|

시장보고서

상품코드

2063752

교육 분야 HCM 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)HCM Software In Education - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

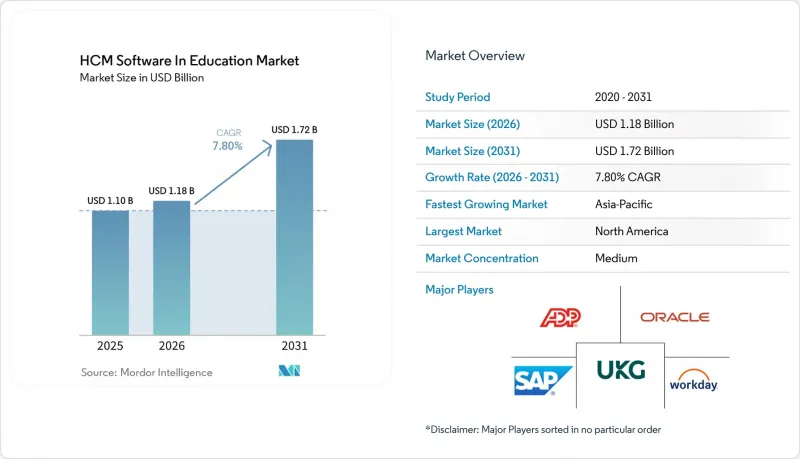

Mordor Intelligence에 의하면, 교육 분야 HCM 소프트웨어 시장 규모는 2025년에 11억 달러, 2026년에 11억 8,000만 달러, 2031년까지 17억 2,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 7.8%로 성장할 것으로 전망됩니다.

본 보고서는 도입 모델(클라우드 및 On-Premise), 솔루션(핵심 HR, 인재 관리, 인력 관리, 급여 계산, 학습 및 개발), 교육 기관 유형(K-12 학교, 커뮤니티 칼리지, 대학, 직업·기술 전문학교), 최종 사용자(교직원 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 교육 분야 HCM 소프트웨어 시장 동향 및 인사이트

대학 내 클라우드 우선 전략의 확대

대학에서는 데이터센터 비용을 절감하고 원격지에 있는 교직원의 접근을 지원하기 위해 급여 계산, 복리후생, 채용 업무를 클라우드 솔루션으로의 전환을 가속화하고 있습니다. 이러한 전환 움직임은 2024년 이후, 하이브리드 수업과 멀티 캠퍼스 모델로 인해 고정형 인프라의 한계가 드러나면서 더욱 탄력을 받았습니다. 현재 각 인터넷 서비스 제공업체들은 복잡한 전환에 수반되는 위험을 줄이기 위한 데이터 변환 도구, 샌드박스, 관리형 서비스를 패키지로 제공합니다. 또한, 클라우드 버전에서는 분기별로 새로운 기능이 출시되므로, 교육 기관은 장기간에 걸친 업그레이드 프로젝트를 진행하지 않고도 분석 기능이나 모바일 셀프 서비스를 도입할 수 있습니다. 워크데이는 2026년도 결산 보고서에서 대규모 공립 대학이 기존의 ERP 시스템군을 통합형 클라우드 제품군으로 교체함에 따라 교육 부문의 수주액이 두 자릿수 성장률을 기록했다고 밝혔습니다. 그 결과, 교육 분야 HCM 소프트웨어 시장에서 On-Premise에서 클라우드 구독 모델로의 워크로드 전환이 꾸준히 진행되고 있습니다. 맞춤형 ERP 시스템에 대한 매몰 비용이 여전히 높은 경우, 여전히 저항이 존재하지만, 유지보수 계약 만료와 유연한 확장성의 매력 덕분에 비즈니스 타당성 분석은 클라우드 도입을 지지하는 방향으로 계속 기울고 있습니다.

교원 경험 관리에 대한 집중도 강화

교육 기관은 교직원의 만족도를 전략적 우선 과제로 삼고, 감정 분석, 업무 부담 추적, 전문 역량 개발 대시보드를 인사 업무 흐름에 통합하고 있습니다. 경험 관리 도구는 수업 부담, 연구 성과, 업무상 책임에 관한 데이터를 시각화하여 학부장이 불균형을 조기에 파악할 수 있도록 합니다. 이러한 중시는 STEM 분야 교수직을 둘러싼 치열한 노동 시장과 맥을 같이하고 있습니다. 그곳에서는 번아웃이나 타 기관으로의 인재 유출이 프로그램의 지속성을 위협하고 있습니다. 멘토십 조합을 제안하고, 과도한 업무 부담의 징후를 관리자에게 경고하며, 학습 개발 라이브러리와 연동되는 솔루션이 지지를 얻고 있습니다. 교원평의회가 평가 지표가 승진이나 종신재직권에 어떤 영향을 미치는지에 대한 투명성을 요구하고 있어 거버넌스의 복잡성은 여전히 남아 있지만, 교육 기관들은 현재 종합적인 참여도 분석을 인재 유지를 위한 필수 요소로 인식하고 있습니다.

공공 기관의 예산상 제약

예산이 정체되고, 신입생 수가 감소하며, 인플레이션 압박으로 인해 공립 대학은 노후화된 인사 시스템의 업데이트 자금을 확보하지 못해 시스템의 수명을 연장할 수밖에 없습니다. 이사회는 종종 채용을 동결하고, IT 관련 설비 투자를 미루며, 교육상의 우선순위에 자금을 할당하고 있습니다. 그 결과, 공급업체는 단계적 도입, 지불 연기, 혹은 비용을 설비 투자 예산에서 운영 예산으로 전환하는 매니지드 서비스 모델을 제안할 수밖에 없습니다. 재정 전망이 불투명한 상황에서는 아무리 매력적인 총소유비용(TCO) 분석이라 하더라도 거버넌스상의 장벽을 극복하기는 어렵습니다. 따라서 자금 사정이 어려워지면서 업그레이드 주기가 지연되고, 교육 시장 내 HCM 소프트웨어의 전반적인 성장이 억제되고 있습니다.

부문별 분석

On-Premise형 시스템은 2025년 매출의 66.78%를 차지하고 있으며, 이는 대학들이 기밀성이 높은 급여 및 복리후생 기록에 대한 관리 권한을 유지하고자 하는 의향을 반영한 것이지만, 한편으로 클라우드 구독 서비스는 연평균 성장률(CAGR) 10.72%로 증가하고 있습니다. 중규모 대학들이 고정적인 서버 비용을 변동적인 구독 요금제로 전환함에 따라, 시장 내 클라우드 기반 HCM 소프트웨어 규모는 2031년까지 On-Premise 방식의 성장률을 상회할 것으로 예측됩니다.

현재 하이브리드 아키텍처가 기존의 학생 관리 시스템과 클라우드 기반 인사 모듈을 연결해 주고 있어, 교육 기관은 데이터 상주 요건을 충족하면서도 클라우드 버전에서만 제공되는 AI 기능을 도입할 수 있게 되었습니다. 각 벤더사는 주권형 호스팅 옵션과 환경 간 기록을 동기화하는 기성 커넥터를 제공함으로써, 과거 마이그레이션의 걸림돌이었던 통합 부담을 줄이고 있습니다.

2025년에는 코어 HR이 45.61%의 점유율을 유지했으나, 대학들이 전문 교원을 확보하고 유지하기 위해 경쟁을 벌이는 가운데, 인재 관리 솔루션은 연평균 성장률(CAGR) 9.42%로 성장하고 있습니다. 학습·개발 카탈로그, AI를 활용한 채용 활동, 마이크로 크레덴셜 추적 기능 덕분에 교육 기관은 과거 기업 인사 부서에만 국한되었던 도구를 활용할 수 있게 되었으며, 전략적 인재 관리 모듈 분야에서 교육 분야 HCM 소프트웨어 시장 점유율을 확대되고 있습니다.

급여 계산 엔진은 끊임없이 변화하는 세제 및 복리후생 규정으로 인해 여전히 필수적이지만, 혁신은 급여 관련 문의를 해결하고 이상 징후를 감지하여 경고를 발령하는 대화형 에이전트의 통합에 집중되고 있습니다. 2026년 1월 ADP가 발표한 ‘AI 에이전트’는 일상적인 급여 관련 문의를 자동화하고 급여 계산 과정에서 발생하는 이상 징후를 감지하는 것으로, 상품화된 분야에 차별화를 가져오는 노력을 보여줍니다. 이는 차별화가 트랜잭션 처리에서 경험 중심의 기능으로 전환되고 있음을 보여줍니다.

지역별 분석

북미는 클라우드의 조기 도입과 엄격한 FERPA(교육 기록 개인정보 보호법) 거버넌스 덕분에 2025년 매출의 36.18%를 차지하며, 여전히 가장 규모가 큰 지역별 기여원으로 자리매김했습니다. 사립대학과 주요 공립대학은 주 예산이 압박받는 상황에서도 통합형 스위트에 대한 투자를 지속하고 있어 안정적인 수요를 유지하고 있습니다. 캐나다도 비슷한 추세를 보이고 있으며, 각 주에서 디지털 캠퍼스 구상을 지원하고 있습니다. 한편, 멕시코의 교육 기관에서는 수기 방식의 근태 관리 시스템을 단계적으로 폐지하기 시작했으나, IT 인프라가 제한적이어서 그 속도는 완만합니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 연평균 성장률(CAGR)은 8.98%로 성장을 지속하고, 있습니다. 중국과 인도에서는 정부의 보조금이 급여 계산 및 인재 분석을 표준화하는 디지털 캠퍼스 프로그램에 투입되고 있으며, 이는 국민보험 및 인증 시스템과 연동되는 현지 공급업체들을 뒷받침하고 있습니다. 호주에서는 클라우드 보급률이 높고, 학습 및 개발 도구의 도입도 성숙 단계에 이르렀지만, 일본에서는 여전히 신중한 태도가 이어지고 있으며, 기밀 데이터는 On-Premise 클러스터에 보관하는 한편, 사립 대학에서는 클라우드 시범 도입을 검토하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정) 준수 및 남유럽 국가들의 예산 긴축으로 인해 조달 주기가 길어지고 있어 성장세가 완만합니다. 영국과 독일에서는 감사 대응 능력을 강화하기 위해 인사·재무 시스템을 현대화하고 있지만, 프랑스, 이탈리아, 스페인에서는 중앙집권적인 공무원 급여 체계로 인해 거래 진행이 지연되고 있습니다. 중동에서는 사우디아라비아와 아랍에미리트가 국가 교육 개혁 계획에 HCM 요건을 포함시키고, 통합 플랫폼 내에서 교원 양성 현황을 추적하도록 의무화함으로써 시장이 가속화되고 있습니다. 남미와 아프리카는 아직 개발도상국이지만, 급여 계산 및 언어 인터페이스를 현지화하는 지역 스타트업 기업들 덕분에 자원이 제한된 소규모 대학에도 교육 분야의 HCM 소프트웨어 시장이 열리고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

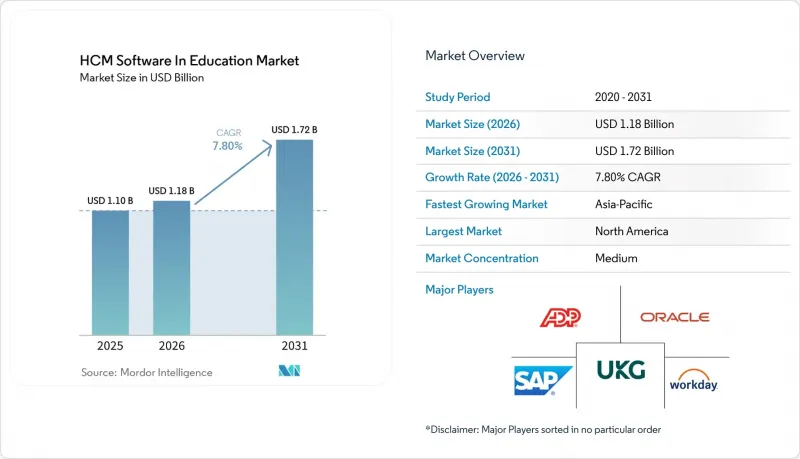

JHS 26.06.23According to Mordor Intelligence, the hCM software in education market size is expected to be USD 1.10 billion in 2025, USD 1.18 billion in 2026, and reach USD 1.72 billion by 2031, growing at a CAGR of 7.8% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud, and On-Premises), Solution (Core HR, Talent Management, Workforce Management, Payroll, and Learning and Development), Institution Type (K-12 Schools, Community Colleges, Universities, and Vocational and Technical Institutes), End-User (Faculty and Staff, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In Education Market Trends and Insights

Growing Cloud-First Strategies Among Universities

Universities are accelerating migrations of payroll, benefits, and recruiting to cloud suites to eliminate data-center costs and support remote faculty access. The shift gained momentum after 2024 when hybrid teaching and multi-campus models exposed the limitations of fixed infrastructure. Providers now package data-conversion tools, sandboxes, and managed services that de-risk complex cutovers. Cloud editions also deliver quarterly feature releases, letting institutions adopt analytics and mobile self-service without long upgrade projects. Workday reported in its fiscal 2026 earnings that education-sector bookings grew by double digits, driven by large public universities replacing legacy ERP stacks with integrated cloud suites. As a result, the HCM software in education market records a steady transfer of workloads from on-premises to cloud subscriptions. Resistance persists where sunk costs in customized ERP stacks remain high, yet expiring maintenance contracts and the lure of elastic scaling continue to tip business cases in favor of cloud adoption.

Increasing Emphasis on Faculty Experience Management

Academic employers are elevating faculty satisfaction to strategic priority, embedding sentiment analysis, workload tracking, and professional-development dashboards into HR workflows. Experience-management tools surface data on teaching loads, research output, and service commitments, enabling deans to spot inequities early. The emphasis aligns with a competitive labor market for STEM professors, where burnout and poaching threaten program continuity. Solutions that recommend mentorship pairings, alert administrators to looming overloads, and integrate with learning-development libraries are gaining favor. Governance complexities remain, because faculty senates demand transparency on how metrics influence promotion and tenure, yet institutions now view holistic engagement analytics as essential for retention.

Budgetary Constraints in Public Institutions

Flat appropriations, enrollment dips, and inflationary pressures leave public universities extending the lives of aging HR systems rather than funding replacements. Boards often freeze hiring and defer IT capital outlays, reserving cash for instructional priorities. Consequently, vendors must propose phased deployments, deferred payment terms, or managed-service models that shift costs from capital to operating budgets. Even attractive total-cost-of-ownership analyses struggle to clear governance hurdles when fiscal forecasts remain uncertain. The funding squeeze therefore slows upgrade cycles and tempers overall expansion of the HCM software in education market.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI-Powered Skills Mapping

- Rising Compliance Burden for Academic Payroll

- Data-Privacy Concerns Around Student Employees

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises systems held 66.78% of 2025 revenue, reflecting universities' desire to retain control of sensitive payroll and benefits records, yet cloud subscriptions are rising at a 10.72% CAGR. The HCM software in education market size for cloud deployments is expected to outpace on-premises growth through 2031 as mid-tier colleges convert fixed server costs into variable subscription fees.

Hybrid architectures now bridge legacy student systems and cloud HR modules, letting institutions meet data-residency mandates while adopting AI features delivered only in cloud releases. Vendors offer sovereign hosting options and pre-built connectors that synchronize records between environments, reducing the integration burden that once deterred migrations.

Core HR maintained 45.61% share in 2025, but talent-management suites are expanding at a 9.42% CAGR as universities compete to attract and retain specialized faculty. Learning-development catalogs, AI-driven recruiting, and micro-credential tracking give institutions tools once confined to corporate HR, broadening the HCM software in education market share for strategic talent modules.

Payroll engines remain indispensable because of ever-changing tax and benefit regulations, yet innovation concentrates on embedding conversational agents that resolve pay inquiries and surface anomaly alerts. ADP's launch of AI Agents in January 2026, which automate routine payroll inquiries and flag anomalies in pay runs, represents an effort to inject differentiation into a commoditized category. This indicates that differentiation is migrating from transactional processing to experience-centric capabilities.

Geography Analysis

North America remained the largest regional contributor with 36.18% revenue in 2025 thanks to early cloud adoption and strict FERPA governance. Private universities and flagship publics continue to fund integrated suites even amid state budget pressure, sustaining steady demand. Canada follows similar patterns as provinces sponsor digital-campus initiatives, while Mexico's institutions begin phasing out manual timekeeping, albeit at slower pace because of limited IT infrastructure.

Asia-Pacific is the fastest-growing territory, posting an 8.98% CAGR. China and India channel government grants into digital-campus programs that standardize payroll and talent analytics, lifting local vendors that integrate with national insurance and accreditation systems. Australia shows high cloud penetration and mature learning-development adoption, whereas Japan remains cautious, keeping sensitive data in on-premises clusters but exploring cloud pilots at private universities.

Europe grows modestly as GDPR compliance and budget austerity in southern states elongate procurement cycles. The United Kingdom and Germany modernize HR and finance stacks to enhance audit readiness, yet centralized civil-service pay frameworks in France, Italy, and Spain slow deal flow. The Middle East accelerates as Saudi Arabia and the United Arab Emirates embed HCM requirements in national education-transformation plans, mandating faculty-development tracking inside integrated platforms. South America and Africa are nascent, but regional startups that localize payroll and language interfaces open the HCM software in education market to smaller colleges with constrained resources.

- Workday Inc.

- Oracle Corporation

- SAP SE

- UKG Inc.

- Cornerstone OnDemand Inc.

- Instructure Holdings Inc.

- Ellucian Company L.P.

- PeopleAdmin Inc.

- Frontline Technologies Group LLC

- PowerSchool Holdings Inc.

- ADP Inc.

- Ceridian HCM Holding Inc.

- Paycom Software Inc.

- BambooHR LLC

- Paycor HCM Inc.

- Namely Inc.

- Gusto, Inc.

- Ramco Systems Limited

- Civica UK Limited

- Blackboard Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Cloud-First Strategies Among Universities

- 4.2.2 Increasing Emphasis on Faculty Experience Management

- 4.2.3 Integration of AI-Powered Skills Mapping

- 4.2.4 Rising Compliance Burden for Academic Payroll

- 4.2.5 Expansion of Hybrid Work Models in Campuses

- 4.2.6 Demand for Analytics-Driven Student Employment Programs

- 4.3 Market Restraints

- 4.3.1 Budgetary Constraints in Public Institutions

- 4.3.2 Data-Privacy Concerns Around Student Employees

- 4.3.3 Fragmented Legacy SIS and ERP Stacks

- 4.3.4 Limited IT Talent in Small Colleges

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.2 By Solution

- 5.2.1 Core HR

- 5.2.2 Talent Management

- 5.2.3 Workforce Management

- 5.2.4 Payroll

- 5.2.5 Learning and Development

- 5.3 By Institution Type

- 5.3.1 K-12 Schools

- 5.3.2 Community Colleges

- 5.3.3 Universities

- 5.3.4 Vocational and Technical Institutes

- 5.4 By End-User

- 5.4.1 Faculty and Staff

- 5.4.2 Administrative HR

- 5.4.3 Student Employees

- 5.4.4 Contractors and Adjuncts

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 SAP SE

- 6.4.4 UKG Inc.

- 6.4.5 Cornerstone OnDemand Inc.

- 6.4.6 Instructure Holdings Inc.

- 6.4.7 Ellucian Company L.P.

- 6.4.8 PeopleAdmin Inc.

- 6.4.9 Frontline Technologies Group LLC

- 6.4.10 PowerSchool Holdings Inc.

- 6.4.11 ADP Inc.

- 6.4.12 Ceridian HCM Holding Inc.

- 6.4.13 Paycom Software Inc.

- 6.4.14 BambooHR LLC

- 6.4.15 Paycor HCM Inc.

- 6.4.16 Namely Inc.

- 6.4.17 Gusto, Inc.

- 6.4.18 Ramco Systems Limited

- 6.4.19 Civica UK Limited

- 6.4.20 Blackboard Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment