|

시장보고서

상품코드

2063787

미국의 요소 회로 장애 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Urea Cycle Disorder Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

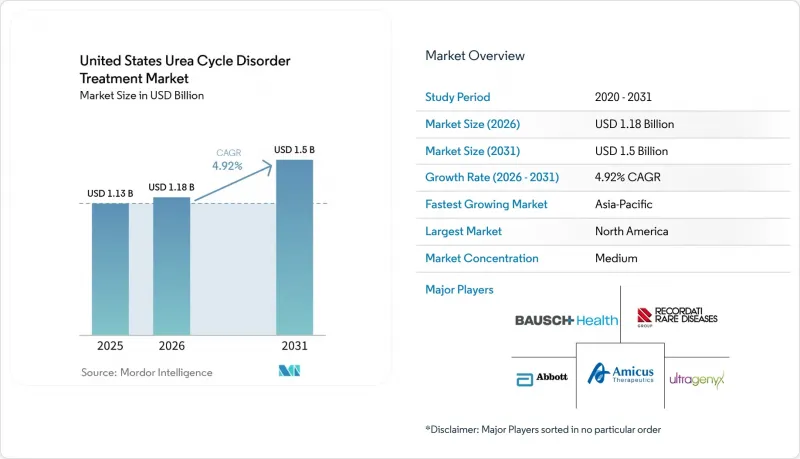

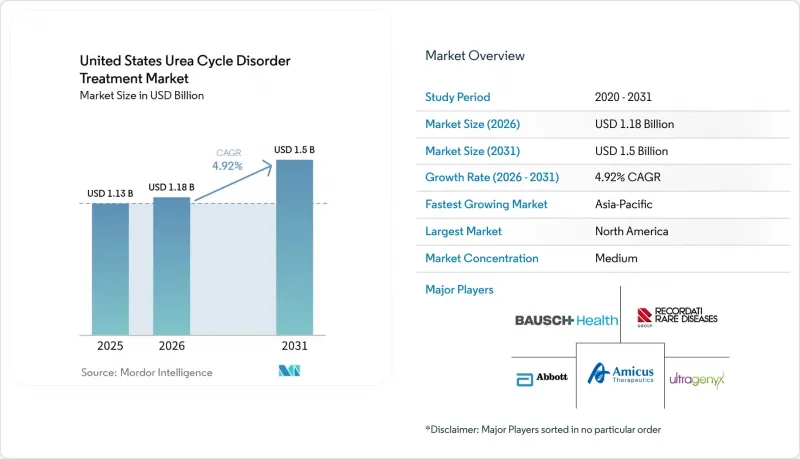

Mordor Intelligence에 의하면, 미국 요소 회로 장애 치료 시장 규모는 2025년에 11억 3,000만 달러로 평가되었고 2026년 11억 8,000만 달러에서 2031년까지 15억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.92%를 나타낼 전망입니다.

본 보고서는 치료법별(페닐부틸레이트 나트륨, 글리세롤 페닐부틸레이트, 벤조산 나트륨/페닐아세트산 나트륨, 칼글루민산, 아미노산 보충제), 효소 결핍증유형별(OTC, CPS1, AS, ASL, ARG1, NAGS 결핍증), 투여 경로별(경구, 정맥 내)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 요소 회로 장애 치료 시장에서 미국 시장 동향 및 인사이트

발병률 증가와 신생아 선별검사의 확대

미국에서는 신생아 약 3만 5,000명 중 1명꼴로, 연간 약 113명의 영아가 요소 회로 장애를 가지고 태어납니다. 기존의 탠덤 질량 분석법을 이용한 스크리닝 프로그램에서는 말단 효소 억제만 확인되었습니다. 그러나 2024년 7월, 아르기니노숙신산뇨증 및 제1형 시트룰린혈증이 ‘권장 통합 선별 검사 패널’에 추가됨에 따라, 이러한 질환의 진단 지연 기간이 최대 3개월 단축되었습니다. 오르니틴 트랜스카르바밀라제와 같은 근위형 이상은 혈장 시트룰린 농도의 감소로 인해 일반적인 선별 검사 패널에서는 검출되지 않지만, 이러한 간과로 인해 매년 약 300명의 신생아가 진단 전에 고암모니아혈증 위기의 위험에 노출되고 있습니다. 주별 대응에는 현저한 차이가 있습니다. 텍사스주는 ASA와 CIT-I를 우선시하고 있지만, 일리노이주는 4가지 말단형 질환 모두에 대한 선별 검사를 실시하고 있음에도 불구하고, 외래 진료(OTC)를 통한 확정 진단을 위한 알고리즘이 부족합니다. 2025년, 전미 요로 장애 재단은 ‘파트너 네트워크’를 도입했습니다. 이에 따라 선별 검사에서 양성 판정을 받은 환자는 72시간 이내에 대사 센터로 의뢰되게 되었으며, 기존에 존재하던 치료 연계의 공백이 해소되었습니다. 조기 진단이 이루어졌음에도 불구하고, 환자의 40%가 여전히 사망 위험에 직면해 있어, 선별 검사 항목의 확충이 시급하다는 점이 부각되고 있습니다.

FDA의 희귀질환 치료제 인센티브 및 최근 승인 현황

2026년 2월, 페그지랄기나제가 신속 승인을 획득하여 아르기닌 농도를 80% 감소시켰으며, 뚜렷한 기능적 이점을 입증했습니다. 이는 생화학적 대체 평가 지표의 활용에 있어 중요한 기준이 되었습니다. 이에 이어, Ultragenyx사의 유전자 치료제 DTX301과 iECURE사의 ECUR-506은 모두 패스트 트랙 지정을 받았으며, 현재 재생의학 첨단 치료법(Regenerative Medicine Advanced Therapy) 지위에 따라 FDA의 우선 지침 혜택을 받고 있습니다. 또한, 새틀라이트 바이오의 SB-101은 2026년 5월에 희귀 소아 질환 지정을 획득했으며, 최대 1억 5,000만 달러의 가치를 가질 수 있는 양도 가능한 바우처를 확보했습니다. 희귀질환 치료제의 독점권은 생물학적 제제와의 경쟁에 대한 완충 역할을 하지만, 독점권 만료 후 글리세롤 페닐부틸레이트의 사례에서 볼 수 있듯이, 저분자 질소 제거제의 가격이 급격히 하락하는 사례는 교훈이 됩니다. 이는 유전자 치료의 후원자에게 있어 일시적인 법적 독점권이 아니라, 지속적인 치료 성과 데이터를 바탕으로 가격을 책정하는 것이 얼마나 중요한지를 여실히 보여주고 있습니다.

고액의 치료비와 보험금 지급의 장벽

도매 가격이 1팩당 5,785달러인 라비크티는 표준 투여량 기준, 성인 1인당 연간 비용이 30만 달러를 초과합니다. 이러한 막대한 비용으로 인해 민간 보험 및 메디케이드 보험 플랜에서는 일률적인 사전 승인 제도가 도입되었습니다. 유나이티드 헬스케어의 2025년 방침에 따르면, 기존 이용자도 신규 환자와 마찬가지로 단계적 치료 프로토콜을 따라야 하므로, 제네릭 의약품을 통한 반복적인 시도가 필요하게 되어 치료 시작이 최대 3개월까지 지연될 가능성이 있습니다. 2025년 말까지 HealthWell 및 NORD와 같은 단체들이 운영하는 자선적 본인부담금 지원 프로그램이 등록 한도에 도달함에 따라, 보험 적용이 충분하지 않은 가정에 있어 필수적인 재정적 지원이 사라지게 되었습니다. 유전자 치료 비용은 1회 투여당 200만 달러 이상에 달할 것으로 예상되므로, 지급 기관은 보다 엄격한 접근 제한을 적용할 가능성이 높습니다. 이에 대응하기 위해, 스폰서는 암모니아 제어 효과의 지속성과 연계된 성과 기반 보증이나 단계적 지급 모델을 채택해야 할 수도 있습니다.

부문별 분석

2025년, 글리세롤 페닐부틸레이트는 미국의 요소 회로 장애 치료제 시장에서 52.24%의 점유율을 차지했습니다. 그러나 Endo사와 Aurobindo사가 제네릭 의약품을 출시함에 따라 브랜드 의약품의 정가는 20% 가까이 하락했습니다. 2024년 미드 존슨(Mead Johnson)사공급 충격에 따라, 아미노산 보충제 및 의료용 조제분유 미국 시장은 단백질이 포함되지 않은 칼로리 섭취를 권장하는 신생아 치료 프로토콜에 힘입어 연평균 성장률(CAGR) 4.62%로 확대되고 있습니다. 단계적 치료(스텝 테라피) 규정에 따라, 신규 치료 시작 시에는 페닐부틸레이트 나트륨이 여전히 주된 치료제로 자리 잡고 있지만, 복약 순응도 문제로 인해 환자들은 1년 이내에 글리세롤 페닐부틸레이트로 다시 전환하는 경우가 많습니다. 한편, 카르굴루민산은 NAGS 결핍증 환자라는 틈새 시장이지만 안정적인 고객층에 계속해서 기여하고 있습니다.

2차적인 영향이 조달 전략에 영향을 미치고 있습니다. 소아병원에서는 단일 공급업체에 따른 위험을 줄이기 위해 이중 조달 계약을 확대하고 있으며, 전문 약국에서는 복약 순응도 분석을 유료 서비스로 제공합니다. 제제 연구 개발(R&D)은 현재 페닐부티레이트 나트륨의 맛을 가린 마이크로캡슐에 주력하고 있으며, 가격 차이가 좁혀지는 가운데 글리세롤 페닐부티레이트가 지닌 기호성 면에서의 우위를 확보하는 것을 목표로 하고 있습니다.

지역 분석

지역 간 격차로 인해, 한 국가의 상황은 뚜렷한 마이크로마켓으로 분할되어 있습니다. 2024년 선별검사를 신속하게 시행한 일리노이주와 매사추세츠주 등에서는 원위 요로 기형(UCD)의 진단 지연이 40% 감소했습니다. 반면, 업데이트 도입이 늦어진 주에서는 여전히 기존의 지연 시간이 지속되고 있습니다. 메디케이드의 처방약 목록은 이러한 상황을 더욱 복잡하게 만들고 있습니다. 14개 주에서는 나트륨 섭취 제한이 있는 환자에게 글리세롤 페닐부틸레이트를 우선 처방 약물로 지정하고 있는 반면, 23개 주에서는 승인 전에 나트륨 페닐부틸레이트 투여가 두 차례 실패했음을 문서로 증명할 것을 요구하고 있습니다. 이러한 규제는 조제 경로에 영향을 미치고 있으며, 남부 주들에서는 뉴잉글랜드 지역에 비해 제네릭 의약품과 브랜드 의약품의 비율이 더 높습니다.

의료 종사자의 불균형한 분포는 의료 접근성 격차를 더욱 심화시키고 있습니다. 필라델피아, 보스턴, 휴스턴의 대학 병원이 3차 의료의 거점 역할을 하고 있는 반면, 다코타주에서 마운틴 웨스트에 이르는 광활한 농촌 지역에서는 생화학 유전학 전문의의 진료를 받을 수 없습니다. 2025년 캘리포니아주와 뉴욕주에서 제정된 원격의료 보험 적용 균등화법에 따라 후속 조치 준수율은 향상되었으나, 중요한 이송 관련 과제는 해결되지 않았습니다. 텍사스주에서는 이동식 ECMO와 신속 이송 네트워크를 도입함으로써 이송 시작부터 투석 시작까지의 시간을 2시간 단축하는 데 성공했으며, 이 운영 모델은 현재 메디케이드 면제 조치를 받고 있는 다른 5개 주에서도 평가가 진행되고 있습니다.

공급망의 혼란으로 인해 지역별 공급 부족이 간헐적으로 발생하고 있습니다. 2024년 미드존슨의 인디애나주 공장에서 발생한 화재로 인해 중서부 전역의 분유 공급에 차질이 빚어졌으며, 5개 병원 시스템이 FDA의 집행 재량에 따라 유럽 공급업체로부터 아미노산 혼합물을 조달하는 사태가 발생했습니다. 허리케인의 영향을 받기 쉬운 멕시코만 연안의 조제 시설에서는 페닐아세트산과 같은 특수 첨가제에 대해 이와 유사한 긴급 대책을 적극적으로 수립하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united states urea cycle disorder treatment market size was valued at USD 1.13 billion in 2025 and is estimated to grow from USD 1.18 billion in 2026 to reach USD 1.5 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031).

This report is Segmented by Treatment Type (Sodium Phenylbutyrate, Glycerol Phenylbutyrate, Sodium Benzoate/Phenylacetate, Carglumic Acid, Amino-Acid Supplements), Enzyme Deficiency Type (OTC, CPS1, AS, ASL, ARG1, NAGS Deficiencies), and Route of Administration (Oral, Intravenous). Market Forecasts are Provided in Terms of Value (USD).

Global United States Urea Cycle Disorder Treatment Market Trends and Insights

Rising Incidence & Newborn-Screening Expansion

In the U.S., approximately 1 in 35,000 births, equating to about 113 infants annually, are born with a urea-cycle defect. Historically, tandem mass-spectrometry programs only identified distal enzyme blocks. However, with the July 2024 addition of argininosuccinic aciduria and citrullinemia type I to the Recommended Uniform Screening Panel, diagnostic delays for these conditions have been reduced by up to three months. While proximal defects like ornithine transcarbamylase remain undetected by routine panels due to a drop in plasma citrulline levels, this oversight leaves around 300 newborns each year at risk of a hyperammonemic crisis before diagnosis. There's notable state-to-state variability: Texas prioritizes ASA and CIT-I, while Illinois screens all four distal disorders but lacks an algorithm for OTC confirmation. In 2025, the National Urea Cycle Disorders Foundation introduced The Partner Network, which now directs positive screens to a metabolic center within 72 hours, bridging a historical care-coordination gap. Despite early diagnoses, 40% of cases still face mortality, highlighting the urgent need for panel enhancements.

FDA Orphan-Drug Incentives & Recent Approvals

In February 2026, pegzilarginase received accelerated approval, achieving an 80% reduction in arginine levels and demonstrating clear functional benefits. This set a significant benchmark for using biochemical surrogate endpoints. Following this, Ultragenyx's DTX301 gene therapy and iECURE's ECUR-506 were both fast-tracked, now benefiting from priority FDA guidance under the Regenerative Medicine Advanced Therapy status. Additionally, Satellite Bio's SB-101 clinched the Rare Pediatric Disease designation in May 2026, earning a transferable voucher potentially worth up to USD 150 million. While orphan-drug exclusivity provides a buffer against competition for biologics, the swift price erosion of small-molecule nitrogen scavengers, exemplified by glycerol phenylbutyrate post-exclusivity, serves as a cautionary tale. This underscores the importance for gene-therapy sponsors to tether pricing to lasting outcome data rather than fleeting statutory monopolies.

High Therapy Cost & Reimbursement Hurdles

Ravicti, priced at a wholesale pack rate of USD 5,785, results in an annual expenditure exceeding USD 300,000 for adults on standard dosing. This significant cost has led commercial and Medicaid plans to implement blanket prior authorizations. UnitedHealthcare's 2025 policy requires established users to follow the same step-therapy protocol as new patients, necessitating repeated trials with generics and potentially delaying access by up to three months. By late 2025, philanthropic copay assistance programs from organizations like HealthWell and NORD reached their enrollment limits, removing critical financial support for underinsured families. With gene-therapy prices expected to exceed USD 2 million per infusion, payers are likely to impose stricter access controls. To address this, sponsors may need to adopt outcome-based guarantees or staged payment models tied to the durability of ammonia-control outcomes.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Glycerol Phenylbutyrate Orals

- Patient-Advocacy & Awareness Campaigns

- Scarcity of Metabolic Specialty Centers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Glycerol phenylbutyrate held a 52.24% share of the U.S. market for Urea Cycle Disorder treatments. However, generics from Endo and Aurobindo have reduced branded list prices by nearly 20%. Following the 2024 Mead Johnson supply shock, the U.S. market for amino-acid supplements and medical formulas is expanding at a 4.62% CAGR, driven by neonatal protocols favoring protein-free calories. While step-therapy rules maintain sodium phenylbutyrate's lead for new starts, adherence challenges often lead patients back to glycerol phenylbutyrate within a year. Meanwhile, Carglumic acid continues to serve a niche but stable group with NAGS deficiency.

Second-order effects are influencing procurement strategies: children's hospitals are broadening dual-sourcing contracts to mitigate single-supplier risks, and specialty pharmacies are offering adherence analytics as a billable service. Formulation R&D is now focusing on taste-masked microcapsules of sodium phenylbutyrate, aiming to counter glycerol phenylbutyrate's palatability advantage as price differences diminish.

Geography Analysis

Regional disparities divide a single country's landscape into distinct micro-markets. States like Illinois and Massachusetts, which quickly implemented the 2024 screening update, have achieved a 40% reduction in distal UCD diagnostic delays. In contrast, states that adopted the update later continue to experience historical lag times. Medicaid formularies further complicate this landscape: fourteen states designate glycerol phenylbutyrate as the preferred agent for patients on sodium restrictions, while twenty-three states require two documented failures of sodium phenylbutyrate before approval. These regulations influence dispensing channels, with southern states demonstrating a higher ratio of generics to branded medications compared to New England.

Workforce maldistribution intensifies access inequities. While academic centers in Philadelphia, Boston, and Houston serve as hubs for tertiary care, vast rural regions from the Dakotas to the Mountain West lack access to biochemical geneticists. Although telehealth coverage parity laws enacted in California and New York in 2025 improved follow-up adherence, they did not resolve critical transport challenges. In Texas, mobile ECMO and rapid-transfer networks have successfully reduced door-to-dialysis intervals by two hours, and this operational model is now being evaluated in five other states with Medicaid waivers.

Supply-chain disruptions create periodic regional shortages. A 2024 fire at Mead Johnson's Indiana plant disrupted formula availability across the Midwest, prompting five hospital systems to source amino-acid mixes from European suppliers under FDA enforcement discretion. Gulf Coast compounding facilities, which are vulnerable to hurricanes, are proactively planning similar contingency measures for specialized excipients like phenylacetic acid.

List of Companies Covered in this Report:

- Abbott Laboratories

- Aeglea BioTherapeutics Inc.

- Amicus Therapeutics Inc.

- Arcturus Therapeutics Holdings Inc.

- Bausch Health

- Biomarin Pharmaceutical

- Danone

- Erytech Pharma

- Eurocept Pharmaceuticals / Lucane Pharma SA

- Horizon Therapeutics

- Immedica Pharma AB

- Mead Johnson & Company

- Nestle

- Orpharma

- PTC Therapeutics

- Recordati Rare Diseases Inc.

- Relief Therapeutics Holding AG

- Sana Biotechnology Inc.

- Selecta Biosciences Inc.

- Sobi AB

- Synlogic

- Ultragenyx Pharmaceutical Inc.

- Zevra Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence & Newborn-Screening Expansion

- 4.2.2 FDA Orphan-Drug Incentives & Recent Approvals

- 4.2.3 Adoption of Glycerol Phenylbutyrate Orals

- 4.2.4 Patient-Advocacy & Awareness Campaigns

- 4.2.5 Wearable Ammonia-Monitoring Integration

- 4.2.6 Taste-Masked Micro-Encapsulated NapB

- 4.3 Market Restraints

- 4.3.1 High Therapy Cost & Reimbursement Hurdles

- 4.3.2 Scarcity of Metabolic Specialty Centers

- 4.3.3 Supply-Chain Fragility for Niche Excipients

- 4.3.4 Viral-Vector CDMO Capacity Bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Treatment Type

- 5.1.1 Sodium Phenylbutyrate

- 5.1.2 Glycerol Phenylbutyrate

- 5.1.3 Sodium Benzoate / Phenylacetate

- 5.1.4 Carglumic Acid

- 5.1.5 Amino-acid Supplements & Specialized Formulas

- 5.2 By Enzyme Deficiency Type

- 5.2.1 Ornithine Transcarbamylase Deficiency

- 5.2.2 Carbamoyl Phosphate Synthetase 1 Deficiency

- 5.2.3 Argininosuccinate Synthetase Def. / Citrullinemia I

- 5.2.4 Argininosuccinate Lyase Deficiency

- 5.2.5 Arginase 1 Deficiency

- 5.2.6 N-Acetylglutamate Synthase Deficiency

- 5.2.7 Others

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Intravenous

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Aeglea BioTherapeutics Inc.

- 6.3.3 Amicus Therapeutics Inc.

- 6.3.4 Arcturus Therapeutics Holdings Inc.

- 6.3.5 Bausch Health Companies Inc.

- 6.3.6 BioMarin Pharmaceutical Inc.

- 6.3.7 Danone S.A. (Nutricia)

- 6.3.8 Erytech Pharma SA

- 6.3.9 Eurocept Pharmaceuticals / Lucane Pharma SA

- 6.3.10 Horizon Therapeutics plc

- 6.3.11 Immedica Pharma AB

- 6.3.12 Mead Johnson & Company, LLC

- 6.3.13 Nestle Health Science

- 6.3.14 Orpharma Pty Ltd.

- 6.3.15 PTC Therapeutics Inc.

- 6.3.16 Recordati Rare Diseases Inc.

- 6.3.17 Relief Therapeutics Holding AG

- 6.3.18 Sana Biotechnology Inc.

- 6.3.19 Selecta Biosciences Inc.

- 6.3.20 Sobi AB

- 6.3.21 Synlogic Inc.

- 6.3.22 Ultragenyx Pharmaceutical Inc.

- 6.3.23 Zevra Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment