|

시장보고서

상품코드

2063845

GPU 히트싱크 및 열 모듈 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)GPU Heatsink And Thermal Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

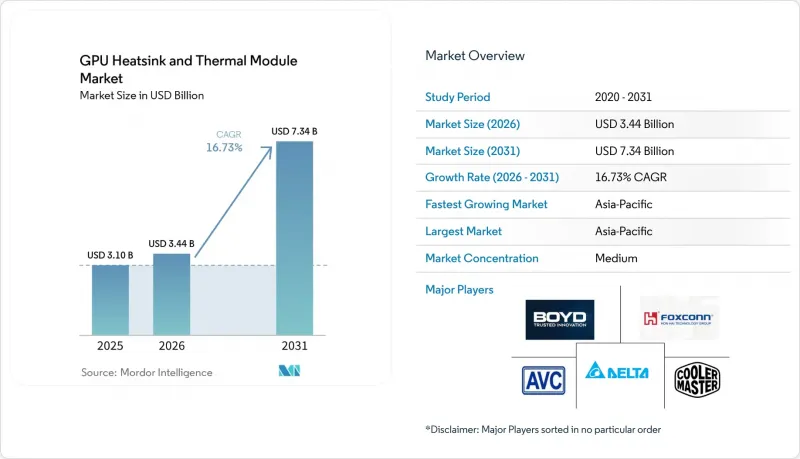

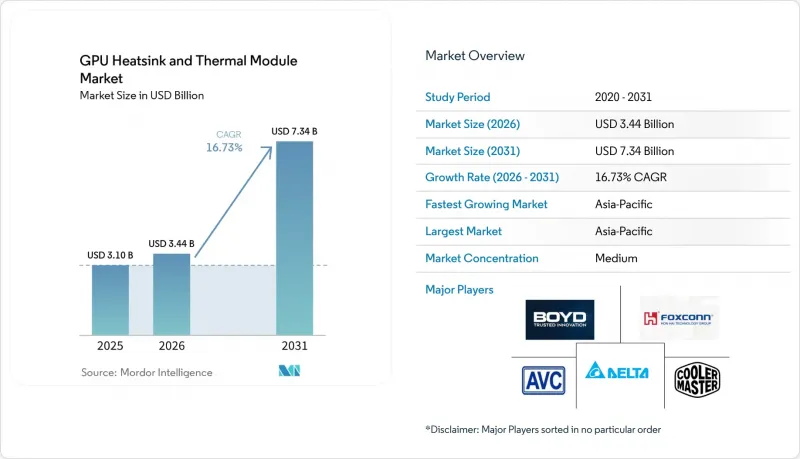

Mordor Intelligence에 의하면, GPU 히트싱크 및 열 모듈 시장 규모는 2025년 31억 달러로 평가되었습니다. 2026년에는 34억 4,000만 달러로 확대되어 2031년까지 73억 4,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 16.37%로 성장할 전망입니다.

본 보고서는 제품 유형(방열판, 베퍼 챔버, 히트파이프 기반 모듈, 액티브 열 모듈), 소재(알루미늄 기반, 구리 기반, 하이브리드), GPU 유형(데이터센터/AI용 GPU, 워크스테이션용 GPU, 소비자/게이밍용 GPU), 지역(북미, 유럽, 아시아태평양, 남미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 GPU 히트싱크 및 열 모듈 시장 동향 및 인사이트

급증하는 AI 워크로드가 데이터센터용 GPU 출하를 견인하고 있습니다.

하이퍼스케일 기업들은 2026년에 AI 인프라에 3,000억 달러 이상을 투자했습니다. 이 금액에는 100kW를 초과하는 랙에서 스로틀링을 방지하기 위해 필요한 액체 냉각 분배 장치가 포함되어 있습니다. NVIDIA의 H200은 700와트, AMD의 MI300X는 750와트의 열을 방출하기 때문에 공랭식 설계의 경제적 한계를 넘어섭니다. 인텔의 Gaudi 3는 수냉 환경에서만 1200와트를 구현하며, 이 33%의 전력 밀도 향상은 모델 훈련 주기의 가속화로 이어집니다. 델타 일렉트로닉스의 보고서에 따르면, 수냉 방식의 보급률은 2024년 14%에서 2026년에는 40%로 상승했으며, 이는 업계의 결정적인 전환을 보여주고 있습니다. 양극화된 시장에서 기존의 핀형 방열판은 300와트 미만의 엣지 추론 박스에 한정되는 반면, 500와트 이상의 부문에서는 베퍼 챔버나 콜드 플레이트가 주류를 이루고 있습니다.

선진 노드에서의 열 설계 전력 증가

GPU의 전력 소비량은 공정 세대가 발전할수록 증가하고 있습니다. NVIDIA의 RTX 5090은 지속적인 레이 트레이싱 작동 시 600와트에 육박하며, 트리플 슬롯 쿨러를 탑재하고 있음에도 불구하고 메모리 접합부의 온도는 92°C에 달할 전망입니다. RTX 4090의 450와트라는 사양으로 인해, 이미 각 보드 파트너사들은 더 넓은 핀 표면에 열을 분산시키는 베퍼 챔버를 채택할 수밖에 없는 상황에 처해 있습니다. 데이터센터용 가속기도 비슷한 추세를 보이고 있으며, 700와트가 진입점으로 자리 잡고 있습니다. 열전도 재료의 열전도율은 현재 15 W m?K를 초과하고 있지만, 접촉 압력을 유지하기 위해서는 금속 재질의 백플레이트가 필요합니다. IEC 62368-1의 접촉 온도 제한으로 인해 핀 밀도가 더욱 제약받게 되어, 독창적인 기류 관리가 요구되고 있습니다.

OEM을 통한 통합형 액체 냉각 루프로의 전환

서버 제조업체들은 현재 폐쇄형 액체 냉각 시스템을 사전 설치한 상태로 제품을 출하하고 있으며, 개별 모듈을 사후에 추가하는 애프터마켓 방식을 피하고 있습니다. 레노버의 ‘Neptune’은 전력 사용 효율(PUE) 1.1을 달성했으며, 폐열을 시설 난방에 재활용함으로써 냉각 에너지를 40% 절감하고 있습니다. 델의 ‘PowerCool eRDHx’는 공랭식 시스템으로는 허용할 수 없는 수준의 소음 없이는 구현할 수 없는 80kW급 랙을 가능하게 합니다. 아세테크가 체결한 3,500만 달러 규모의 2년 공급 계약은 OEM 중심의 수익원으로의 전환을 뒷받침하고 있습니다. 액체 루프는 시장 전체를 확대시키는 한편, 특히 수냉 방식이 표준으로 자리 잡은 데이터센터용 GPU의 경우, 단독 방열판의 판매 대수를 감소시키고 있습니다.

부문별 분석

베퍼 챔버 시장은 가장 빠른 성장세를 보이고 있으며, GPU의 전력 소비량이 600와트를 넘어섬에 따라 연평균 성장률(CAGR) 17.17%를 나타낼 것으로 전망됩니다. 히트싱크는 300와트 미만의 소비자용 GPU 시장을 아우르며 2025년 매출의 37.48%를 차지했지만, 보드 파트너들이 하이엔드 설계를 베이퍼 챔버 방식으로 전환함에 따라 그 점유율은 축소될 전망입니다. 히트파이프 모듈은 약 320와트급의 RTX 4080급 그래픽 카드에 대응하고 있지만, 모세관 현상으로 인한 한계에 직면해 있습니다. 납땜 접합 방식의 베퍼 챔버는 GPU 접합부의 온도를 10-15% 낮추기 때문에 전문가용 렌더링 스테이션에서 없어서는 안 될 요소로 자리 잡고 있습니다. 액티브 열 모듈은 펌프와 라디에이터를 일체형으로 설계하여 100kW를 넘는 랙 밀도를 실현합니다. TaiSol의 3D 베이퍼 챔버는 칩렛의 실적에 맞추어 증발기를 적층한 반면, Cooler Master의 FreeForm 2.0은 하나의 라디에이터에서 듀얼 GPU 루프를 구현합니다.

베퍼 챔버 방식의 GPU 히트싱크 및 열 모듈 시장에서의 점유율이 상승하고 있습니다. 이는 멀티 슬롯 카드에 있어 매우 중요한, 슬림한 설계이면서도 0.1°C·W 미만의 열저항을 실현하고 있기 때문입니다. 한편, 400와트를 초과하면 공랭 방식의 효율이 한계에 도달하기 때문에 기존 히트싱크가 차지하는 GPU 히트싱크 및 열 모듈 시장 점유율은 축소될 전망입니다. 액티브 모듈은 수량 면에서는 틈새 시장 제품이지만, AI 서버 분야에서는 높은 평균 판매 가격을 유지하고 있습니다. 이러한 제품 유형의 동향이 맞물리면서, 혁신의 초점은 핀 스택의 높이가 아니라 베퍼 챔버의 형상이나 콜드 플레이트의 마이크로채널에 계속 집중되고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 67.81%를 차지했으며, 대만의 베이퍼 챔버 제조 전문 지식과 중국의 대규모 조립 역량을 바탕으로 2031년까지 연평균 성장률(CAGR) 17.29%를 기록하며 성장할 것으로 전망됩니다. 델타 일렉트로닉스는 타오위안의 생산 능력 확대에 121억 대만 달러(3억 8,000만 달러)를 투자하여, 해당 지역에서 시장 지배력을 한층 더 공고히 하고 있습니다. 일본의 후루카와 전기공업은 1U 섀시용으로 특별히 설계된 소결 파이프를 공급함으로써 중요한 역할을 수행하고 있는 반면, 베트남과 태국은 비용 면에서의 우위를 제공하며 기존 제조 거점에 대한 의존도를 낮춤으로써 조립의 대체 거점으로 부상하고 있습니다.

북미는 버지니아주, 오리건주, 아이오와주 등에 위치한 하이퍼스케일 데이터센터 단지의 지원을 받아 시장 규모 면에서 2위를 차지하고 있습니다. 이러한 시설에서는 100kW를 초과하는 전력 용량을 갖춘 수냉식 랙의 도입이 점점 더 확대되고 있습니다. 유리한 세제 혜택과 재생에너지 원에 대한 접근성이 해당 지역 내 신규 데이터센터 건설을 지속적으로 뒷받침하고 있습니다. 유럽에서는 수요가 독일의 자동차 시뮬레이션 클러스터와 영국의 핀테크 데이터센터에 집중되어 있습니다. 두 지역 모두 엄격한 탄소 가격 규제 하에서 운영되고 있으며, 지속가능성 목표를 달성하기 위해 구매자들에게 고성능 콜드 플레이트 등 에너지 효율이 높은 솔루션의 도입이 요구되고 있습니다.

남미, 중동 및 아프리카는 여전히 시장 개발의 초기 단계에 있습니다. 남미에서는 브라질의 데이터센터 시설이 30kW급 랙으로 전환되고 있으며, 열 방산을 효과적으로 관리하기 위해 첨단 베퍼 챔버 설계가 요구되고 있습니다. 한편, 중동 걸프 지역 국가들에서는 AI를 활용한 석유 탐사 활동을 지원하기 위해 수냉식 워크스테이션이 도입되고 있으며, 이는 이 지역에서 고성능 컴퓨팅에 대한 관심이 높아지고 있음을 반영하고 있습니다. 지리적 분산은 여전히 중요한 추세이며, 공급업체들은 대만 중심의 제조에 수반되는 위험을 완화하고 전 세계적으로 증가하는 열 관리 솔루션 수요에 부응하기 위해 베트남, 태국, 멕시코 등지에 생산 라인을 구축하는 움직임을 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the gPU heatsink and thermal module market size is expected to increase from USD 3.1 billion in 2025 to USD 3.44 billion in 2026 and reach USD 7.34 billion by 2031, growing at a CAGR of 16.37% over 2026-2031.

This report is Segmented by Product Type (Heat Sinks, Vapor Chambers, Heat Pipe-Based Modules, and Active Thermal Modules), Material (Aluminum-Based, Copper-Based, and Hybrid), GPU Type (Data Center/AI GPUs, Workstation GPUs, and Consumer/Gaming GPUs), and Geography (North America, Europe, Asia Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global GPU Heatsink And Thermal Module Market Trends and Insights

Surging AI Workloads Driving Data-Center GPU Shipments

Hyperscale operators spent more than USD 300 billion on AI infrastructure in 2026, a figure that includes liquid-cooling distribution units needed to prevent throttling in racks exceeding 100 kilowatts. NVIDIA's H200 dissipates 700 watts, and AMD's MI300X reaches 750 watts, pushing air-cooled designs beyond their economic limits. Intel's Gaudi 3 delivers 1200 watts only under liquid cooling, a 33% power-density premium that translates into faster model-training cycles. Delta Electronics reports liquid-cooling penetration climbing from 14% in 2024 to 40% in 2026, illustrating a decisive industry pivot. The bifurcated market now sees traditional finned heat sinks limited to edge-inference boxes below 300 watts, whereas vapor chambers and cold plates dominate the 500-watt-plus tier.

Escalating Thermal Design Power of Advanced Nodes

GPU power envelopes rise with each process generation. NVIDIA's RTX 5090 approaches 600 watts under sustained ray tracing, and memory junctions climb to 92 °C despite triple-slot coolers. RTX 4090's 450-watt spec already forced board partners to adopt vapor chambers that spread heat across larger fin surfaces. Data-center accelerators follow the same arc, with 700 watts becoming the entry point. Thermal-interface materials now exceed 15 W m-K but demand metal backplates to maintain contact pressure. IEC 62368-1 touch-temperature limits further constrain fin density, forcing creative airflow management.

OEM Shift Toward Integrated Liquid Cooling Loops

Server builders now ship closed-loop liquid systems pre-installed, bypassing the aftermarket for discrete modules. Lenovo's Neptune achieves a 1.1 power-usage effectiveness and recycles waste heat for facility heating, cutting cooling energy by 40%. Dell's PowerCool eRDHx enables 80-kilowatt racks that air systems cannot meet without prohibitive noise. Asetek's USD 35 million, two-year supply contract underscores the pivot toward OEM-centric revenue streams. While liquid loops enlarge the total market, they erode unit sales of standalone heat sinks, especially in data-center GPUs where liquid is the default.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Chiplet-Based GPU Architectures

- Growth of Ray-Tracing Gaming Titles

- Volatility in Copper Commodity Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vapor chambers accounted for the fastest expansion, posting a 17.17% CAGR outlook as GPU envelopes breach 600 watts. Heat sinks still secured 37.48% of 2025 revenue, covering sub-300-watt consumer GPUs, yet their share will contract as board partners migrate high-end designs to vapor chambers. Heat-pipe modules serve RTX 4080-class cards around 320 watts, but they face capillary-limit ceilings. Solder-attached vapor chambers lower GPU junction temperatures by 10-15%, making them indispensable in professional rendering stations. Active thermal modules integrate pumps and radiators, unlocking rack densities above 100 kilowatts. TaiSol's 3D vapor chamber layers evaporators to match chiplet footprints, while Cooler Master's FreeForm 2.0 allows dual-GPU loops on one radiator.

The GPU heatsink and thermal module market share of vapor chambers is rising because they deliver sub-0.1 °C-W thermal resistance in a thin profile, critical for multi-slot cards. Meanwhile, the GPU heatsink and thermal module market share of traditional heatsinks will shrink as air-cooling meets diminishing returns beyond 400 watts. Active modules remain niche in volume but command high average selling prices in AI servers. Together, these product-type dynamics keep innovation centered on vapor-chamber geometry and cold-plate microchannels rather than on fin-stack height.

Geography Analysis

Asia-Pacific generated 67.81% of 2025 revenue and is forecast to grow at a compound annual growth rate (CAGR) of 17.29% through 2031, driven by Taiwan's expertise in vapor-chamber manufacturing and China's large-scale assembly capabilities. Delta Electronics has committed NTD 12.1 billion (USD 380 million) to expand its Taoyuan production capacity, further solidifying the region's dominance in the market. Japan's Furukawa Electric plays a key role by supplying sintered pipes specifically designed for 1U chassis, while Vietnam and Thailand are emerging as alternative hubs for assembly, offering cost advantages and reducing reliance on traditional manufacturing centers.

North America ranks as the second-largest market, supported by hyperscale data center campuses located in states such as Virginia, Oregon, and Iowa. These facilities are increasingly adopting liquid-cooled racks with power capacities exceeding 100 kilowatts. Favorable tax incentives and access to renewable energy sources continue to drive the construction of new data centers in the region. In Europe, demand is concentrated in Germany's automotive simulation clusters and the United Kingdom's fintech data centers. Both regions operate under stringent carbon-pricing regulations, which are pushing buyers to adopt energy-efficient solutions such as advanced cold plates to meet sustainability goals.

South America, the Middle East, and Africa are still in the early stages of market development. In South America, Brazil's data center facilities are transitioning to 30-kilowatt racks that require advanced vapor-chamber designs to effectively manage heat dissipation. Meanwhile, Gulf nations in the Middle East are deploying liquid-cooled workstations to support AI-driven oil exploration activities, reflecting the region's growing interest in high-performance computing. Geographic diversification remains a key trend, as suppliers are increasingly establishing production lines in countries such as Vietnam, Thailand, and Mexico to mitigate risks associated with Taiwan-centric manufacturing and to meet the growing global demand for thermal management solutions.

- Boyd Corporation

- Cooler Master Technology Inc.

- Noctua GmbH

- Arctic GmbH

- Hon Hai Precision Industry Co., Ltd.

- Delta Electronics, Inc.

- Sunonwealth Electric Machine Industry Co., Ltd.

- Furukawa Electric Co., Ltd.

- Asia Vital Components Co., Ltd.

- Taisol Electronics Co., Ltd.

- Asetek A/S

- EKWB d.o.o.

- Thermalright Inc.

- Listan GmbH

- Corsair Gaming, Inc.

- ASUSTeK Computer Inc.

- Gigabyte Technology Co., Ltd.

- Micro-Star International Co., Ltd.

- Zotac Technology Limited

- Palit Microsystems Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI Workloads Driving Data-Center GPU Shipments

- 4.2.2 Escalating Thermal Design Power of Advanced Nodes

- 4.2.3 Growth of Ray-Tracing Gaming Titles

- 4.2.4 Expansion of Cloud Gaming Infrastructure Globally

- 4.2.5 Emergence of Chiplet-Based GPU Architectures

- 4.2.6 Increasing Use of Solder-Attached Vapor Chambers in Workstations

- 4.3 Market Restraints

- 4.3.1 Volatility in Copper Commodity Prices

- 4.3.2 OEM Shift Toward Integrated Liquid Cooling Loops

- 4.3.3 Supply Chain Concentration in East Asia

- 4.3.4 Environmental Regulations on Mining of Thermal Interface Metals

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Heat Sinks

- 5.1.2 Vapor Chambers

- 5.1.3 Heat Pipe-Based Modules

- 5.1.4 Active Thermal Modules

- 5.2 By Material

- 5.2.1 Aluminum-Based

- 5.2.2 Copper-Based

- 5.2.3 Hybrid (Aluminum + Copper)

- 5.3 By GPU Type

- 5.3.1 Data Center / AI GPUs

- 5.3.2 Workstation GPUs

- 5.3.3 Consumer / Gaming GPUs

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Southeast Asia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Boyd Corporation

- 6.4.2 Cooler Master Technology Inc.

- 6.4.3 Noctua GmbH

- 6.4.4 Arctic GmbH

- 6.4.5 Hon Hai Precision Industry Co., Ltd.

- 6.4.6 Delta Electronics, Inc.

- 6.4.7 Sunonwealth Electric Machine Industry Co., Ltd.

- 6.4.8 Furukawa Electric Co., Ltd.

- 6.4.9 Asia Vital Components Co., Ltd.

- 6.4.10 Taisol Electronics Co., Ltd.

- 6.4.11 Asetek A/S

- 6.4.12 EKWB d.o.o.

- 6.4.13 Thermalright Inc.

- 6.4.14 Listan GmbH

- 6.4.15 Corsair Gaming, Inc.

- 6.4.16 ASUSTeK Computer Inc.

- 6.4.17 Gigabyte Technology Co., Ltd.

- 6.4.18 Micro-Star International Co., Ltd.

- 6.4.19 Zotac Technology Limited

- 6.4.20 Palit Microsystems Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment