|

시장보고서

상품코드

2063788

임상시험 최적화 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Clinical Trials Optimization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

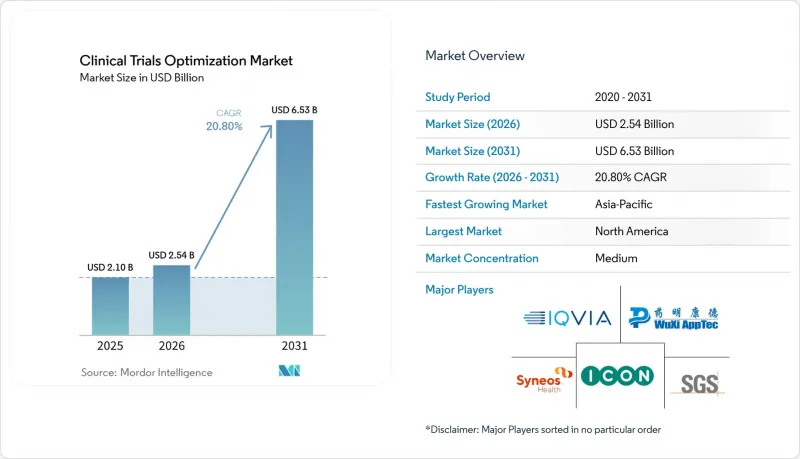

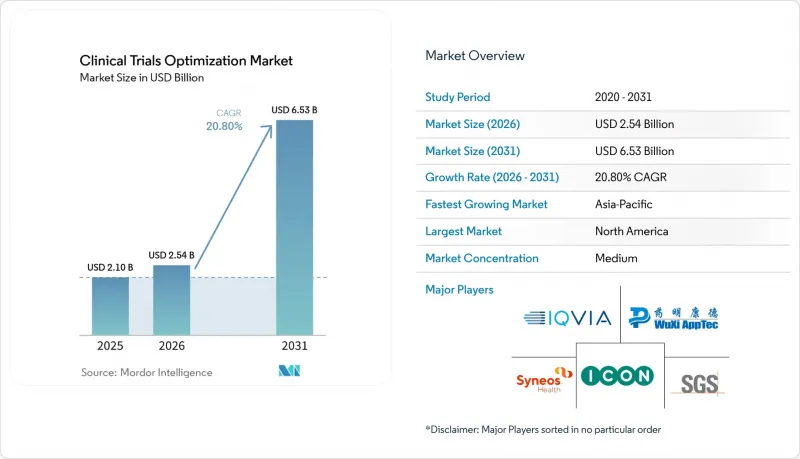

Mordor Intelligence에 의하면, 임상시험 최적화 시장 규모는 2025년 21억 달러로 평가되었습니다. 2026년에는 25억 4,000만 달러로 확대되어 2031년까지 65억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 20.80%로 성장할 전망입니다.

본 보고서는 솔루션 유형(임상 연구 서비스 등), 임상시험 단계(I, II, III, IV), 치료 분야(종양학, 순환기, 중추신경계, 감염증, 대사), 제공 모델(FSO, FSP, 하이브리드), 최종 사용자(제약, 생명공학 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 임상시험 최적화 시장 동향 및 인사이트

복잡한 임상시험을 풀서비스 CRO에 아웃소싱

스폰서들은 적응형 프로토콜에 필요한 사내 생체 인식 관련 전문 지식과 전 세계 임상시험 기관 네트워크가 부족하기 때문에 2상 및 3상 프로그램 전체를 대규모 CRO에 위탁하는 경향이 강해지고 있습니다. IQVIA가 2025년에 Flagship Pioneering과 제휴를 맺음으로써, 자체적으로 관리하는 임상시험에 비해 첫 번째 피험자 등록까지 걸리는 기간이 30% 단축되었습니다. 종양학 분야에서 바스켓 임상시험 및 엄브렐라 임상시험이 확산됨에 따라, 실시간 바이오마커를 활용한 환자군 분류의 필요성이 높아지고 있으나, 이러한 역량을 갖춘 곳은 소수의 CRO에 집중되어 있습니다. 그러나 의존 위험은 높아지고 있습니다. 일라이 릴리(Eli Lilly)는 2025년에 단일 공급업체와 데이터 품질 문제가 발생한 것을 계기로, 알츠하이머병 프로그램을 ICON과 파렉셀(Parexel) 두 회사로 분산하기로 결정했습니다. 또한, FDA의 ‘Complex Innovative Trial Designs’ 시범 프로그램에 따라 사내 팀에 대한 기술적 요건이 강화되면서 아웃소싱 추세가 더욱 가속화되고 있습니다.

분산형 및 하이브리드형 시험 모델의 도입

당초 팬데믹 대응책으로 도입된 분산형 임상시험 설계는 현재 만성 질환 및 심혈관 대사 질환 연구의 표준이 되었습니다. FDA는 2025년에 127건의 완전 원격 임상시험 프로토콜을 승인했는데, 이는 2023년 대비 3.4배 증가한 수치입니다. 의료기관에서의 정맥 주사 투여 및 영상 진단과 재택 모니터링을 결합한 하이브리드 모델이 종양학 분야에서 점차 보급되고 있습니다. 2025년 1월 영국 규제 당국이 원격 동의를 승인함에 따라, 83건의 연구에서 피험자 등록까지 소요되는 기간이 19일 단축되었습니다. 그러나 이러한 발전에는 비용 증가도 따릅니다. 현재, 후원사가 환자에 대한 수당, 재택 간호, 의료기기 배송 비용을 부담하게 됨에 따라, 초희귀질환 임상시험에서는 환자 1인당 예산이 15%-22% 증가하고 있습니다. 규제 당국의 대응은 여전히 일관성이 없으며, 일본의 PMDA는 여전히 대면 방식의 사전 동의를 의무화하고 있어, 완전히 분산화된 임상시험의 도입은 제한되고 있습니다.

다자간 규제의 파편화

국제조화회의(ICH)가 정한 지침이 있음에도 불구하고, 증거 기준이 국가마다 다르기 때문에 후원사는 병행 전략을 시행해야 합니다. FDA는 적응증 확대를 위해 실제 세계 데이터(REW)를 수용하고 있는 반면, EMA는 여전히 무작위 배정 데이터를 우선시하고 있습니다. 중국에서는 피험자의 50%를 국내 환자로 구성해야 한다는 요건이 있기 때문에 서유럽 시장에서 개발된 의약품의 경우에도 아시아 시장을 대상으로 한 별도의 시험군이 마련되도록 되어 있습니다. 일본에서는 원격 동의가 제한되어 있기 때문에 위험이 낮은 시술이라 하더라도 실제로 시설을 방문해야 합니다. 한편, 브라질의 신속 승인 절차에서도 여전히 번역된 원본 자료의 제출이 요구되고 있습니다. 가장 엄격한 규제 요건을 준수하기 위해, 후원사는 종종 과도한 피험자 등록을 실시하며, 그 결과 다지역 프로그램의 총 임상시험 비용이 최대 25% 증가하고 있습니다.

부문별 분석

2025년, 임상 연구 서비스가 총 수익의 57.34%를 차지했으며, 시설 관리, 모니터링 및 규제 당국에 대한 신청 분야에서 CRO에 대한 의존도가 여전히 지속되고 있음이 드러났습니다. 임상시험 최적화 분야의 피험자 모집 시장은 선별 검사 기간을 단축하는 AI 플랫폼에 힘입어 2031년까지 17억 9,000만 달러에 달할 것으로 전망됩니다. 데이터 플랫폼의 부상이에도 불구하고, 스폰서들은 프로토콜 수정 및 위험 기반 모니터링에 있어 여전히 인간의 판단을 우선시하고 있습니다. 임상시험 최적화 시장은 또한 종합적인 엔드투엔드 수요를 목표로 하는 찰스 리버 래버러토리즈를 통합한 IQVIA의 2026년 전략에도 부합합니다.

연평균 성장률(CAGR) 21.95%라는 견실한 성장이 예상되는 환자 모집 서비스는 규제상의 다양성 요건에 따라 다양한 집단을 정확하게 매칭하는 데 중점을 두고 있습니다. 분산형 임상시험(decentralized trial) 기술은 북미 이외의 지역에서는 여전히 틈새 시장 수준에 머물러 있지만, 일본과 중국에서 원격 동의에 대한 소극적인 태도가 이 기술의 도입을 제한하고 있습니다. 그러나 유럽에서 CTR(임상시험 규정)이 시행됨에 따라 관리상의 부담이 줄어들었고, 후원사가 기술 중심의 모니터링 체계를 도입하도록 장려되고 있습니다. 시판 후 조사 의무를 지는 후원사는 청구 데이터, 전자 기록, 환자 보고 결과를 통합하기 위해 데이터 분석 플랫폼에 대한 의존도를 높이고 있으며, 이러한 추세는 2031년까지 더욱 가속화될 것으로 예측됩니다.

2025년에는 3상 임상시험이 지출의 48.45%를 차지하며, 승인을 위한 관문으로서의 역할을 확고히 다졌습니다. 그러나 IRA(인플레이션 억제법)에 따른 가격 협상이 실제 데이터에 미치는 영향을 고려할 때, 4상 임상시험은 연평균 성장률(CAGR) 22.15%를 나타낼 것으로 예측되며, 예산이 확대될 전망입니다. 2031년까지 4상 임상시험이 임상시험 최적화 시장의 18% 이상을 차지할 것으로 예상되며, 안전성 신호 분석에 대한 수요가 증가하고 있습니다. 이 스폰서는 1상 종양학 임상시험에 바이오마커 확장 코호트를 포함시켜 개념 증명(PoC) 일정을 단축하고 있습니다.

2025년에는 프로그램의 불과 31%만이 2상에서 3상으로 진행되었지만, 탈락률이 감소함에 따라 후원사들은 위험을 줄이기 위해 더 대규모의 다군 설계 2상 임상시험을 채택했습니다. 확증적 근거가 필요한 신속 승인 절차는 파이프라인에 대한 압박을 가중시키고, 시판 후 조사의 시급성을 높이고 있습니다. 또한, 지불자로부터의 청구 데이터와 디지털 치료제의 결과를 통합하는 데이터 생태계는 임상시험 단계의 예산 구성을 변화시키고 있으며, 4상 임상시험을 단순한 규정 준수 단계에서 전략적 확장 단계로 그 위상을 높이고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 41.35%를 차지했습니다. 이는 89건의 적응형 임상시험 신청을 가속화한 FDA의 ‘Complex Innovative Trial Designs’ 시범 프로그램과, 종양학 분야의 피험자 모집 기간을 22% 단축한 NIH의 ‘TrialGPT’에 힘입은 결과입니다. 미국은 시장을 주도하고 있으며, AI를 활용한 임상시험 기관 선정 알고리즘을 강화하는 전자건강기록(EHR)의 광범위한 도입에 힘입어 전 세계 제약 연구개발비의 48%를 차지하고 있습니다. 2026년 IRA(인플레이션 억제법)에 따른 가격 협상이 실시됨에 따라, 스폰서들은 여러 적응증을 단일 프로토콜로 통합하도록 권장받고 있으며, 이로 인해 복잡성은 증가하는 반면 계약 금액은 늘어나고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 23.00%라는 견실한 성장을 달성할 것으로 전망됩니다. 이러한 성장은 중국이 2025년에 47건의 분산형 프로토콜을 승인한 것과 ICH 승인 의약품에 대한 현지 임상시험 요건이 완화된 데 힘입은 것으로, 이로 인해 국경을 넘는 임상시험 소요 기간이 40% 단축되었습니다. 인도에서는 패스트트랙 제도를 통해 심혈관 질환 및 당뇨병 치료제의 승인 기간이 18개월에서 불과 90일로 단축되었습니다. 일본의 협의 이니셔티브는 오랜 기간 해결 과제로 남아 있던 ‘의약품 출시 지연’ 문제를 해소하는 것을 목표로 하고 있지만, 원격 동의에 관한 규제가 여전히 완전한 분산화를 가로막고 있습니다. 동남아시아의 임상시험 기관들이 새롭게 참여함에 따라 환자에 대한 접근성이 확대되고, 종양학 및 대사 질환 연구 분야의 인종적·지리적 다양성이 향상되고 있습니다.

유럽에서는 2025년 임상시험 규정(CTR) 시행 이후 상당한 회복세가 나타나, 다국간 승인 절차가 18개월에서 106일로 단축되었습니다. 독일, 영국, 프랑스, 이탈리아, 스페인 등 5개국이 임상시험 개시 건수의 68%를 차지하고 있지만, GDPR(EU 개인정보보호규정) 해석의 차이로 인해 미국에서의 연구와 비교했을 때 환자 1인당 규정 준수 비용이 12%에서 18% 증가했습니다. 동유럽 국가들은 중추신경계(CNS) 및 희귀질환 연구 분야에서 비용 대비 효과가 높은 대안을 제공하고 있지만, 언어 장벽이나 데이터 보관 관련 규제 같은 과제는 여전히 남아 있습니다. 중동 및 아프리카은 아직 개발도상국 단계이지만, 계속해서 성장하고 있습니다. 사우디아라비아는 ‘비전 2030’ 이니셔티브의 일환으로 15곳의 임상시험 시설을 설립하기 위해 12억 달러를 투자하겠다고 약속했으며, 아랍에미리트(UAE)에서는 중재 임상시험 승인 건수가 3배로 증가했습니다. 남미에서는 브라질이 뎅기열 및 샤가스병에 대한 신속 승인을 통해 눈에 띄는 진전을 이루고 있는 반면, 아르헨티나에서는 문서 번역 요건으로 인해 여전히 일정이 지연되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the clinical trials optimization market size is expected to increase from USD 2.10 billion in 2025 to USD 2.54 billion in 2026 and reach USD 6.53 billion by 2031, growing at a CAGR of 20.80% over 2026-2031.

This report is Segmented by Solution Type (Clinical Research Services, Dand More), Trial Phase (I, II, III, IV), Therapeutic Area (Oncology, Cardiovascular, CNS, Infectious, Metabolic), Delivery Model (FSO, FSP, Hybrid), End User (Pharma, Biotech, and More), and Geography (North America, Europe, APAC, MEA, South America). Market Forecasts are in Value (USD).

Global Clinical Trials Optimization Market Trends and Insights

Outsourcing of Complex Trials to Full-Service CROs

Sponsors are increasingly outsourcing entire Phase II and Phase III programs to large CROs due to a lack of internal biometrics expertise and global site networks required for adaptive protocols. IQVIA's 2025 partnership with Flagship Pioneering reduced time-to-first-patient-in by 30% compared to self-managed studies.The growing prevalence of oncology basket and umbrella trials has amplified the need for real-time biomarker stratification, a capability concentrated among a limited number of CROs. However, dependency risks are increasing; Eli Lilly, following a data-quality issue in 2025 with a single vendor, opted to dual-source its Alzheimer's program between ICON and Parexel. Additionally, the FDA's Complex Innovative Trial Designs pilot has raised technical requirements for in-house teams, further driving the outsourcing trend.

Adoption of Decentralized and Hybrid Trial Models

Decentralized trial designs, initially adopted as a pandemic workaround, have now become the standard for chronic and cardiometabolic studies. The FDA approved 127 fully remote protocols in 2025, reflecting a 3.4-fold increase from 2023. Hybrid models, which combine on-site infusions or imaging with home-based monitoring, are gaining traction in oncology. The U.K. regulator's approval of remote consent in January 2025 reduced enrollment timelines by 19 days across 83 studies. However, these advancements come with increased costs, as sponsors now cover patient stipends, home nursing, and device shipping, raising per-patient budgets by 15%-22% in ultra-rare trials. Regulatory acceptance remains inconsistent, with Japan's PMDA still requiring in-person informed consent, limiting the adoption of fully decentralized trials.

Fragmented Multi-Country Regulations

Despite the guidelines set by the International Council for Harmonisation, varying evidentiary standards require sponsors to implement parallel strategies. The FDA accepts real-world evidence for label expansions, while the EMA continues to prioritize randomized data. China's requirement for 50% domestic patient enrollment has led to the creation of separate Asian arms for drugs developed in Western markets. In Japan, the restriction on remote informed consent necessitates physical site visits, even for low-risk interventions. Meanwhile, Brazil's fast-track approval process still requires translated source documents. To comply with the strictest regulatory demands, sponsors often over-enroll, increasing total trial costs by up to 25% for multiregional programs.

Other drivers and restraints analyzed in the detailed report include:

- Oncology and Rare-Disease Pipeline Expansion

- AI-Driven Analytics for Rapid Patient Recruitment

- Shortage of Experienced Biometrics Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Clinical Research Services accounted for 57.34% of total revenue, highlighting the ongoing dependence on CROs for site management, monitoring, and regulatory filings. The market for patient-recruitment services in clinical trials optimization is projected to reach USD 1.79 billion by 2031, driven by AI platforms that streamline screening timelines. Even with the rise of data platforms, sponsors continue to prioritize human judgment for protocol amendments and risk-based monitoring. The clinical trials optimization market is also responding to IQVIA's 2026 strategy to integrate Charles River Laboratories, targeting comprehensive end-to-end demand.

Patient-Recruitment Services, set for a robust 21.95% CAGR, focus on accurately matching diverse populations, in line with regulatory diversity requirements. While decentralized-trial technology remains a niche outside North America, Japan and China's reluctance on remote consent has limited its adoption. However, the implementation of CTR in Europe has reduced administrative hurdles, encouraging sponsors to adopt tech-driven oversight. Sponsors with post-marketing commitments are increasingly turning to data-analytics platforms to integrate claims, electronic records, and patient-reported outcomes, a trend expected to gain momentum through 2031.

In 2025, Phase III trials accounted for 48.45% of expenditures, solidifying their role as the gateway to licensure. Yet, with a projected CAGR of 22.15%, Phase IV is seeing budget expansions, driven by the IRA's price-negotiation implications on real-world evidence. By 2031, Phase IV studies are anticipated to capture over 18% of the clinical trials optimization market share, bolstering the demand for safety-signal analytics. Sponsors are embedding biomarker expansion cohorts in Phase I oncology trials, expediting proof-of-concept timelines.

While only 31% of programs advanced from Phase II to III in 2025, a decline in attrition rates is prompting sponsors to adopt larger, multi-arm Phase II designs to mitigate risks. Accelerated approval pathways, requiring confirmatory evidence, intensify pipeline pressures and heighten the urgency for post-marketing studies. Moreover, data ecosystems, integrating payer claims and digital therapeutic outputs, are reshaping trial-phase budgets, elevating Phase IV's status from a mere compliance step to a strategic extension.

Geography Analysis

In 2025, North America accounted for 41.35% of global revenue, driven by the FDA's Complex Innovative Trial Designs pilot, which accelerated 89 adaptive submissions, and the NIH's TrialGPT, which reduced oncology recruitment time by 22%. The U.S. leads the market, contributing 48% of global pharmaceutical R&D spending, supported by extensive electronic health record adoption that enhances AI-driven site-selection algorithms. The implementation of IRA price negotiations in 2026 is prompting sponsors to consolidate multiple indications into single protocols, increasing complexity while boosting contract value.

Asia-Pacific is projected to achieve a strong 23.00% CAGR through 2031. This growth is supported by China's 2025 approval of 47 decentralized protocols and the relaxation of local-trial requirements for ICH-approved drugs, which has reduced cross-border timelines by 40%. In India, fast-track processes have cut approval times for cardiovascular and diabetes treatments from 18 months to just 90 days. Japan's consultation initiative aims to address the longstanding "drug lag," although restrictions on remote consent continue to limit full decentralization. Emerging participation from Southeast Asian sites is expanding patient access and improving ethnogeographic diversity in oncology and metabolic studies.

Europe experienced a significant recovery following the 2025 enforcement of the Clinical Trials Regulation (CTR), which reduced the multistate approval process from 18 months to 106 days. Germany, the U.K., France, Italy, and Spain accounted for 68% of trial initiations, although variations in GDPR interpretations have increased per-patient compliance costs by 12% to 18% compared to U.S. studies. Eastern European countries offer cost-effective options for CNS and rare-disease research, though challenges such as language barriers and data custody regulations persist. The Middle East and Africa, while still developing, are expanding; Saudi Arabia has committed USD 1.2 billion to establish 15 trial sites under its Vision 2030 initiative, and the UAE has tripled interventional approvals. In South America, Brazil has made notable progress with fast-tracked approvals for dengue and Chagas, although Argentina's document-translation requirements continue to extend timelines.

- Advanced Clinical

- Allucent

- Caidya (formerly Clinipace)

- Charles River

- Fortrea Holdings Inc.

- Hangzhou Tigermed Consulting Co., Ltd.

- ICON

- IQVIA

- KCR S.A.

- LabCorp

- MedPace

- Novotech Health Holding

- Parexel International Corp.

- Premier Research Group Limited

- PSI CRO

- SGS

- Syneos Health, LLC

- Thermo Fisher Scientific

- Worldwide Clinical Trials

- WuXi AppTec Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outsourcing of Complex Trials to Full-Service CROs

- 4.2.2 Adoption of Decentralized & Hybrid Trial Models

- 4.2.3 Oncology & Rare-Disease Pipeline Expansion

- 4.2.4 AI-Driven Analytics for Rapid Patient Recruitment

- 4.2.5 Regulatory Diversity Mandates Boosting Geo-Targeted Enrolment

- 4.2.6 IRA-Driven Simultaneous-Indication Trials Accelerating Optimization Needs

- 4.3 Market Restraints

- 4.3.1 Fragmented Multi-Country Regulations

- 4.3.2 Shortage of Experienced Biometrics Talent

- 4.3.3 Escalating Cybersecurity / Data-Privacy Compliance Costs

- 4.3.4 Tariff Swings on Remote-Monitoring Hardware

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Solution Type

- 5.1.1 Clinical Research Services

- 5.1.2 Data & Analytics Platforms

- 5.1.3 Patient-Recruitment Services

- 5.1.4 Decentralised / Virtual Trial Technology

- 5.1.5 Regulatory & Medical Affairs Services

- 5.2 By Trial Phase

- 5.2.1 Phase I

- 5.2.2 Phase II

- 5.2.3 Phase III

- 5.2.4 Phase IV / Post-Marketing

- 5.3 By Therapeutic Area

- 5.3.1 Oncology

- 5.3.2 Cardiovascular

- 5.3.3 CNS Disorders

- 5.3.4 Infectious Diseases

- 5.3.5 Metabolic & Endocrine

- 5.4 By Delivery Model

- 5.4.1 Full-Service Outsourcing (FSO)

- 5.4.2 Functional Service Provider (FSP)

- 5.4.3 Hybrid / Strategic Partnership

- 5.5 End User

- 5.5.1 Pharmaceutical Companies

- 5.5.2 Biotechnology Companies

- 5.5.3 Medical-Device Manufacturers

- 5.5.4 Academic & Research Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Advanced Clinical

- 6.3.2 Allucent

- 6.3.3 Caidya (formerly Clinipace)

- 6.3.4 Charles River Laboratories International, Inc.

- 6.3.5 Fortrea Holdings Inc.

- 6.3.6 Hangzhou Tigermed Consulting Co., Ltd.

- 6.3.7 ICON plc

- 6.3.8 IQVIA

- 6.3.9 KCR S.A.

- 6.3.10 Laboratory Corporation of America Holdings (Labcorp)

- 6.3.11 Medpace Holdings Inc.

- 6.3.12 Novotech Health Holding

- 6.3.13 Parexel International Corp.

- 6.3.14 Premier Research Group Limited

- 6.3.15 PSI CRO AG

- 6.3.16 SGS SA

- 6.3.17 Syneos Health, LLC

- 6.3.18 Thermo Fisher Scientific Inc

- 6.3.19 Worldwide Clinical Trials

- 6.3.20 WuXi AppTec Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment