|

시장보고서

상품코드

2063834

규제 업무 분야 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Regulatory Affairs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

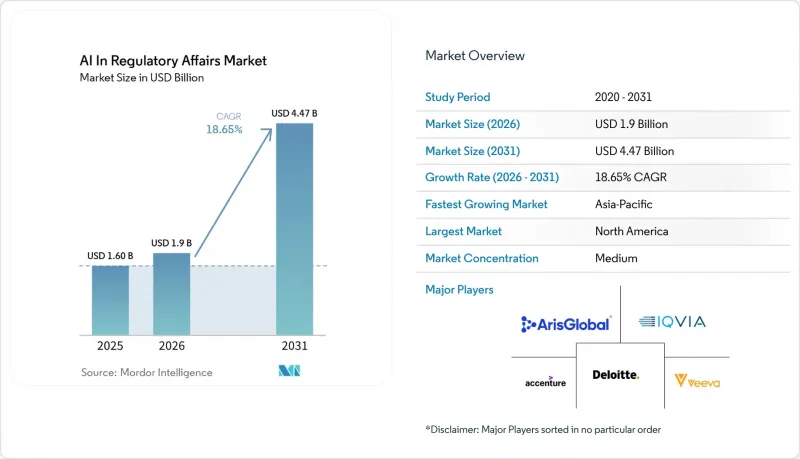

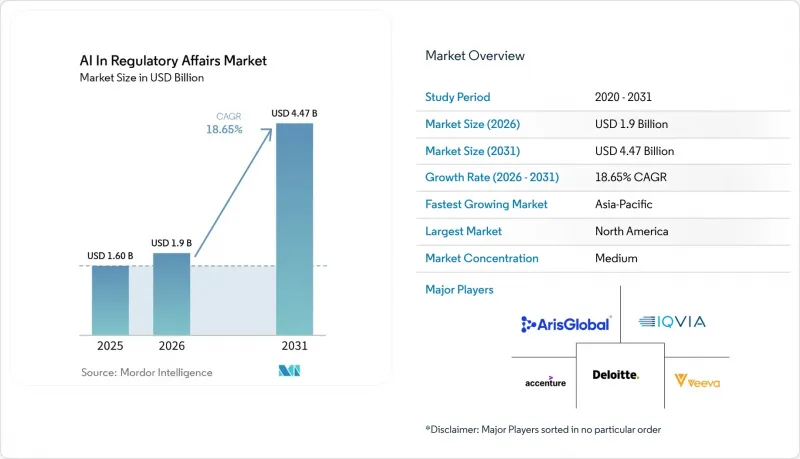

Mordor Intelligence에 의하면, 규제 업무 분야 인공지능(AI) 시장 규모는 2025년 16억 달러로 평가되었습니다. 2026년 19억 달러에서 2031년까지 44억 7,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 18.65%를 나타낼 것으로 예측됩니다.

본 보고서는 배포 모드(On-Premise, 클라우드 기반), 기술(머신러닝, 자연어 처리, RPA, 컴퓨터 비전, 지식 그래프), 용도(규제 인텔리전스, 문서 관리, 라벨링, 시판 후 조사, 기타), 최종 사용자(제약, 생명공학, 의료기기, CRO, 컨설팅, 기타), 지역별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계의 규제 업무 분야 인공지능(AI) 시장 동향 및 인사이트

제약 및 생명공학 기업에서 규제 당국에 대한 신청 절차 가속화

암, 희귀질환 및 팬데믹 대응 치료법에 대한 신속 승인 절차는 임상시험용 의약품 및 신약 허가 신청 일정을 단축하는 강력한 유인책이 되고 있습니다. 현재, 후원 기업들은 임상시험 데이터의 자동 추출, 참고문헌 검증, 전자판 공통 기술 문서(CTD) 작성을 몇 주가 아닌 몇 시간 만에 완료할 수 있는 AI 플랫폼을 도입하고 있습니다. Weave Bio와 Parexel은 2026년 4월 기준으로 신약 승인 신청(NDA) 준비 주기를 60% 단축했음을 입증하며, 조기 도입 기업들에게 측정 가능한 투자 대비 효과를 보여주었습니다. Recursion Pharmaceuticals에서도 이와 유사한 생산성 향상이 나타났으며, 이 회사의 Recursion OS를 통해 LSD1 억제제의 첫 인체 투여 준비가 기존 평균 45개월에 비해 약 20개월 만에 완료되어, 수년에 걸친 유지 비용을 절감했습니다.

여러 시장에 출시됨에 따라 전 세계적으로 라벨 변경량이 증가

미국의 구조화 제품 라벨, 유럽의 제품 요약서(SmPC), 일본의 첨부문서 등 각각 다른 규제 요건에 따라, 스폰서는 언어, 형식, 참조 채널별로 업데이트 내용을 조정해야 합니다. 단일 안전 신호만으로도 50개국에 걸친 변경이 필요할 수 있어, 수작업에 의한 조정은 출시를 분기 단위로 지연시키는 요인이 되는 경우가 많습니다. 2025년, Consainsights는 과거 라벨 템플릿과 의약품 안전성 모니터링 분류 체계를 활용하여 대규모 언어 모델을 미세 조정함으로써, 처리 시간을 70% 단축하는 동시에 AI가 생성한 초안과 당국의 승인을 받은 최종 라벨 간의 일치율을 85%로 높였습니다. 다국어 업데이트를 신속하게 진행함으로써, 세계 시장에서의 출시 시기를 일치시켜 수익 손실을 방지할 수 있습니다.

데이터 개인정보 보호 및 주권에 대한 우려가 국경을 넘는 AI 훈련 데이터 세트의 활용을 제한하고 있습니다.

유럽연합(EU), 중국, 아랍에미리트(UAE), 사우디아라비아의 데이터 주권 관련 법률로 인해 훈련 코퍼스가 분할되면서, 생명과학 기업들은 모델을 현지에서 복제할지, 아니면 연합 학습(federated learning)을 채택할지 선택해야 하는 상황에 직면해 있습니다. 예를 들어 UAE에서는 예외 기준을 충족하지 않는 한 건강 데이터의 국경 간 이전이 제한되며, 국내에서 처리하거나 비가역적인 익명화를 거쳐야 합니다. 데이터 세트가 파편화되면, 전 세계 AI 서비스가 지역 고유의 의료 용어를 해석하려고 할 때 모델의 정확도가 떨어지고, 검증 및 유지 관리 비용이 증가할 가능성이 있습니다.

부문별 분석

2025년 규제 업무 분야 인공지능(AI) 시장에서 클라우드 도입 비율은 64.15%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 20.55%로 확대되며 우위를 유지할 것으로 전망됩니다. 클라우드 기반 솔루션 분야의 규제 업무용 AI 시장 규모는 2031년까지 29억 3,000만 달러에 달할 것으로 전망됩니다. 다중 테넌트 아키텍처는 검증 및 사이버 보안 비용을 분산시키고, 기능 업그레이드를 즉시 제공하며, 재해 복구를 간소화합니다. 데이터 현지화 관련 법규가 여전히 엄격한 일본이나 독일에서는 On-Premise 구축이 계속되고 있지만, GPU 가격, 전기 요금 및 전문 DevOps 담당자의 급여가 상승함에 따라 총 소유 비용도 증가하고 있습니다. 클라우드 공급업체는 현재 21 CFR Part 11, EU Annex 11, ISO 27001과 같은 독립적인 검증 감사를 통과했으며, 대부분의 규제 당국 검사관을 만족시킬 수 있는 문서화된 보증을 제공합니다. 전자 시험 마스터 파일(eTMF) 및 품질 관리 시스템과의 통합을 통해, 클라우드는 신규 진출기업들에게 기본적인 선택지가 되고 있습니다.

2025년 규제 업무 시장에서 AI가 차지하는 비중 중 머신러닝이 41.00%를 차지한 반면, 지식 그래프는 연평균 성장률(CAGR) 21.00%로 가장 빠르게 성장했습니다. 그래프 데이터베이스는 엔티티 간의 관계, 제품, 적응증, 관할 구역 및 지침 문서를 규제 심사 담당자가 신뢰할 수 있는 사람이 읽기 쉬운 형식으로 표현합니다. 70개국에 걸쳐 영향을 받는 모든 라벨에 안전성 신호를 연결하는 작업은 수천 번에 달하는 수작업 대조 대신, 단 한 번의 쿼리로 처리될 수 있게 됩니다. 한편, 자연어 처리는 표나 통계 결과를 신청 문서로 변환하는 생성형 코파일럿의 기반이 되고 있습니다. 로보틱 프로세스 자동화(RPA)는 레거시 PDF에서 스캔된 서명을 추출하는 것과 같은 틈새 과제를 해결하지만, 그 규칙 기반 논리는 확장성을 제한하고 있습니다. 컴퓨터 비전은 여전히 초기 단계에 머물러 있으며, 검색이 불가능한 이미지 내의 표나 서명을 식별하는 수준에 그치고 있습니다.

지역별 분석

북미는 FDA의 주도적인 역할을 바탕으로 2025년 매출의 46.48%를 차지했습니다. 해당 기관은 2025년 1월에 AI 신뢰성에 관한 지침 초안을 발표했으며, 2025년 6월에는 내부용 생성형 AI 검토 보조 도구인 ‘Elsa’를 공개했습니다. 이러한 노력은 AI의 정당성을 뒷받침하며, 민간 투자를 촉진하고 있습니다. 2025년 AI 기반 규제 기술과 관련된 특허 출원의 절반 이상을 미국 기업들이 차지했습니다. 또한, 캐나다도 2026년에 ‘Regulatory Experimentation Hub in Health(의료 분야 규제 실험 허브)’를 확대하고, AI의 설명 가능성과 관련된 시범 사업을 위한 샌드박스를 개설했습니다.

유럽도 이에 뒤를 잇고 있습니다. 2026년 1월, 유럽의약품청(EMA)과 미국 식품의약국(FDA)이 의약품 개발에 있어 AI를 규제하는 10가지 원칙에 합의했기 때문입니다. 2026년에 발효될 EU의 AI법은 의료 제품 규제를 위한 AI를 ‘고위험’으로 분류하고 품질 관리 시스템 및 인적 감독 규정을 의무화하고 있지만, 많은 공급업체가 이미 이를 이행하고 있어 전환 비용은 줄어들고 있습니다. 영국 의약품 및 의료기기 규제청(MHRA)은 시판 후 안전성 분석을 더욱 정교화하기 위해 2025년 10월 독자적인 AI 신호 감지 시범 사업을 시작했습니다.

아시아태평양은 가장 빠른 성장세를 보이고 있으며, 2031년까지의 연평균 성장률(CAGR)은 22.45%로 예측됩니다. 2025년 6월부터 시행되고 있는 일본의 ‘AI 추진법’은 트랜스레이셔널 AI 프로젝트에 자금을 지원하고, 디지털화된 신청에 대한 심사 기간을 단축하고 있습니다. 2026년 1월에 시행된 한국의 ‘AI 기본법’은 투명성 확보 의무와 인증된 AI 제공업체에 대한 인센티브를 결합하여 국내 업체들을 지원하고 있습니다. 2026년 2월에 개정된 인도의 ‘신약 및 임상시험 규정’은 전자 원본 데이터와 AI를 활용한 신청 서류 작성을 허용하게 되었으며, 미국 FDA와의 동등성을 추구하는 제네릭 의약품 제조업체들 사이에서 SaaS 도입을 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the aI in regulatory affairs market size is projected to expand from USD 1.60 billion in 2025 and USD 1.9 billion in 2026 to USD 4.47 billion by 2031, registering a CAGR of 18.65% between 2026 to 2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud-Based), Technology (Machine Learning, NLP, RPA, Computer Vision, Knowledge Graphs), Application (Regulatory Intelligence, Document Management, Labeling, Post-Market Surveillance, Others), End-User (Pharmaceutical, Biotech, Medical Device, CRO, Consulting, Others), and Geography. Forecasts are in Value (USD).

Global AI In Regulatory Affairs Market Trends and Insights

Accelerated Regulatory-Submission Timelines in Pharmaceutical and Biotechnology Companies

Expedited approval pathways for oncology, rare-disease, and pandemic-response therapies create strong incentives to compress investigational new drug and new drug application timelines. Sponsors now deploy AI platforms that auto-extract clinical study data, validate references, and assemble electronic Common Technical Documents in hours rather than weeks. Weave Bio and Parexel demonstrated a 60% faster NDA preparation cycle in April 2026, illustrating measurable return on investment for early adopters. Similar productivity gains appear at Recursion Pharmaceuticals, where its Recursion OS accelerated first-in-human readiness for an LSD1 inhibitor in roughly 20 months versus the historical 45-month average, saving multiple years of carrying costs.

Growing Volume of Global Labeling Changes Driven by Multi-Market Launches

Divergent U.S. Structured Product Labeling, European Summary of Product Characteristics, and Japanese package-insert rules require sponsors to tailor each update by language, format, and referral channels. A single safety signal can mandate changes across 50 countries, and manual coordination often pushes launches back an entire quarter. In 2025 Consainsights fine-tuned large language models on historic labeling templates and pharmacovigilance taxonomies, achieving 70% cycle-time compression and 85% concordance between AI drafts and final authority-approved labels. Faster multi-lingual updates preserve synchronized global market availability and prevent revenue leakage.

Data Privacy and Sovereignty Concerns Limiting Cross-Border AI Training Datasets

Sovereign data laws in the European Union, China, UAE, and Saudi Arabia fracture training corpora, forcing life-sciences companies to either replicate models locally or adopt federated learning. The UAE, for example, restricts cross-border transfer of health data unless exception criteria are met, requiring in-country processing or irreversible anonymization. Fragmented data sets can lower model accuracy when global AI services attempt to interpret region-specific medical terminologies, complicating validation and maintenance costs.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native AI Platforms Lowering Total Cost of Ownership for Mid-Size Sponsors

- Deployment of Generative AI Co-Pilots for Dossier Authoring and Quality Control

- "Black-Box" AI Explainability Gaps in Regulatory Submissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 64.15% AI in the regulatory affairs market share in 2025 and are projected to maintain supremacy by expanding at 20.55% CAGR through 2031. The AI in Regulatory Affairs market size for cloud-based solutions is forecast to reach USD 2.93 billion by 2031. Multitenant architecture spreads validation and cybersecurity costs, delivers instant feature upgrades, and simplifies disaster recovery. On-premises deployments persist in Japan and Germany, where data localization laws remain strict, but their total cost of ownership climbs as GPU prices, electricity tariffs, and specialized DevOps salaries rise. Cloud vendors now pass independent validation audits 21 CFR Part 11, EU Annex 11, ISO 27001, providing documented assurance that satisfies most agency inspectors. Integration bridges to electronic trial master file and quality-management systems make the cloud the default for new market entrants.

Machine learning accounted for 41.00% AI in the regulatory affairs market share in 2025, yet knowledge graphs should grow fastest at a 21.00% CAGR. Graph databases represent entity relationships, products, indications, jurisdictions, and guidance documents in a human-readable form that regulatory reviewers trust. Linking a safety signal to all affected labels across 70 countries becomes one query instead of thousands of manual cross-checks. Meanwhile, natural-language processing underpins generative co-pilots that translate tables and statistical outputs into submission narratives. Robotic process automation fills niche gaps such as extracting scanned signatures from legacy PDFs, but its rule-based logic limits scalability. Computer vision remains in an early stage, confined to identifying tables or signatures in non-searchable images.

Geography Analysis

North America contributed 46.48% revenue in 2025 on the back of FDA leadership. The agency released draft guidance on AI credibility in January 2025 and unveiled "Elsa," an internal generative AI reviewer assistant, in June 2025. Such initiatives validate AI's legitimacy and encourage private investment. U.S. firms accounted for more than half of 2025 patent filings related to AI-driven regulatory technologies. Canada also expanded its Regulatory Experimentation Hub in Health in 2026, opening sandboxes for AI explainability pilots.

Europe follows closely after the EMA and FDA agreed on ten principles governing AI in drug development in January 2026. The EU's AI Act, entering force in 2026, classifies medical-product regulatory AI as "high-risk," requiring quality-management systems and human-oversight provisions that many vendors already implement, easing transition costs. The United Kingdom Medicines and Healthcare products Regulatory Agency (MHRA) launched its own AI Signal Detection Pilot in October 2025 to refine post-marketing safety analytics.

Asia-Pacific posts the fastest growth, forecast at 22.45% CAGR through 2031. Japan's AI Promotion Act, live since June 2025, funds translational AI projects and shortens review windows for digitally enabled submissions. South Korea's AI Framework Act, effective January 2026, couples transparency mandates with incentives for certified AI providers, spurring domestic vendors. India's New Drugs and Clinical Trials Rules, amended in February 2026, now recognize electronic source data and AI-assisted dossier preparation, boosting SaaS adoption among generics manufacturers seeking U.S. FDA parity.

- Accenture

- Aris Global

- Celegence

- Certara

- Clarivate (Cortellis)

- Cognizant

- Deloitte

- Ennov

- Freyr Solutions

- IQVIA

- Genpact

- Kinapse

- Korber Pharma (Werum IT)

- MasterControl

- Montrium

- Parexel International

- Phlexglobal

- SamaCare

- Sparta Systems (Honeywell)

- Veeva Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Regulatory-Submission Timelines in Pharma

- 4.2.2 Rising Regtech Adoption Mandates by the U.S. FDA & EMA

- 4.2.3 Cloud-Native AI Platforms Lowering Total Cost of Ownership

- 4.2.4 Growing Volume of Global Labeling Changes

- 4.2.5 Deployment of Generative-AI Co-Pilots for Dossier Authoring

- 4.2.6 Knowledge-Graph Driven Proactive Compliance Analytics

- 4.3 Market Restraints

- 4.3.1 Legacy On-Premise Validation Hurdles

- 4.3.2 Data-Privacy & Sovereignty Concerns

- 4.3.3 Limited Annotated Regulatory Data for Training

- 4.3.4 "Black-Box" AI Explainability Gaps in Regulatory Review

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Deployment Mode

- 5.1.1 On-premise

- 5.1.2 Cloud-based

- 5.2 By Technology

- 5.2.1 Machine Learning

- 5.2.2 Natural Language Processing

- 5.2.3 Robotic Process Automation

- 5.2.4 Computer Vision

- 5.2.5 Knowledge Graphs

- 5.3 By Application

- 5.3.1 Regulatory Intelligence

- 5.3.2 Document & Data Management

- 5.3.3 Dossier Preparation & Submission

- 5.3.4 Labelling & Artwork Management

- 5.3.5 Post-Market Surveillance & Compliance

- 5.3.6 Others

- 5.4 By End-User

- 5.4.1 Pharmaceutical Companies

- 5.4.2 Biotechnology Firms

- 5.4.3 Medical Device Manufacturers

- 5.4.4 Contract Research Organizations

- 5.4.5 Regulatory Consulting Firms

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Accenture

- 6.3.2 ArisGlobal

- 6.3.3 Celegence

- 6.3.4 Certara

- 6.3.5 Clarivate (Cortellis)

- 6.3.6 Cognizant

- 6.3.7 Deloitte

- 6.3.8 Ennov

- 6.3.9 Freyr Solutions

- 6.3.10 IQVIA

- 6.3.11 Genpact

- 6.3.12 Kinapse

- 6.3.13 Korber Pharma (Werum IT)

- 6.3.14 MasterControl

- 6.3.15 Montrium

- 6.3.16 Parexel

- 6.3.17 Phlexglobal

- 6.3.18 SamaCare

- 6.3.19 Sparta Systems (Honeywell)

- 6.3.20 Veeva Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment