|

시장보고서

상품코드

2063871

치내요법용 소모품 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Endodontic Consumables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

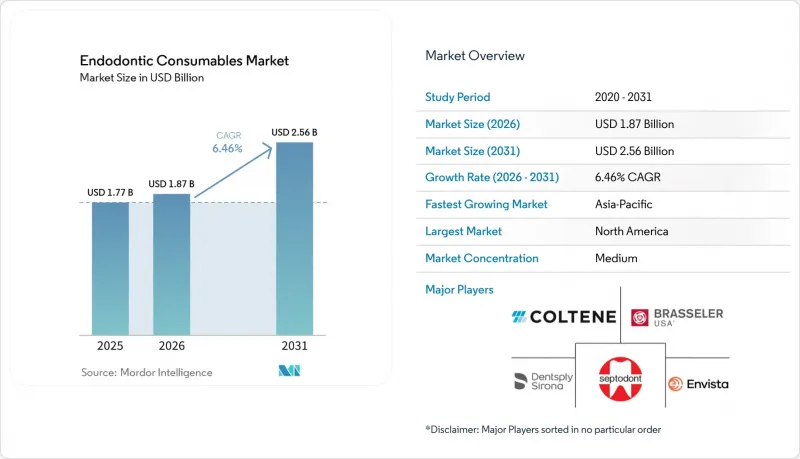

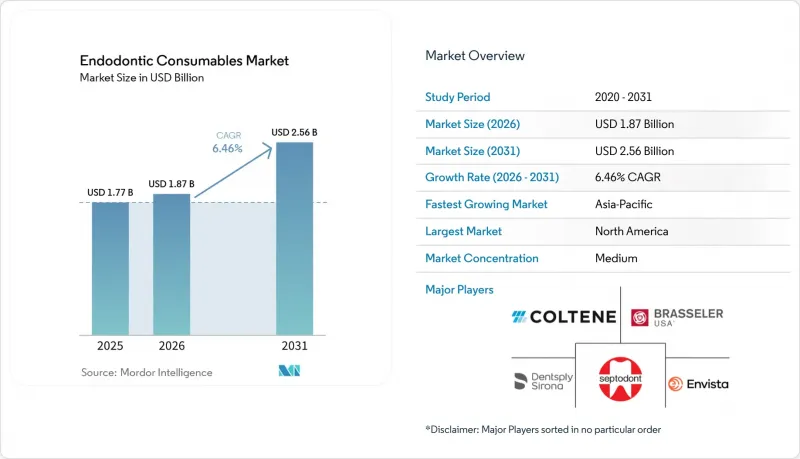

Mordor Intelligence에 의하면, 치내요법용 소모품 시장 규모는 2025년 17억 7,000만 달러에서 2026년에는 18억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 6.46%로 성장을 지속하여, 2031년까지 25억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(치과용 버·드릴, 치과용 댐, 치내요법용 파일 등), 시술 유형(접근 형성, 성형·세정 등), 최종 사용자(치과 병원, DSO/그룹 진료소, 치과 병원, 학술·연구 기관), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 치내요법용 소모품 시장 동향 및 인사이트

근관 치료 건수 증가와 자연치아 보존에 대한 경향

세계 임상 현장에서는 자연치아 보존이 여전히 중요하게 여겨지고 있으며, 이것이 치내요법용 소모품 시장 전체에서 파일, 실러, 콘 및 세척용 소모품에 대한 수요를 뒷받침하고 있습니다. 최근 문헌에 보고된 1차 근관 치료의 성공률은 80%대 중반에서 후반, 90%대 초반에 달하며, 재치료 결과도 70%대 후반에서 80%대 초반으로 양호한 수준을 유지하고 있어, 이는 고성능 재료 및 기술에 대한 지속적인 투자를 뒷받침하고 있습니다. 복원 전략은 장기적인 생존율에 있어 매우 중요하며, 직접 복원에 비해 크라운을 씌우는 것이 유지력을 향상시킵니다. 이는 보존적인 성형 및 충전 방법을 선택함으로써 치관 구조와 페룰 효과를 유지하는 워크플로우의 가치를 입증하는 것입니다.

잔존 치질과 치료 실패 위험 간의 연관성을 보여주는 증거는 효과적인 봉쇄를 달성하면서도 불필요한 상아질 제거를 최소화할 수 있는 유연하고 내피로성이 뛰어난 파일 및 생체활성 실러의 중요성을 부각시키고 있습니다. 바이오세라믹 실러에 관한 임상 시리즈 데이터(12개월 시점의 높은 치유율 포함)는 전문의와 다수의 진료 사례를 보유한 일반 치과의사들의 채택을 더욱 촉진하고 있으며, 이는 치내요법용 소모품 시장의 꾸준한 성장을 뒷받침하고 있습니다. 이러한 성과들이 맞물려 발치보다 보존 치료가 우선시되는 경향이 지속되고 있으며, 이에 따라 시술 건수가 증가하여 치내요법용 소모품 시장 전체의 지출을 뒷받침하고 있습니다.

일반 치과 진료에서 NiTi 로터리/레시프로 파일 시스템의 보급

니켈-티타늄 재질의 로터리 및 레시프로 플랫폼은 전문의 전용에서 많은 일반 치과 진료소의 표준 도구로 자리 잡으면서, 사례당 소모품 사용량과 치내요법용 소모품 시장 전체의 지출을 증가시키고 있습니다. FireWire 처리 시스템 등의 열처리 방법과 독자적인 금속 공학 기술을 통해, 기존 세대 제품에 비해 2-6배 높은 반복 피로 강도를 실현함으로써, 올바르게 사용하면 분리 사고를 줄이면서 휘어진 근관이나 석회화된 근관을 보다 안전하게 관통할 수 있게 되었습니다. 한편, 발표된 연구에 따르면, 조작, 재사용, 근관의 곡률 및 시술자의 경험에 따라 기구 파절률이 1% 미만에서 한 자릿수 초반 대에 이르는 것으로 여전히 보고되고 있으며, 이에 따라 치내요법용 소모품 시장에서는 훈련 및 일회용 전략이 계속해서 주목받고 있습니다.

XP-4D 시스템에 상세하게 설명된 바와 같이, 여러 차례의 가열 처리 전략 및 적응형 설계는 비틀림 피로와 굽힘 피로에 대한 내성을 유지하면서 상아질의 보존과 효과적인 성형 간의 균형을 맞추는 것을 목적으로 합니다. 최근 510(k) 승인 결정에서 참조되고 있는 ISO 10993 생체적합성 및 ISO 6876 성능 지표를 포함한 새로운 파일 시스템에 대한 규제 안전 기준은 기본적인 안전성과 성능을 확보하는 데 도움이 되며, 견고한 품질 관리 시스템을 갖춘 공급업체를 우대합니다. 이러한 전환이 진행됨에 따라, 일반 치과 진료에서 간소화된 왕복 운동 순서가 채택되면서 치내요법용 소모품 시장 수요 기반이 계속해서 확대되고 있습니다.

프리미엄 파일 및 충전재의 높은 1건당 비용

고급 열처리 NiTi 파일이나 바이오세라믹 충전 시스템은 단가가 높기 때문에 가격에 민감한 환경에서 도입을 저해하는 요인이 되며, 치내요법용 소모품 시장에서 파절 위험을 높일 가능성이 있는 재사용 행위를 조장하고 있습니다. 원자재 가격 변동도 가격 압박의 한 요인으로 작용하고 있으며, 2025년에는 의료용 니켈-티타늄 선의 가격이 폭넓은 범위에서 등락할 것으로 보고되어, 엄격한 조달 및 사용 방침의 필요성이 더욱 커지고 있습니다. 시장 피드백에 따르면, 매주 안정적인 환자 수를 처리하는 치과에서는 효율과 비용을 저울질하며, 치내요법용 소모품 시장의 재료비를 관리하기 위해 단일 파일 방식의 리시프로케이션, 간소화된 세척, 그리고 용제 선택을 고려하는 경우가 많은 것으로 보입니다.

임상 현장에서 얻은 정성적 연구 결과에 따르면, 예산 제약으로 인한 재사용 기간의 장기화가 피로로 인한 파손으로 이어질 가능성이 상세하게 밝혀졌으며, 가능한 한 명확한 일회용 사용 방침의 필요성이 부각되고 있습니다. 공급업체 측의 대응으로는 치내요법용 소모품 시장의 다양한 진료 프로파일에 맞추어 비용, 안전성, 성능의 균형을 도모하는 것을 목적으로 한 단계별 제품 라인업 및 대상층을 좁혀 진행한 교육 활동 등을 들 수 있습니다. 임상적 근거에 기반한 일관된 ‘비용 대비 가치’ 프레임워크는 치료 성과나 업무 흐름의 효율성이 그 비용에 상응할 경우, 이해관계자들이 고가 제품을 선택하는 것이 정당함을 입증하는 데 도움이 됩니다.

부문별 분석

근관용 파일은 2025년에 치내요법용 소모품 시장의 36.39% 점유율을 차지해, 2031년까지 연평균 성장률(CAGR) 6.98%로 성장하여 다른 소모품 부문을 앞지를 것으로 전망됩니다. 스테인리스 스틸 핸드 파일에서 열처리 니켈-티타늄 로터리 및 레시프로 시스템으로의 전환은 여전히 주요 촉진요인으로 작용하고 있습니다. 이는 임상의들이 유연성, 절삭 효율, 그리고 치료 시간을 단축시켜 주는 예측 가능한 성형 결과를 원하기 때문입니다. 금속 공학의 발전으로 인해 기존 플랫폼보다 높은 주기적 피로 내구성이 실현되었으며, 곡선형 근관에서 안전 여유가 향상되어 일반 치과 진료 분야에서 더욱 광범위하게 채택되고 있습니다. 충전 분야에서는 가타파차 콘을 독자적인 파일 형상에 맞추어 사용함으로써, 치근단부의 적합성이 향상되었고, 수술 중 조정 횟수가 줄었습니다. 이로 인해 치내요법용 소모품 시장에서 싱글 콘 방식의 효율성이 강화되고 있습니다. 또한, 치내요법용 소모품 업계에서는 보존적인 성형과 확실한 봉쇄를 가능하게 하는 기기나 화학 약품에 대한 관심이 높아지고 있으며, 공급업체의 가치는 단순한 파일 그 자체를 넘어 확장되고 있습니다.

실러, 세정액, 근관 내 약제, 페이퍼 포인트 등을 포함한 소모품 중 ‘기타’ 부문은 다양한 성장 경로를 보이고 있으며, 그중에서도 바이오세라믹 실러가 치내요법용 소모품 시장의 주요 성장 동력으로 두각을 나타내고 있습니다. 에폭시계 및 바이오세라믹 실러 모두에 대한 규제 당국의 승인은 ISO 성능 기준 준수는 물론, 안정성과 유동성을 목표로 한 지속적인 소재 혁신을 입증하고 있습니다. 사전 혼합된 삼칼슘실리케이트계 실러의 승인은 생체활성 제품군의 미래 가능성을 입증하는 것이며, 일반 치과의사 및 전문의에게 근관 충전 절차의 표준화에 기여하고 있습니다. 바이오세라믹 잔여물을 용해하는 특수 용매 기술은 재치료 시 파일 제거 전략을 보완해 주며, 단단한 상아질에 부착되어 재진입이 어려운 경우 시술의 유연성을 높여 치내요법용 소모품 시장에 기여하고 있습니다. EDM(방전 가공) 기반프로파일 등, 표면 공학을 적극 활용한 프리미엄 파일 시리즈는 그 신뢰성과 효율성 덕분에 기구에 가해지는 부담과 진료 시간을 현저히 줄일 수 있어, 계속해서 가격 결정력을 유지하고 있습니다.

지역별 분석

2025년 북미는 치내요법용 소모품 시장 규모의 44.14%를 차지했습니다. 이는 전문의의 밀도가 높고, 로터리 기구의 보급률이 높으며, 전문의에 의한 바이오세라믹 충전의 조기 도입에 힘입은 결과입니다. 규제 당국의 승인 절차는 주요 재료 및 기기의 유효성을 지속적으로 입증하고 있으며, 이를 통해 신제제에 대한 신뢰도가 높아지고, 치내요법용 소모품 시장 전체의 업그레이드 주기가 강화되고 있습니다. 대규모 진료 네트워크는 조달 기준에 영향을 미치며, 주요 소모품 및 관련 디지털 도구의 표준화를 촉진하고 있어, 이에 따라 통합형 솔루션에 대한 수요가 확대되고 있습니다. 북미에서 강력한 유통 및 서비스망을 갖춘 제조업체들의 투자는 교육, 근거 창출, 그리고 진료 현장 도입을 지원하고 있으며, 이러한 요소들이 예측 기간 동안 교체 수요를 지속시키고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.89%를 나타낼 것으로 예측되며, 도시 지역의 진료소 확대와 소득 증가에 힘입어 고도의 치근관 치료 및 최신 장비에 대한 접근성이 확대되고 있습니다. 전문의가 운영하는 진료소나 진료 건수가 많은 클리닉은 열처리 NiTi 시스템 및 바이오세라믹 워크플로우를 조기에 도입한 곳이며, 이를 위해서는 치내요법용 소모품 시장에서 호환 가능한 셰이핑 파일, 적합한 콘, 그리고 관련 화학제품이 필요합니다. 디지털 영상 진단에 대한 투자는 진단 및 재치료 계획의 정확도를 높여주며, 치료 대상 범위의 확대와 복잡성 증가에 따라 실러, 파일, 세척 및 관류용 부품에 대한 수요를 끌어올리고 있습니다. 온라인 조달 채널과 현지 생산을 통해 제품의 입수 가능성이 높아짐에 따라, 진료소에서는 표준화된 키트를 도입할 수 있게 되어, 치내요법용 소모품 시장 전체의 처리 능력과 균일성이 향상됩니다.

유럽은 탄탄한 전문의 커뮤니티, 대학의 교육 인프라, 그리고 진단 및 치료 계획 수립 과정에서 CBCT가 광범위하게 활용되고 있는 점에 힘입어 여전히 큰 시장 점유율을 유지하고 있습니다. 영국에서 전문의의 진료 현황을 조사한 결과, 협시야 CBCT의 도입률과 보유율이 높은 것으로 나타났으며, 이는 영상 진단의 모범 사례 원칙에 부합하는 것으로, 치내요법용 소모품 시장에서 복잡한 증례의 관리를 지원하고 있습니다. 중동 및 아프리카 및 남미 전역에서는 선택적 치료와 전문 의료 서비스를 제공하는 민간 클리닉이 프리미엄 부문의 소비를 주도하고 있지만, 성장 양상은 국가나 지불 주체 구조에 따라 다릅니다. 교육 및 기술에 대한 접근성이 확대됨에 따라, 해당 지역에서는 수요가 더욱 증가할 것으로 예상되며, 표준화된 워크플로우와 제품 키트를 통해 치내요법용 소모품 시장에서 의료기관 간의 일관성이 향상될 것으로 전망됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the endodontic consumables market size is expected to grow from USD 1.77 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.56 billion by 2031 at 6.46% CAGR over 2026-2031.

This report is Segmented by Product Type (Dental Burs & Drills, Dental Dams, Endodontic Files, and More), Procedure Type (Access Preparation, Shaping and Cleaning, and More), End User (Dental Clinics, DSO/Group Practices, Dental Hospitals, and Academic and Research Institutes), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Endodontic Consumables Market Trends and Insights

Rising Root Canal Treatment Volumes and Preference for Tooth Preservation

Global clinical practice continues to emphasize conserving the natural tooth, which sustains demand for files, sealers, cones, and irrigation supplies across the endodontic consumables market. Primary root canal success rates reported in recent literature sit in the mid-to-high 80s to low 90s, while retreatment outcomes remain favorable in the upper 70s to low 80s, which supports ongoing investment in higher performing materials and techniques. Restoration strategy is critical to long-term survival, with crown coverage improving retention compared with direct restorations, which reinforces the value of workflows that preserve coronal structure and ferrule effect through conservative shaping and obturation choices.

Evidence linking residual tooth structure to failure risk highlights the premium placed on flexible, fatigue-resistant files and bioactive sealers that minimize unnecessary dentin removal while achieving an effective seal. Clinical-series data for bioceramic sealers, including high healing rates at 12 months, further encourage specialist and high-volume generalist adoption that supports steady growth in the endodontic consumables market. Together these outcomes maintain a preference for retention over extraction, which expands procedure volumes and underpins spending across the endodontic consumables market.

Penetration of NiTi Rotary/Reciprocating File Systems into General Practice

Nickel-titanium rotary and reciprocating platforms have moved from specialist-only use to standard tools in many general practices, lifting per-case consumable use and spend across the endodontic consumables market. Thermal processing methods and proprietary metallurgy, such as FireWire-treated systems, have delivered 2-6 times higher cyclic fatigue resistance than earlier file generations, enabling safer navigation of curved and calcified canals with fewer separation events when used correctly. At the same time, published studies still report instrument separation spanning under 1% to the low double digits depending on motion, reuse, canal curvature, and operator experience, which keeps training and single-use strategies in focus for the endodontic consumables market.

Multi-treatment heat strategies and adaptive designs, such as those detailed for the XP-4D system, aim to balance dentin preservation with effective shaping while maintaining resistance to torsional and flexural fatigue. Regulatory guardrails for new file systems, including ISO 10993 biocompatibility and ISO 6876 performance metrics referenced in recent 510(k) decisions, help ensure baseline safety and performance and favor vendors with robust quality systems. As this transition deepens, general-practice adoption of simplified reciprocating sequences continues to broaden the demand base for the endodontic consumables market.

High Per-Case Cost of Premium Files and Obturation Materials

Premium heat-treated NiTi files and bioceramic obturation systems carry higher unit costs, which pressures adoption in price-sensitive settings and encourages reuse behaviors that can raise fracture risk in the endodontic consumables market. Volatile feedstock costs contribute to price pressure, with medical-grade nickel-titanium wire pricing documented across a wide band during 2025, reinforcing the need for disciplined procurement and usage policies. Market feedback shows that clinics performing steady weekly case volumes weigh efficiency against cost, often evaluating single-file reciprocation, simplified irrigation, and solvent choices to manage the bill of materials in the endodontic consumables market.

Qualitative insights from clinical settings detail how extended reuse due to budget constraints can lead to fatigue-induced failures, highlighting the need for clear single-use policies where feasible. Vendor responses include tiered portfolios and targeted education aimed at balancing cost, safety, and performance for different practice profiles in the endodontic consumables market. Consistent cost-to-value framing with clinical evidence helps stakeholders justify premium choices when outcomes and workflow efficiency merit the spend.

Other drivers and restraints analyzed in the detailed report include:

- Practice Consolidation and DSOs Standardizing Endodontic Procurement

- Adoption of Bioceramic Sealers and Single-Cone Obturation Workflows

- Instrument Separation Risk and Clinician Learning Curve

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Endodontic files captured 36.39% endodontic consumables market share in 2025 and are projected to grow at a 6.98% CAGR through 2031, outpacing other consumable categories. The transition from stainless-steel hand files to heat-treated nickel-titanium rotary and reciprocating systems remains the central driver, as clinicians seek flexibility, cutting efficiency, and predictable shaping outcomes that shorten chair time across the endodontic consumables market. Metallurgy advancements have pushed cyclic fatigue resistance multiples higher than legacy platforms, improving safety margins in curved canals and supporting broader general-practice adoption. Within obturation, matching gutta-percha cones to proprietary file geometries has enhanced apical fit and reduced intraoperative adjustments, reinforcing single-cone efficiency in the endodontic consumables market. The endodontic consumables industry has also seen momentum around devices and accessory chemistries that enable conservative shaping and reliable sealing, extending vendor value beyond standalone files.

The "others" within consumables, which include sealers, irrigation solutions, intracanal medicaments, and paper points, hold diverse growth paths, with bioceramic sealers standing out as the key growth engine in the endodontic consumables market. Regulatory clearances for both epoxy-based and bioceramic sealers underscore adherence to ISO performance criteria and ongoing material innovation targeted at stability and flow. Approvals for premixed tricalcium silicate-based sealers affirm the bioactive pipeline and help standardize obturation steps for generalists and specialists. Specialized solvent chemistries that dissolve bioceramic residues now complement file removal strategies in retreatment, adding procedural flexibility where strong dentin adhesion complicates re-entry in the endodontic consumables market. Premium file families with surface engineering, such as EDM-based profiles, continue to command pricing power where reliability and efficiency demonstrably reduce instrument stress and chair time.

Geography Analysis

North America commanded 44.14% of the endodontic consumables market size in 2025, supported by high specialist density, strong adoption of rotary instrumentation, and early uptake of bioceramic obturation among specialists. Regulatory pathways continue to validate key materials and devices, adding credibility for new formulations and reinforcing the upgrade cycle across the endodontic consumables market. Large practice networks influence procurement norms, helping standardize core consumables and associated digital tools, which channels more volume to integrated solutions. Investments by manufacturers with strong North American distribution and service footprints support training, evidence generation, and practice integration that sustain replacement demand over the forecast period.

Asia-Pacific is projected to grow at a 6.89% CAGR through 2031, with urban clinic expansion and rising incomes broadening access to advanced endodontic care and modern instrumentation. Specialist practices and high-volume clinics are early adopters of heat-treated NiTi systems and bioceramic workflows, which requires compatible shaping files, matched cones, and accessory chemistries in the endodontic consumables market. Digital imaging investments improve diagnosis and retreatment planning, which lifts demand for sealers, files, and irrigation components given expanded case identification and complexity. As online procurement channels and local manufacturing improve product availability, clinics can adopt standardized kits that enhance throughput and uniformity across the endodontic consumables market.

Europe maintains a substantial share backed by robust specialist communities, university training infrastructure, and widespread use of CBCT for diagnosis and treatment planning. Surveys of specialist utilization in the United Kingdom show high adoption and ownership of small field-of-view CBCT, which aligns with best-practice imaging principles and supports complex case management in the endodontic consumables market. Across the Middle East and Africa and South America, private clinics serving elective and specialist care drive consumption in premium categories, though growth patterns vary by country and payer structure. As training and technology access increase, these regions are expected to contribute incremental volume, with standardized workflows and product kits improving consistency across settings in the endodontic consumables market.

- Angelus

- Brasseler USA

- COLTENE Group

- Dentsply Sirona

- DiaDent

- EdgeEndo

- Envista

- Essential Dental Systems

- FKG Dentaire

- GC Corporation

- Hu-Friedy

- MANI, Inc.

- META Biomed

- Micro-Mega

- Neoendo

- Pulpdent Corporation

- Septodont

- Solventum Corporation

- Ultradent Products

- VDW GmbH

- Zarc4Endo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Root Canal Treatment Volumes and Preference for Tooth Preservation

- 4.2.2 Penetration of NiTi Rotary/Reciprocating File Systems into General Practice

- 4.2.3 Practice Consolidation and DSOs Standardizing Endodontic Procurement

- 4.2.4 Adoption of Bioceramic Sealers and Single-Cone Obturation Workflows

- 4.2.5 CBCT-Driven Case Selection Expanding Retreatment and Complex Indications

- 4.2.6 Expansion of Private-Label and E-Commerce Channels in Emerging Markets

- 4.3 Market Restraints

- 4.3.1 High Per-Case Cost of Premium Files and Obturation Materials

- 4.3.2 Instrument Separation Risk and Clinician Learning Curve

- 4.3.3 Case Diversion to Implants for Complex Failures

- 4.3.4 Supply Risk and Price Volatility in Niti Alloy and Gutta-Percha Feedstocks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Dental Burs & Drills

- 5.1.2 Dental Dams

- 5.1.3 Endodontic Files

- 5.1.4 Gutta-percha Points

- 5.1.5 Others (Dental Sealers, etc.)

- 5.2 By Procedure Type

- 5.2.1 Access preparation

- 5.2.2 Shaping and cleaning

- 5.2.3 Others (Irrigation and intracanal disinfection, Post-endodontic restoration, etc.)

- 5.3 By End User

- 5.3.1 Dental Clinics

- 5.3.2 DSO/group practices

- 5.3.3 Dental hospitals

- 5.3.4 Academic and research institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Angelus

- 6.3.2 Brasseler USA

- 6.3.3 COLTENE Group

- 6.3.4 Dentsply Sirona

- 6.3.5 DiaDent Group International

- 6.3.6 EdgeEndo

- 6.3.7 Envista

- 6.3.8 Essential Dental Systems

- 6.3.9 FKG Dentaire

- 6.3.10 GC Corporation

- 6.3.11 Hu-Friedy

- 6.3.12 MANI, Inc.

- 6.3.13 META Biomed

- 6.3.14 Micro-Mega

- 6.3.15 Neoendo

- 6.3.16 Pulpdent Corporation

- 6.3.17 Septodont

- 6.3.18 Solventum Corporation

- 6.3.19 Ultradent Products

- 6.3.20 VDW GmbH

- 6.3.21 Zarc4Endo

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment