|

시장보고서

상품코드

2063784

크로마토그래피 액세서리 및 소모품 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Chromatography Accessories And Consumables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

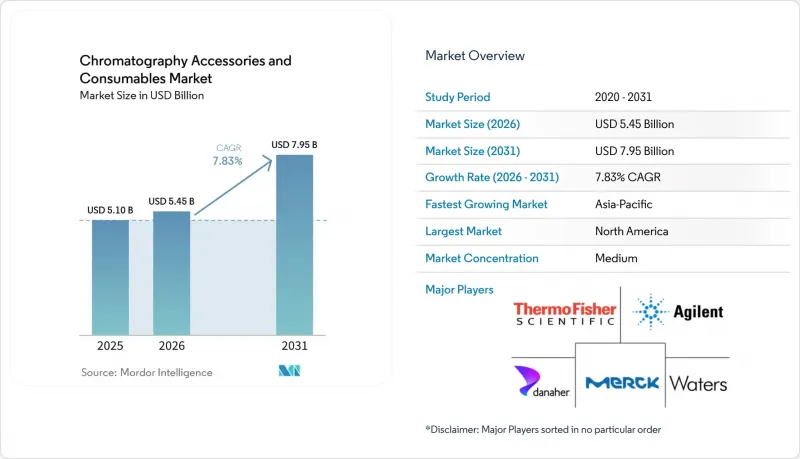

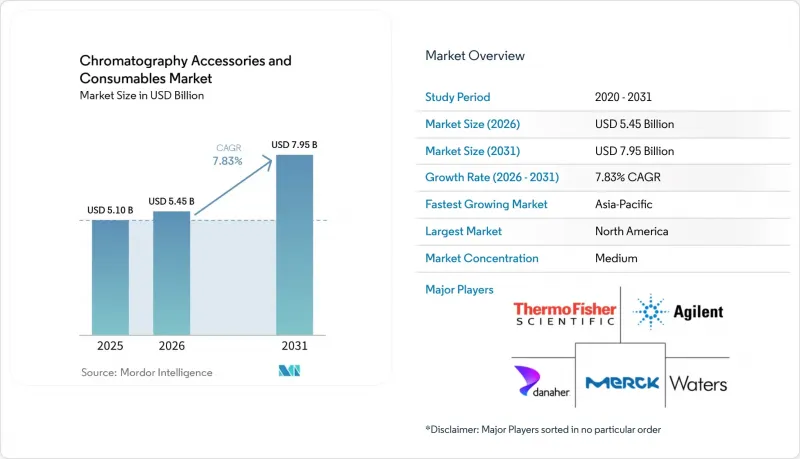

Mordor Intelligence에 의하면, 크로마토그래피 액세서리 및 소모품 시장 규모는 2025년 51억 달러로 평가되었습니다. 2026년에는 54억 5,000만 달러로 확대되어 2031년까지 79억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 7.83%로 성장할 전망입니다.

본 보고서는 제품별(컬럼 및 가드 컬럼, 시료 전처리, 필터 등), 크로마토그래피 유형별(액체, 기체, 이온, 기타), 최종 사용자별(제약, 생명공학, CRO 및 CDMO 등), 용도별(신약 개발 및 전임상, 제약 제조 분야의 QA/QC 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 크로마토그래피 액세서리 및 소모품 시장 동향 및 인사이트

바이오의약품 파이프라인 확대와 GMP 분석 수요 증가가 LC/GC 소모품에 대한 지속적인 수요를 견인하고 있습니다.

유전자 치료, mRNA 백신, 항체-약물 복합체(ADC)와 같은 복잡한 치료법에서는 배치마다 여러 차례의 크로마토그래피 분석이 필요하기 때문에 컬럼 교체 빈도와 용매 소비량이 증가하고 있습니다. 워터스사는 2025년, 바이러스 벡터 및 지질 나노입자의 특성 평가에 최적화된 ‘BioAccord LC-MS’를 출시했습니다. 이 시스템은 특수한 역상 컬럼 및 크기 배제 컬럼을 사용하여, 저분자 품질 관리(QC) 시험에 비해 최대 5배 빠른 속도로 분석을 수행합니다. 아길렌트의 ‘AdvanceBio’ 올리고뉴클레오티드 컬럼은 2024년에 상용화되었으며, 안티센스 및 siRNA 치료제를 대상으로 고분해능 분리를 실현하고 있어, 범용 C18 상에 비해 20% 높은 가격 프리미엄이 책정되어 있습니다. 수탁 제조업체는 의뢰사 수요에 부응하기 위해 생산 능력을 확대되고 있습니다. 2026년에 개장 예정인 론자의 10억 달러 규모 스타인 시설에는 프리팩 컬럼과 일회용 플로우 패스를 지속적으로 소비하는 여러 개의 GMP 스위트가 설치될 예정입니다. 삼성바이오로직스는 2025년에 78만 4,000리터의 바이오리액터 용량을 보고했으며, 이는 검증 완료된 공급업체 목록에 포함된 하류 정제용 소모품에 대한 수요가 선형적으로 증가할 것임을 시사합니다.

식품 안전 및 환경 시험에 대한 규제 강화로 처리 능력 확대

2024년 12월에 발효된 미국 FDA의 LAAF 프로그램은 미코톡신 및 알레르겐 검사에서 ISO/IEC 17025 인증을 의무화하고 있으며, 이에 따라 인증 표준 물질 및 추적성 대응 컬럼에 대한 주문이 증가하고 있습니다. 유럽 규정 2025/854에 따라, 2026-2028년 주기 필수 모니터링 목록에 27종의 농약 잔류물이 추가됨에 따라, 검사 기관은 QuEChERS 키트와 대용량 분석 컬럼에 의존하는 다중 잔류 LC-MS/MS 분석법의 도입을 피할 수 없게 되었습니다. Eurofins 및 SGS와 같은 세계 네트워크는 수백 개의 연구소에 걸쳐 소모품을 표준화하고, 감사 및 분석법 이전을 효율화하는 한편, 승인된 소수공급업체에 지출을 집중하고 있습니다. 2024년에 공표된 미국 환경보호청(EPA)의 법적 구속력이 있는 PFAS 규제 기준에 따라, 공급업체들은 PFAS가 포함되지 않은 하드웨어를 제공해야만 했습니다. 애지런트는 새로운 소모품 하위 부문을 개척하는 오염이 없는 변환 키트를 출시했습니다. ECHA의 2025년판 요람에는 REACH 규정 시행을 위한 LC-MS/MS 및 SPE 요건이 명시되어 있으며, 바이알, SPE 카트리지, 추출용 흡착제의 유럽연합 전역에서 수요 증가가 규정되었습니다.

범용 바이알 및 필터의 상품화와 가격 압박으로 인해 평균 판매 가격(ASP)이 억제되고 있습니다.

2mL 오토샘플러 바이알이나 0.45µm 주사기 필터 등 대량 판매 SKU의 경우, ISO-9001 인증 부품을 20-30% 할인된 가격으로 공급하는 중국 및 인도 제조업체들이 시장에 진입하면서 다국적 공급업체들의 이익률을 압박하고 있습니다. 학술 연구 기관이나 환경 검사 기관은 최저가 입찰자에게 발주하기 때문에 프리미엄 브랜드라 하더라도 평균 판매 가격(ASP)이 하락하고 있습니다. 세계의 주요 기업들은 판매량을 유지하기 위해 소모품을 서비스 계약이나 장비 구매와 함께 묶어 판매하고 있지만, 할인으로 인해 매출 총이익이 압박받고 있습니다. 머크 KGaA는 GMP 용도 분야에서 프리미엄 위치를 유지하고 있지만, 일상적인 시험 분야에서는 저비용 대체품에 시장 점유율을 빼앗기고 있습니다. 전자상거래 플랫폼의 확대에 따라 구매자들은 실시간으로 가격을 비교할 수 있게 되었으며, 상품화된 부문에서의 경쟁이 치열해지고 있습니다.

부문별 분석

컬럼 및 가드 컬럼은 2025년 매출의 28.5%를 차지하며, 액체 및 기체 분리 분야에서 가장 고부가가치 일회용 제품으로서의 입지를 확고히 다졌습니다. 컬럼 관련 크로마토그래피 액세서리 및 소모품 시장 규모는 2025년에 14억 6,000만 달러에 달했으며, 연구소에서 최상의 성능을 확보하기 위해 교체 주기를 단축함에 따라 꾸준히 확대될 것으로 전망됩니다. 필터는 단가가 낮은 제품이며, 배치별로 무균 상태로 사전 검증이 완료된 멤브레인 유닛이 필요한 일회용 바이오프로세스 라인 덕분에 연평균 성장률(CAGR) 8.43%로 성장할 전망입니다. 각 벤더사는 혁신적인 고정상 화학 기술을 활용하여 컬럼을 차별화하고 있습니다. Restek사의 Raptor ARC-18 컬럼은 기존의 C18 상으로는 대응하기 어려운 산성 및 염기성 시약에 대응할 수 있으며, 수명을 희생하지 않으면서도 가격 경쟁력을 확보하고 있습니다. 한편, 범용 바이알 공급업체들이 일반 상품 시장에 진출함에 따라 이익률은 압박을 받고 있지만, 특히 학술 기관을 대상으로 한 조달 채널에서는 총 판매량이 증가하고 있습니다. UHPLC의 도입 확대에 따라 튜브와 피팅 시장도 성장하고 있습니다. 이는 고압 대응이나 저분산 형상 같은 요건을 저비용 대체품으로는 충족할 수 없기 때문이며, 틈새 시장 부품 제조업체의 경우 높은 투자자본이익률(ROIC)이 유지되고 있습니다.

애지런트가 Poroshell 120 HILIC-OH5 및 PFP 상을 출시한 것은 PFAS 및 올리고뉴클레오티드 분리 등 새로운 분석 과제를 해결하는 용도 특화형 소모품으로의 전환을 보여줍니다. 워터스사는 단백질체학용 ‘ionKey/MS’를 통해 이 전략을 보완하고 있습니다. 이 제품은 용매 폐기량을 99% 줄여주는 마이크로플루이딕스 카트리지로, 수명이 짧은데도 불구하고 800-1,200달러에 판매되어 프리미엄 지속적 수익 모델을 강화하고 있습니다. 한편, 오토샘플러용 바이알, 캡 및 마개는 심각한 상품화 현상에 직면해 있으며, 브랜드 제조업체들은 제네릭 진출기업들이 쉽게 재현할 수 없는 추적성, 인증된 청정도 및 스마트 태그 기능에 주력해야 하는 상황에 놓여 있습니다. 용매 및 완충액은 여전히 규모는 크지만 이익률이 낮은 분야이며, 수직 통합, 물류 규모 및 대량 계약이 수익성을 좌우하고 있습니다.

액체 분석 플랫폼은 2025년 지출의 57.38%를 차지했으며, 이는 의약품 방출 시험, 식품 잔류물 모니터링 및 대사체 프로파일링 분야에서 규제 당국이 LC-UV 및 LC-MS에 의존하고 있다는 점에 기인합니다. LC-MS 워크플로우에서는 시험 1건당 더 많은 컬럼을 소모하고, 분석용 등급의 동급 제품에 비해 가격이 2배인 MS 등급 용매가 필요하기 때문에 액체 분석법용 크로마토그래피 액세서리 및 소모품 시장 점유율은 확대될 것으로 예측됩니다. 가스 크로마토그래피는 휘발성 유기 화합물이나 석유 화학 물질의 분석 분야에서 여전히 중요한 위치를 차지하고 있지만, 환경 규제가 LC-MS/MS를 이용한 분석이 가장 적합한 다중 잔류 농약 및 PFAS 분석 방식으로 전환됨에 따라, 이 장비의 성장률은 LC에 뒤처지고 있습니다.

기존에는 틈새 분야였던 이온 크로마토그래피는 미국 및 유럽의 규제 당국이 수중 PFAS에 대해 1조분의 1 수준(ppt)의 기준치를 설정함에 따라 새로운 중요성을 띠게 되었습니다. 이에 따라, 서모피셔사의 ICS-7000 Plus와 원활하게 연동되는 서프레서 카트리지, 용리액 재생 장치 및 특수 컬럼의 구매가 촉진되고 있습니다. 2025년에 출시된 시마즈 제작소의 Nexera IC-40은 고감도 검출기를 컴팩트한 본체에 탑재함으로써, 중규모 연구소에서의 이온 분석 보급을 한층 더 촉진하고 있습니다. 초임계 유체 크로마토그래피는 매출의 2% 미만에 그치고 있지만, 용매 폐기량 감축이 기업의 지속가능성 방침과 부합하기 때문에 제약 분야의 정제 과정에서 성장세를 보이고 있습니다. 이처럼 분리 방식이 다양해짐에 따라, 크로마토그래피 액세서리 및 소모품 시장은 기술 대체 위험의 영향을 덜 받게 되었습니다.

지역별 분석

북미는 2025년 매출의 42.45%를 차지했습니다. 이는 미국이 FDA 규제 대상 의약품 생산을 집중하고 있으며, CRO 및 표준 시험소와 긴밀한 네트워크를 구축하고 있기 때문입니다. FDA가 바코드가 부착된 소모품을 권장하는 전자 기록에 관한 지침을 공식 발표한 후, 기기 업그레이드가 가속화되었고 자체 브랜드의 보급이 촉진되었습니다. 캐나다 환경 당국은 2025년에 엄격한 PFAS 지침을 채택했으며, 이에 따라 공공 연구소의 LC-MS/MS 장비 현대화를 위한 주 정부의 자금 지원이 시작되면서 소모품 수요가 더욱 확대되었습니다.

유럽은 시장 규모 면에서 2위를 차지하며, 지속가능성 분야의 동향을 주도하고 있습니다. EMA의 ICH Q3D 지침은 소량 분리를 권장하고 있으며, 용매 폐기량을 최대 90%까지 줄일 수 있는 내경 1.0mm 컬럼의 채택을 장려하고 있습니다. 독일, 프랑스, 북유럽 국가들의 연구소에서는 수명주기 평가를 조달 과정에 반영하여 재활용 포장재와 마이크로플로우 장비를 우선적으로 채택하고 있습니다. 농약 잔류물에 관한 EU 규정 2025/854에 따라, 공인 검사 기관의 LC-MS/MS 연간 분석 횟수가 최소 30% 증가해야 하며, 이는 컬럼 회전율 상승 및 고순도 용매 주문 증가로 이어집니다. 동유럽에서는 수질 개선을 목적으로 하는 공동 기금의 지원금을 통해 PFAS(퍼플루오로알킬 물질) 분석에 이온 크로마토그래피를 도입하는 움직임이 빠르게 확산되고 있습니다.

아시아태평양은 성장의 원동력이 되고 있으며, 중국과 인도가 바이오시밀러 및 백신 생산 능력을 확대함에 따라 2031년까지 연평균 성장률(CAGR)은 8.48%로 성장을 지속하고, 있습니다. 애지런트는 2025년 5월, 인도 마네사르에 1만 2,500제곱피트 규모의 솔루션 센터를 개설하고, UHPLC 및 LC-MS 유지보수에 관한 사용자 교육을 실시함으로써, 후공정 소모품에 대한 수요 증가를 공고히 하고 있습니다. 지역 벤처 캐피털의 지원을 받은 중국의 국내 시약 제조업체는 200달러 미만의 C18 컬럼으로 2선 도시 시장에 진출하며 경쟁 구도를 새롭게 바꾸고 있습니다. 일본은 정밀 기기 수출을 통해 수요를 뒷받침하고 있는 반면, 호주의 PFAS 정화 프로그램은 이온 크로마토그래피 및 SPE 카트리지의 현지 도입을 촉진하고 있습니다.

남미는 수출 인증을 위해 다중 농약 잔류물 검사에 의존하는 브라질의 농업 관련 산업에 힘입어 한 자릿수 중반의 성장률을 보이고 있으며, 이는 QuEChERS 키트 및 GC 라이너의 구매를 촉진하고 있습니다. 중동에서는 석유화학 산업의 다각화가 호재로 작용하고 있습니다. 시마즈 제작소는 2024년, 두바이에 위치한 3,800제곱미터 규모의 통합 시설을 확장하고, 정유시설용도로 사전 설정된 GC 시스템을 제공함으로써 세프타 및 라이너에 대한 지역 수요를 끌어올리고 있습니다. 아프리카 시장은 아직 발전 단계에 있지만, 다국적 광업 및 음료 기업들이 유럽의 품질 보증(QA) 프로토콜을 준수하는 컴플라이언스 연구소를 설립함에 따라 점차 성장세를 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the chromatography accessories and consumables market size is expected to increase from USD 5.10 billion in 2025 to USD 5.45 billion in 2026 and reach USD 7.95 billion by 2031, growing at a CAGR of 7.83% over 2026-2031.

This report is Segmented by Product (Columns & Guard Columns, Sample Preparation, Filters, and More), Chromatography Type (Liquid, Gas, Ion, Others), End User (Pharmaceutical, Biotechnology, Cros & CDMOs, and More), Application (Drug Discovery & Preclinical, QA/QC in Pharmaceutical Manufacturing, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Chromatography Accessories And Consumables Market Trends and Insights

Biopharma Pipeline Expansion And Rising GMP Analytics Drive Recurring LC/GC Consumable Demand

Complex modalities such as gene therapies, mRNA vaccines, and antibody-drug conjugates require multiple chromatographic assays per batch, raising column replacement frequency and solvent consumption. Waters launched the BioAccord LC-MS in 2025, optimized for viral-vector and lipid-nanoparticle characterization, which uses specialized reversed-phase and size-exclusion columns at up to five times the rate of small-molecule QC tests. Agilent's AdvanceBio oligonucleotide columns, commercialized in 2024, deliver high-resolution separation for antisense and siRNA therapeutics and command 20% price premiums over generic C18 phases. Contract manufacturers scale capacity to meet sponsor demand; Lonza's USD 1 billion Stein facility opening in 2026 will house multiple GMP suites that consume prepacked columns and single-use flow paths continuously. Samsung Biologics reported 784,000 liters of bioreactor capacity in 2025, implying linear growth in downstream purification consumables locked into validated vendor lists.

Regulatory Stringency In Food Safety And Environmental Testing Expands Throughput

The U.S. FDA's LAAF program, effective December 2024, obliges ISO/IEC 17025 accreditation for mycotoxin and allergen testing, accelerating orders for certified reference materials and traceability-enabled columns. European Regulation 2025/854 adds 27 pesticide residues to the mandatory monitoring list for the 2026-2028 cycle, forcing laboratories to adopt multi-residue LC-MS/MS methods that rely on QuEChERS kits and high-capacity analytical columns. Global networks such as Eurofins and SGS standardize consumables across hundreds of labs to streamline audits and method transfer, concentrating spend with a handful of approved suppliers. The U.S. EPA's enforceable PFAS limits promulgated in 2024 pushed vendors to offer PFAS-free hardware; Agilent delivered a contamination-free conversion kit that opened a new consumables sub-segment. ECHA's 2025 compendium spelled out LC-MS/MS and SPE requirements for REACH enforcement, codifying pull-through of vials, SPE cartridges, and extraction sorbents across the European Union.

Commoditization And Price Pressure In Generic Vials And Filters Constrain ASPs

High-volume SKUs such as 2 mL autosampler vials and 0.45 µm syringe filters attract Chinese and Indian producers offering ISO-9001 certified parts at 20-30% discounts, eroding multinational vendor margins. Academic research and environmental labs award tenders to the lowest bid, reducing average selling prices (ASPs) even for premium brands. Global giants bundle consumables with service contracts or instrument purchases to defend volume, but discounts compress gross profit. Merck KGaA maintains premium positioning in GMP applications, yet loses share in routine testing to lower-cost alternatives. As e-commerce platforms expand, buyers compare prices in real time, intensifying competition in commoditized segments.

Other drivers and restraints analyzed in the detailed report include:

- Installed-Base Upgrades To UHPLC/LC-MS Boost Pull-Through Of Columns, Vials, And Solvents

- Vendor-Integrated Ecosystems With Smart Consumables Increase Lock-In

- Supply Volatility In High-Purity Solvents And Silica Extends Lead Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Columns & Guard Columns delivered 28.5% of 2025 revenue, cementing their role as the highest-value disposables in liquid and gas separations. The chromatography accessories and consumables market size for columns reached USD 1.46 billion in 2025 and is forecast to climb steadily as laboratories shorten replacement cycles to ensure peak performance. Filters, although lower in ticket price, are set to rise at an 8.43% CAGR due to single-use bioprocessing lines that require sterile, pre-validated membrane units before every batch. Vendors differentiate columns through novel stationary-phase chemistries; Restek's Raptor ARC-18 column addresses acidic and basic drugs where legacy C18 phases falter, commanding price premiums without sacrificing lifetime. Meanwhile, generic vial suppliers crowd the commodity end, dragging margins but expanding overall unit volume, especially in academic procurement channels. Tubing and fittings grow in tandem with UHPLC deployment because high-pressure ratings and low-dispersion geometries cannot be met by low-cost substitutes, sustaining high return on invested capital for niche component makers.

Agilent's roll-out of Poroshell 120 HILIC-OH5 and PFP phases speaks to a shift toward application-specific consumables that solve emerging analytical pain points like PFAS or oligonucleotide separations. Waters complements this strategy with ionKey/MS for proteomics, a microfluidic cartridge that trims solvent waste by 99% yet sells at USD 800-1,200 despite shorter lifetimes, reinforcing a premium recurring model. Conversely, autosampler vials, caps, and closures face intense commoditization, pushing branded players to focus on traceability, certified cleanliness, and smart-tag features that generic entrants cannot easily replicate. Solvents and buffers remain a large but low-margin pool where vertical integration, logistics scale, and bulk contracts dictate profitability.

Liquid platforms accounted for 57.38% of 2025 spend, underpinned by regulatory reliance on LC-UV and LC-MS for drug release testing, food residue monitoring, and metabolite profiling. The chromatography accessories and consumables market share for liquid methods is projected to widen because LC-MS workflows consume more columns per study and require MS-grade solvents that sell at double the price of analytical-grade equivalents. Gas chromatography maintains relevance in volatile organic compound and petrochemical assays, yet unit growth lags LC as environmental regulations skew toward multi-residue pesticide and PFAS methods best handled by LC-MS/MS.

Ion chromatography, historically a niche, is enjoying new relevance after U.S. and European agencies set parts-per-trillion PFAS limits in water, driving purchases of suppressor cartridges, eluent regenerators, and specialty columns that integrate seamlessly with Thermo Fisher's ICS-7000 Plus. Shimadzu's Nexera IC-40, launched in 2025, further democratizes ion analysis for mid-sized labs by packaging high-sensitivity detectors with compact footprints. Supercritical fluid chromatography, though below 2% of revenue, grows in pharma purification because reduced solvent disposal aligns with corporate sustainability mandates. Such diversification across separation modes insulates the chromatography accessories and consumables market from technology substitution risk.

Geography Analysis

North America contributed 42.45% of 2025 revenue as the United States concentrates FDA-regulated pharmaceutical output and houses a dense network of CROs and reference labs. Instrument upgrades gained pace after the FDA formalized electronic-record guidance that favors barcoded consumables, accelerating proprietary pull-through. Canada's environmental authorities adopted stringent PFAS guidelines in 2025, triggering provincial funding for LC-MS/MS modernization in public laboratories, further enlarging consumables demand.

Europe ranks second by value and leads sustainability trends. EMA's ICH Q3D guideline incentivizes low-volume separations, pushing adoption of 1.0 mm internal-diameter columns that trim solvent waste by up to 90%. Laboratories in Germany, France, and the Nordics integrate life-cycle assessments into procurement, prioritizing recycled packaging and microflow devices. EU Regulation 2025/854 on pesticide residues compels at least 30% more annual LC-MS/MS runs across official control labs, translating into higher column turnover and higher purity solvent orders. Eastern Europe shows fast take-up of ion chromatography for PFAS thanks to cohesion-fund grants earmarked for water-quality improvements.

Asia-Pacific is the growth engine, posting an 8.48% CAGR through 2031 as China and India scale biosimilar and vaccine capacity. Agilent inaugurated a 12,500 sq ft Solution Center in Manesar, India, in May 2025 to train users on UHPLC and LC-MS maintenance, cementing downstream consumables pull-through. Chinese domestic reagent makers, backed by local venture capital, penetrate tier-two city markets with sub-USD 200 C18 columns, reshaping competitive dynamics. Japan supports demand through precision equipment exports, while Australia's PFAS remediation programs fuel local adoption of ion chromatography and SPE cartridges.

South America grows at mid-single digits led by Brazil's agribusiness, which relies on multi-residue pesticide testing for export certification, driving purchases of QuEChERS kits and GC liners. The Middle East benefits from petrochemical diversification; Shimadzu expanded a 3,800 m2 integration facility in Dubai in 2024 to deliver GC systems pre-configured for refinery applications, pushing regional demand for septa and liners. Africa remains nascent but gains incremental momentum as multinational mining and beverage firms establish compliance labs that mirror European QA protocols.

- Agilent Technologies

- Avantor

- Bio-Rad Laboratories

- Biotage

- Danaher

- Daicel Chiral Technologies

- GL Sciences Inc.

- Hamilton Company

- Imtakt Corporation

- KNAUER Wissenschaftliche Gerate GmbH

- MACHEREY-NAGEL GmbH & Co. KG

- Merck

- Metrohm

- PerkinElmer

- Phenomenex, Inc.

- Regis Technologies, Inc.

- Restek

- Sartorius

- Shimadzu

- Thermo Fisher Scientific

- Tosoh

- Trajan Scientific and Medical

- VICI

- Waters Corporation

- YMC Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Biopharma Pipeline Expansion and Rising GMP Analytics Drive Recurring LC/GC Consumable Demand

- 4.2.2 Regulatory Stringency in Food Safety and Environmental Testing Expands Test Volumes and Lab Throughput

- 4.2.3 Installed-Base Upgrades to UHPLC/LC-MS Boost Pull-Through of Columns, Vials, Filters, And Solvents

- 4.2.4 Vendor-Integrated Ecosystems with Smart/Barcoded Consumables Increase Lock-In and Repeat Purchases

- 4.2.5 Green Chromatography Spurs Demand for New Low-Volume SKUs

- 4.2.6 Outsourced R&D/QA to CROs/CDMOs Concentrates Spend with Standardized Consumables Lists

- 4.3 Market Restraints

- 4.3.1 Commoditization and Price Pressure in Generic Vials/Filters Constrain ASPs

- 4.3.2 Supply Volatility in High-Purity Solvents/Silica Media Extends Lead Times and Safety Stocks

- 4.3.3 Alternative Direct MS/Ambient Ionization Workflows Can Bypass Separations in Niche Use-Cases

- 4.3.4 Lab Sustainability Mandates Penalize Single-Use Plastics, Tightening Demand in Disposables

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Columns & Guard Columns

- 5.1.2 Sample Preparation

- 5.1.3 Filters

- 5.1.4 Vials, Caps, Closures, Well Plates

- 5.1.5 Tubing, Fittings, Ferrules, Unions, Valves

- 5.1.6 Solvents, Buffers, Adsorbents

- 5.1.7 GC Supplies

- 5.1.8 Autosampler & Detector Accessories

- 5.1.9 Calibration & Derivatization Reagents

- 5.1.10 Column Hardware & Packing Materials

- 5.2 By Chromatography Type

- 5.2.1 Liquid Chromatography (HPLC, UHPLC)

- 5.2.2 Gas Chromatography

- 5.2.3 Ion Chromatography

- 5.2.4 Others (Size-Exclusion Chromatography, Affinity Chromatography, Chiral Chromatography, etc.)

- 5.3 By End User

- 5.3.1 Pharmaceutical Companies

- 5.3.2 Biotechnology Companies

- 5.3.3 CROs & CDMOs

- 5.3.4 Academic & Research Institutes

- 5.3.5 Clinical & Diagnostic Laboratories

- 5.3.6 Others (Food & Beverage Testing Labs, Environmental Testing Laboratories, Forensics & Public Safety Labs, etc.)

- 5.4 By Application

- 5.4.1 Drug Discovery & Preclinical

- 5.4.2 QA/QC in Pharmaceutical Manufacturing

- 5.4.3 Biologics & Bioprocess Analytics

- 5.4.4 Clinical Diagnostics & Therapeutic Drug Monitoring

- 5.4.5 Food Safety & Quality

- 5.4.6 Others (Environmental Monitoring, Forensics & Toxicology, Specialty Chemicals & Petrochemicals, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Agilent Technologies, Inc.

- 6.3.2 Avantor, Inc.

- 6.3.3 Bio-Rad Laboratories, Inc.

- 6.3.4 Biotage AB

- 6.3.5 Danaher Corporation (Cytiva)

- 6.3.6 Daicel Chiral Technologies

- 6.3.7 GL Sciences Inc.

- 6.3.8 Hamilton Company

- 6.3.9 Imtakt Corporation

- 6.3.10 KNAUER Wissenschaftliche Gerate GmbH

- 6.3.11 MACHEREY-NAGEL GmbH & Co. KG

- 6.3.12 Merck KGaA

- 6.3.13 Metrohm AG

- 6.3.14 PerkinElmer, Inc.

- 6.3.15 Phenomenex, Inc.

- 6.3.16 Regis Technologies, Inc.

- 6.3.17 Restek Corporation

- 6.3.18 Sartorius AG

- 6.3.19 Shimadzu Corporation

- 6.3.20 Thermo Fisher Scientific Inc.

- 6.3.21 Tosoh Bioscience

- 6.3.22 Trajan Scientific and Medical

- 6.3.23 VICI

- 6.3.24 Waters Corporation

- 6.3.25 YMC Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment