|

시장보고서

상품코드

2063839

곡물 건조기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Grain Dryers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

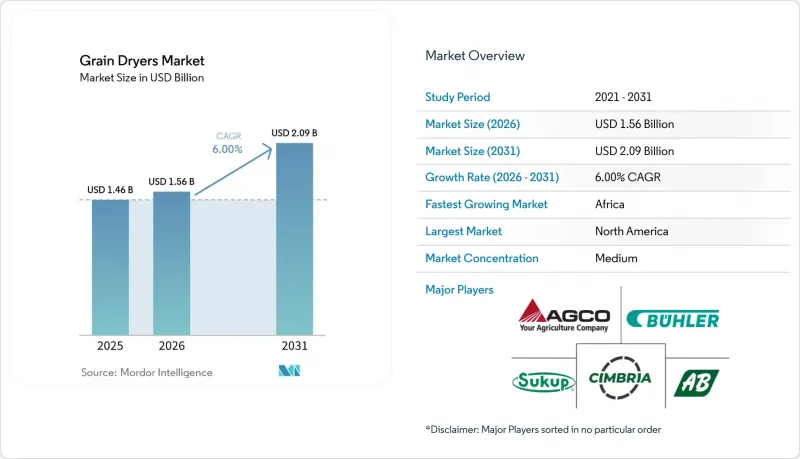

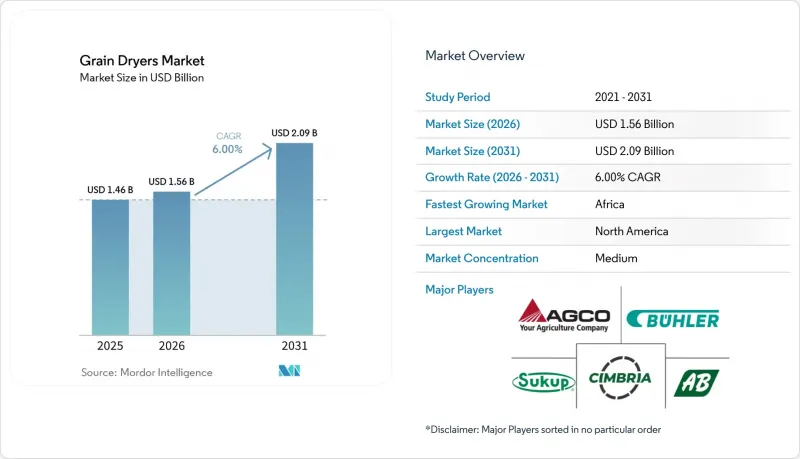

Mordor Intelligence에 의하면, 곡물 건조기 시장 규모는 2025년 14억 6,000만 달러에서 2026년에는 15억 6,000만 달러, 2031년까지 20억 9,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 예측 기간에서 CAGR 6.0%를 기록할 전망입니다.

본 보고서는 건조기 유형(혼합류식 건조기, 횡류식 건조기, 배치식 건조기 등), 운전 방식(연속류식, 재순환 배치식 등), 곡물 유형(옥수수, 밀, 쌀 등), 최종 사용자(상업용 곡물 엘리베이터, 농장 내 시설 등), 지역별(북미, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 곡물 건조기 시장 동향 및 분석

상업용 엘리베이터에 연속류식 건조기 도입 급증

상업용 곡물 엘리베이터에서는 업무 효율을 높이고 수확기라는 짧은 기간 동안 처리 능력을 강화하기 위해 연속류식 건조기의 활용이 확대되고 있습니다. 기존의 배치식 시스템과 달리, 연속류식 건조기는 곡물 처리를 중단하지 않고 진행할 수 있으므로, 현대 엘리베이터 운영에 필요한 대규모 처리 요건을 충족할 수 있습니다. 이러한 전환은 반입 시 혼잡을 최소화하고, 운송 차량의 회전 시간을 단축하며, 대량의 곡물에 대해 일관된 품질을 유지해야 할 필요성에 따라 추진되고 있습니다.

전기화를 통한 에너지 비용 변동 억제

사업자들이 화석 연료에 대한 의존도를 줄이고 운영 효율을 높이려는 가운데, 곡물 건조 시스템의 전기화가 점점 더 주목받고 있습니다. 기존 건조기는 프로판이나 천연가스에 의존하고 있기 때문에 운영 비용에 변동이 발생합니다. 반면, 전기식 및 하이브리드 시스템은 보다 안정적이고 예측 가능한 에너지 비용을 실현합니다. 또한, 이러한 시스템은 건조 조건을 정밀하게 제어할 수 있으므로 곡물의 품질을 향상시키고 손실을 최소화할 수 있습니다. 『Renewable and Sustainable Energy Reviews』(2024년)에 따르면, 곡물 건조기의 에너지 효율은 건조기 유형에 따라 26%에서 80% 사이입니다. 이는 보다 효율적이고 제어성이 뛰어난 건조 기술에 대한 수요가 증가하고 있음을 보여줍니다.

어려운 농업 수익 환경 속의 높은 초기 투자 비용

높은 초기 투자 비용은 특히 중소규모 농가에서 곡물 건조기 도입에 있어 여전히 큰 과제로 남아 있습니다. 농업 수익성의 저하는 첨단 건조 시스템과 같은 자본 집약적 설비에 투자하려는 생산자들의 능력을 더욱 제약하고 있습니다. 미국 농무부 경제조업체국에 따르면, 2024년 농업 순수입은 1,407억 달러로 감소했으며, 이는 2023년 대비 95억 달러 감소한 수치입니다. 이러한 소득 감소는 수확 후 인프라에 자금을 투입할 농가의 능력에 직접적인 영향을 미치며, 효율적인 곡물 건조 기술의 도입을 지연시키고 시장 성장을 저해하고 있습니다.

부문별 분석

2025년, 혼합류식 유닛은 곡물 건조기 시장 점유율의 38%를 차지하며 최대 점유율을 유지했습니다. 이러한 우위는 연비 효율이 뛰어난 기류 설계와, 일관된 건조 성능을 확보하면서도 다양한 곡물 유형에 대응할 수 있는 능력에서 비롯됩니다. 이러한 시스템은 균형 잡힌 열 분포와 운영상의 유연성을 제공하기 때문에 상업용 엘리베이터 시설과 중규모 시설 모두에 적합합니다. 로터리식 및 크로스플로우식 건조기는 수분 함량이 높은 곡물의 처리 용도로 계속해서 활용되고 있는 반면, 배치식 시스템은 계절에 따라 사용 수요가 발생하는 소규모 농장에서 여전히 중요한 역할을 수행하고 있습니다. 혼합 유동식 시스템의 범용성과 높은 비용 효율성이 다양한 농업 지역에서 이 시스템의 광범위한 도입을 촉진하고 있습니다.

하이브리드/마이크로파 보조식 건조기 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.8%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 이러한 성장은 에너지 소비를 줄이면서도 곡물의 품질을 유지하는 정밀 건조 솔루션에 대한 수요 증가에 힘입어 이루어지고 있습니다. 하이브리드 시스템을 통해 작업자는 건조 모드를 전환할 수 있어, 다양한 작물 유형에 걸쳐 효율을 높일 수 있습니다. 이러한 기술은 수분 함량 조절이 필수적인 종자 가공업체나 고부가가치 작물 분야에서 특히 중요합니다. 모듈식 구성과 에너지 절약 설계의 발전이 도입을 더욱 촉진하고 있으며, 건조 기술 분야에서 하이브리드 시스템이 주요 성장 분야로서의 입지를 확고히 하고 있습니다.

2025년 기준으로, 연속 유동식 시스템은 곡물 건조기 시장 점유율의 52%를 차지하며 가장 큰 점유율을 기록했습니다. 해당 시장에서 차지하는 선도적인 지위는 대량의 곡물을 연속적으로 처리할 수 있는 능력에서 비롯된 것으로, 이를 통해 가동 중단 시간을 최소화하고 처리 효율을 높이고 있습니다. 이러한 시스템은 주로 상업용 곡물 사일로에서 사용되며, 수확 성수기에 중단 없는 건조가 필수적인 상황에서 활용되고 있습니다. 또한, 자동화된 곡물 처리 인프라와의 호환성을 통해 업무 효율성이 향상되고, 일관된 수분 관리가 보장됩니다. 연속류식 건조기는 대규모 곡물 생산과 고도로 발달된 물류 네트워크가 특징인 지역에서 특히 선호되고 있습니다.

태양광 발전 보조형 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 11.2%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 시장의 성장은 전력 인프라가 제한적인 지역에서 에너지 효율이 뛰어나고 독립형 건조 솔루션에 대한 수요가 증가하는 것이 주된 요인입니다. 태양광 보조 시스템은 기존 연료에 대한 의존도를 낮추고, 소규모 농가에게 비용 대비 효과가 높은 건조 방안을 제공합니다. 이러한 시스템은 분산형 건조 솔루션이 필수적인 아시아태평양과 아프리카에서 점점 더 널리 도입되고 있습니다. 하이브리드 백업 시스템과의 통합으로 신뢰성이 향상된 한편, 태양열 기술의 발전으로 효율이 높아지면서 신흥 농업 시장에서의 도입이 촉진되고 있습니다.

지역별 분석

2025년, 북미는 곡물 건조기 시장 점유율의 42%를 차지하며 가장 큰 점유율을 기록했습니다. 이는 선진적인 농업 인프라와 높은 기계화 수준에 힘입은 결과입니다. 이 지역의 대규모 농업 경영과 잘 갖춰진 곡물 처리 시스템은 효율적인 건조 솔루션에 대한 안정적인 수요를 창출하고 있습니다. 자동화 기술과 통합형 저장 시스템의 도입이 급속히 진행되고 있는 점도 대용량 건조기에 대한 수요를 더욱 부추기고 있습니다. 또한, 자금 조달 프로그램에 대한 접근성과 지속적인 기술 발전이 설비 현대화에 기여하고 있으며, 곡물 건조 능력과 운영 효율성 면에서 북미의 선도적 위치를 공고히 하고 있습니다.

아프리카 시장 규모는 수확 후 손실 감소와 식량 안보 강화에 대한 관심이 높아짐에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.3%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 도입을 주도하고 있는 것은 분산형 태양광 발전을 활용한 건조 솔루션을 추진하는 개발 프로그램입니다. 인프라의 제약이나 전력 이용 제한과 같은 과제가 있기는 하지만, 투자 증가와 인식 제고에 힘입어 도입은 서서히 진행되고 있습니다. 이러한 노력을 통해 소규모 농가 시스템의 건조 능력이 확대되었으며, 신흥 농업 경제국에서 수확 후 관리 관행이 개선되고 있습니다.

지역별 차이를 통해 시장 간 인프라와 투자에 격차가 있음을 알 수 있습니다. 선진 지역에서는 첨단 건조 기술의 도입률이 높은 반면, 신흥 지역에서는 증가하는 수요에 대응하기 위해 기초적인 역량 확대에 중점을 두고 있습니다. 브라질 지리통계원(IBGE)에 따르면, 브라질의 농업용 저장 능력은 2025년 상반기에 2억 3,110만 톤에 달할 것으로 예상되며, 이는 곡물 생산이 기록적인 증가세를 이어가고 있는 상황과 일치합니다. 곡물 생산량과 이용 가능한 저장 인프라 간의 격차가 확대됨에 따라, 추가적인 곡물 건조·저장 시설의 필요성이 더욱 대두되고 있습니다. 이러한 불균형을 해소하는 것은 수확 후 손실을 줄이고, 공급망의 효율성을 높이며, 주요 곡물 생산 지역의 농업 생산성을 뒷받침하는 데 필수적입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the grain dryers market size is projected to grow from USD 1.46 billion in 2025 to USD 1.56 billion in 2026 and USD 2.09 billion by 2031, registering a CAGR of 6.0% during the forecast period from 2026 to 2031.

This report is Segmented by Dryer Type (Mixed-Flow Dryers, Cross-Flow Dryers, Batch Dryers, and More), by Mode of Operation (Continuous-Flow, Recirculating Batch, and More), by Grain Type (Corn/Maize, Wheat, Rice, and More), by End User (Commercial Grain Elevators, On-Farm Facilities, and More), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Grain Dryers Market Trends and Insights

Surging Adoption of Continuous-Flow Dryers in Commercial Elevators

Commercial grain elevators are increasingly utilizing continuous-flow dryers to improve operational efficiency and handle higher throughput during compressed harvest periods. In contrast to traditional batch systems, continuous-flow dryers enable uninterrupted grain processing, addressing the large-scale handling requirements of modern elevator operations. This transition is driven by the need to minimize intake congestion, reduce transport vehicle turnaround times, and maintain consistent grain quality across substantial volumes.

Electrification Reduces Energy Cost Volatility

The electrification of grain drying systems is becoming increasingly prominent as operators seek to decrease dependence on fossil fuels and enhance operational efficiency. Traditional dryers rely on propane and natural gas, resulting in variable operating costs. In contrast, electric and hybrid systems provide more stable, predictable energy costs. These systems also enable precise control of drying conditions, improving grain quality and minimizing losses. According to Renewable and Sustainable Energy Reviews (2024), the energy efficiency of grain dryers ranges from 26% to 80%, depending on the type of dryer . Which underscoring the demand for more efficient and controlled drying technologies.

High Capital Costs Amid Tight Farm Margins

High initial investment costs continue to pose a significant challenge to the adoption of grain dryers, especially among small and medium-scale farmers. Declining farm profitability further constrains producers' ability to invest in capital-intensive equipment like advanced drying systems. According to the United States Department of Agriculture Economic Research Service, net farm income declined to USD 140.7 billion in 2024, a reduction of USD 9.5 billion compared to 2023 . This decline in income directly impacts farmers' capacity to allocate funds for post-harvest infrastructure, delaying the adoption of efficient grain drying technologies and hindering market growth.

Other drivers and restraints analyzed in the detailed report include:

- Post-Harvest Loss Reduction Mandates in Developing Countries

- Rapid Adoption of IoT-Enabled Grain-Handling Automation

- Inconsistent Grain Quality Standards in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mixed-flow units held the largest 38% of the grain dryer market share in 2025. This dominance is attributed to their fuel-efficient airflow design and capability to handle multiple grain types while ensuring consistent drying performance. These systems offer balanced heat distribution and operational flexibility, making them suitable for both commercial elevators and mid-scale facilities. Rotary and cross-flow dryers continue to address high-moisture grain applications, while batch systems remain relevant for small farms with seasonal usage needs. The versatility and cost efficiency of mixed-flow systems drive their widespread adoption across various agricultural regions.

The hybrid/microwave-assisted dryers market is projected to grow at the fastest CAGR of 9.8% from 2026 to 2031. This growth is driven by increasing demand for precision drying solutions that maintain grain quality while reducing energy consumption. Hybrid systems allow operators to switch between drying modes, enhancing efficiency across different crop types. These technologies are particularly significant for seed processors and high-value crop segments where controlled moisture levels are essential. Advancements in modular configurations and energy-efficient designs are further supporting adoption, establishing hybrid systems as a key growth segment within drying technologies.

Continuous-flow systems held the largest 52% of the grain dryers market share in 2025. Their market leadership stems from their capability to handle large grain volumes continuously, minimizing operational downtime and enhancing throughput efficiency. These systems are predominantly utilized in commercial grain elevators, where uninterrupted drying is crucial during peak harvest seasons. Their compatibility with automated grain handling infrastructure facilitates streamlined operations and ensures consistent moisture control. Continuous-flow dryers are particularly favored in regions characterized by large-scale grain production and advanced logistics networks.

The solar-assisted market size is projected to grow at the fastest 11.2% CAGR from 2026 to 2031. Market growth is primarily driven by the rising demand for energy-efficient and off-grid drying solutions in areas with limited power infrastructure. Solar-assisted systems help reduce reliance on conventional fuels, offering cost-effective drying options for smallholder farmers. These systems are increasingly adopted in Asia-Pacific and Africa, where decentralized drying solutions are essential. Integration with hybrid backup systems is enhancing reliability, while advancements in solar thermal technologies are improving efficiency and driving adoption in emerging agricultural markets.

Geography Analysis

North America accounted for the largest 42% of the grain dryers market share in 2025, driven by advanced agricultural infrastructure and high mechanization levels. The region's large-scale farming operations and well-developed grain handling systems create a consistent demand for efficient drying solutions. The strong adoption of automated technologies and integrated storage systems further supports the demand for high-capacity dryers. Additionally, access to financing programs and ongoing technological advancements contribute to equipment upgrades, reinforcing North America's leadership in grain drying capacity and operational efficiency.

The Africa market size is projected to grow at the fastest 7.3% CAGR from 2026 to 2031, supported by increasing focus on reducing post-harvest losses and improving food security. Adoption is driven by development programs that promote decentralized, solar-based drying solutions. While infrastructure limitations and restricted access to electricity pose challenges, rising investments and growing awareness are fostering gradual adoption. These efforts are expanding drying capacity within smallholder farming systems and improving post-harvest management practices in emerging agricultural economies.

Regional variations reveal disparities in infrastructure and investment across markets. Developed regions demonstrate high adoption rates of advanced drying technologies, while emerging regions focus on expanding basic capacity to meet rising demand. According to the Brazilian Institute of Geography and Statistics (IBGE), Brazil's agricultural storage capacity reached 231.1 million metric tons in the first half of 2025, coinciding with continued record growth in grain production. The growing gap between grain production and available storage infrastructure underscores the increasing need for additional grain drying and storage facilities. Addressing this imbalance is essential to reducing post-harvest losses, enhancing supply chain efficiency, and supporting agricultural productivity in key grain-producing regions.

- AGCO Corporation

- Buhler Holding AG

- Sukup Manufacturing Co.

- Alvan Blanch Development Company Limited

- Cimbria A/S

- Mathews Company

- Chief Industries Inc.

- Mysilo Grain Storage Systems (Ozyurek A.S.)

- Shivvers Manufacturing Inc.

- Brock Grain Systems (CTB Inc.)

- Perry Engineering Services Ltd.

- Agridry Dryers Pty Ltd.

- Grain Handler USA Inc.

- Fratelli Pedrotti S.r.l.

- Silos Cordoba S.L.U.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging adoption of continuous-flow dryers in commercial elevators

- 4.2.2 Electrification reduces energy cost volatility

- 4.2.3 Post-harvest loss reduction mandates in developing countries

- 4.2.4 Rapid adoption of IoT-enabled grain-handling automation

- 4.2.5 Green hydrogen burner pilots in Europe and Australia

- 4.2.6 Rising use of microwave-assisted hybrid dryers for specialty grains

- 4.3 Market Restraints

- 4.3.1 High capital costs amid tight farm margins

- 4.3.2 Inconsistent grain quality standards in emerging markets

- 4.3.3 Limited three-phase power in rural Africa

- 4.3.4 Supply risks of stainless-steel heat exchangers due to nickel constraints

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Dryer Type

- 5.1.1 Mixed-Flow Dryers

- 5.1.2 Cross-Flow Dryers

- 5.1.3 Batch Dryers

- 5.1.4 Rotary Dryers

- 5.1.5 Hybrid/Microwave-Assisted Dryers

- 5.2 By Mode of Operation

- 5.2.1 Continuous-Flow

- 5.2.2 Recirculating Batch

- 5.2.3 Solar-Assisted

- 5.3 By Grain Type

- 5.3.1 Corn/Maize

- 5.3.2 Wheat

- 5.3.3 Rice

- 5.3.4 Soybean

- 5.3.5 Pulses and Others

- 5.4 By End User

- 5.4.1 Commercial Grain Elevators

- 5.4.2 On-Farm Facilities

- 5.4.3 Seed Processors

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 Russia

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 Nigeria

- 5.5.6.2 South Africa

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 AGCO Corporation

- 6.4.2 Buhler Holding AG

- 6.4.3 Sukup Manufacturing Co.

- 6.4.4 Alvan Blanch Development Company Limited

- 6.4.5 Cimbria A/S

- 6.4.6 Mathews Company

- 6.4.7 Chief Industries Inc.

- 6.4.8 Mysilo Grain Storage Systems (Ozyurek A.S.)

- 6.4.9 Shivvers Manufacturing Inc.

- 6.4.10 Brock Grain Systems (CTB Inc.)

- 6.4.11 Perry Engineering Services Ltd.

- 6.4.12 Agridry Dryers Pty Ltd.

- 6.4.13 Grain Handler USA Inc.

- 6.4.14 Fratelli Pedrotti S.r.l.

- 6.4.15 Silos Cordoba S.L.U.