|

시장보고서

상품코드

2063783

비근침윤성 방광암 치료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Non-muscle Invasive Bladder Cancer Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

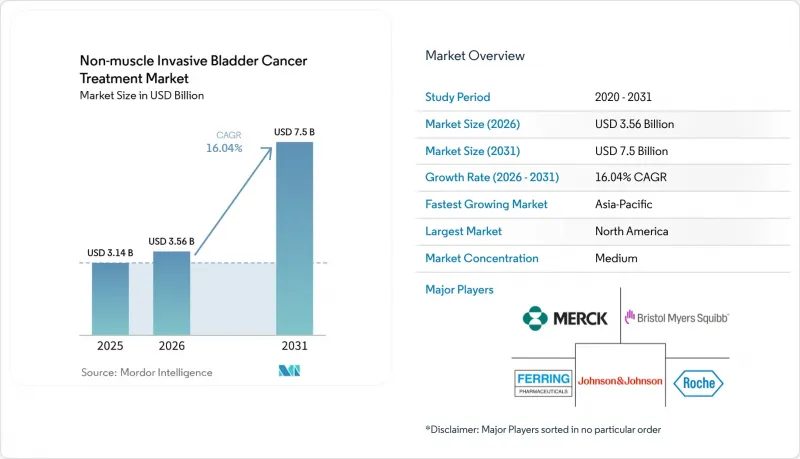

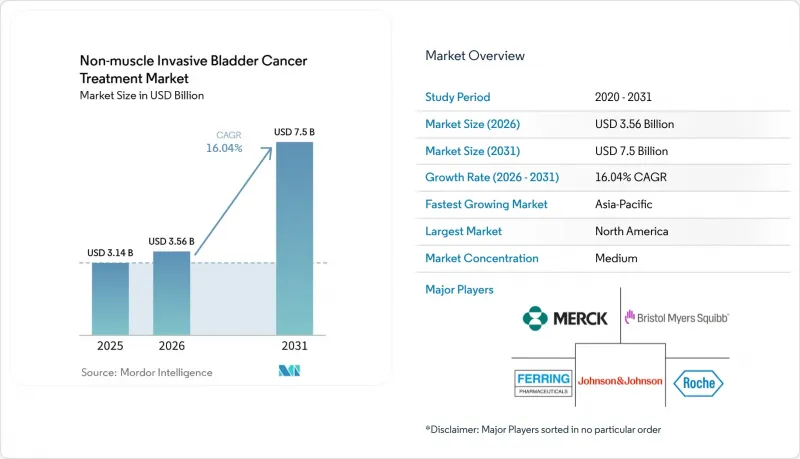

Mordor Intelligence에 의하면, 비근침윤성 방광암 치료 시장 규모는 2025년에 31억 4,000만 달러로 평가되었습니다. 2026년에 35억 6,000만 달러에서 2031년까지 75억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 16.04%로 성장할 것으로 전망됩니다.

본 보고서는 치료법(BCG, 화학요법, 면역요법, 유전자 치료, 기기 보조 방광 내 치료), 투여 경로(방광 내, 전신), 질환 병기(Ta, T1, CIS), 최종 사용자(병원, 전문 클리닉, ASC), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계의 비근침윤성 방광암 치료 시장 동향 및 인사이트

승인 범위가 확대됨에 따라 BCG 비반응성 치료의 선택지가 넓어집니다.

나도파라젠 필라데노베크, 안크티바, 펨브롤리주맙에 대한 FDA 및 EMA의 승인이 잇따르면서, BCG에 대한 지속적인 반응을 얻지 못하는 환자를 위한 구제 치료의 방향이 재정의되고 있습니다. ANKTIVA의 IL-15 슈퍼아고니즘은 자연살해세포의 침윤을 증폭시켜, 주요 QUILT 3.032 임상시험에서 12개월 완전 반응률 62%를 달성했으며, 이는 단일제 화학요법의 기존 기준치의 2배에 해당합니다. 펠링(Felling)사의 아데노바이러스 p53 유전자 치료법은 고악성 종양의 50%를 유발하는 TP53 돌연변이 부하에 대응하는 것이며, 한편 CG 종양(CG Oncology)사의 크레토스티모젠에 대한 획기적 치료제 지정은 종양 용해성 플랫폼에 대한 규제 당국의 신뢰가 높아지고 있음을 보여줍니다. 이러한 일련의 승인으로 인해, BCG 치료 실패 후 다음 치료법으로 전환하기까지의 기간이 18개월에서 6개월 미만으로 단축되었으며, 기존에는 조기에 방광 전적출술을 받아야만 했던 진행 단계까지의 기간을 단축할 수 있게 되었습니다.

BCG 공급 제약으로 대체 요법 도입이 가속화되고 있습니다.

만성적인 공급 부족에 따라, 미국 비뇨기과학회는 BCG를 구할 수 없는 경우의 첫 번째 선택으로 유전자 치료 또는 체크포인트 억제제를 권장하고 있습니다. UroGen Pharma는 2025년 1분기 Jelmyto의 처방 건수가 전년 동기 대비 140% 증가했다고 보고했으며, 의사들이 BCG에 의존하는 치료 경로 대신 조기 화학요법을 선택하고 있는 것으로 보아 치료 알고리즘의 구조적 재편이 진행되고 있음이 드러나고 있습니다. 효모를 이용해 생산량을 15배로 늘린 머크의 재조합 BCG는 2024년에 2상 임상시험에 진입하여 2027년 출시를 향해 순조롭게 진행되고 있지만, 그때까지는 생산 능력 부족이 지속될 전망입니다. 이러한 공급 부족으로 인해, 치료 경험이 없는 환자들이 과거에는 구제 요법으로만 사용되던 대체 요법으로 몰리고 있으며, 면역 요법에 대한 기본적인 수요가 지속적으로 증가하고 있습니다.

기존의 방광 내 화학요법 및 BCG와 비교했을 때 높은 비용

나도파라진의 1코스당 가격은 18만 9,000달러인 반면, 6주간의 BCG 유도 요법 비용은 3,500-5,000달러이며, 제네릭 미토마이신은 1회 투여당 400달러로, 무려 30배나 되는 가격 차이가 발생하고 있어, 이로 인해 지불 측의 반발을 불러일으키고 있습니다. 메디케어는 BCG 치료가 실패한 경우 및 고악성도 조직형의 경우에만 유전자 치료를 적용하고 있으며, 신규 환자의 60%를 차지하는 중간 위험군 Ta 환자는 대상에서 제외됩니다. 영국과 독일의 성과 연계형 계약에서는 12개월 시점에서 완전한 치료 효과를 얻지 못한 경우, 제약사가 치료비의 40%를 환불할 의무가 있기 때문에 조기 도입이 억제되고 있습니다. 본인 부담률이 50% 이상의 인도와 브라질에서는 많은 환자가 제네릭 항암제로 전환하거나, 바로 방광 전적출술을 받고 있습니다.

부문별 분석

2025년 기준으로, 비근침윤성 방광암 치료 시장 점유율의 45.09%를 화학요법이 차지했으며, 미토마이신과 젬시타빈이 주를 이루었습니다. 그러나 면역요법은 2031년까지 연평균 성장률(CAGR) 18.19%로 성장할 전망이며, 이는 체크포인트 억제제와 IL-15 작용제가 초기 치료 단계에서 사용되고 있음을 반영한 것입니다. BCG 요법은 고위험 질환에 대한 1차 치료법으로 자리 잡고 있지만, 치료 능력의 한계가 그 발전을 저해하고 있습니다. 유전자 치료는 프리미엄 가격을 형성하고 있으며, 이것이 막대한 수익으로 이어지고 있습니다. 2025년에는 유럽의 의료기관들이 Combat Medical사의 BRS를 도입함에 따라, 의료기기를 활용한 온열 요법 시스템의 매출액이 전년 대비 22% 증가를 기록했습니다.

면역요법의 부상은 장기적인 데이터에 달려 있습니다. 2026년에 예정된 Keynote-057 임상시험의 36개월 시점 분석 결과를 통해, 체크포인트 억제 요법이 근육 침윤을 막을 수 있는지 여부가 밝혀질 것입니다. 실제 임상 현장에서 니볼마브의 반응률은 임상시험 결과보다 낮게 나타나고 있으며, 통제된 환경과 일반 의료 현장 간에 차이가 있음이 밝혀졌습니다. 유전자 치료의 1회 투여라는 편의성은 건강이 약한 고령자들에게 호응을 얻고 있지만, 인증과 관련된 병목 현상이 임상 참여에 제약을 주고 있습니다. 생물학적 제제의 가격이 여전히 부담스러운 저소득 지역에서는 화학요법이 계속해서 주류를 이룰 것으로 보이지만, 특허 만료로 인한 가격 결정력 약화에 따라 그 성장세는 둔화되고 있습니다.

2025년 기준으로 방광 내 투여는 비근침윤성 방광암 치료 시장의 55.14%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 18.14%로 확대될 것으로 전망됩니다. TAR-200은 6회의 카테터 삽입을 1회의 방광경 삽입으로 통합하여, 진료 시간과 간호 자원을 확보해 줍니다. RTGel은 미토마이신의 접촉 시간을 6배로 연장하여, 지역 의료에 적합한 주 1회 투여 일정을 가능하게 합니다. 전신성 PD-1 억제제는 다발성 병변이 있거나 카테터 삽입이 불가능한 환자에게 사용되지만, 면역 관련 이상반응의 위험이 높아집니다. 2상 임상시험 단계에 있는 경구용 PD-1 억제제는 카테터 삽입이 불가능한 환자군을 대상으로 하고 있지만, 방광 내 투여를 통한 표준 치료법을 대체하기 위해서는 효능의 지속성과 안전성 문제를 해결해야 합니다.

투여 경로의 선택은 점점 더 생물학적 특성에 근거하여 이루어지고 있습니다. PD-L1 발현이 높은 종양의 경우 전신 요법이 선택되는 추세인 반면, 유두상 Ta 병변의 경우 방광 내 치료를 통한 표면 재형성을 중시하는 치료법이 적합합니다. 콜드체인 요건으로 인해 유전자 치료는 인증된 시설로 제한되는 경향이 있지만, 서방형 장치는 실온 보관만으로 충분하기 때문에 지리적 적용 범위가 넓어집니다.

지역별 분석

북미는 2025년 매출의 45.35%를 차지했으며, 그 중심은 미국 내 근층 비침윤성 방광암(NMIBC) 치료에 대한 지출입니다. 메디케어의 광범위한 보험 적용, FDA의 신속한 승인, 그리고 높은 가처분 소득이 고가의 생물학적 제제 및 의료기기의 도입을 뒷받침하고 있습니다. 그러나 지불 측의 압박이 거세지고 있으며, 성과 연동형 계약과 진료 장소에 따른 비용 차이로 인해 치료는 이미 진료소로 옮겨가고 있습니다.

유럽은 독일, 프랑스, 영국을 필두로 2025년 매출에서 상당한 점유율을 차지했습니다. EMA의 PRIME 지정에 따라 나도파라겐의 시판까지 걸리는 기간은 대폭 단축되었으나, 의료 기술 평가의 차이로 인해 지역별로 접근 상황이 제각각입니다. 독일은 2025년에 전액 상환을 승인한 반면, 프랑스는 3년간의 등록 의무를 부과했기 때문에 도입이 지연되고 있습니다. 스페인의 HIVEC 컨소시엄이 제공하는 공유 서비스와 확대된 ‘컴패셔네이트 유스(Compassionate Use)’ 체크포인트는 혁신과 비용 절감의 균형을 모색하는 유럽의 실용적인 노력을 여실히 보여주고 있습니다.

아시아태평양은 급성장 지역으로, 2031년까지 연평균 성장률(CAGR) 18.3%를 나타낼 것으로 전망됩니다. 중국이 2024년 11월 BCG 무효성 CIS에 대한 펨브롤리주맙을 승인한 데 더해, 연간 8,000달러로 가격이 책정된 국내 PD-1 바이오시밀러가 치료 접근성의 민주화를 추진하고 있습니다. 인도에서는 2025년에 미토마이신의 제네릭 의약품이 승인되고, 1바이알당 가격이 1만 2,000루피(145달러)로 인하됨에 따라 2급 도시에서 보급이 확대되고 있습니다. 일본은 고령화가 진행되고 있으며, 국민건강보험 제도가 잘 갖춰져 있어 해당 지역에서 두 번째로 큰 시장을 형성하고 있지만, PMDA가 정한 국내 임상시험 요건으로 인해 신규 진입이 지연되고 있습니다. 2025년 한국의 펨브롤리주맙 가격 40% 인하와 2026년 호주의 TAR-200 승인을 계기로, 비용 대비 효과가 높은 제네릭 의약품과 고부가가치 서방형 제형 장치를 모두 적극적으로 도입하는 아시아태평양이 형성되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the non-muscle invasive bladder cancer treatment market size is projected to be USD 3.14 billion in 2025, USD 3.56 billion in 2026, and reach USD 7.5 billion by 2031, growing at a CAGR of 16.04% from 2026 to 2031.

This report is Segmented by Therapy (BCG, Chemotherapy, Immunotherapy, Gene Therapy, Device-Assisted Intravesical), Route of Administration (Intravesical, Systemic), Disease Stage (Ta, T1, CIS), End User (Hospitals, Specialty Clinics, Ascs), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

Global Non-muscle Invasive Bladder Cancer Treatment Market Trends and Insights

Approvals Expanding BCG-Unresponsive Care

A wave of FDA and EMA clearances for nadofaragene firadenovec, ANKTIVA, and pembrolizumab is redefining the salvage pathway for patients who cannot mount a durable response to BCG. ANKTIVA's IL-15 superagonism amplifies natural-killer cell infiltration, delivering a 62% 12-month complete response rate in the pivotal QUILT 3.032 study, twice the historical benchmark for single-agent chemotherapy. Ferring's adenoviral p53 gene therapy addresses the TP53 mutation burden that drives 50% of high-grade tumors, while Breakthrough Therapy status for CG Oncology's cretostimogene signals growing regulatory confidence in oncolytic platforms. Collectively, these approvals cut the lag between BCG failure and next-line therapy from 18 months to less than 6 months, mitigating the progression window that historically forced early cystectomy.

BCG Supply Constraints Accelerating Alternatives Adoption

Chronic shortages have prompted the American Urological Association to recommend gene therapy or checkpoint inhibitors as first-line options when BCG is unavailable. UroGen Pharma reported a 140% year-over-year jump in Jelmyto prescriptions during Q1 2025, underscoring a structural reordering of the treatment algorithm as physicians substitute earlier chemotherapeutic recourse for BCG-reliant pathways. Merck's recombinant BCG, engineered in yeast to generate 15-fold higher yields, entered Phase II trials in 2024 and is on course for a 2027 launch, yet capacity gaps will persist until then. The shortfall is already funneling treatment-naive patients into alternatives once reserved for salvage, permanently lifting baseline demand for immunotherapy.

High Cost Versus Legacy Intravesical Chemo and BCG

Nadofaragene lists at USD 189,000 per course, while a six-week BCG induction costs USD 3,500-5,000 and generic mitomycin USD 400 per instillation, leaving a 30-fold price chasm that sparks payer pushback. Medicare covers gene therapy only after BCG failure and high-grade histology, excluding intermediate-risk Ta patients who make up 60% of incident cases. Outcomes-based contracts in the U.K. and Germany oblige manufacturers to rebate 40% of therapy cost if complete response is not achieved at 12 months, throttling early uptake. In India and Brazil, where out-of-pocket spending exceeds 50%, many patients default to generic chemotherapy or proceed directly to cystectomy.

Other drivers and restraints analyzed in the detailed report include:

- Aging Incidence Base and High NMIBC Share of Bladder Cancer

- Device-Assisted Intravesical Therapy Adoption

- Limited Durability and Retreatment Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemotherapy accounted for 45.09% of non-muscle invasive bladder cancer treatment market share in 2025, anchored by mitomycin and gemcitabine. Yet immunotherapy is set to grow at 18.19% CAGR through 2031, reflecting earlier-line use of checkpoint inhibitors and IL-15 agonists. BCG therapy remains first-line for high-risk disease, but capacity limits crimp growth. Gene therapy commands a premium that translates into outsized revenue. Device-assisted hyperthermia systems logged 22% year-over-year gains in 2025, as European centers adopted Combat Medical's BRS.

Immunotherapy's ascent hinges on long-term data. Keynote-057 36-month readouts due in 2026 will determine if checkpoint blockade can forestall muscle invasion. Real-world nivolumab response rates trail clinical trials, revealing a gap between controlled and community settings. Gene therapy's single-dose convenience resonates with frail elders, yet certification bottlenecks limit clinic participation. Chemotherapy will persist in low-income regions where biologic pricing remains prohibitive, but its growth is slowing as patent cliffs erode pricing power.

Intravesical delivery represented 55.14% of non-muscle invasive bladder cancer treatment market size in 2025 and is projected to expand at an 18.14% CAGR through 2031. TAR-200 condenses six catheterizations into a single cystoscopic insertion, freeing clinic slots and nursing capacity. RTGel extends mitomycin contact time sixfold, enabling weekly schedules that fit community practice. Systemic PD-1 inhibitors serve multifocal disease and patients unable to catheterize, but carry higher immune-related adverse-event risk. Oral PD-1 inhibitors in Phase II target non-catheterizable cohorts but must clear durability and safety hurdles before displacing intravesical standards.

The route split is increasingly biology-driven. Tumors with high PD-L1 expression trend toward systemic therapy, while papillary Ta disease favors resurfacing-focused intravesical options. Cold-chain requirements tilt gene therapy toward accredited centers, whereas sustained-release devices need only room-temperature storage, broadening their geographic reach.

Geography Analysis

North America generated 45.35% of 2025 revenue, anchored by the United States' spending on NMIBC therapies. Broad Medicare coverage, rapid FDA approvals, and high disposable incomes underpin adoption of premium biologics and devices. Yet payer pressure is mounting; outcomes-based contracts and site-of-service differentials are already nudging therapy into physician offices.

Europe captured a significant share of 2025 revenue, led by Germany, France, and the United Kingdom. EMA's PRIME designation slashed launch timelines for nadofaragene, but divergent health-technology assessments create patchwork access. Germany granted full reimbursement in 2025, while France imposed a three-year registry, delaying uptake. Shared-service HIVEC consortia and expanded compassionate-use checkpoints in Spain illustrate Europe's pragmatic drive to balance innovation with cost containment.

Asia-Pacific is the breakout region, forecast to grow at an 18.3% CAGR through 2031. China's November 2024 approval of pembrolizumab for BCG-unresponsive CIS, combined with domestic PD-1 biosimilars priced at USD 8,000 annually, is democratizing access. India's 2025 mitomycin generic slashed per-vial prices to INR 12,000 (USD 145), expanding uptake in tier-2 cities. Japan's aging cohort and universal insurance position it as the region's second-largest market, but PMDA demands for local trials delay novel entrants. South Korea's 40% price cut for pembrolizumab in 2025 and Australia's 2026 TAR-200 approval round out an APAC region embracing both cost-effective generics and high-value sustained-release devices.

- Asieris Pharmaceuticals

- AstraZeneca

- Bristol-Myers Squibb

- CG Oncology

- Combat Medical

- F. Hoffmann-La Roche (Roche)

- Ferring Pharmaceuticals

- ImmunityBio, Inc.

- Johnson & Johnson

- Merck

- Pfizer

- UroGen Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Approvals Expanding BCG-Unresponsive Care (Gene Therapy, IL-15, PD-1)

- 4.2.2 BCG Supply Constraints Accelerating Alternatives Adoption

- 4.2.3 Aging Incidence Base and High NMIBC Share of Bladder Cancer

- 4.2.4 Device-Assisted Intravesical Therapy (HIVEC/EMDA) Adoption

- 4.2.5 Drug-Device Sustained-Release Platforms

- 4.2.6 Manufacturing Scale-Up (Gene Therapy, rBCG) De-Bottlenecking Access

- 4.3 Market Restraints

- 4.3.1 High Cost Vs. Legacy Intravesical Chemo/BCG

- 4.3.2 Limited Durability/Retreatment Burden in Some Therapies

- 4.3.3 Complex Biologics Manufacturing and Cold-Chain Constraints

- 4.3.4 Capital/Staff Needs for Hyperthermia/EMDA Devices Slow Uptake

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy

- 5.1.1 BCG therapy

- 5.1.2 Chemotherapy

- 5.1.3 Immunotherapy

- 5.1.4 Gene therapy

- 5.1.5 Device-assisted intravesical

- 5.2 By Route of administration

- 5.2.1 Intravesical

- 5.2.2 Systemic (IV/Oral)

- 5.3 By Disease Stage

- 5.3.1 Ta (non-invasive papillary)

- 5.3.2 T1 (lamina propria)

- 5.3.3 Carcinoma in situ (CIS)

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Asieris Pharmaceuticals

- 6.3.2 AstraZeneca

- 6.3.3 Bristol-Myers Squibb

- 6.3.4 CG Oncology

- 6.3.5 Combat Medical

- 6.3.6 F. Hoffmann-La Roche (Roche)

- 6.3.7 Ferring Pharmaceuticals

- 6.3.8 ImmunityBio, Inc.

- 6.3.9 Johnson & Johnson (Janssen)

- 6.3.10 Merck & Co.

- 6.3.11 Pfizer Inc.

- 6.3.12 UroGen Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

(주말 및 공휴일 제외)