|

시장보고서

상품코드

2063868

AI 기반 케어 코디네이션 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI-Based Care Coordination - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

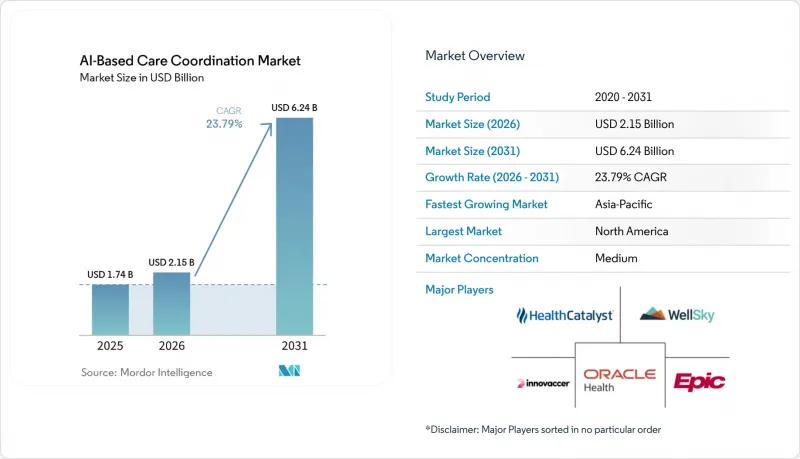

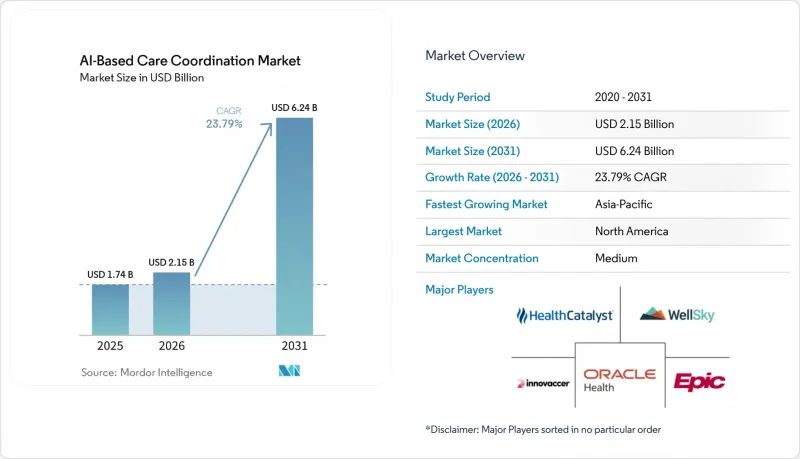

Mordor Intelligence에 의하면, AI 기반 케어 코디네이션 시장 규모는 2025년 17억 4,000만 달러로 평가되었고, 2026년 21억 5,000만 달러로 추정되고, 2031년까지 62억 4,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 23.79%를 나타낼 것으로 예측됩니다.

본 보고서는 솔루션 유형별(EHR 내장형, 케어 관리 제품군 등), 케어 환경별(병원, 외래 등), 구현 모델별(클라우드/SaaS, 온프레미스, 하이브리드), 용도별(만성 질환 케어 패스웨이 등), AI 기술별(예측 분석 및 위험 계층화 등), 통합 접근 방식(EHR 통합형 등), 지역별로 분류되어 있습니다. 시장 규모 예측은 달러 기준으로 이루어집니다.

세계의 AI 기반 케어 코디네이션 시장 동향 및 인사이트

가치 기반 의료 및 ACO 모델로의 전환이 분석 중심의 업무 흐름을 촉진합니다.

사용량 기반 보상 방식에서 가치 기반 계약으로의 전환은 AI 기반 케어 코디네이션 시장에 대한 직접적인 운영 수요를 지속적으로 창출하고 있습니다. 왜냐하면, 위험 분담 모델의 성공은 조기 개입, 보다 치밀한 사후 관리, 그리고 예방 가능한 의료 서비스 공백의 축소에 달려 있기 때문입니다. ‘The State and Science of Value-based Care 2025’ 조사에 따르면, 조사 대상 기관의 50%가 데이터 분석과 AI에 적극적으로 투자하고 있으며, 65%는 가치 기반 계약에서 AI의 예측 가치에 대해 낙관적인 전망을 보이고 있습니다.

사용자 초안에 인용된 증거에 따르면, AI를 활용한 분석을 도입한 메디케어 공유 절감 프로그램(Medicare Shared Savings Program)의 ACO(Accountable Care Organization)는 40% 더 높은 공유 절감액 배분을 보고하고 있으며, 이는 진료 조정 성과 향상을 통해 추가적인 기술 투자 자금을 조달할 수 있다는 주장을 뒷받침하고 있습니다. 이러한 경향이 중요한 이유는 AI 기반 케어 코디네이션 시장이 더 이상 단순한 소프트웨어로 구매되는 데 그치지 않고, 위험 계약 하에서 의료비를 절감하고 품질 성과를 향상시키는 운영상의 수단으로 평가받고 있기 때문입니다. 이용 관리, 퇴원 계획, 만성 질환의 사후 관리 분야에서 재현 가능한 성과를 추구하는 ACO 및 관련 의료 제공업체 그룹이 늘어남에 따라, 자동화에 대한 상업적 수요는 더욱 높아지고 있습니다. 그 결과, 우수한 조정 도구를 보유한 조직은 계약 실적을 향상시키고 경제성을 유지하며, 여전히 수동적인 진료 관리 모델에 의존하고 있는 제공업체와의 격차를 더욱 벌릴 수 있다는 선순환이 형성되고 있습니다.

CMS-0057-F 상호운용성 의무가 API 우선 조정 아키텍처를 촉진합니다.

CMS의 상호운용성 및 사전 승인에 관한 최종 규정은 AI 기반 케어 코디네이션 시장에서 API 우선 워크플로우 설계로의 전환을 가속화했습니다. 이는 상호 운용성을 단순한 계획 목표에서 기한이 정해진 준수 요건으로 전환했기 때문입니다. CMS는 2024년 1월 17일에 이 규정을 확정하였으며, 특정 사전 승인 응답 기한은 2026년 1월 일로, 의료 서비스 제공업체에 대한 접근, 지불자 간 정보 교환 및 사전 승인을 다루는 관련 FHIR API 요건에 대해서는 2027년 1월 일을 기한으로 정했습니다. ONC는 또한 관련 상호운용성 노력을 행정 부담 경감과 연계하여, 전자 사전 승인 기준을 통해 향후 10년간 192억 달러의 비용 절감이 예상된다고 지적했습니다.

의료 제공업체의 시스템이 표준화된 인터페이스를 통해 지급자 측의 더 완전한 이력을 확보할 수 있게 되면, AI를 활용한 조정 도구를 통해 기존에는 개별 지급자 포털, 수동 이력 확인, 그리고 직원의 반복적인 후속 조치가 필요했던 업무를 효율화할 수 있습니다. 이러한 변화로 인해, AI 기반 케어 코디네이션 시장은 특히 소개, 승인, 진료 전 준비와 같은 업무 흐름에서 대규모 사무 처리의 간소화가 필요한 의료 시스템이나 보험사에게 더욱 매력적인 시장이 될 것입니다. 또한, 폐쇄적인 인터페이스나 로컬 맞춤형 통합에 의존하는 벤더보다, 구조화된 데이터 교환과 유연한 오케스트레이션을 전제로 구축된 벤더에게 유리한 상황이 됩니다.

데이터 개인정보 보호, 보안 및 통합의 복잡성이 AI 도입을 지연시키고 있습니다.

AI 기반 케어 코디네이션 시장은 여전히 기본적인 도입 과제에 직면해 있습니다. 왜냐하면, 연동을 개선하기 위한 광범위한 데이터 접근은 개인정보 보호, 동의, 신원 확인 및 인터페이스의 신뢰성과 관련된 운영상의 부담도 동시에 증가시키기 때문입니다. 이러한 플랫폼은 EHR(전자건강기록), 보험사 시스템, HIE(의료정보교환기관), 원격 모니터링 데이터 스트림, 지역 자원 네트워크에서 제공하는 정보를 수집하여 표준화해야 하지만, 각 소스는 종종 서로 다른 데이터 모델과 거버넌스 요건을 가지고 있습니다. 『The State and Science of Value-based Care 2025』 조사에 따르면, 응답자의 69%가 도입 지연의 원인 중 하나로 규제의 복잡성을 꼽았으며, 이 문제는 단순한 기술적 인터페이스 작업의 범위를 훨씬 넘어선다는 사실이 드러났습니다.

연방 정부의 TEFCA 규정 제정 및 관련 상호운용성 노력은 데이터 교환 경로를 지속적으로 확대하고 있으며, 그 결과 엔터프라이즈 AI를 활용한 진료 조정 도입을 검토 중인 구매자들에게 신뢰성, 라우팅 및 데이터 처리 관행이 더욱 투명해지고 있습니다. 대규모 의료 시스템은 대개 내부 디지털 팀을 통해 이러한 통합 노력을 더 잘 소화해 낼 수 있지만, 소규모 의료 제공업체는 동일한 수준의 데이터 엔지니어링, 동의 관리, 워크플로우 재설계를 지원하는 데 어려움을 겪는 경우가 많습니다. 이러한 불균형으로 인해 AI 기반 케어 코디네이션 시장의 광범위한 도입이 지연되고 있습니다. 특히, 이러한 혜택이 절실히 필요한 곳, 즉 도입 자원이 부족한 중규모 네트워크, 지역 의료 현장 및 지방 기관에서 그 효과가 두드러집니다.

부문별 분석

2025년, EHR에 통합된 케어 코디네이션 플랫폼은 35.16%의 시장 점유율을 차지하며 솔루션 시장을 선도했습니다. 이는 임상의나 케어 매니저가 이미 사용하고 있는 핵심 워크플로우 내에서 진행될 수 있다는 장점을 반영한 것입니다. AI 기반 케어 코디네이션 시장에서 이러한 도입 기반의 경쟁력은 매우 중요합니다. 왜냐하면 시스템 간 전환은 여전히 문서 작성, 후속 조치 및 예외 처리에 지연을 초래하기 때문입니다. 집단건강관리를 위한 케어 관리 제품군은 특히 조직이 할당된 대상 집단 전체에 걸쳐 보다 광범위한 시간적 관점을 필요로 하는 경우, 여전히 중요한 2위 자리를 유지했습니다. 소개 및 네트워크 관리 도구 역시 여전히 그 중요성을 유지하고 있습니다. 왜냐하면 급성기 이후의 돌봄과 외부 기관으로의 인계는 돌봄 과정 중에서도 여전히 디지털화가 가장 덜 진행된 부분 중 하나이기 때문입니다. 독립형 및 기타 솔루션 유형은 풀 스위트로의 대체가 아닌, 특정 기능에 특화된 솔루션을 원하는 공급업체들로부터 계속해서 투자를 유치했습니다.

가장 빠르게 성장하고 있는 솔루션 분야는 SDoH(사회적 결정 요인)의 폐쇄형 루프 조정 플랫폼입니다. 이는 품질 관리 및 집단건강관리 워크플로우에서 사회적 요구 사항의 해결이 더욱 가시화됨에 따라, 2031년까지 연평균 성장률(CAGR) 24.88%를 나타낼 것으로 예측됩니다. AI 기반 케어 코디네이션 업계의 이 분야가 성장세를 보이고 있는 이유는 구매자들이 지역 밀착형 기관으로의 소개가 확실하게 완료되고, 그 과정이 추적되며, 환자의 사후 관리로 이어졌습니다는 증거를 요구하고 있기 때문입니다. Innovaccer는 2025년 11월, PopHealth Learning Center와 주 전역에 걸친 파트너십을 발표했으며, 200개 진료소에 등록된 200만 명의 메디컬(Medi-Cal) 환자에 대한 진료 조정을 지원하게 되었습니다. 이는 공공 자금을 활용한 프로그램이 SDoH(사회적 결정 요인)와 관련된 도입을 보다 광범위하게 추진하고 있음을 보여줍니다. 이러한 정책과 프로그램에 따른 압력은 AI 기반 케어 코디네이션 시장 수요 구성을 변화시키고 있습니다. 왜냐하면 구매자들은 더 이상 사회적 심사만으로는 충분하다고 여기지 않기 때문입니다. 대신, 임상 팀, 사회복지 서비스, 보고 요건을 단일 운영 체인으로 연결하는 감사 가능한 폐쇄형 프로세스를 요구하고 있습니다.

2025년 현재, 병원 및 의료 시스템은 46.17%의 점유율을 차지했으며, 막대한 기술 예산을 관리하고 가장 복잡한 환자를 치료하고 있다는 점에서 모든 의료 현장에서 주도적인 위치를 확립했습니다. 이러한 규모 덕분에 병원 구매자들은 AI 기반 케어 코디네이션 시장에서 초기 우위를 점하고 있습니다. 왜냐하면 도입 비용을 간호 관리, 이용 심사, 퇴원 계획 및 인구 건강 프로그램에 분산시킬 수 있기 때문입니다. 외래 진료나 의사 그룹의 현장도 여전히 중요하지만, 그 구매 패턴은 더욱 세분화되어 있으며, 대부분의 경우 보다 제한적인 이용 사례나 공유 인프라에 의존하고 있습니다. 급성기 이후의 돌봄 및 장기 돌봄 현장은 현재 시장 점유율이 여전히 낮은 편이지만, 일상 업무에서 가장 심각한 조정상의 과제를 안고 있습니다. 그 밖의 의료 현장도 지역 네트워크 조정에서 격차가 큰 경우, 수요 구성의 일부로 남아 있습니다.

재택치료 및 재택 병원 서비스는 2031년까지 24.12%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측되며, 이는 기존 입원 환자 중심 시설에서 재택치료 및 재택 병원 서비스에 대한 수요가 얼마나 빠르게 확대되고 있는지를 보여줍니다. 2030년까지의 재택 병원 서비스 면제 조치 연장 및 139개 의료 시스템에 걸쳐 승인된 프로그램의 보급은 분산형 급성기 의료를 일시적인 실험이 아닌 보다 지속 가능한 운영 모델로 자리매김함으로써 이러한 변화를 뒷받침하고 있습니다. WellSky사는 2026년 2월, 자사의 SkySense AI를 장기 요양 및 전문 간병 분야로 확대함으로써 재택치료 업무 흐름에서 문서 작성 시간을 최대 50% 단축할 수 있다고 발표했습니다. 이는 급성기 이후 의료 현장에서 자동화 수요가 증가하고 있음을 시사합니다. 실무적인 관점에서 볼 때, AI 기반 케어 코디네이션 시장은 사후 관리가 미흡한 사례가 빈번히 발생하고, 인력 부족으로 인한 압박이 끊이지 않는 분야로 변모하고 있습니다. 따라서 현재 지출 규모에서는 여전히 병원이 가장 큰 비중을 차지하고 있지만, 재택 간호 및 급성기 후 간호는 자연스럽게 성장하는 분야가 되고 있습니다.

지역별 분석

2025년 기준 북미는 43.18%의 점유율을 차지했으며, AI 기반 케어 코디네이션 시장에서 최대 지역 블록으로서의 위상을 유지했습니다. 이러한 추세는 보다 견고한 규제 및 운영 체계에 기인합니다. 왜냐하면 CMS의 상호운용성 관련 기한, TEFCA 네트워크의 개발, 그리고 가치 기반 의료의 도입이 모두 같은 방향으로 나아가고 있기 때문입니다. 또한, 미국에는 대규모 공급업체가 가장 밀집해 있어, 이것이 제품 개발을 보험사 및 의료 제공 기관과의 실제 계약으로 이어지게 하는 데 일조하고 있습니다. 북미에서 AI 기반 케어 코디네이션 시장은 리스크 기반 케어, 이용 관리, 상호 운용성에 대한 지출에 이미 익숙한 구매자층의 혜택을 받고 있습니다. 캐나다와 멕시코는 여전히 초기 단계에 있으며, 디지털 헬스 기반은 갖춰져 있지만 미국만큼 직접적인 정책적 압박은 받고 있지 않습니다.

유럽에서는 AI 기반 케어 코디네이션 시장에서 시스템의 출시 및 확장에 있어 규정 준수 설계가 더 큰 역할을 수행하기 때문에 사업 전개 양상이 다릅니다. AI 법과 MDR(의료기기 규정) 또는 IVDR(체외진단용 의료기기 규정) 간의 상호 관계에 관한 유럽의 공식 지침은 임상적 의사 결정 및 규제 대상 워크플로우와 관련된 많은 진료 조정 도구가 더 엄격한 감독 요건에 직면하게 되는 이유를 설명하고 있습니다. 프랑스는 2025년 7월 AI와 건강 데이터에 관한 국가 전략을 발표했으며, CNSA(프랑스 요양·고령자국)도 자율 지원 및 케어 코디네이션 분야의 AI에 관한 2025-2026년 로드맵을 공표했는데, 이는 특정 분야에서 공공 부문의 적극적인 지원을 시사하고 있습니다. 독일에서 진행되고 있는 실질적인 사례로는 프라운호퍼 ITWM의 ‘ViKI pro’ 프로젝트를 들 수 있습니다. 이는 장기 요양 환경에서의 AI 기반 돌봄 계획에 관한 것으로, 이 분야의 기회가 병원을 넘어 보다 광범위한 돌봄 제공 모델로까지 확대되고 있음을 보여줍니다. 따라서 이 지역에는 확실한 수요가 존재하지만, 그 수요는 보다 강력한 거버넌스, 보다 엄격한 적합성 요건, 그리고 도구의 분류 및 감독 방식에 대한 세심한 주의를 통해 선별될 것입니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR) 27.36%로 확대될 것으로 예상되며, AI 기반 케어 코디네이션 시장에서 가장 강력한 미래 성장 전망을 보이고 있습니다. 이 지역의 성장은 고령화, 보다 적극적인 공공 디지털 헬스 프로그램, 그리고 시스템 현대화의 일환으로 AI를 활용하려는 일부 국가들의 의지에 힘입어 이루어지고 있습니다. 인도는 2026년 2월 ‘의료 분야 인공지능 전략’을 발표하며, 케어 코디네이션을 우선적인 활용 사례 중 하나로 꼽았습니다. 이는 공공 디지털 인프라가 확대되고 있는 지역에서 장기적인 도입 가능성을 뒷받침하는 것입니다. 일본도 진전을 보이고 있으며, 후지쯔는 2026년 3월, 테이쿄 대학 병원과의 공동 실증 실험을 발표했습니다. 이는 의뢰 환자 관리 및 데이터 분석에 중점을 둔 것으로, AI를 활용한 조정 워크플로우에 대한 구체적인 관심을 보여주고 있습니다. 주요 3개 지역 이외에는 중동 및 아프리카 및 남미가 여전히 초기 단계 수요 거점으로 자리 잡고 있으며, 활동은 광범위한 도입이라기보다는 특정 스마트 병원이나 디지털 헬스 프로그램에 집중되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the aI-Based care coordination market size is projected to expand from USD 1.74 billion in 2025 and USD 2.15 billion in 2026 to USD 6.24 billion by 2031, registering a CAGR of 23.79% between 2026 to 2031.

This report is Segmented by Solution Type (EHR-Embedded, Care Management Suites, and More), Care Setting (Hospitals, Ambulatory, and More), Deployment Model (Cloud/SaaS, On-Premises, Hybrid), Application (Chronic Disease Care Pathways, and More) AI Technique (Predictive Analytics & Risk Stratification, and More), Integration Approach (EHR-Integrated, and More), and Geography. Value Forecasts in USD.

Global AI-Based Care Coordination Market Trends and Insights

Shift To Value-Based Care And ACO Models Elevates Analytics-Driven Workflows

The move from fee-for-service reimbursement toward value-based contracting continues to create a direct operating need for the AI-based care coordination market, because success under shared-risk models depends on earlier outreach, tighter follow-up, and fewer avoidable gaps in care. The State and Science of Value-based Care 2025 study found that 50% of surveyed organizations were actively investing in data analytics and AI, while 65% expressed optimism about AI's predictive value in value-based arrangements.

Evidence cited in the user draft also showed that Medicare Shared Savings Program ACOs using AI-enhanced analytics reported 40% higher shared savings distributions, which supports the case that better coordination performance can fund additional technology spending. That pattern matters because the AI-based care coordination market is no longer being bought only as software, it is being evaluated as an operating lever that can improve medical cost control and quality performance under risk contracts. As more ACOs and related provider groups seek repeatable gains in utilization management, discharge planning, and chronic disease follow-up, the commercial pull for automation becomes stronger. The result is a self-reinforcing cycle in which organizations with better coordination tools can post better contract performance, defend their economics, and widen the gap with providers still dependent on manual care management models.

CMS-0057-F Interoperability Mandate Catalyzes API-First Coordination Architectures

The CMS Interoperability and Prior Authorization final rule has accelerated the move toward API-first workflow design in the AI-based care coordination market, because it turns interoperability from a planning goal into a dated compliance requirement. CMS finalized the rule on January 17, 2024, with a January 1, 2026 deadline for certain prior authorization response timelines and a January 1, 2027 deadline for the related FHIR API requirements covering provider access, payer-to-payer exchange, and prior authorization. ONC also tied related interoperability work to lower administrative burden, noting projected savings of USD 19.2 billion over the coming decade from electronic prior authorization standards.

Once provider systems can retrieve more complete payer-side history through standardized interfaces, AI coordination tools can compress work that previously required separate payer portals, manual history checks, and repeated staff follow-up. That change makes the AI-based care coordination market more attractive to health systems and payers that need administrative simplification at scale, especially in referral, authorization, and pre-visit preparation workflows. It also favors vendors that were built for structured data exchange and flexible orchestration rather than those relying on closed interfaces and local custom integrations.

Data Privacy, Security, And Integration Complexity Slow AI Deployment

The AI-based care coordination market still faces a basic deployment challenge, because the same broad data access that improves coordination also widens the operational burden around privacy, consent, identity resolution, and interface reliability. These platforms need to ingest and normalize information from EHRs, payer systems, HIEs, remote monitoring streams, and community resource networks, and each source often carries a different data model and governance expectation. The State and Science of Value-based Care 2025 study found that 69% of surveyed respondents cited regulatory complexities as a primary reason for slower adoption, which shows that the issue extends well beyond technical interface work alone.

Federal TEFCA rulemaking and related interoperability activity continue to expand exchange pathways, but they also make trust, routing, and data-handling practices more visible to buyers that are assessing enterprise AI coordination deployments. Large health systems can usually absorb more of this integration effort through internal digital teams, but smaller providers often struggle to support the same level of data engineering, consent management, and workflow redesign. That imbalance slows broader adoption of the AI-based care coordination market, especially in mid-sized networks, community settings, and rural organizations that need the benefit but have fewer deployment resources.

Other drivers and restraints analyzed in the detailed report include:

- TEFCA QHIN-To-QHIN FHIR Exchange Accelerates Cross-Network Coordination

- AI-Driven Patient Flow And Discharge Orchestration Unlocks System Capacity

- High Implementation And Change-Management Costs Challenge ROI Realization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EHR-embedded care coordination platforms led the solution landscape in 2025 with a 35.16% share, which reflected the advantage of staying inside the core workflow already used by clinicians and care managers. In the AI-based care coordination market, that installed-base position matters because switching between systems still slows documentation, follow-up, and exception handling. Care management suites for population health continued to hold an important secondary position, especially where organizations wanted a broader longitudinal view across attributed populations. Referral and network management tools also remained relevant, because post-acute and external handoffs still sit among the least digitized parts of the care journey. Standalone and other solution types continued to attract investment where providers wanted focused functionality without a full suite replacement.

The fastest-growing solution segment is SDoH closed-loop coordination platforms, which are projected to grow at 24.88% CAGR through 2031 as social needs closure becomes more visible in quality and population health workflows. This part of the AI-based care coordination industry is gaining traction because buyers now want evidence that referrals to community-based organizations were completed, tracked, and tied back to patient follow-up. Innovaccer announced in November 2025 a statewide partnership with the PopHealth Learning Center to support care coordination for 2 million Medi-Cal patients across 200 clinics, which illustrates how publicly sponsored programs are pushing broader SDoH-linked deployment. That policy and program pressure is changing the mix of demand inside the AI-based care coordination market, because buyers are no longer treating social screening as sufficient on its own. They are instead looking for auditable closed-loop processes that connect clinical teams, social services, and reporting requirements in one operating chain.

Hospitals and health systems held 46.17% share in 2025, which gave them the leading position across care settings because they control large technology budgets and manage the most complex patients. That scale gives hospital buyers an early advantage in the AI-based care coordination market, since they can spread deployment costs across care management, utilization review, discharge planning, and population health programs. Ambulatory and physician group settings still matter, but their buying patterns are more fragmented and often depend on narrower use cases or shared infrastructure. Post-acute and long-term care settings remained smaller in current share terms, yet they carry some of the highest coordination pain points in day-to-day operations. Other care settings also remained part of the demand mix where local network coordination gaps were large.

Home health and hospital-at-home is projected to record the fastest CAGR at 24.12% through 2031, which shows how quickly coordination demand is moving beyond the traditional inpatient campus. The hospital-at-home waiver extension through 2030 and the spread of approved programs across 139 health systems support that shift by making distributed acute care a more durable operating model rather than a temporary experiment. WellSky stated in February 2026 that its SkySense AI expansion into long-term care and skilled nursing could reduce documentation time by up to 50% in home health workflows, which signals stronger automation demand in post-acute settings. In practical terms, the AI-based care coordination market is moving toward the places where follow-up failures are common and staffing pressure is persistent. That makes home-based and post-acute care a natural growth area, even while hospitals continue to hold the largest current spending base.

Geography Analysis

North America held 43.18% share in 2025, which kept it as the largest regional block in the AI-based care coordination market. That lead is tied to a stronger regulatory and operating framework, because CMS interoperability deadlines, TEFCA network development, and value-based care adoption are moving in the same direction. The United States also has the densest concentration of scaled vendors, which helps convert product development into live contracts across payer and provider organizations. Within North America, the AI-based care coordination market benefits from a buyer base that is already familiar with risk-based care, utilization controls, and interoperability spending. Canada and Mexico remain at earlier stages, with some digital health foundation in place but less direct policy pressure than in the United States.

Europe presents a different operating profile for the AI-based care coordination market because compliance design plays a larger role in how systems are brought to market and scaled. Official European guidance on the interaction between the AI Act and MDR or IVDR shows why many care coordination tools tied to clinical decision or regulated workflows face heavier oversight requirements. France published a national strategy for AI and health data in July 2025, and CNSA also released its 2025-2026 roadmap for AI in autonomy and care coordination, which points to active public-sector support in targeted areas. Germany's applied activity is also visible through Fraunhofer ITWM's ViKI pro work in AI-based care planning for long-term care settings, which shows that the regional opportunity extends beyond hospitals and into broader care delivery models. The region therefore offers real demand, but that demand is filtered through stronger governance, more formal conformity expectations, and closer attention to how tools are classified and supervised.

Asia-Pacific is the fastest-growing region and is projected to expand at 27.36% CAGR through 2031, which gives it the strongest forward growth profile in the AI-based care coordination market. Growth in this region is being supported by aging populations, more active public digital health programs, and a willingness in several countries to use AI as part of system modernization. India published its Strategy for Artificial Intelligence in Healthcare in February 2026 and identified care coordination among the priority use cases, which supports longer-term deployment potential where digital public infrastructure is expanding. Japan is also moving forward, and Fujitsu Japan announced in March 2026 a joint proof of concept with Teikyo University Hospital focused on referred-patient management and data analysis, which shows concrete interest in AI-assisted coordination workflows. Outside the 3 leading regions, the Middle East and Africa and South America remain earlier-stage demand pockets, with activity concentrated in selective smart hospital and digital health programs rather than broad-based adoption.

- Arcadia

- athenahealth

- Bamboo Health

- eClinicalWorks

- Epic Systems

- Health Catalyst (Lumeon & Twistle)

- HealthEdge (GuidingCare)

- Innovaccer

- Lightbeam Health Solutions

- Medecision

- Netsmart

- Oracle Health (Cerner)

- PointClickCare

- Qventus

- Salesforce (Health Cloud)

- Signify Health (CVS)

- Unite Us

- Veradigm

- WellSky (CarePort)

- ZeOmega

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift To Value-Based Care and ACO Models Elevates Coordinated, Analytics-Driven Workflows

- 4.2.2 Interoperability Mandates (CMS 0057-F) Catalyze API-First, Automated Coordination

- 4.2.3 Cloud-First Architectures Scale AI Pipelines Across Settings and Stakeholders

- 4.2.4 TEFCA QHIN-To-QHIN FHIR Exchange Enables Cross-Network, Near Real-Time Data Flows

- 4.2.5 AI-Driven Patient Flow/Discharge Orchestration to Unlock Capacity And Reduce LOS

- 4.3 Market Restraints

- 4.3.1 Data Privacy/Security and Integration Complexity Slow AI Deployment

- 4.3.2 High Implementation and Change-Management Costs Challenge ROI

- 4.3.3 EU AI Act High-Risk Obligations Raise Compliance Burden in Europe

- 4.3.4 Uneven Real-Time Cross-Network Eventing Until TEFCA FHIR Matures

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Solution Type

- 5.1.1 EHR-embedded care coordination platforms

- 5.1.2 Care management suites (population health / care management)

- 5.1.3 Patient flow & discharge orchestration

- 5.1.4 Referral & network management (including post-acute transitions)

- 5.1.5 SDoH closed-loop coordination platforms

- 5.1.6 Others

- 5.2 By Care Setting

- 5.2.1 Hospitals & health systems

- 5.2.2 Ambulatory/physician groups & clinics

- 5.2.3 Post-acute & long-term care (SNF, rehab, home health)

- 5.2.4 Home health & hospital-at-home

- 5.2.5 Others

- 5.3 By Deployment Model

- 5.3.1 Cloud / SaaS

- 5.3.2 On-premises

- 5.3.3 Hybrid

- 5.4 By Application

- 5.4.1 Chronic disease care pathways

- 5.4.2 Transitions of care / discharge & post-acute coordination

- 5.4.3 High-risk identification & outreach

- 5.4.4 Prior authorization & utilization management coordination

- 5.4.5 SDoH referrals & closed-loop coordination

- 5.4.6 Others

- 5.5 By AI Technique

- 5.5.1 Predictive analytics & risk stratification

- 5.5.2 NLP & information extraction/summarization

- 5.5.3 Workflow automation, RPA & agentic AI

- 5.5.4 Recommender systems / next best action

- 5.5.5 Computer vision & remote monitoring

- 5.6 By Integration Approach

- 5.6.1 EHR-integrated

- 5.6.2 HIE/QHIN-integrated

- 5.6.3 Standalone with open APIs

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Arcadia

- 6.3.2 athenahealth

- 6.3.3 Bamboo Health

- 6.3.4 eClinicalWorks

- 6.3.5 Epic Systems

- 6.3.6 Health Catalyst (Lumeon & Twistle)

- 6.3.7 HealthEdge (GuidingCare)

- 6.3.8 Innovaccer

- 6.3.9 Lightbeam Health Solutions

- 6.3.10 Medecision

- 6.3.11 Netsmart

- 6.3.12 Oracle Health (Cerner)

- 6.3.13 PointClickCare

- 6.3.14 Qventus

- 6.3.15 Salesforce (Health Cloud)

- 6.3.16 Signify Health (CVS)

- 6.3.17 Unite Us

- 6.3.18 Veradigm

- 6.3.19 WellSky (CarePort)

- 6.3.20 ZeOmega

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment