|

시장보고서

상품코드

2063729

그람 양성 감염증 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Gram-Positive Bacterial Infections Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

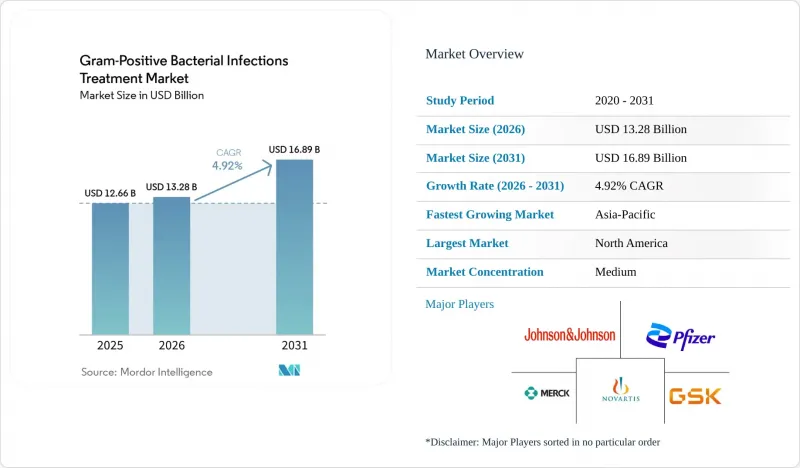

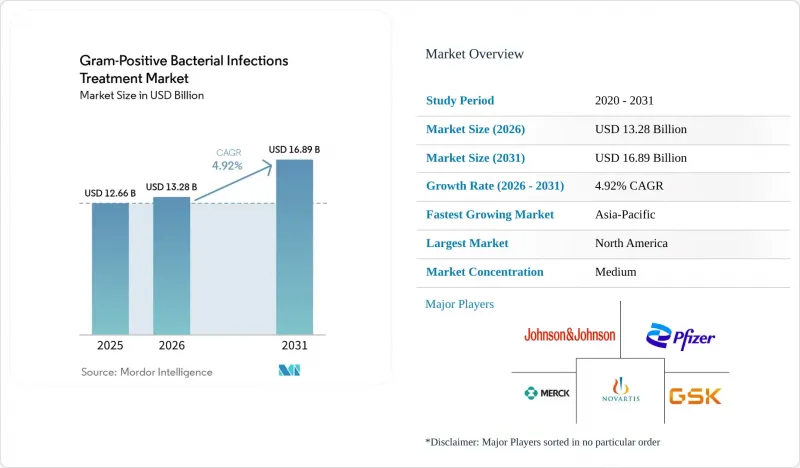

Mordor Intelligence에 의하면, 그람 양성 감염증 치료 시장 규모는 2025년 126억 6,000만 달러, 2026년 132억 8,000만 달러에서 2031년까지 168억 9,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 4.92%를 나타낼 것으로 예측됩니다.

본 보고서는 약제의 유형(β-락탐계 항생제, 세팔로스포린계, 플루오로퀴놀론계 등), 질환(폐렴, 패혈증, MRSA 감염증 등), 유통 채널(병원 약국, 소매 약국, 온라인 약국), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 그람 양성 감염증 치료 시장 동향 및 인사이트

그람 양성 감염증의 유병률 증가

의료 관련 감염증의 발생률은 여전히 높은 수준을 유지하고 있으며, MRSA만 해도 연간 12만 1,000명의 항생제 내성 관련 사망자가 보고되고 있습니다. 현재 병원에서는 고위험 입원 환자를 대상으로 88분 이내에 93.3%의 검출 정확도를 달성하는 PCR 패널을 활용한 선별 검사를 실시하고 있으며, 이를 통해 임상의는 표적 치료를 더 조기에 시작할 수 있고, 광범위 항생제는 확실히 필요한 경우에만 사용할 수 있게 되었습니다. 고령화에 따라 암 치료나 장기 이식을 받고 있는 면역결핍 환자 수가 증가하고 있으며, 이는 그람 양성에 대한 효과적인 치료제에 대한 수요를 더욱 높이고 있습니다. 새로운 내성 요소를 지닌 초강독성 균주는 스튜어드십의 시급성을 더욱 부각시키고 있지만, 그 중 상당수는 현재 그람 음성균에 영향을 미치고 있습니다. 이러한 동향들이 복합적으로 작용하여 옥사졸리디논계, 리포펩타이드계 및 신세대 세팔로스포린계의 기본 사용률을 끌어올리고 있습니다.

승인된 의약품 수 증가와 파이프라인의 진전

2024년부터 2025년까지, 미국 FDA는 MRSA 균혈증 및 급성 피부 감염증의 치료제로 세프토비프로를 승인했습니다. 이 약은 균혈증 시험에서 68.9%의 성공률을 기록했습니다. 게포치다신은 수십년만에 토포이소메라제 억제형 항생제로서 우선심사(Priority Review) 대상이 되었습니다. 한편, 콘테졸리드는 리네졸리드보다 혈액학적 부작용이 적다는 이유로 중국에서 승인되었습니다. WHO의 집계에 따르면, 임상 개발 단계에 있는 항균제 후보는 97건이며, 그중 32건이 우선순위 병원체를 표적으로 하고 있습니다. QIDP(우선 개발 제품) 및 패스트트랙(신속 심사) 제도를 통한 인센티브는 독점권을 연장하고, 개발 위험을 부분적으로 상쇄하는 동시에 그람 양성 감염증 시장에 대한 신규 자본 유입을 촉진하고 있습니다. 이러한 규제 측면에서의 추세가 예측 기간 동안 꾸준한 신약 출시 속도를 뒷받침하고 있습니다.

그람 양성 병원체에서 항생제 내성의 확산

리네졸리드 내성은 현재 23S rRNA의 변이 및 cfr 유전자의 획득을 통해 여러 지역에서 확인되고 있으며, 이로 인해 치료 기간이 단축되고 치료 성공률이 낮아지고 있습니다. 캄보디아의 감시 조사 결과, 2023년에 광범위 내성 임질균(Neisseria gonorrhoeae) 분리주가 12.5%를 기록했으며, 이는 사용 빈도가 낮은 환경에서도 내성 형질이 얼마나 빠르게 확산되는지를 여실히 보여주고 있습니다. 전 세계 항생제 소비량은 2016년부터 2023년 사이에 16.3% 증가했으며, 이대로 방치할 경우 2030년까지 52.3% 증가할 것으로 예상되어 선택압이 가속화되고 있습니다. 이러한 경향은 현재의 파이프라인을 위협하는 것이므로, 예방, 진단 및 새로운 작용기전에 대한 동시 투자가 요구되고 있습니다.

부문별 분석

세팔로스포린계 항생제는 광범위한 임상적 사용과 외과적 예방 지침에 포함된 점을 배경으로, 2025년 그람 양성 감염 치료 시장에서 24.20%의 점유율을 차지했습니다. MRSA 균혈증 치료제인 세프토비프로롤에 대한 FDA 승인은 고가 제품군의 매출을 이끌어내며, 세팔로스포린계 항생제의 견실한 수익성을 뒷받침하고 있습니다. 그러나 적정 사용 지침과 일부 지역에서 세팔로스포린계 항생제 내성이 증가함에 따라 장기적인 성장이 억제되고 있습니다. 리네졸리드를 필두로 하는 옥사졸리디논 계열은 2031년까지 연평균 성장률(CAGR) 9.26%를 기록하며 가장 빠른 성장세를 보였습니다. 중국에서 콘테졸리드의 승인 및 테지졸리드 유사 약물의 유망한 3상 임상시험 데이터에 힘입어, 안전성에 대한 인식이 높아지면서 처방 의사들의 신뢰도도 확산되고 있습니다. 달바반신 등의 장시간 작용형 리포펩타이드는 외래 정맥 주사 요법에서 특화된 유용성을 지니고 있으나, 1회 투여 비용이 높은 점을 상쇄하기 위해서는 보험 급여 제도의 정비에 의존하고 있습니다. 글리코펩타이드계 항생제는 반코마이신 내성 장구균으로 인한 지속적인 위협에 직면해 있습니다. 이에 대해 각 제약사는 신독성 위험을 줄이고 임상적 유용성을 장기화시키는 용량 최적화 제제로 대응하고 있습니다. 파이프라인 단계의 병용 요법, 예를 들어 β-락탐계 항생제와 β-락타마제 억제제의 조합은 주로 그람 음성균을 대상으로 하지만, 교차 표적화의 가능성으로 인해 혼합 감염에서의 적용 범위가 확대될 가능성이 있습니다. 백신 개발의 진전, 특히 B군 연쇄상구균에 대한 백신의 경우, 현재 장기간의 정맥 내 치료가 필요한 감염증을 예방함으로써 수요를 점차 회복시킬 가능성이 있습니다.

지역별 분석

북미는 조기 규제 승인, 높은 진단 보급률, 그리고 광범위한 보험 적용에 힘입어 2025년에는 전 세계 매출의 38.40%를 차지했습니다. EQUIP-A-Pharma 이니셔티브는 국내 리네졸리드의 3D 프린팅 생산 능력을 확대하여 공급 탄력성을 강화하는 동시에, 운송에 따른 배출량을 줄이고 있습니다. 캐나다 당국은 현재 제조업체에 공급 부족 대비 계획을 제출하고 안전 재고를 확보하도록 의무화하고 있으며, 이러한 조치들은 병원 구매 담당자들의 예측 가능성을 높여주고 있습니다. 멕시코는 니어쇼어링의 동향과, 주요 원자재의 리드타임을 단축하는 USMCA(미국·멕시코·캐나다 협정)에 따른 무역 경로 합리화의 혜택을 누리고 있습니다. 그러나 항생제 적정 사용에 대한 집행이 여전히 단편적인 수준에 머물러 있어, 일부 지역에서는 여전히 경험적 치료로서 다제 병용 요법이 권장되고 있습니다.

유럽은 일관된 AMR(항생제 내성) 정책 체계를 통해 여전히 큰 점유율을 유지하고 있습니다. 제안된 ‘중요 의약품법’은 공동 조달을 조정하여, 소규모 회원국도 가격 급등을 초래하지 않으면서 신약에 접근할 수 있도록 합니다. ECDC(유럽질병예방통제센터)의 감시 데이터는 광범위 항생제 소비량이 내성균의 진화와 밀접한 관련이 있음을 뒷받침하고 있으며, 이에 따라 협범위 항생제의 적정 사용을 장려하는 성과 연계형 보상 모델이 강화되고 있습니다. 서유럽 시장에서는 개발 중인 후보 약물에 대한 선구매 계약이 확보된 반면, 동유럽에서는 보험 급여 지연으로 인해 도입이 더딘 양상을 보이고 있습니다. 지역을 아우르는 임상 학회는 바이오마커에 기반한 투여 개시 및 신속한 투약 단계 하향을 중시하는 응급실용 지침을 발표함으로써, 서로 다른 의료 제도 간의 진료 패턴을 통일하고 있습니다.

아시아태평양은 보편적 의료 보장(UHC) 제도의 확대와 국내 혁신 파이프라인에 힘입어 2031년까지 연평균 성장률(CAGR) 7.78%라는 가장 높은 성장률을 기록하고 있습니다. 싱가포르는 박테리오파지 및 항균 펩타이드 분야의 스타트업을 육성하며, 중개 연구 허브로서의 입지를 확고히 하고 있습니다. 중국 국가의약품감독관리국은 카리미신과 콘테졸리드를 승인함으로써 규제 당국의 유연성과 강화되는 혁신 역량을 보여주었습니다. 일본은 3세대 세팔로스포린의 소비량을 대폭 줄였으나, MRSA로 인한 부담은 여전히 크며, 고가 의약품에 대한 수요가 지속되고 있습니다. 인도는 브랜드 의약품인 옥사졸리디논 계열 약물에 대한 접근을 제한하는 가격 격차에 직면해 있으며, 국내 공급이 불안정할 때에는 제네릭 의약품으로의 전환이나 병행 수입이 촉진되고 있습니다. 호주에서는 재고 보유 의무와 공급업체에 대한 가격 인상 덕분에, 긴 공급망에도 불구하고 안정적인 공급이 유지되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the gram-Positive bacterial infections treatment market size is projected to expand from USD 12.66 billion in 2025 and USD 13.28 billion in 2026 to USD 16.89 billion by 2031, registering a CAGR of 4.92% between 2026 to 2031.

This report is Segmented by Drug Type (Beta-Lactam Antimicrobials, Cephalosporins, Fluoroquinolones, and More), Disease (Pneumonia, Sepsis, MRSA Infections, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Gram-Positive Bacterial Infections Treatment Market Trends and Insights

Rising Prevalence of Gram-Positive Infections

Healthcare-associated infections remain stubbornly high, and MRSA alone represented 121,000 AMR-related deaths annually. Hospitals now screen high-risk admissions with PCR panels that deliver 93.3% detection accuracy within 88 minutes, allowing clinicians to start targeted therapy sooner and reserve broad-spectrum agents for confirmed need. Aging populations enlarge the pool of immunocompromised patients undergoing cancer therapy or organ transplantation, further boosting demand for effective gram-positive coverage. Hypervirulent strains with novel resistance elements add urgency to stewardship, although most currently affect gram-negative pathogens. Collectively, these dynamics lift baseline utilization of oxazolidinones, lipopeptides, and new-generation cephalosporins.

Increasing Number of Drug Approvals & Pipeline Progression

Between 2024 and 2025, the U.S. FDA cleared ceftobiprole for the treatment of MRSA bacteremia and acute skin infections, achieving a 68.9% success rate in bacteremia trials. Gepotidacin secured Priority Review as the first topoisomerase-inhibiting antibiotic in decades, while contezolid earned approval in China with fewer hematologic adverse events than linezolid. WHO counts 97 antibacterial candidates in clinical development, 32 of which target priority pathogens. QIDP and Fast-Track incentives extend exclusivity, partially offsetting development risk and attracting new capital into the market for gram-positive bacterial infections. This regulatory momentum underpins a steady launch cadence through the forecast period.

Escalating Antibiotic Resistance Among Gram-Positive Pathogens

Linezolid resistance now appears in multiple regions via 23S rRNA mutation and cfr gene uptake, curbing therapy length and success. Cambodia's surveillance logged 12.5% extensively drug-resistant Neisseria gonorrhoeae isolates in 2023, underscoring how resistance traits spread quickly even in lower-use settings. Global antibiotic consumption climbed 16.3% between 2016 and 2023, with forecasts of 52.3% growth by 2030 if unchecked, accelerating selection pressure. These patterns threaten current pipelines and require simultaneous investment in prevention, diagnostics, and novel mechanisms.

Other drivers and restraints analyzed in the detailed report include:

- Growing Healthcare Expenditure In Emerging Economies

- Adoption Of Rapid Molecular Diagnostics Enabling Targeted Therapy

- Patent Expiries Driving Generic Erosion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cephalosporins held 24.20% of the gram-positive bacterial infections treatment market share in 2025, anchored by broad empirical use and inclusion in surgical prophylaxis guidelines. FDA approval of ceftobiprole for MRSA bacteremia adds premium-priced volume and supports cephalosporin revenue resilience; however, stewardship directives and growing cephalosporin resistance in some geographies moderate long-term growth. Oxazolidinones, led by linezolid, posted the fastest expansion, with a 9.26% CAGR projected through 2031. Contezolid's approval in China and promising Phase 3 data for tedizolid-analogue agents enhance safety perceptions and widen prescriber comfort. Long-acting lipopeptides such as dalbavancin hold niche utility for outpatient parenteral therapy but rely on reimbursement alignment to offset high single-dose prices. Glycopeptides face sustained pressure from vancomycin-resistant enterococci; developers respond with dosing-optimized formulations that lower nephrotoxicity risk and prolong clinical relevance. Pipeline-stage combination agents, for example, beta-lactam plus B-lactamase inhibitor pairings, mainly target gram-negative organisms, yet cross-labeling potential may expand coverage in mixed infections. Vaccinology advances, particularly against Group B Streptococcus, could gradually reshape demand by preventing infections that currently require prolonged intravenous treatment.

Geography Analysis

North America commanded 38.40% of global revenue in 2025, propelled by early regulatory approvals, high diagnostic penetration, and broad insurance coverage. The EQUIP-A-Pharma initiative adds domestic 3D-printed linezolid capacity, fortifying supply resilience while lowering transportation emissions. Canadian authorities now oblige manufacturers to file shortage-risk plans and hold safety stocks, steps that enhance predictability for hospital buyers. Mexico benefits from near-shoring trends and streamlined USMCA trade lanes that shorten lead times for critical inputs. However, fragmented stewardship enforcement still encourages empiric multi-drug regimens in some regions.

Europe preserves a sizeable share through cohesive AMR policy frameworks. The proposed Critical Medicines Act coordinates joint procurement, ensuring smaller member states can access novel agents without price inflation. Surveillance data from ECDC confirm that broad-spectrum consumption tracks resistance evolution closely, reinforcing pay-for-performance models that reward narrow-spectrum adherence. Western European markets secure advance-purchase agreements for pipeline candidates, whereas Eastern Europe faces reimbursement delays that slow uptake. Pan-regional clinical societies publish emergency-department guidelines emphasizing biomarker-guided initiation and rapid de-escalation, harmonizing practice patterns across disparate health systems.

Asia-Pacific registers the fastest growth at a 7.78% CAGR to 2031, buoyed by expanding universal health coverage schemes and domestic innovation pipelines. Singapore incubates bacteriophage and antimicrobial-peptide startups, positioning itself as a translational hub. China's National Medical Products Administration approved carrimycin and contezolid, demonstrating regulatory agility and rising innovation capacity. Japan achieved sizable consumption cuts for third-generation cephalosporins, yet the MRSA burden remains high, sustaining premium agent demand. India contends with affordability gaps that limit access to branded oxazolidinones, encouraging generic substitution and parallel importation when domestic supply falters. Australia's stockholding mandate and supplier price uplifts underpin stable supplies despite long supply chains.

- Abbvie

- AstraZeneca

- Basilea Pharmaceutica Ltd.

- Bayer

- Bristol-Myers Squibb

- Cumberland Pharmaceuticals

- Dr Reddy's Laboratories Ltd.

- Fresenius

- GlaxoSmithKline

- Hikma Pharmaceuticals

- Johnson & Johnson

- Lupin

- Melinta Therapeutics

- Merck

- Novartis

- Paratek Pharmaceuticals

- Pfizer

- Sanofi

- Shionogi & Co. Ltd.

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Gram-Positive Infections

- 4.2.2 Surge in Drug Approvals & Advancements in Pipeline

- 4.2.3 Escalating Healthcare Spending in Developing Nations

- 4.2.4 Embrace of Rapid Molecular Diagnostics for Targeted Treatments

- 4.2.5 Revival of Older Narrow-Spectrum Antibiotics Through Stewardship Initiatives

- 4.2.6 Government Subscription Models & Pull-Incentives

- 4.3 Market Restraints

- 4.3.1 Growing Antibiotic Resistance in Gram-Positive Pathogens

- 4.3.2 Patent Expirations Leading to Generic Erosion

- 4.3.3 Strict Antimicrobial Stewardship Curtailing Broad-Spectrum Usage

- 4.3.4 Vulnerable API Supply Chains for Specialized Gram-Positive Agents

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Drug Type

- 5.1.1 Beta-Lactam Antimicrobials

- 5.1.2 Cephalosporins

- 5.1.3 Penicillins

- 5.1.4 Fluoroquinolones

- 5.1.5 Lipopeptides

- 5.1.6 Oxazolidinones

- 5.1.7 Glycopeptides

- 5.1.8 Vaccines

- 5.1.9 Combination Therapies & More

- 5.2 By Disease

- 5.2.1 Pneumonia

- 5.2.2 Sepsis

- 5.2.3 Pharyngitis

- 5.2.4 MRSA Infections

- 5.2.5 Endocarditis

- 5.2.6 Meningitis

- 5.2.7 Other Diseases

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 AstraZeneca plc

- 6.3.3 Basilea Pharmaceutica Ltd.

- 6.3.4 Bayer AG

- 6.3.5 Bristol-Myers Squibb Co.

- 6.3.6 Cumberland Pharmaceuticals

- 6.3.7 Dr Reddy's Laboratories Ltd.

- 6.3.8 Fresenius Kabi AG

- 6.3.9 GSK plc

- 6.3.10 Hikma Pharmaceuticals plc

- 6.3.11 Johnson & Johnson (Janssen)

- 6.3.12 Lupin Ltd.

- 6.3.13 Melinta Therapeutics

- 6.3.14 Merck & Co. Inc.

- 6.3.15 Novartis AG

- 6.3.16 Paratek Pharmaceuticals

- 6.3.17 Pfizer Inc.

- 6.3.18 Sanofi SA

- 6.3.19 Shionogi & Co. Ltd.

- 6.3.20 Sun Pharmaceutical Industries Ltd.

- 6.3.21 Teva Pharmaceutical Industries Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment