader combination use. In the Middle East and Africa, diagnostic grants and multinational partnerships build testing labs, yet high list prices remain a hurdle. South America, led by Brazil and Argentina, improves access slowly through private insurance expansion and updated national formularies, but currency volatility tempers absolute growth.

- Abbvie

- AstraZeneca

- BeiGene

- Roche

- Gilead Sciences

- Novartis

- Eli Lilly and Company

- Secura Bio

- Sanofi

- Ono Pharmaceutical

- Teva Pharmaceutical Industries

- Incyte

- Astellas Pharma

- Genmab / AbbVie

- Adaptive Biotechnologies

- Merck Co & Inc

- TG Therapeutics

- Bristol-Myers Squibb

- Juno Therapeutics (BMS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise In Global CLL Prevalence & Rapidly Ageing Population

- 4.2.2 Expanding Pipeline Of Next-Gen BTK, BCL-2 & PI3K Inhibitors

- 4.2.3 Improved Diagnostic Accuracy Via Flow-Cytometry & NGS Panels

- 4.2.4 Favourable Reimbursement For Oral Targeted Therapies In US & EU-5

- 4.2.5 Growing Off-Label Use Of Minimal-Residual-Disease (MRD) Testing To Shorten Therapy Duration

- 4.2.6 Hospital-To-Home Shift Enabling Outpatient Venetoclax Ramp-Up Protocols

- 4.3 Market Restraints

- 4.3.1 High Cost Of Patented Novel Agents & Combination Regimens

- 4.3.2 Grade >=3 Adverse Events Driving Early Discontinuations

- 4.3.3 Emerging BTK-Inhibitor Resistance Mutations (E.G., L528W) Eroding Long-Term Efficacy

- 4.3.4 Supply-Chain Bottlenecks For Specialised Cytometry Reagents In LMICs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Route of Administration

- 5.1.1 Oral

- 5.1.2 Parenteral

- 5.1.3 Others

- 5.2 By Therapy Type

- 5.2.1 Targeted Therapy

- 5.2.2 Chemotherapy

- 5.2.3 Immunotherapy (mAbs & BsAbs)

- 5.2.4 CAR-T & Cell Therapy

- 5.2.5 Combination Regimens

- 5.3 By Drug Class

- 5.3.1 BTK Inhibitors

- 5.3.2 BCL-2 Inhibitors

- 5.3.3 PI3K Inhibitors

- 5.3.4 CD20 mAbs

- 5.3.5 Cytotoxic Agents

- 5.3.6 Others

- 5.4 By Line of Therapy

- 5.4.1 First-Line

- 5.4.2 Second-Line

- 5.4.3 Relapsed / Refractory

- 5.5 By Distribution Channel

- 5.5.1 Hospitals

- 5.5.2 Speciality Clinics

- 5.5.3 Online & Retail Pharmacies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AbbVie

- 6.3.2 AstraZeneca

- 6.3.3 BeiGene

- 6.3.4 F. Hoffmann-La Roche

- 6.3.5 Gilead Sciences

- 6.3.6 Novartis

- 6.3.7 Eli Lilly

- 6.3.8 Secura Bio

- 6.3.9 Sanofi

- 6.3.10 Ono Pharmaceutical

- 6.3.11 Teva Pharmaceutical

- 6.3.12 Incyte

- 6.3.13 Astellas Pharma

- 6.3.14 Genmab / AbbVie

- 6.3.15 Adaptive Biotechnologies

- 6.3.16 Merck Co & Inc

- 6.3.17 TG Therapeutics

- 6.3.18 Bristol Myers Squibb

- 6.3.19 Juno Therapeutics (BMS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

(주말 및 공휴일 제외)