|

시장보고서

상품코드

2063896

북미의 오프쇼어 헬리콥터 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America Offshore Helicopter Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

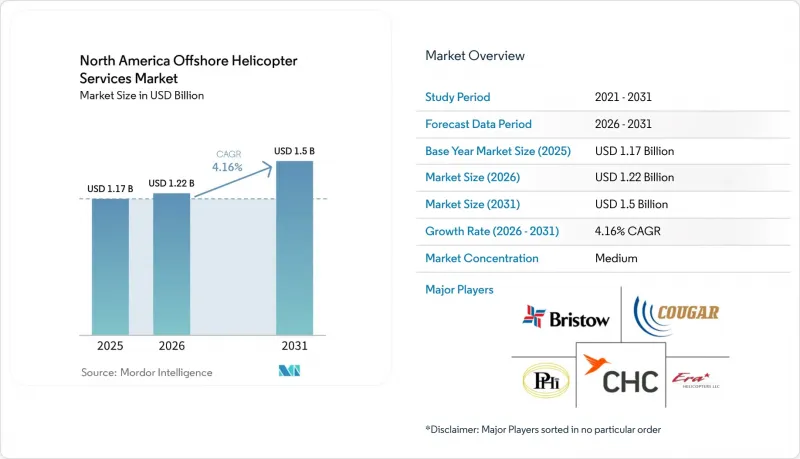

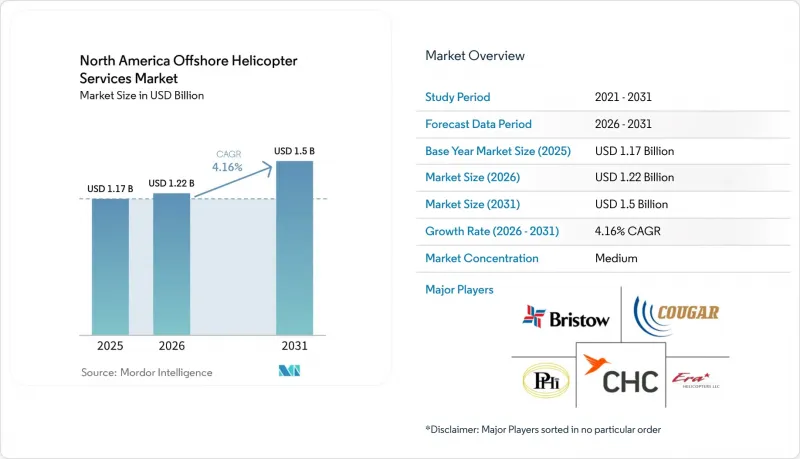

Mordor Intelligence에 의하면, 북미 오프쇼어 헬리콥터 서비스 시장 규모는 2025년 11억 7,000만 달러에서 2026년에는 12억 2,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 4.16%로 성장을 지속하여, 2031년까지 15억 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(경형, 중형, 대형 헬리콥터), 용도별(승무원 수송, 화물 수송, 점검·감시·측량, 이전·폐지 지원, 기타), 최종 사용자 산업별(석유 및 가스, 해상 풍력, 해운·선박, 기타), 지역별(미국, 캐나다, 멕시코)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 오프쇼어 헬리콥터 서비스 시장 동향 및 인사이트

심해 해양 개발 활동 증가

2024년 3월에 실시된 멕시코만 임대권 경매 261에서는 39만 5,000에이커에 달하는 73개 구획이 낙찰되었으며, 최고 입찰가는 3억 8,200만 달러에 달했습니다. 이는 후마 및 라파예트 육상 기지에서 헬리콥터로 90분이 소요되는 수심 깊은 해역에 위치한 광구에 대해 사업자가 강한 관심을 보이고 있음을 보여줍니다. 이에 이어 쉘은 2025년부터 2026년까지 수심 1,500미터 이하의 유망 지역을 대상으로 최대 4개의 탐사정 시추를 승인함으로써, 해상 상태 6(Sea State 6) 생존 요건을 충족하는 중형 및 대형 헬리콥터에 대한 수요를 지속시키고 있습니다. 멕시코의 트리온 유전(해안에서 180킬로미터 떨어진 해저 2,500미터 지점)에서는 2024년에 시추가 시작될 예정이며, 2028년에는 탐피코를 거점으로 하는 슈퍼미디엄급 선박을 이용해 승무원을 교대해야 하는 24개의 해저 유정 시추가 계획되어 있습니다. 세이블 섬 지역을 대상으로 하는 노바스코샤주의 2026년 라이선싱 라운드는 단기적으로 시추공 수가 낮은 수준을 유지하더라도 캐나다 대서양 연안 부문에 새로운 활력을 불어넣고 있습니다. 심해 작업에는 본질적으로 더 넓은 객실, 보조 연료 및 비상 부력 키트가 필요하기 때문에 북미 해양 헬리콥터 서비스 시장에서 구조적인 수요 하한선이 형성되고 있습니다.

해양 석유 및 가스 프로젝트의 실현 가능성 제고

멕시코만 심해 유정의 지역별 손익분기점은 해저 생산 설비의 표준화와 시추 기간 단축으로 인해 현재 브렌트 원유 1배럴당 35-45달러 수준입니다. 이에 따라 상품 가격의 변동에도 불구하고, 사업자들은 수년까지 헬리콥터 운항 능력을 확보하도록 장려받고 있습니다. 멕시코만의 생산량은 2026년에 하루 196만 배럴에 달하고, 팬데믹 이전 수준을 상회하고 있으며, 이는 예측 가능한 비행 시간 구매를 뒷받침하고 있습니다. 뉴펀들랜드 연안에서 에퀴노르(Equinor)가 개발을 추진 중인 베이 뒤 노르(Bay du Nord) 프로젝트는 2027년에 승인을 받아 2031년에 첫 원유 생산을 시작할 예정입니다. 이 프로젝트에서는 세인트존스에서 270해리 거리의 장거리 비행이 필요하기 때문에 대형 쌍발기를 통한 수송 능력 유지를 정당화할 수 있습니다. 웨스트 화이트 로즈의 2026년 가동 개시 및 헤브론과 하이베르니아에서의 타이백 프로젝트는 캐나다가 2050년까지 탄소 중립을 목표로 하는 가운데에서도 기준선 수요를 확실하게 뒷받침할 것입니다. 따라서 프로젝트의 경제성이 향상됨에 따라, 과거 북미 오프쇼어 헬리콥터 서비스 시장 특징이었던 수익 변동성이 줄어들고 있습니다.

승무원 수송선(CTV)과의 경쟁

WINDEA 및 Atlantic Wind Transfers가 운항하는 존스법(Jones Act)을 준수하는 CTV(승무원 수송선)는 왕복 요금을 150-250달러로 책정하고 있으며, 동등한 헬리콥터 좌석 요금인 800-1,200달러와 비교했을 때, 미국 풍력 발전소의 인력 수송의 약 85%를 차지하고 있습니다. 현재, 흔들림 보정 기능이 탑재된 갱웨이를 통해 파고 1.5미터의 상황에서도 안전하게 승하선할 수 있으며, 이는 뉴욕만 연안에서 대부분의 운영일에 나타나는 조건입니다. 헬리콥터는 응급 의료 이송, 경영진의 시찰, 겨울철 긴급 수송에서 없어서는 안 될 역할을 수행하고 있지만, 이러한 임무는 해상 풍력 발전 현장에서의 근무 시간 중 불과 10-15%에 불과합니다. 풍력 발전 용량이 확대됨에 따라 CTV와의 경쟁으로 인해 북미 오프쇼어 헬리콥터 서비스 시장의 해당 부문에서 회전익 항공기의 수익 상한선이 설정될 것입니다.

부문별 분석

중형 헬리콥터는 2025년 매출의 51.7%를 차지했으나, AW169 및 H135 기종이 해상 풍력 발전소의 승무원 수송에서 빈번한 점검 비행으로 용도가 전환됨에 따라, 북미 오프쇼어 헬리콥터 서비스 시장에서 경량 쌍발기 시장 규모는 2031년까지 연평균 성장률(CAGR) 6.6%로 확대될 것으로 예측됩니다. 시장 수익의 28%를 차지하는 대형 헬리콥터의 수송 능력은 운영사들이 유지보수 비용이 높은 S-92 및 H225 기체를 퇴역시키면서 점차 축소되고 있습니다. AW189나 조만간 인증을 받을 예정인 Bell 525와 같은 슈퍼 미디엄급 신형 기종은 승객 1마일당 연료 소비량 측면에서 20-30%의 우위를 보이고 있으며, 이것이 PHI, CHC, Bristow가 18개월의 리드타임에도 불구하고 막대한 규모의 주문을 진행하고 있는 이유를 설명해 줍니다.

슈퍼 미디엄 기종의 도입 확대는 임무 최적화를 촉진하고 있습니다. 조종사들은 더 이상 헬리콥터를 ‘만능 자산’으로 취급하지 않고, 대신 작업 부하에 맞추어 기체를 최적화하고 있습니다. 예를 들어, 심해에서의 승무원 교대에는 대형 쌍발기를 배치하고, 터빈 블레이드 점검이나 항만 조타사의 왕복 수송에는 경량 쌍발기를 배정하는 식입니다. 이러한 세심한 장비 구성을 통해 가동률을 높임으로써, 매출 성장세가 정체되는 시나리오에서도 북미 오프쇼어 헬리콥터 서비스 시장이 수익성을 유지하는 데 기여하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the north america offshore helicopter services market size is expected to grow from USD 1.17 billion in 2025 to USD 1.22 billion in 2026 and is forecast to reach USD 1.5 billion by 2031 at 4.16% CAGR over 2026-2031.

This report is Segmented by Type (Light, Medium, Heavy Helicopters), Application (Crew Transport, Cargo Transport, Inspection/Monitoring/Surveying, Relocation/Decommissioning Support, and Others), End-User Industry (Oil and Gas, Offshore Wind, Marine and Shipping, and More), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Offshore Helicopter Services Market Trends and Insights

Rising Deep-Water Offshore Development Activity

Gulf of Mexico Lease Sale 261 in March 2024 awarded 73 tracts covering 395,000 acres and produced USD 382 million in high bids, demonstrating strong operator appetite for acreage in water depths that necessitate 90-minute helicopter transits from Houma and Lafayette shore bases. Shell followed by approving up to four exploration wells for 2025-2026 targeting prospects below 1,500 meters, sustaining call-outs for medium and heavy helicopters certified to Sea State 6 survival requirements. Mexico's Trion field, 180 kilometers offshore at 2,500 meters, began drilling in 2024 and plans 24 subsea wells that will rely on Tampico-based super-medium aircraft for crew rotations as soon as 2028. Nova Scotia's 2026 licensing round covering the Sable Island area re-energizes Canada's Atlantic offshore sector even if near-term well counts stay low . Deep-water campaigns inherently require larger cabins, auxiliary fuel, and emergency-flotation kits, creating a structural demand floor for the North America offshore helicopter services market.

Improved Viability of Offshore Oil & Gas Projects

Regional breakeven prices for deep-water Gulf of Mexico wells now sit at USD 35-45 per barrel Brent thanks to standardized subsea trees and faster drill-times, encouraging operators to commit to multi-year helicopter capacity blocks despite commodity swings. Gulf production climbed to 1.96 million barrels per day in 2026, above the pre-pandemic level and supporting predictable flight-hour purchasing. Equinor's Bay du Nord development offshore Newfoundland, expected to sanction in 2027 with first oil in 2031, will need long-range flights of 270 nautical miles from St. John's, justifying heavy twin-engine capacity retention. West White Rose's 2026 startup and tie-back projects at Hebron and Hibernia safeguard baseline demand even as Canada targets net-zero by 2050. Stronger project economics therefore decrease the revenue volatility that once typified the North America offshore helicopter services market.

Competition from Crew-Transfer Vessels

Jones Act-compliant CTVs operated by WINDEA and Atlantic Wind Transfers price a round trip at USD 150-250 versus USD 800-1,200 for comparable helicopter seats, absorbing roughly 85% of personnel transfers at U.S. wind farms . Motion-compensated gangways now allow safe transfers in 1.5-meter wave heights, conditions that represent most operational days along the New York Bight. Helicopters retain indispensable roles for emergency medical evacuation, senior-executive visits, and winter contingency transport, but those missions account for only 10-15% of offshore-wind labor hours. As wind capacity expands, CTV competition will cap the upside for rotary-wing revenues in that segment of the North America offshore helicopter services market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of U.S. Offshore-Wind Construction Zone

- Fleet-Modernization Cycle

- High Operating & Maintenance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium helicopters retained 51.7% of 2025 revenue, yet the North America offshore helicopter services market size for light twins is projected to grow at 6.6% CAGR through 2031 as AW169 and H135 aircraft migrate from offshore-wind crew transfer to high-frequency inspection flights. Heavy-lift capacity, still 28% of market revenue, is slowly shrinking as operators retire high-maintenance S-92 and H225 airframes. Super-medium newcomers such as the AW189 and soon-to-be-certified Bell 525 deliver a 20-30% fuel-burn advantage per passenger-mile, explaining why PHI, CHC, and Bristow are placing sizeable orders despite 18-month lead times .

Super-medium fleet uptake promotes mission optimization. Operators no longer treat helicopters as one-size-fits-all assets; instead, they tailor capacity to workload, deploying heavy twins for deep-water crew rotations while assigning light twins to turbine-blade inspections and harbor-pilot shuttles. This nuanced fleet mix keeps utilization high and helps the North America offshore helicopter services market defend profitability even under flat topline growth scenarios.

List of Companies Covered in this Report:

- Bristow Group Inc.

- PHI Inc.

- CHC Helicopter

- Era Helicopters LLC

- Cougar Helicopters Inc.

- Babcock International Group PLC

- Air Center Helicopters Inc.

- HNZ Group Ltd.

- Omni Helicopters International

- Gulf Helicopters Co.

- NHV Group

- Abu Dhabi Aviation Co.

- Leonardo SpA

- Airbus SE

- Lockheed Martin/Sikorsky

- Textron (Bell)

- Russian Helicopters JSC

- Kaman Corp.

- Heli-One (CHC MRO)

- Petroleum Helicopters International (PHI)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising deep-water offshore development activity

- 4.2.2 Improved viability of offshore oil & gas projects

- 4.2.3 Expansion of U.S. offshore-wind construction zone

- 4.2.4 Fleet-modernization cycle (AW139/S-92 replacements)

- 4.2.5 U.S. SAF tax-credit incentives lowering fuel costs

- 4.2.6 AI-driven predictive-maintenance savings

- 4.3 Market Restraints

- 4.3.1 Competition from crew-transfer vessels (CTV)

- 4.3.2 High operating & maintenance costs

- 4.3.3 Oil-price volatility reducing drilling programs

- 4.3.4 FAA Part-135 retrofit mandates (avionics/safety)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Light Helicopters

- 5.1.2 Medium Helicopters

- 5.1.3 Heavy Helicopters

- 5.2 By Application

- 5.2.1 Crew Transport

- 5.2.2 Cargo Transport

- 5.2.3 Inspection, Monitoring, and Surveying

- 5.2.4 Relocation and Decommissioning Support

- 5.2.5 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Offshore Wind

- 5.3.3 Marine and Shipping

- 5.3.4 Government and Defence

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Bristow Group Inc.

- 6.4.2 PHI Inc.

- 6.4.3 CHC Helicopter

- 6.4.4 Era Helicopters LLC

- 6.4.5 Cougar Helicopters Inc.

- 6.4.6 Babcock International Group PLC

- 6.4.7 Air Center Helicopters Inc.

- 6.4.8 HNZ Group Ltd.

- 6.4.9 Omni Helicopters International

- 6.4.10 Gulf Helicopters Co.

- 6.4.11 NHV Group

- 6.4.12 Abu Dhabi Aviation Co.

- 6.4.13 Leonardo SpA

- 6.4.14 Airbus SE

- 6.4.15 Lockheed Martin/Sikorsky

- 6.4.16 Textron (Bell)

- 6.4.17 Russian Helicopters JSC

- 6.4.18 Kaman Corp.

- 6.4.19 Heli-One (CHC MRO)

- 6.4.20 Petroleum Helicopters International (PHI)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment