|

시장보고서

상품코드

2063898

드릴 칼라 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Drill Collar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

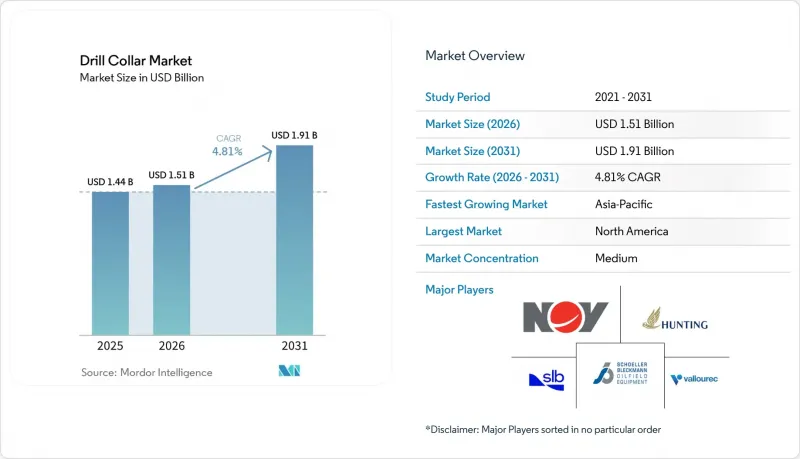

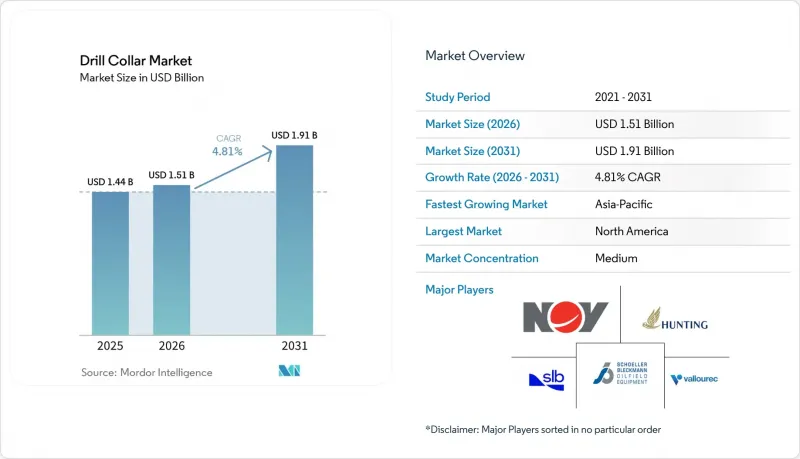

Mordor Intelligence에 의하면, 드릴 칼라 시장 규모는 2025년에 14억 4,000만 달러, 2026년에 15억 1,000만 달러, 2031년까지 19억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 4.81%로 성장할 전망입니다.

본 보고서는 유형(표준 강제 드릴 칼라, 비자성 드릴 칼라), 재질 등급(4145H 개질강, 4330V강, 비자성 14Cr-MoV 스테인리스 스틸), 도입 형태(육상, 해양), 용도(육상 시추 장비, HPHT 유정, 방향성·수평 시추), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)에 따라 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계 드릴 칼라 시장 동향 및 인사이트

2025년 이후 전 세계 시추 장비 수의 회복

수년에 걸친 감소 추세를 거친 후, 2026년 초에는 229기의 해상 시추선을 포함해 총 1,058기가 가동되며, 국제적인 시추 활동이 바닥을 쳤습니다. ADNOC Drilling은 2026년 1월, 총액 11억 5,000만 달러 규모의 프리미엄 잭업 리그 2기를 발주하며 이러한 상승 추세를 뒷받침했습니다. 인도 규제 당국은 1,000억 달러 규모의 업스트림 부문 목표를 제시했으며, 여기에는 40개의 심해 탐사정이 포함되어 있으며, 각 탐사정에는 전용 드릴 칼라 스트링이 필요합니다. 가동을 재개한 8세대 드릴십은 연료 소비를 최대 30% 절감하는 하이브리드 동력 시스템을 채택하고 있지만, 이 선박들이 작업 대상으로 하는 더 깊은 유정에서는 수심 2,000미터에서 비트에 가해지는 하중(웨이트 온 비트)을 확보하기 위해 더 무거운 칼라가 필요합니다. 그 결과, 수요는 대량이지만 사양이 낮은 교체에서 소량이지만 사양이 높은 업그레이드로 전환되고 있습니다.

심해·초심해 시추 프로젝트의 확대

페트로브라스는 2025년 초 SEAP I 및 SEAP II를 승인하고, 수심 2,000미터를 초과하는 저류층에 위치한 32개의 유정에 120억 달러 이상을 배정했습니다. 이 우물들은 15,000 psi를 초과하는 압력이 가해지기 때문에 4330V 또는 14Cr-MoV 재질의 칼라가 필수입니다. 비콘 오프쇼어 에너지(Beacon Offshore Energy)사의 셰넌도 유전은 20,000 psi 이하의 조건에서 일일 생산량 10만 배럴을 넘어섬으로써, 극한 환경으로의 전환을 여실히 보여주었습니다. 에퀴놀사는 북극권의 기온으로 인해 NORSOK 인증이 요구되는 요한 스베르도르프 2단계 사업 등 2026년 프로젝트에 1,400억 노르웨이 크로네(131억 달러)를 배정했습니다. 초심해에서의 경제성은 하루에 100만 달러의 손실을 초래하는 파이프 막힘 사고를 피할 수 있느냐에 달려 있기 때문에 각 운영사들은 높은 항복 강도를 지닌 단조 칼라에 투자하고 이를 실시간 피로 모델과 결합하고 있습니다. 이러한 기술적 장벽이 드릴 칼라 시장을 고품질 금속 소재와 디지털 지원 서비스 쪽으로 이끌고 있습니다.

원유 가격 변동이 E&P의 설비 투자를 억제

미국 에너지정보청(EIA)은 2024년 업스트림 부문의 설비 투자가 14% 감소했고, 상장 생산 기업의 현금 흐름이 9% 감소했다고 지적했으며, 이로 인해 재량적 시추 예산이 압박을 받고 있습니다. 셰브론은 2026년 설비 투자 계획을 180억-190억 달러로 발표했으나, 이 상향 조정은 브렌트유 가격이 배럴당 70달러 이상으로 안정될 것을 전제로 하고 있습니다. 운영사는 단기적인 생산 손실 없이 마무리 작업을 연기하거나 시추 장비를 신속히 가동 중단할 수 있기 때문에 드릴 칼라 수요는 간헐적으로 변동합니다. 이러한 수요 감소는 대개 표준 강재 수주에 가장 먼저 영향을 미치며, 공장의 가동률을 떨어뜨리고 이익률을 압박합니다. 손익분기 가격이 세계 벤치마크 가격 수준에서 형성되고 있는 지역에서는 조달 팀이 고합금강 구매를 미루게 되어, 드릴 칼라 시장의 단위 성장세가 둔화됩니다.

부문별 분석

2025년 판매량의 65.1%를 표준 강재가 차지하고 있으며, 이는 저렴한 비용과 수직 우물에 대한 적합성을 반영한 것입니다. 그러나 비자성 칼라 부문은 연평균 성장률(CAGR) 5.5%로 성장하고 있습니다. 이는 고주파 센서가 투자율 1.01을 초과하는 물체를 감지할 수 없기 때문입니다. 비자성형 드릴 칼라 시장 규모는 해저 심층 및 장거리 횡갱 증가에 따라 2026년부터 2031년까지 확대될 것으로 전망됩니다. 할리버튼의 EarthStar 3DX는 현재 모든 HPHT BHA에 이 금속 재료를 지정하고 있으며, 이는 해당 재료의 프리미엄 가치를 입증하고 있습니다.

각 제조업체들은 이러한 가격 책정 여지를 활용하고 있습니다. 쉐러-브렉만사의 2024년 EBIT 마진은 합금 수요 증가에 힘입어 15.0%에 달했습니다. 수직 깊이가 1,500m를 초과하는 미국의 셰일층에서는 운영사가 재고를 적극적으로 재사용하고 있기 때문에 표준 강재가 여전히 주류를 이루고 있습니다. 그러나 유선 파이프가 육상 작업에도 도입됨에 따라 센서 밀도가 높아지고, 이에 따라 드릴 칼라 시장에서 비자성 제품의 점유율도 상승하고 있습니다.

4145H 개질강은 API 규격 준수 및 균형 잡힌 비용 덕분에 2025년 출하량의 44.9%를 차지했습니다. 비자성 14Cr-MoV 스테인리스 스틸은 CO₂ 및 H₂S에 대한 노출도가 높은 프리솔트층 유정에 주로 사용되며, 연평균 성장률(CAGR) 5.8%를 기록하며 가장 빠르게 성장하고 있는 등급입니다. 이 등급의 드릴 칼라 시장 규모 확대는 미국 멕시코만에서 진행 중인 20,000 psi 프로젝트에서 가장 두드러지게 나타납니다.

4330V는 북극권 및 초심해에서의 용도에서 고강도를 실현하는 중간적인 선택지가 됩니다. Equinor사는 해저 온도가 4℃ 전후로 유지되는 요한 스베르도르프 2단계 프로젝트에서 이 기술을 채택하고 있습니다. Tenaris Dopeless와 같은 고품질 연결 부품은 갈링 위험을 줄이고 재사용 주기를 연장할 뿐만 아니라, 합금 가격 변동으로부터 운영자를 보호합니다.

지역별 분석

북미는 멕시코만 심해 개발 및 미국의 셰일가스 개발 활성화에 힘입어 2025년에는 38.5%의 점유율을 기록했으나, 2026년 4월까지 해당 지역의 시추 장비 수는 548기로 감소했습니다. 셰브론은 여전히 2026년 예산 중 약 70억 달러를 멕시코만 프로젝트에 할당하고 있으며, 이는 비자성 및 HPHT 대응 제품에 대한 수요를 뒷받침하고 있습니다. 캐나다에서는 가동 중인 시추 설비가 고작 54기에 그쳐, 수송 능력의 제약에 직면해 있습니다. 이로 인해 색상 사용은 줄어들고 있지만, 한랭지용 금속 가공 기술에 능한 틈새 시장 공급업체들을 지탱하는 요인이 되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.2%를 기록하며 성장할 것으로 예상되며, 이는 각 지역 중 가장 빠른 성장 속도입니다. 인도 탄화수소 총국은 40기의 심해 탐사정을 포함한 업스트림 사업에 1,000억 달러를 투자하고 있으며, 각 유정에는 전용 드릴 칼라 스트링이 필요합니다. ONGC의 크리슈나 고다바리 시추 프로젝트와 관련된 3억 8,550만 달러 규모의 계약에 따라, 고압·고온(HPHT)용 합금에 대한 조기 발주가 이루어지고 있습니다. CNOOC의 문창 16-2는 리드타임 단축을 위해 국내 제철소에 의존하고 있으며, 이로 인해 지역 내 수요를 뒷받침하고 있습니다.

유럽의 성장은 노르웨이가 주도하고 있습니다. 에퀴놀사의 1,400억 노르웨이 크로네 규모의 2026년 계획에 따르면, 요한 스베르드루프 유전의 생산량을 현재 수준으로 유지하고, 브레다브릭 유전의 생산량을 일일 14만 배럴로 확대할 방침이며, 두 유전 모두 북극권 시추 기준 인증을 받았습니다. 노르웨이의 CO2 가격 급등은 하이브리드 시추 장비의 도입을 촉진하고 있지만, 아이러니하게도 더 깊은 유정을 관리하기 위해서는 강성이 더 높고 무거운 칼라가 필요합니다. 중동 및 아프리카에서는 ADNOC Drilling이 수주한 36억 달러 규모의 프로젝트가 고품질 BHA에 대한 수요가 장기적으로 지속되고 있음을 입증하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the drill collar market size is projected to be USD 1.44 billion in 2025, USD 1.51 billion in 2026, and reach USD 1.91 billion by 2031, growing at a CAGR of 4.81% from 2026 to 2031.

This report is Segmented by Type (Standard Steel Drill Collar, Non-Magnetic Drill Collar), Material Grade (4145H Mod Steel, 4330V Steel, Non-Magnetic 14Cr-MoV Stainless), Deployment (Onshore, Offshore), Application (Land Rigs, HPHT Wells, Directional and Horizontal Drilling), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Drill Collar Market Trends and Insights

Recovery in Global Rig Counts Post 2025

International rig activity found a floor in early 2026 with 1,058 units working, including 229 offshore rigs, after several years of attrition. ADNOC Drilling reinforced the upward trend by ordering two premium jack-ups valued at USD 1.15 billion in January 2026. India's regulator outlined a USD 100 billion upstream target that includes 40 deepwater wildcats, each demanding dedicated drill-collar strings. Reactivated eighth-generation drillships employ hybrid power that cuts fuel use by as much as 30%, yet the deeper wells they target require heavier collars to deliver weight-on-bit at 2,000 m water depth. As a result, demand is migrating from high-volume, low-spec replacements to lower-volume, high-spec upgrades.

Growth of Deep- & Ultra-Deepwater Drilling Projects

Petrobras approved SEAP I and SEAP II in early 2025, earmarking more than USD 12 billion for 32 wells in reservoirs beyond 2,000 m depth, with pressures above 15,000 psi that mandate 4330V or 14Cr-MoV collars. Beacon Offshore Energy's Shenandoah field surpassed 100,000 bpd under 20,000 psi conditions, underscoring the shift toward extreme environments. Equinor allocated NOK 140 billion (USD 13.1 billion) for 2026 projects such as Johan Sverdrup Phase 2, where Arctic temperatures demand NORSOK-certified collars. Ultra-deepwater economics depend on avoiding stuck-pipe events that cost USD 1 million per day, so operators invest in collars forged for high yield strength and paired with real-time fatigue models. These technical thresholds are pushing the drill collar market toward premium metallurgy and digital support services.

Crude-Oil Price Volatility Dampens E&P CAPEX

The U.S. Energy Information Administration noted a 14% decline in upstream capital spending during 2024 and a 9% slide in cash flow among public producers, squeezing discretionary drilling budgets. Chevron disclosed a USD 18-19 billion 2026 capital plan but tied any upside to Brent benchmarks stabilizing above USD 70 per barrel. Operators can quickly defer completions or idle rigs without near-term production loss, causing sporadic demand swings for drill collars. Such pullbacks typically hit standard steel orders first, compressing plant utilization and eroding margins. In regions where breakeven prices hover near global benchmarks, procurement teams delay high-alloy purchases, slowing unit growth in the drill collar market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Directional & Horizontal Drilling

- OEM-Led Collar Weight Optimization to Cut Rig Emissions

- Availability of Substitute Down-Hole Weight Solutions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard steel accounted for 65.1% of 2025 volume, reflecting its low cost and readiness for vertical wells. Non-magnetic collars, however, are expanding at 5.5% CAGR because high-frequency sensors cannot tolerate magnetic permeability above 1.01. The drill collar market size for non-magnetic variants is projected to expand from 2026 through 2031 as subsalt and long-reach laterals proliferate. Halliburton's EarthStar 3DX now specifies this metallurgy on every HPHT BHA, validating the premium.

Manufacturers exploit the pricing headroom: Schoeller-Bleckmann's 2024 EBIT margin reached 15.0% on stronger alloy demand. Standard steel continues to dominate U.S. shale where vertical sections exceed 1,500 m and operators recycle inventory aggressively. Yet as wired pipe migrates into land operations, sensor density rises and the non-magnetic share of the drill collar market rises alongside.

4145H modified steel secured 44.9% of 2025 shipments thanks to its API acceptance and balanced cost. Non-magnetic 14Cr-MoV stainless is the fastest-growing grade at 5.8% CAGR, supported by pre-salt wells with high CO2 and H2S exposure. Drill collar market size growth in this grade is most noticeable in the U.S. Gulf of Mexico's 20,000 psi projects.

4330V provides a higher-strength middle ground for Arctic and ultra-deepwater applications. Equinor employs it in Johan Sverdrup Phase 2 where seabed temperatures hover near 4 °C. Premium connections such as Tenaris Dopeless reduce galling risk, extending reuse cycles and shielding operators from volatile alloy prices.

Geography Analysis

North America commanded 38.5% share in 2025 on the back of Gulf of Mexico deepwater and U.S. shale intensity, though regional rig counts slipped to 548 units by April 2026. Chevron still directs roughly USD 7 billion of its 2026 budget to Gulf projects, maintaining a floor for non-magnetic and HPHT-rated demand. Canada's modest 54 working rigs grapple with takeaway constraints, tempering collar consumption but supporting niche suppliers skilled in cold-weather metallurgy.

Asia-Pacific is forecast to grow at 6.2% CAGR through 2031, the fastest pace among regions. India's Directorate General of Hydrocarbons is steering USD 100 billion toward upstream work that includes 40 deepwater wildcats, each requiring dedicated drill-collar strings. ONGC's USD 385.5 million contract for Krishna-Godavari drilling places early orders for HPHT-ready alloys. CNOOC's Wenchang 16-2 adds regional pull, relying on domestic mills for shorter lead times.

Europe growth is anchored by Norway. Equinor's NOK 140 billion 2026 plan keeps Johan Sverdrup on plateau and moves Breidablikk toward 140,000 bpd, both certified under Arctic drilling codes. Norway's sharp CO2 price encourages hybrid rigs that paradoxically need stiffer, heavier collars to manage deeper wells. In the Middle East and Africa, ADNOC Drilling's USD 3.6 billion award slate confirms prolonged appetite for premium BHAs.

- Hunting plc

- SLB N.V.

- NOV Inc.

- SBO AG

- China Vigor Drilling Oil Tools and Equipment Co., Ltd.

- International Drilling Services Ltd. (IDS)

- Zhong Yuan Special Steel Co., Ltd.

- American Oilfield Tools, Inc.

- Workstrings International Ltd.

- Texas Steel Conversion, Inc.

- Challenger International, Inc.

- Vallourec S.A.

- Weatherford International plc

- Tenaris S.A.

- Jiangsu Shuguang Huayang Drilling Tool Co., Ltd.

- Superior Drillpipe Manufacturing, Inc.

- Tejas Tubular Products, Inc.

- Drill Collars & Drill Pipe, Inc.

- Ramco Tubular Services, Inc.

- Drill Collar USA, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Recovery in global rig counts post-2025

- 4.2.2 Growth of deep- & ultra-deep-water drilling projects

- 4.2.3 Rapid adoption of directional & horizontal drilling

- 4.2.4 OEM-led collar weight optimisation to cut rig emissions

- 4.2.5 Surging demand for non-magnetic collars for high-freq MWD/LWD

- 4.2.6 Digital-twin based fatigue-life prediction extends service life

- 4.3 Market Restraints

- 4.3.1 Crude-oil price volatility dampens E&P CAPEX

- 4.3.2 Availability of substitute down-hole weight solutions

- 4.3.3 Supply crunch in low-permeability non-magnetic alloys

- 4.3.4 Stricter drilling-waste regulations shortening collar cycles

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Standard Steel Drill Collar

- 5.1.2 Non-magnetic Drill Collar

- 5.2 By Material Grade

- 5.2.1 4145H Mod Steel

- 5.2.2 4330V Steel

- 5.2.3 Non-magnetic 14Cr-MoV Stainless

- 5.3 By Deployment

- 5.3.1 Onshore

- 5.3.2 Offshore

- 5.4 By Application

- 5.4.1 Land Rigs

- 5.4.2 High-Pressure High-Temperature (HPHT) Wells

- 5.4.3 Directional and Horizontal Drilling

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Norway

- 5.5.2.2 United Kingdom

- 5.5.2.3 Russia

- 5.5.2.4 Netherlands

- 5.5.2.5 Germany

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Iran

- 5.5.5.4 Nigeria

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Hunting plc

- 6.4.2 SLB N.V.

- 6.4.3 NOV Inc.

- 6.4.4 SBO AG

- 6.4.5 China Vigor Drilling Oil Tools and Equipment Co., Ltd.

- 6.4.6 International Drilling Services Ltd. (IDS)

- 6.4.7 Zhong Yuan Special Steel Co., Ltd.

- 6.4.8 American Oilfield Tools, Inc.

- 6.4.9 Workstrings International Ltd.

- 6.4.10 Texas Steel Conversion, Inc.

- 6.4.11 Challenger International, Inc.

- 6.4.12 Vallourec S.A.

- 6.4.13 Weatherford International plc

- 6.4.14 Tenaris S.A.

- 6.4.15 Jiangsu Shuguang Huayang Drilling Tool Co., Ltd.

- 6.4.16 Superior Drillpipe Manufacturing, Inc.

- 6.4.17 Tejas Tubular Products, Inc.

- 6.4.18 Drill Collars & Drill Pipe, Inc.

- 6.4.19 Ramco Tubular Services, Inc.

- 6.4.20 Drill Collar USA, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment