|

시장보고서

상품코드

2063786

미국의 단풍시럽뇨병치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Maple Syrup Urine Disease Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

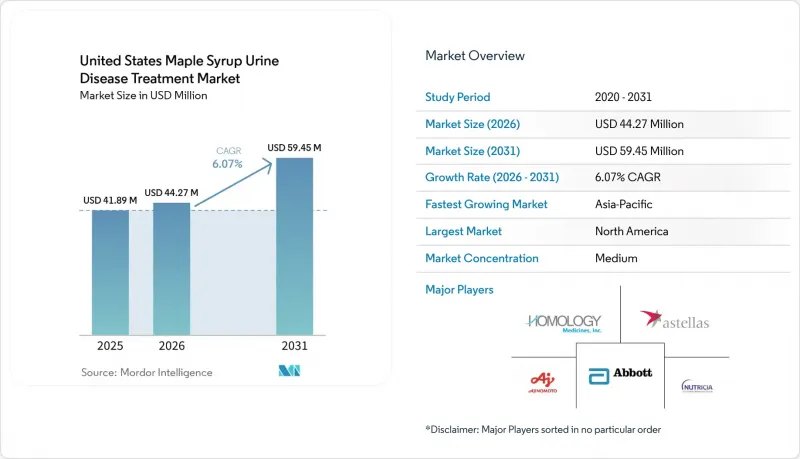

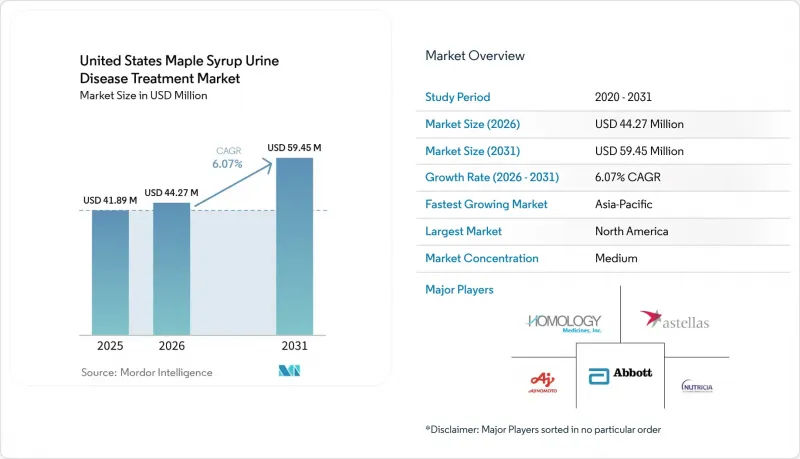

Mordor Intelligence에 의하면, 미국 단풍시럽뇨병 치료 시장 규모는 2025년에 4,189만 달러로 평가되었고 2026년 4,427만 달러에서 2031년까지 5,945만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.07%를 나타낼 전망입니다.

본 보고서는 질환의 표현형(전형, 중간형, 간헐형, 티아민 반응형), 연령대(신생아·영아, 소아, 성인) 및 유통 채널(전문 약국·의료기기 판매점, 병원 약국, 소비자 대상 직접 판매 전자상거래)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 단풍시럽뇨병 치료 시장(미국)의 동향 및 인사이트

신생아 선별검사가 MSUD 진단을 촉진합니다.

현재 미국 내 54개 관할 구역에서 출생 후 24-48시간 이내에 류신 수치 상승을 확인하는 탠덤 질량 분석법을 이용한 선별 검사가 의무화되어 있으며, MSUD는 ‘위급한 상황이 되어서야 진단되는 질환’에서 ‘일상적으로 발견되는 질환’으로 변화하고 있습니다. 조기 발견을 통해 포도당의 정맥 내 투여 및 BCAA가 포함되지 않은 조제분유의 신속한 투여가 가능해짐에 따라, 돌이킬 수 없는 신경 장애를 예방하고, 기존의 사망률을 낮추며, 평생 관리가 필요한 환자 수를 늘리고 있습니다. 2005년부터 2024년까지 루이지애나주의 등록 데이터에 따르면, 120만 명의 출생아 중 4건의 사례가 보고되었으며, 이는 전미 발병률인 18만 5,000명당 1명과 일치하여 본 프로그램의 유효성을 입증하고 있습니다. 생존 기간이 연장됨에 따라 사춘기 및 성인 대상 진료과가 환자로 꽉 차고 있지만, 성인 환자의 80%는 여전히 소아과 센터에서 치료를 받고 있어 대사질환 팀에 더 큰 부담이 가중되고 있습니다. 원격의료, 가정용 류신 측정기, 주 경계를 넘는 면허 면제 조치 덕분에 접근성은 점차 개선되고 있지만, 인력 부족은 여전히 큰 과제로 남아 있습니다.

생체 간 이식에서 생존율의 급격한 상승

미국의 단일 기관 코호트에서 최근 발표된 데이터에 따르면, 생체 간 이식 후 생존율은 100%에 달하며, 이에 따라 전형적인 표현형을 보이는 환자들은 평생 지속해 온 응급 상황 시의 식이 제한을 중단할 수 있게 되었습니다. 이종 이식체의 기증자를 활용함으로써, 대사적 위험을 수반하지 않으면서 기증자 후보의 폭이 넓어지고, 대기 목록의 대기 기간을 효과적으로 단축하고 있습니다. 이식 후에는 류신 수치가 안정되지만, 패혈증으로 인해 때때로 발생하는 위급한 상황은 스트레스 상태에서 근육 및 신장의 BCKDH 활성에 잠재적인 한계가 있음을 시사합니다. 이식 적격인 가족들이 대학병원으로 일시적으로 이사하는 사례가 늘어나면서, 주거 지원 및 장기적인 사후 관리 조정에 대한 수요가 높아지고 있습니다.

식이 요법의 높은 비용과 준수 문제

연간 인공 영양제 비용은 보충제나 응급 입원 비용을 제외하더라도 종종 1만 3,320달러를 초과합니다. 2.5개월 분량을 한 번 배송하는 데만 2,775달러 가까이 듭니다. 보험사가 류신 프리 혼합제를 보장해 주는 경우도 있지만, 발린이나 이소류신 캡슐에 대해서는 보험금 지급을 자주 거부하기 때문에 가족들은 매달 100달러가 넘는 본인 부담금을 감당해야만 합니다. 사전 승인 절차는 배송을 지연시키고, 치료 중단 위험을 높입니다. 대사 위기 시 입원 비용은 5만 달러를 초과할 수 있으며, 특히 혈장 류신 농도를 1,100µmol/L 미만으로 낮추기 위해 투석이 필요한 경우에는 비용이 매우 많이 듭니다. 주의력 결핍 장애나 실행 기능 발달 지연과 같은 인지적 문제는 소아 환자의 45.7%에게 영향을 미치고 있으며, 이로 인해 식이 요법 준수가 더욱 어려워지고 있습니다.

부문별 분석

잔존 BCKD 활성이 거의 제로이며, 평생 동안 전용 포뮬러를 사용해야 하는 ‘전형형’은 2025년 매출의 67.34%를 차지했습니다. 미국에서는 단풍시럽뇨병(MSUD)의 전형적 유형 환자를 대상으로 한 치료 시장이 제약사들에게 여전히 핵심 시장으로 자리 잡고 있습니다. 이 환자들은 섭취하는 단백질의 90% 가까이를 BCAA가 포함되지 않은 혼합물 형태로 섭취하고 있으므로, 매월 혈장 모니터링이 필요합니다. 한편, 효소 결핍이 비교적 경미한 중간형 및 간헐형 표현형의 경우, 제한적으로 완전 단백질을 섭취할 수 있거나 발병 시에만 특별식을 사용할 수 있습니다. 이로 인해 연간 제품 수요가 감소할 뿐만 아니라, 이화 스트레스가 발생할 경우 응급실 내원 건수도 증가하게 됩니다.

티아민 반응성 MSUD는 현재 비중이 작은 부문이지만, 연평균 성장률(CAGR) 7.77%라는 급격한 성장을 보이고 있습니다. 이러한 급증은 10-1,000mg 범위의 티아민 투여에 반응하는 DBT 변이를 규명하는 유전자형 및 표현형 매핑 기술의 발전에 기인한 것입니다. 앞으로, 특히 지역 클리닉에서 정밀 투여 프로토콜과 전체 엑솜 시퀀싱이 보급됨에 따라, 미국 내 티아민 반응성 MSUD 시장 점유율은 확대될 전망입니다. 또한, 각 기업은 부분적인 단백질 제한 완화에 맞추어 발린 함량이 낮은 모듈식 분말을 개발하고 있으며, 이는 대량으로 판매되고 있는 기존 제제 시장 점유율을 일부 잠식할 가능성은 있지만, 성장 잠재력을 시사하고 있습니다.

지역별 분석

지역 간 격차는 각 주의 메디케이드 정책 차이, 인구의 창립자 효과, 그리고 학술 연구 거점의 집중으로 인해 발생하고 있습니다. 펜실베이니아주, 오하이오주, 인디애나주 등 메노나이트나 아미쉬 인구가 많은 주에서는 출생 1,380건당 1건이라는 높은 발병률이 보고되고 있습니다. 이로 인해 해당 지역에서는 영양제 수요와 이식 의뢰 건수가 국지적으로 증가하고 있습니다. 반면, 인구 밀도가 낮은 마운틴 웨스트 지역의 주에서는 주 내에 대사 질환 전문의가 부족한 경우가 많아, 응급 치료를 받기 위해 가족들이 시애틀 소아병원과 같은 주요 의료 거점까지 이동할 수밖에 없는 상황이 발생하고 있습니다.

메디케이드의 급여 내용은 주마다 크게 다릅니다. 북동부 지역의 일부 주에서는 BCAA가 함유되지 않은 제품을 약국 보험 적용 품목으로 분류하여 본인 부담금을 최소화하고 있지만, 다른 주에서는 일반의약품으로 취급하고 있어 상당한 본인 부담금이 발생하고 있습니다. 2024년 클리닉 조사에 따르면, 보험이 적용되지 않는 주의 가족들은 스스로 분유 사용량을 제한할 가능성이 3배 더 높으며, 이로 인해 병세가 악화될 위험이 높아지고 있습니다. 그 결과, 미국의 단풍시럽뇨병 치료 시장에서 전자상거래의 점유율은 공적 보험 적용 범위의 사각지대와 광범위한 광대역 환경, 그리고 고용주가 제공하는 보험이 중첩되는 지역에서 가장 높게 나타났습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united states maple syrup urine disease treatment market size was valued at USD 41.89 million in 2025 and is estimated to grow from USD 44.27 million in 2026 to reach USD 59.45 million by 2031, at a CAGR of 6.07% during the forecast period (2026-2031).

This report is Segmented by Disease Phenotype (Classic, Intermediate, Intermittent, Thiamine-Responsive), Age Group (Neonates/Infants, Pediatrics, Adults), and Distribution Channel (Specialty Pharmacies & DME, Hospital Pharmacies, Direct-To-Consumer E-Commerce). The Market Forecasts are Provided in Terms of Value (USD).

Global United States Maple Syrup Urine Disease Treatment Market Trends and Insights

Newborn Screening Boosts MSUD Diagnoses

Mandatory tandem mass spectrometry panels now identify elevated leucine levels within 24 to 48 hours of birth across 54 U.S. jurisdictions, transforming MSUD from a late-crisis diagnosis to a routinely detected condition. Early detection enables the prompt initiation of intravenous dextrose and BCAA-free formulas, preventing irreversible neurological damage, reducing historical mortality rates, and increasing the number of patients requiring lifelong management. Louisiana's registry from 2005 to 2024 reported four cases among 1.2 million births, consistent with the national incidence rate of 1 in 185,000, demonstrating the program's effectiveness. While longer survival rates are filling adolescent and adult clinics, 80% of adult patients still receive care in pediatric centers, creating additional pressure on metabolic teams. Although telemedicine, at-home leucine meters, and cross-state licensure waivers are improving access, workforce shortages remain a significant challenge.

Living-Donor Liver Transplantation Sees Surge in Survival Rates

Recent data from U.S. single-center cohorts indicate a 100% survival rate following living-donor liver transplantation, enabling classic-phenotype patients to discontinue lifelong emergency dietary restrictions. The use of heterozygous parental donors has expanded the donor pool without introducing metabolic risks, effectively reducing wait-list times. While leucine levels stabilize post-transplant, occasional crises triggered by sepsis suggest potential limitations in muscle and kidney BCKDH activity during stress. An increasing number of transplant-eligible families are temporarily relocating to academic centers, driving demand for housing assistance and long-term follow-up coordination.

High Costs and Adherence Challenges of Dietary Therapy

Annual formula expenses often exceed USD 13,320, excluding supplements and emergency admissions. A single shipment lasting 2.5 months is priced at nearly USD 2,775. While insurers occasionally cover leucine-free blends, they frequently deny coverage for valine and isoleucine capsules, leading families to incur out-of-pocket expenses exceeding USD 100 monthly. The prior-authorization process delays deliveries and increases the risk of lapses. Hospitalizations during metabolic crises can cost over USD 50,000, particularly when dialysis is required to reduce plasma leucine levels below 1,100 µmol/L. Cognitive challenges, including attention-deficit disorder and executive-function delays, affect 45.7% of pediatric patients, further complicating dietary adherence.

Other drivers and restraints analyzed in the detailed report include:

- Orphan Drug Incentives and Expanded Payer Coverage

- BCKDH mRNA and Enzyme-Replacement Therapies in the Clinical Pipeline

- Limited Patient Pool Restricts Commercial Returns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Classic phenotype, driven by near-zero residual BCKD activity and a mandatory life-long formula reliance, accounted for 67.34% of 2025 revenue. In the U.S., the treatment market for classic patients with Maple Syrup Urine Disease (MSUD) remains a cornerstone for manufacturers. These patients consume nearly 90% of their protein as BCAA-free mixtures and require monthly plasma monitoring. On the other hand, intermediate and intermittent phenotypes, with milder enzymatic deficits, can either take limited intact-protein or use episodic formulas during illness. This not only reduces their annual product demand but also leads to heightened emergency-room billings during times of catabolic stress.

Thiamine-responsive MSUD, though currently a minor segment, is witnessing a growth spurt at a 7.77% CAGR. This surge is attributed to enhanced genotype-phenotype mapping, which identifies DBT variants responsive to daily thiamine doses ranging from 10 to 1,000 mg. Looking ahead, the market share for thiamine-responsive MSUD in the U.S. is poised to expand, especially as precision-dosing protocols and whole-exome sequencing gain traction in regional clinics. Companies are also developing low-valine modular powders tailored for partial protein liberalization, hinting at potential growth, even if it might cannibalize some high-volume classic formulations.

Geography Analysis

Regional disparities arise from variations in state Medicaid policies, population founder effects, and the concentration of academic centers. States with significant Mennonite or Amish populations, such as Pennsylvania, Ohio, and Indiana, report incidences as high as 1 in 380 births. This has driven localized increases in formula demand and transplant referrals. In contrast, sparsely populated Mountain West states often lack in-state metabolic specialists, prompting families to travel to major hubs like Seattle Children's Hospital for urgent care.

Medicaid coverage differs significantly across states. Several Northeastern states classify BCAA-free products as pharmacy benefits with minimal copays, while others treat them as over-the-counter supplements, resulting in substantial out-of-pocket expenses. A 2024 clinic survey indicated that families in states without coverage were three times more likely to ration formula themselves, increasing the risk of decompensation. As a result, the U.S. Maple Syrup Urine Disease treatment market's e-commerce share is highest in regions where public coverage gaps overlap with extensive broadband access and employer-sponsored insurance.

List of Companies Covered in this Report:

- Abbott Laboratories

- Astellas Pharma Inc..

- Biomarin Pharmaceutical

- BridgeBio Pharma Inc.

- Ajinomoto Cambrooke, Inc..

- DSM Nutritional Products India Private Limited

- Homology Medicines

- Kaleido Biosciences, Inc.

- Moderna Therapeutics Inc.

- Nutricia North America, Inc.

- Orpheris Inc.

- PerkinElmer

- Retrophin

- Thermo Fisher Scientific

- Travere Therapeutics Inc.

- Ultragenyx Pharmaceutical Inc.

- Vertex Pharmaceuticals Inc.

- Vitaflo USA (Nestle Health Science)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Newborn Screening-Led Rise in Diagnosed MSUD Cases

- 4.2.2 Improved Survival Rates Post-Living-Donor Liver Transplantation

- 4.2.3 Orphan-Drug Incentives & Payer Coverage Expansions

- 4.2.4 Clinical Pipeline of BCKDH mRNA & Enzyme-Replacement Therapies

- 4.2.5 Growing Awareness on Rare Metabolic Diseases

- 4.2.6 Next-Gen BCAA-Free Medical-Food Technologies

- 4.3 Market Restraints

- 4.3.1 High Lifetime Cost & Adherence Burden of Dietary Therapy

- 4.3.2 Small Patient Pool Limiting Commercial ROI

- 4.3.3 Ultra Rare Nature of The Disease

- 4.3.4 Volatile Supply of Pharma-Grade BCAA-Free Amino-Acid Inputs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Disease Phenotype

- 5.1.1 Classic

- 5.1.2 Intermediate

- 5.1.3 Intermittent

- 5.1.4 Thiamine-responsive

- 5.2 By Age Group

- 5.2.1 Neonates / Infants

- 5.2.2 Pediatrics

- 5.2.3 Adults

- 5.3 By Distribution Channel

- 5.3.1 Specialty Pharmacies & DME

- 5.3.2 Hospital Pharmacies

- 5.3.3 Direct-to-Consumer E-Commerce

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories.

- 6.3.2 Astellas Pharma Inc..

- 6.3.3 BioMarin Pharmaceutical Inc.

- 6.3.4 BridgeBio Pharma Inc.

- 6.3.5 Ajinomoto Cambrooke, Inc..

- 6.3.6 DSM Nutritional Products India Private Limited

- 6.3.7 Homology Medicines Inc.

- 6.3.8 Kaleido Biosciences, Inc.

- 6.3.9 Moderna Therapeutics Inc.

- 6.3.10 Nutricia North America, Inc.

- 6.3.11 Orpheris Inc.

- 6.3.12 PerkinElmer Inc.

- 6.3.13 Retrophin Inc.

- 6.3.14 Thermo Fisher Scientific Inc.

- 6.3.15 Travere Therapeutics Inc.

- 6.3.16 Ultragenyx Pharmaceutical Inc.

- 6.3.17 Vertex Pharmaceuticals Inc.

- 6.3.18 Vitaflo USA (Nestle Health Science)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

(주말 및 공휴일 제외)