|

시장보고서

상품코드

2063754

바이오마커 탐색 분야 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Biomarker Discovery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

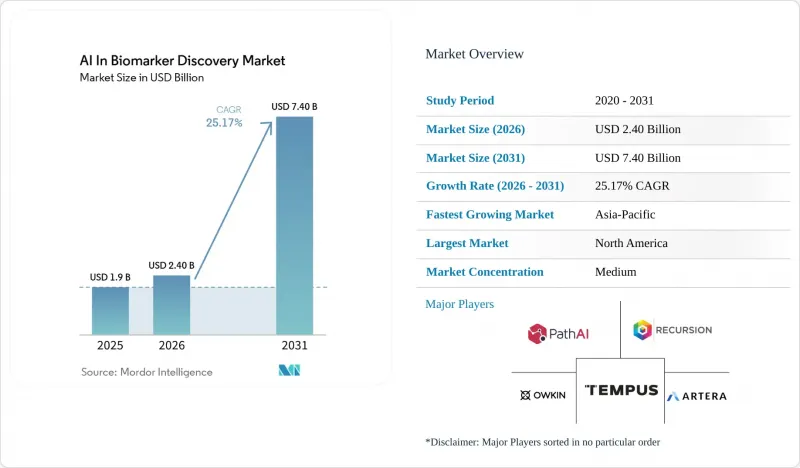

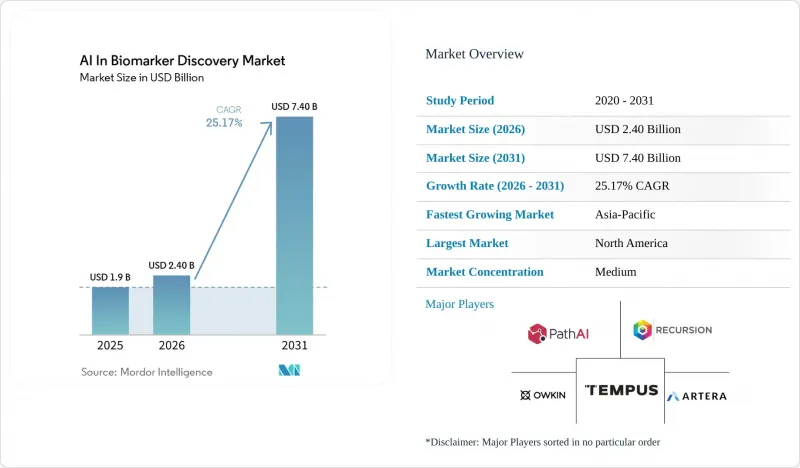

Mordor Intelligence에 의하면, 바이오마커 탐색 분야 인공지능(AI) 시장 규모는 2025년 19억 달러로 평가되었습니다. 2026년에는 24억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 25.17%로 성장을 지속해, 2031년까지 74억 달러에 이를 것으로 예측됩니다.

본 보고서는 데이터 모달리티(유전체학, 전사체학 등), 질환 분야(종양학, 면역학/염증 등), AI 접근법(지도 학습/고전적 머신러닝 등), 바이오마커 유형(예측 바이오마커 등), 최종 사용자(바이오의약품 등), 도입 모델(클라우드/SaaS, 하이브리드 등), 지역(북미 등)에 따라 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계의 바이오마커 탐색 분야 인공지능(AI) 시장 동향 및 인사이트

종양학 주도의 정밀 의학에 대한 수요

임상 현장에서는 기존의 조직병리학을 대신해 AI를 활용한 분자 아형 분류가 점점 더 널리 채택되고 있습니다. 2025년, FDA는 17건의 종양학 AI 바이오마커 검사를 승인했는데, 이는 2024년의 9건에서 증가한 수치입니다. 이 중 12건은 면역요법 반응에 초점을 맞춘 것이었고, 5건은 미세 잔류 병변을 대상으로 한 것이었습니다. 전체 슬라이드 이미징과 공간 전사체학을 결합함으로써, 체크포인트 억제제의 효능을 예측할 때의 양성 예측치는 82%에 달했으며, 이는 기존의 PD-L1 염색에 비해 14포인트 향상된 수치입니다. 순환 종양 DNA 검출에 있어 1ppm의 감도를 지닌 체액 생검 패널은 침습적인 생검을 대체할 수 있는 능력에 힘입어 연평균 31%의 성장률을 보이고 있습니다. 또한, 멀티오믹스 패널을 통해 신약 개발 기간이 36개월에서 1년 미만으로 대폭 단축되었으며, 의약품 특허의 보호 기간이 연장되고 있습니다.

다중오믹스 데이터셋과 디지털 병리학의 확대

고해상도 스캐너는 현재 비용 효율적인 속도로 기가픽셀 이미지를 아카이브하고 있어, 병원이 이미 보존된 슬라이드 라이브러리를 활용할 수 있게 되었습니다. 단일 세포 RNA 시퀀싱 기술은 한 번의 실행으로 100만 개의 세포를 처리할 수 있을 정도로 발전한 반면, 공간 플랫폼은 세포당 5,000개의 유전자를 매핑함으로써, 벌크 프로파일링에서는 간과되기 쉬운 국소적인 틈새를 밝혀내고 있습니다. 영국과 중국 등에서 진행 중인 대규모 사업을 통해 향후 10년 동안 150만 건의 유전체 데이터가 추가될 것으로 예상되며, 희귀 변이와의 연관성을 감지하는 능력이 강화될 전망입니다. 극소량의 시료로 7,000종의 단백질을 정량할 수 있는 혈장 프로테옴 분석법은 전사체학과 프로테옴학 사이의 기능적 격차를 메우고 있습니다.

데이터 사일로화, 개인정보 보호 및 국경을 넘는 데이터 전송에 대한 제약

GDPR(EU 개인정보보호규정)이나 PIPL과 같은 규제, 그리고 취약한 EU-미국 데이터 개인정보 보호 체제로 인해, 다국적 간 데이터 통합은 여전히 불투명한 상황입니다. 병원에서는 오믹스 아카이브를 경쟁 우위 자산으로 취급하는 경향이 강해지는 반면, 재식별 연구에 따르면 ‘익명화’된 유전체의 83%가 추적 가능한 것으로 나타났으며, 이에 따라 데이터 이용 조건이 더욱 엄격해지고 있습니다. 대규모 훈련 데이터셋에 의존하는 바이오마커 발견 시장에서는 엄격한 ε 수준에서 차등 프라이버시 노이즈가 AUROC를 최대 7포인트까지 낮출 가능성이 있습니다. 이로 인해 규정 준수와 실용성 사이에서 상충 관계가 발생하여, 이 분야의 AI 발전이 더뎌지고 있습니다.

부문별 분석

2025년, 유전체학은 매출의 35.12%를 차지하며 정밀 종양학 분야에서 핵심적인 역할을 확고히 다졌습니다. 한편, 단일 세포 및 공간적 기법에 힘입어 전사체학은 연평균 성장률(CAGR) 28.16%로 성장하고 있습니다. 세포당 비용이 0.10달러 미만으로 떨어짐에 따라, 전사체학은 유전체학과의 격차를 좁힐 것으로 예측됩니다. 이 두 가지 모달리티의 통합을 통해, 그동안 간과되었던 인과관계를 나타내는 신호가 밝혀졌으며, 특히 멀티오믹스 플랫폼 분야에서 바이오마커 발견 시장의 AI 성장을 주도하고 있습니다.

Paige사의 Virchow2는 라벨이 지정되지 않은 슬라이드 아카이브를 활용하여 희귀암 모델을 개발할 수 있음을 입증했습니다. 이는 병리 영상이 향후 멀티모달 파이프라인에서 약한 라벨을 제공하는 데 중요한 역할을 할 수 있음을 시사합니다. 그러나 현재 유전체, 트랜스크립토-ム, 프로테오-ム, 대사체 프로파일이 완전히 일치하는 암 환자는 5% 미만에 불과하며, 이로 인해 종합적인 기반 모델의 학습에 제약이 따르고 있습니다.

2025년 지출 중 종양학이 43.18%를 차지했으며, 이는 바이오마커 기반 치료법의 승인에 중점을 두고 있는 점과 종양의 이질성이 지닌 복잡성을 반영하고 있습니다. 희귀질환 분야는 환자 수가 적다는 과제를 해결하기 위해, 후원사들이 합성 코호트 및 연합 등록 시스템을 점점 더 많이 도입함에 따라 연평균 성장률(CAGR) 29.61%라는 강력한 성장세를 보이고 있습니다. 이러한 전략은 2024년 하반기에 성숙기에 접어들었으며, 현재는 바이오마커 탐색 분야 인공지능(AI) 시장 전체로 확대되고 있습니다.

면역학 분야의 응용에서는 T세포 클로노유형을 효과적으로 분석할 수 있는 단일 세포 RNA-seq 기술의 이점을 누리고 있습니다. 반면, 심혈관 대사 질환 프로젝트는 보험 급여 승인 절차가 종양학 분야보다 약 2년 정도 지연되고 있어 여전히 발전 단계에 있습니다. 그러나 AI 기반 다유전자 위험 예측 엔진이 10년 후 심혈관 질환 예측에서 AUROC 0.75를 달성한 바 있으며, 지불자 코드가 도입된다면 이 부문은 상당한 성장이 예상됩니다.

지역별 분석

2025년, 북미는 매출의 43.16%를 차지했습니다. 이는 NIH의 ‘All of Us’ 코호트 확대와 메디케어의 다중 암 조기 발견 검사 적용 확대에 힘입은 결과입니다. 벤처 캐피탈의 활발한 유입과 FDA의 신속화된 PCCP(Precision Cancer Control Program) 절차 덕분에 스타트업 기업들은 경쟁 우위를 유지할 수 있게 되었으며, AI를 활용한 바이오마커 발견 시장에서 이 지역의 리더십이 강화되고 있습니다.

아시아태평양은 중국의 92억 달러 규모의 ‘정밀 의학 이니셔티브’와 인도에서 AI에 특화된 진단 벤처 기업의 부상 등 막대한 투자의 뒷받침을 받아, 2031년까지 연평균 성장률(CAGR) 30.08%라는 견실한 성장이 예상됩니다. 데이터 주권법의 시행에 따라 개인정보 보호형 머신러닝과 페더레이티드 컴퓨팅의 도입이 가속화되고 있으며, 이는 제품 개발 분야의 혁신을 주도하고 있습니다. 또한, 일본이 2025년을 목표로 FDA 지침을 준수함으로써, 전 세계 개발 기업들의 이중 제출 전략이 간소화될 것입니다.

유럽에서는 꾸준한 성장이 나타나고 있지만, IVDR(체외진단의료기기규정)의 엄격한 증거 요건이 과제로 대두되고 있습니다. 한편, 걸프협력회의(GCC) 회원국들의 유전체 프로젝트와 브라질에서 AI를 활용한 결핵 선별 검사 사업은 신흥 시장이 바이오마커 응용 분야에서 AI를 빠르게 도입하고 있는 실태를 여실히 보여주고 있습니다. 이 지역들은 현재 총 수익의 15% 미만을 차지하고 있을 뿐이지만, 인프라 구축이 진행됨에 따라 높은 성장 잠재력을 지니고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the aI in biomarker discovery market size is expected to grow from USD 1.9 billion in 2025 to USD 2.40 billion in 2026 and is forecast to reach USD 7.40 billion by 2031 at 25.17% CAGR over 2026-2031.

This report is Segmented by Data Modality (Genomics, Transcriptomics, and More), Disease Area (Oncology, Immunology/Inflammation, and More), AI Approach (Supervised/Classical ML, and More), Biomarker Type (Predictive, and More), End User (Biopharma, and More), Deployment Model (Cloud/SaaS, Hybrid, and More), and Geography (North America, and More). Market Forecasts are Provided in Value (USD).

Global AI In Biomarker Discovery Market Trends and Insights

Oncology-Led Precision Medicine Demand

Clinical practices are increasingly adopting AI-driven molecular subtyping over traditional histopathology. In 2025, the FDA approved 17 oncology AI biomarker tests, up from 9 in 2024. Of these, 12 focused on immunotherapy responses, while 5 targeted minimal residual disease. Whole-slide imaging combined with spatial transcriptomics now achieves an 82% positive predictive value for predicting checkpoint-inhibitor efficacy, a 14-point improvement over traditional PD-L1 staining. Liquid-biopsy panels, with a sensitivity of 1 ppm in detecting circulating tumor DNA, are growing at an annual rate of 31%, driven by their ability to replace invasive biopsies. Additionally, multi-omic panels have significantly reduced discovery timelines from 36 months to under a year, enhancing the protection of drug-patent life.

Expansion of Multi-Omics Datasets and Digital Pathology

High-resolution scanners now archive gigapixel images at a cost-effective rate, enabling hospitals to utilize their archived slide libraries. Single-cell RNA sequencing has advanced to process 1 million cells per run, while spatial platforms map 5,000 genes per cell, uncovering localized niches that bulk profiling often misses. Large-scale initiatives, such as those in the UK and China, are projected to add 1.5 million genomes this decade, strengthening the ability to detect rare-variant associations. Plasma-proteome assays, capable of quantifying 7,000 proteins from minimal sample volumes, are narrowing the functional gap between transcriptomics and proteomics.

Data Silos, Privacy, and Cross-Border Data Transfer Limits

Multi-national data pooling remains uncertain due to regulations such as GDPR, PIPL, and the fragile EU-US Data Privacy Framework. Hospitals increasingly treat omics archives as competitive assets, while re-identification studies indicate that 83% of "anonymized" genomes can be traced, leading to stricter terms for data usage. In the biomarker discovery market, where deployments depend on extensive training datasets, differential-privacy noise can reduce AUROC by up to seven points at stringent epsilon levels. This creates a trade-off between compliance and utility, slowing AI advancements in the sector.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Tailwinds (FDA BQP; Evolving AI/ML SaMD Guidance)

- Cloud/SaaS-Native Analytics and Scalable Compute

- Analytical/Clinical Validation Burden Under IVDR and LDT Reforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Genomics accounted for 35.12% of the revenue, solidifying its foundational role in precision oncology. Meanwhile, Transcriptomics, driven by single-cell and spatial methods, is advancing with a 28.16% CAGR. As per-cell costs decrease below USD 0.10, Transcriptomics is expected to close the gap with Genomics. The integration of these two modalities is uncovering causal signals previously overlooked, driving the growth of AI in the biomarker discovery market, particularly for multi-omic platforms.

Paige's Virchow2 demonstrated that unlabeled slide archives can be utilized to develop models for rare cancers. This indicates that pathology images could play a significant role in providing weak labels for future multimodal pipelines. However, fewer than 5% of cancer patients currently have fully matched genomic, transcriptomic, proteomic, and metabolomic profiles, which limits comprehensive foundation-model training.

Oncology accounted for 43.18% of the 2025 expenditure, reflecting the emphasis on biomarker-guided therapy approvals and the complexity of tumor heterogeneity. Rare disorders are experiencing strong growth at a 29.61% CAGR, driven by sponsors increasingly adopting synthetic cohorts and federated registries to address the challenges of small patient populations. These strategies matured in late 2024 and are now scaling across the AI in biomarker discovery market.

Immunology applications are benefiting from single-cell RNA-seq techniques that effectively profile T-cell clonotypes. In contrast, cardiometabolic projects remain underdeveloped due to reimbursement processes lagging behind oncology by approximately two years. However, with AI-driven polygenic-risk engines achieving a 0.75 AUROC for 10-year cardiovascular predictions, this segment is positioned for significant growth once payer codes are introduced.

Geography Analysis

In 2025, North America accounted for 43.16% of the revenue, driven by the expansion of the NIH's "All of Us" cohort and Medicare's coverage of multi-cancer early-detection tests. A strong flow of venture capital and the FDA's expedited PCCP pathway enable startups to maintain a competitive edge, reinforcing the region's leadership in the AI-driven biomarker discovery market.

Asia-Pacific, supported by significant investments such as China's USD 9.2 billion Precision Medicine Initiative and the rise of AI-focused diagnostic ventures in India, is projected to grow at a robust 30.08% CAGR through 2031. The implementation of data-sovereignty laws is accelerating the adoption of privacy-preserving machine learning and federated computing, driving innovation in product development. Additionally, Japan's alignment with FDA guidelines for 2025 simplifies dual-filing strategies for global developers.

Europe is experiencing steady growth, although the IVDR's stringent evidence requirements pose challenges. Meanwhile, genomics projects in the Gulf Cooperation Council and AI-based tuberculosis screening initiatives in Brazil highlight how emerging markets are rapidly adopting AI in biomarker applications. While these regions currently contribute less than 15% of the total revenue, they represent high-growth opportunities as infrastructure development progresses.

- ArteraAI

- Caris Life Sciences Inc.

- ConcertAI

- Foundation Medicine (Roche)

- Freenome

- GeneDx

- GRAIL

- Guardant Health

- Ibex Medical Analytics

- Imagene AI

- Immunai

- Insitro

- Lunit

- nference

- Owkin Inc.

- Paige

- PathAI Inc.

- Recursion

- SOPHiA GENETICS

- Tempus AI, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 arket Drivers

- 4.2.1 Oncology-Led Precision Medicine Demand

- 4.2.2 Expansion of Multi-Omics Datasets and Digital Pathology

- 4.2.3 Regulatory Tailwinds (FDA BQP; Evolving AI/ML Samd Guidance)

- 4.2.4 Cloud/Saas-Native Analytics and Scalable Compute

- 4.2.5 Federated Learning Unlocking Cross-Institution Discovery

- 4.2.6 Multimodal Foundation Models Linking Omics-Imaging Clinical

- 4.3 Market Restraints

- 4.3.1 Data Silos, Privacy, and Cross-Border Data Transfer Limits

- 4.3.2 Analytical/Clinical Validation Burden Under IVDR And LDT Reforms

- 4.3.3 Batch Effects and Assay Drift Causing Model Non-Stationarity

- 4.3.4 Explainability and Lifecycle Change Control (PCCP) for AI Biomarkers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Data Modality

- 5.1.1 Genomics (WES/WGS, targeted panels)

- 5.1.2 Transcriptomics (bulk, single-cell)

- 5.1.3 Proteomics

- 5.1.4 Metabolomics/Lipidomics

- 5.1.5 Epigenomics

- 5.1.6 Others

- 5.2 By Disease Area

- 5.2.1 Oncology (solid and hematologic)

- 5.2.2 Immunology/Inflammation

- 5.2.3 Cardiometabolic (CVD, diabetes, NASH)

- 5.2.4 Neurology/Neurodegeneration

- 5.2.5 Infectious Diseases

- 5.2.6 Rare/Genetic Disorders

- 5.2.7 Others

- 5.3 By AI Approach

- 5.3.1 Supervised and Classical ML

- 5.3.2 Deep Learning (CNNs/RNNs/Transformers)

- 5.3.3 Self-/weakly-supervised and Transfer Learning

- 5.3.4 Foundation Models (pathology, radiology, omics)

- 5.3.5 Graph and Network-based ML

- 5.3.6 Others

- 5.4 By Bimarker Type

- 5.4.1 Predictive Biomarkers

- 5.4.2 Prognostic Biomarkers

- 5.4.3 Safety Biomarkers

- 5.4.4 Surrogate Endpoints

- 5.4.5 Other Types

- 5.5 By End User

- 5.5.1 Biopharma and Biotech Sponsors

- 5.5.2 Diagnostics and CDx Developers

- 5.5.3 Contract Research/Central Labs

- 5.5.4 Academic and Research Institutes

- 5.5.5 Others

- 5.6 By Deployment / Access Model

- 5.6.1 Cloud/SaaS

- 5.6.2 Hybrid

- 5.6.3 On-premises

- 5.6.4 Federated/Edge Deployments

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 ArteraAI

- 6.3.2 Caris Life Sciences Inc.

- 6.3.3 ConcertAI

- 6.3.4 Foundation Medicine (Roche)

- 6.3.5 Freenome

- 6.3.6 GeneDx

- 6.3.7 GRAIL

- 6.3.8 Guardant Health

- 6.3.9 Ibex Medical Analytics

- 6.3.10 Imagene AI

- 6.3.11 Immunai

- 6.3.12 Insitro

- 6.3.13 Lunit

- 6.3.14 nference

- 6.3.15 Owkin Inc.

- 6.3.16 Paige

- 6.3.17 PathAI Inc.

- 6.3.18 Recursion

- 6.3.19 SOPHiA GENETICS

- 6.3.20 Tempus AI, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment