|

시장보고서

상품코드

2063902

유전체학 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Genomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

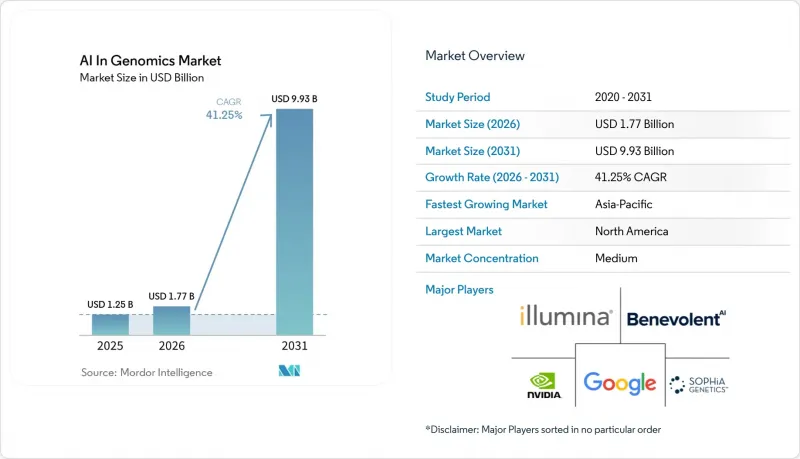

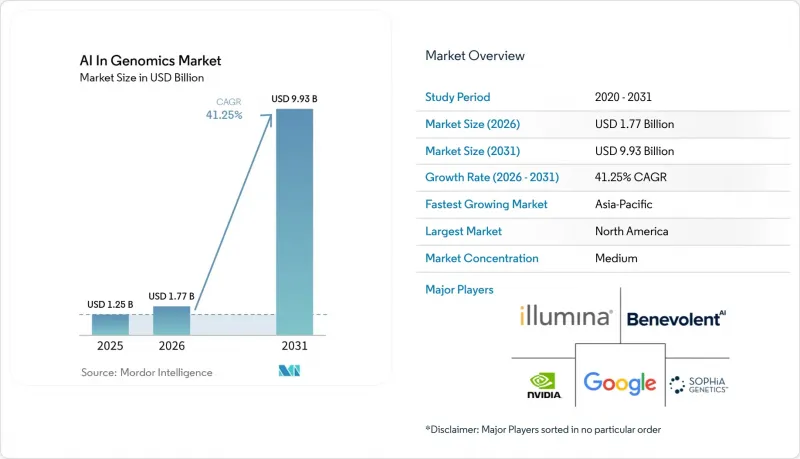

Mordor Intelligence에 의하면, 유전체학 AI 시장 규모는 2025년에 12억 5,000만 달러로 평가되었고, 2026년 17억 7,000만 달러로 추정되고, 2031년까지 99억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 41.25%를 나타낼 전망입니다.

본 보고서는 구성 요소별(소프트웨어, 서비스, 하드웨어), 기술별(머신러닝, 딥러닝, 기타), 기능별(유전체 시퀀싱, 유전자 편집, 기타), 용도별(신약 및 의약품 개발, 정밀의료, 기타), 도입 모델별(클라우드 기반, 기타), 최종 사용자별(제약 및 바이오기술 기업, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 유전체학 AI 시장 동향 및 인사이트

수동 분석을 능가하는 유전체 데이터의 폭발적인 증가

단일 전체 유전체 염기서열 분석에서 200GB에서 300GB의 원시 데이터가 생성되며, 현재 전 세계적으로 연간 생성되는 유전체 데이터의 양은 수십 엑사바이트에 달할 전망입니다. 이 데이터 양은 수작업으로 분석하는 팀이 검토할 수 있는 속도를 능가하는 속도로 증가하고 있기 때문에 유전체학 AI 시장은 단순한 데이터 생성뿐만 아니라 해석 속도와도 점점 더 밀접한 관련을 맺고 있습니다. 이러한 변화는 알고리즘과 대규모로 라벨링되고 임상적으로 검증된 변이 라이브러리를 결합한 공급업체에게도 유리하게 작용합니다. 왜냐하면 처리 능력이 제약 요인이 될 경우, 모델 설계와 마찬가지로 큐레이션의 품질도 중요해지기 때문입니다. 2025년 9월 SeqOne이 Congenica를 인수한 것은 이러한 논리를 반영한 것이었습니다. 통합된 플랫폼을 통해 AI 시퀀싱 분석과 웰컴-샌거 생태계에서 비롯된 임상 판단 라이브러리가 융합되었습니다. 통합된 사업체는 2025년에 20만 건 이상의 환자 유전체 분석을 처리했습니다. 이는 2024년 대비 3배 증가한 수치로, 대규모 해석 플랫폼이 얼마나 빠르게 일상적인 사용으로 자리 잡고 있는지를 보여줍니다. 실용적인 관점에서 볼 때, 유전체학 시장에서 AI는 현재 개별 모델의 성능을 강조하기보다는 데이터 큐레이션의 깊이, 사례 수, 워크플로우 자동화를 더욱 중시하는 추세입니다.

종양학과 희귀질환 분야에서 정밀의학의 확대

유전체학 AI 시장에서는 정밀 의학 분야 수요가 증가하고 있으며, 특히 종양학 및 희귀질환 프로그램이 현재 동일한 해석 스택에 의존하고 있는 부문에서 이러한 현상이 두드러집니다. 『Clinical and Experimental Medicine』 저널에 실린 2025년 연구에 따르면, 조직병리학과 유전체학을 결합한 자율형 AI 에이전트는 면역요법 선택에 있어 중요한 바이오마커인 미세위성 불안정성(MSI) 진단에서 91%의 정확도를 달성했습니다. 이 결과는 단순히 독립적인 의사결정 도구가 아니라, 조직·분자·임상 데이터에 걸쳐 있는 통합 모델의 활용을 뒷받침하는 것으로, 중요한 의미를 지닙니다. 희귀질환 부문에서는 GeneDx가 2025년 잠정 매출액으로 전년 대비 41% 증가한 4억 2,700만 달러를 기록했다고 보고했습니다. 한편, 주 정부가 지원하는 프로그램을 통해 신생아 유전체 선별 검사가 확대됨에 따라 엑솜 및 유전체 관련 매출이 54% 증가했습니다. 이 두 가지 케어 패스는 더 이상 고립되어 발전하는 것이 아니며, 이것이 유전체 AI 시장의 잠재적 수요 기반을 확대되고 있습니다. 종양학 분야에서 치료법 매칭을 뒷받침하는 것과 동일한 운영 모델이 소아 질환 및 유전성 질환의 신속한 진단도 뒷받침할 수 있습니다.

데이터 개인정보 보호 및 임상 AI의 규정 준수 부담

유전체학 AI 시장은 유럽에서 실질적인 규제상의 장벽에 직면해 있습니다. EU의 AI 법에 따르면, 상위 등급의 유전체 IVD 시스템이 고위험 AI 시스템으로 분류되기 때문입니다. 이 체계에서는 위험 관리, 기술 문서, 인적 감독, 사이버 보안 대책이 요구되며, 고위험 시스템에 대한 완전한 규정은 2027년 8월부터 시행됩니다. 모델을 지속적으로 업데이트하는 공급업체의 경우, 부담이 더욱 커집니다. 왜냐하면 문서화는 플랫폼 전체를 한 번에 포괄하는 것이 아니라, 중요한 모델 변경 사항을 추적해야 하기 때문입니다. 2025년에 발표된 프랑스의 인공지능 및 건강 데이터에 관한 국가 전략 역시, 도입을 2차 이용에 대한 거버넌스 및 상호 운용 가능한 건강 데이터 규정과 더욱 밀접하게 연계하고 있습니다. 이러한 규정은 하이브리드형 및 로컬 제어형 아키텍처를 권장하고 있으며, 유전체학 AI 시장에 진출한 중소기업들에게는 비용 증가와 규모 확대 지연으로 이어집니다. 따라서 컴플라이언스는 시장의 선별 요인으로 작용하고 있지만, 이는 기술이 미숙하기 때문이 아니라 상용화에 따른 문서화 부담이 증가하고 있기 때문입니다.

부문별 분석

2025년, 소프트웨어는 매출의 42.1%를 차지했으며, 유전체학 AI 시장에서 가장 큰 비중을 차지하는 부문이 되었습니다. 이 부문에는 변이 해석 플랫폼, 생물정보학 파이프라인, 임상 의사결정 지원 도구, 유전체 기반 모델 API가 포함됩니다. 이러한 주도적인 위상은 밸류 스택이 하드웨어에서 지속적인 계약을 통해 판매 가능한 해석 계층으로 전환되고 있음을 보여줍니다. 따라서, 유전체학 AI 시장에서는 분석 로직을 지속적인 수익원으로 전환하는 클라우드 네이티브 소프트웨어 모델이 높이 평가받고 있습니다. QIAGEN이 2025년 5월 7,000만-8,000만 달러에 Genoox를 인수한 것은 Franklin AI 클라우드 플랫폼을 자사의 Digital Insights 포트폴리오에 추가함으로써 이러한 방향성을 뒷받침하는 것이었습니다. Franklin은 인수 당시 50개국 이상의 4,000여 개 의료 기관에서 활용되고 있었으며, 75만 건 이상의 사례 해석을 지원해 왔습니다.

서비스 부문은 가장 빠르게 성장하고 있는 부문으로, 2026-2031년 연평균 성장률(CAGR) 42.87%를 나타낼 것으로 전망됩니다. 이러한 추세는 AI 도구가 규제 환경에 도입된 후, 구현, 검증 및 지속적인 모델 유지 관리가 얼마나 중요한지를 반영하고 있습니다. 유전체학 AI 시장은 실험실 및 의료 시스템의 통합, 감사 추적, 도입 후 튜닝과 관련된 지원이 빈번히 필요하기 때문에 전문 서비스에 대한 의존도가 높아지고 있습니다. 하드웨어는 여전히 성장 속도가 가장 느린 부문이지만, 연산 성능이 처리 시간을 좌우하는 처리량 중심의 워크플로우에서는 여전히 중요합니다. NVIDIA는 2025년 3월, Parabricks v4.5가 4개의 GPU를 사용하여 전체 유전체 생식세포 계통 분석을 8분 이내로 단축하고, Blackwell 아키텍처에 대한 지원을 추가했다고 발표했습니다. 이는 연구실이 긴 연산으로 인한 병목 현상 없이 대규모 데이터 처리를 수행할 수 있을 때 소프트웨어의 효과가 가장 잘 발휘되기 때문에 중요한 의미를 지닙니다. 앞으로 유전체학 산업의 AI 부문에서는 소프트웨어, 도입 서비스, 하드웨어 가속화를 단일 운영 모델로 통합한 엔드투엔드 계약이 증가할 것으로 전망됩니다. 이러한 번들 계약은 전환 비용을 높이며, 고객 생애 가치를 초기 소프트웨어 구독 기간을 훨씬 넘어 확장시킬 가능성이 있습니다.

2025년에는 머신러닝이 매출의 63.18%를 차지했으며, 유전체학 AI 시장에서 중심적인 위치를 유지했습니다. 머신러닝은 변이 효과 예측, 다유전자 위험도 평가, 바이오마커 분류, 조사 및 임상 활용 분야의 기타 주요 과제를 뒷받침하고 있습니다. 그라디언트 부스팅이나 랜덤 포레스트와 같은 고전적인 기법은 여전히 소규모의 저차원 임상 데이터셋에 적합합니다. 딥러닝은 워크플로우에 대규모 멀티오믹스 입력이나 고차원 특징량 융합이 포함될 때 더욱 유용합니다. 『Clinical and Experimental Medicine』 저널에 실린 체계적 문헌고찰에 따르면, 그래프 신경망과 어텐션 기반 모델이 멀티오믹스 종양학 분야에서 뛰어난 성능을 보인 것으로 보고되었습니다. 이러한 조합은 유전체학 AI 시장이 단일 모델 아키텍처로 향하고 있는 것이 아니라, 신구 기법이 공존하는 계층적인 툴킷으로 나아가고 있음을 의미합니다.

자연어 처리는 가장 빠르게 성장하고 있는 기술로, 2031년의 연평균 성장률(CAGR)은 43.18%로 예측됩니다. 이러한 성장은 임상 기록, 과학 문헌, 변이 데이터베이스를 동일한 워크플로우 내에서 분석할 수 있는 기반 모델 아키텍처 덕분입니다. Tempus One은 2025년 1월, 환자 타임라인 통합, 사전 승인 지원, 대량의 비정형 문서에 대한 쿼리 검색을 지원하는 GenAI 기능을 추가했습니다. 유전체학 AI 시장에서 이에 따라 NLP는 단순한 배경 정보 보완의 역할에서 벗어나 주요 임상 인터페이스 계층으로 전환되고 있습니다. 또한 컴퓨터 비전은 공간적 멀티오믹스 및 디지털 병리학의 워크플로우에서 특히 이미지 데이터와 분자 데이터를 함께 분석해야 하는 상황에서 여전히 중요한 역할을 수행하고 있습니다. 설계 과제를 위한 강화 학습이나 불확실성 처리를 위한 베이즈 기법 등, 그 밖의 기법들은 여전히 구성 요소의 일부에 불과하지만, 유전체학 AI 시장 기술 기반을 지속적으로 확대되고 있습니다.

지역별 분석

북미는 2025년에 38.52%의 점유율을 차지했으며, 지역별 최대 점유율을 유지했습니다. 이는 시퀀싱 역량, 상용 AI 유전체학 플랫폼, 첨단 진단법에 대한 조기 보험 급여 확대와 같은 성숙한 기반을 반영한 것입니다. Tempus AI는 2026년 1분기 매출이 전년 동기 대비 36.1% 증가한 3억 4,810만 달러를 기록했다고 보고했습니다. 유전성 질환 검사 건수는 54% 증가했으며, 미세잔존병변(MRD) 검사 건수는 500% 이상 증가했습니다. 이러한 성과는 북미 유전체학 AI 시장이 전문적인 종양학 영역에서 보다 광범위한 임상 용도로 전환되고 있음을 보여줍니다. 미국은 여전히 상업 활동의 중심지이지만, 캐나다는 2025년 9월, 국가 유전체 전략과 정밀의료 이니셔티브를 통해 독자적인 유전체 데이터와 AI 인프라를 구축할 의향을 밝혔습니다.

유럽은 긴밀한 임상 유전체 네트워크와 전 세계 제품 설계에 점점 더 큰 영향을 미치는 규제 체계를 모두 갖추고 있어, 유전체학 AI 시장에 계속해서 주요한 기여 요인으로 자리 잡고 있습니다. EU AI법은 공급업체들이 검증되고 감사 가능한 시스템으로 전환하도록 장려하고 있으며, 이는 모델의 동작 및 워크플로우 관리를 상세하게 문서화할 수 있는 플랫폼에 유리하게 작용하고 있습니다. 영국의 ‘Cancer 2.0’ 프로그램과 지역 차원의 광범위한 임상 도입 활동은 유럽이 AI 유전체 도구를 규제할 뿐만 아니라 그 활용 사례를 확대하고 있음을 보여줍니다. 2026년 3월 보고서에 따르면, 이 회사는 2025년 말 기준으로 90개국 이상에 528개의 주요 유전체 고객을 보유하고 있으며, 여기에는 에든버러 왕립병원, 벨기에의 AZ Delta, 독일의 루르 대학교 보훔과의 신규 계약이 포함됩니다. 프랑스의 ‘인공지능 및 건강 데이터에 관한 2025년 전략’ 역시 대규모 상호운용 가능한 유전체 데이터 시스템 구축을 위한 구체적인 정책 추진 방안을 제시하고 있습니다.

아시아태평양은 유전체학 AI 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 42.81%를 나타낼 것으로 전망됩니다. 이 분야의 전망은 각국의 유전체 프로그램, AI 기반 진단 인프라의 광범위한 구축, 서로 다른 조상 집단 간 성능을 향상시키는 지역 데이터 자원에 대한 수요 증가에 힘입어 밝습니다. 아시아태평양의 유전체학 분야 AI 시장은 기존 도입 기반이 작다는 단순한 사실만으로도 신규 용량이 추가되고 있는 혜택을 누리고 있으며, 이것이 성숙한 지역보다 더 빠른 성장을 뒷받침하고 있습니다. 호주와 한국은 국가 유전체 이니셔티브 및 병원 연계 시퀀싱 프로그램을 통해 지속적으로 입지를 강화하고 있는 반면, 동 지역의 다른 시장에서는 임상 및 중개 연구 역량 구축이 진행되고 있습니다.

중동 및 아프리카와 남미는 현재 수익 규모 면에서는 여전히 작지만, 모두 도입의 초기 상업 단계로 한 걸음 더 나아가고 있습니다. 2026년 3월 보고서에 따르면, 사우디아라비아의 킹 압둘라 국제의료센터에서 액체 생검을 도입한 사례와 브라질의 인간 유전체·줄기세포 연구센터에서 플랫폼을 활용한 사례는 주요 확립된 지역 이외의 곳에서도 그 활용이 확대되고 있음을 보여줍니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the aI in genomics market size was valued at USD 1.25 billion in 2025 and is estimated to grow from USD 1.77 billion in 2026 to reach USD 9.93 billion by 2031, at a CAGR of 41.25% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Services, Hardware), Technology (Machine Learning, Deep Learning, and More), Functionality (Genome Sequencing, Gene Editing, and More), Application (Drug Discovery & Development, Precision Medicine, and More), Deployment Model (Cloud-Based, and More), End User (Pharma & Biotech, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global AI In Genomics Market Trends and Insights

Genomic Data Explosion Outpacing Manual Interpretation

A single whole-genome sequence can generate 200 GB to 300 GB of raw data, and annual genomic data output now runs into tens of exabytes globally. That data load is growing faster than manual analyst teams can review it, so the AI in genomics market is increasingly tied to interpretation speed rather than to data generation alone. This shift also favors vendors that combine algorithms with large, labeled, clinically validated variant libraries, because curation quality matters as much as model design once throughput becomes the constraint. SeqOne's acquisition of Congenica in September 2025 reflected that logic, as the combined platform brought AI sequencing analytics together with a clinical decision library derived from the Wellcome Sanger ecosystem. The combined operation processed more than 200,000 patient genomic analyses in 2025, which was a 3-fold increase over 2024 and shows how fast scaled interpretation platforms are moving into routine use. In practical terms, the AI in genomics market now rewards data curation depth, case volume, and workflow automation more than stand-alone model claims.

Precision Medicine Scaling Across Oncology and Rare Disease

The AI in genomics market is seeing stronger demand from precision medicine, especially where oncology and rare disease programs now rely on the same interpretation stack. A 2025 study in Clinical and Experimental Medicine found that an autonomous AI agent that combined histopathology and genomics reached 91% accuracy for microsatellite instability diagnosis, which is a key biomarker for immunotherapy selection. That result matters because it supports the use of unified models across tissue, molecular, and clinical data rather than isolated decision tools. In rare disease, GeneDx reported preliminary 2025 revenue of USD 427 million, up 41% year over year, while exome and genome revenue grew 54% as genomic newborn screening expanded through state-backed programs. Those two care pathways are no longer developing in isolation, and that is widening the addressable demand base for the AI in genomics market. The same operating model that supports therapy matching in oncology can also support fast diagnosis in pediatric and inherited disorders.

Data Privacy And Clinical AI Compliance Burden

The AI in genomics market faces a real regulatory barrier in Europe, where the EU AI Act treats genomic IVD systems in higher classes as high-risk AI systems. That framework requires risk management, technical documentation, human oversight, and cybersecurity controls, and full provisions for high-risk systems take effect from August 2027. The burden is heavier for vendors that update models continuously, because documentation must track material model changes rather than cover the entire platform once. France's national strategy for artificial intelligence and health data, published in 2025, also ties deployment more closely to secondary-use governance and interoperable health data rules. Those rules favor hybrid and locally controlled architectures, which adds cost and slows scale for smaller companies in the AI in genomics market. Compliance therefore acts as a market filter, not because the technology is weak, but because commercialization is becoming more documentation-heavy.

Other drivers and restraints analyzed in the detailed report include:

- AI-Led Drug Discovery Shortening Hypothesis Cycles

- Falling Sequencing Costs Widening Multi-Omic Adoption

- Scarcity of AI-Genomics Talent and Curated Labels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 42.1% of revenue in 2025, which made it the largest component in the AI in genomics market. The segment covers variant interpretation platforms, bioinformatics pipelines, clinical decision-support tools, and genomic foundation model APIs. Its lead position shows that the value stack is moving away from instruments and toward interpretation layers that can be sold on recurring terms. The AI in genomics market is therefore rewarding cloud-native software models that turn analytic logic into a repeatable revenue stream. QIAGEN's May 2025 acquisition of Genoox, valued at USD 70 million to USD 80 million, confirmed this direction by adding the Franklin AI cloud platform to its Digital Insights portfolio. Franklin was active in more than 4,000 healthcare organizations across 50 countries and had supported more than 750,000 case interpretations at the time of the deal.

Services is the fastest-growing component, with a projected CAGR of 42.87% from 2026 to 2031. That pace reflects how much implementation, validation, and ongoing model maintenance matter once AI tools enter regulated environments. The AI in genomics market increasingly depends on professional services because laboratories and health systems often need support for integration, audit trails, and post-deployment tuning. Hardware remains the slowest-growing component, but it still matters in throughput-heavy workflows where compute performance shapes turnaround time. NVIDIA stated in March 2025 that Parabricks v4.5 reduced whole-genome germline analysis to under 8 minutes using 4 GPUs and added support for Blackwell architecture. That matters because software gains are strongest when labs can also process data at scale without long compute bottlenecks. Over time, the AI in genomics industry is likely to see more end-to-end contracts that bundle software, implementation services, and hardware acceleration into a single operating model. Those bundled deals raise switching costs and can stretch customer lifetime value well beyond an initial software subscription.

Machine learning held 63.18% of revenue in 2025, which kept it at the center of the AI in genomics market. Machine learning supports variant-effect prediction, polygenic risk scoring, biomarker classification, and other core tasks across research and clinical use. Classical methods such as gradient boosting and random forests still fit smaller and lower-dimensional clinical datasets well. Deep learning is more useful when the workflow involves large multi-omic inputs and higher-dimensional feature fusion. A systematic review in Clinical and Experimental Medicine reported that graph neural networks and attention-based models delivered strong performance in multi-omic oncology settings. That mix means the AI in genomics market is not moving toward a single model architecture, but toward a layered toolkit where older and newer methods coexist.

Natural language processing is the fastest-growing technology, with a projected CAGR of 43.18% through 2031. That growth comes from foundation model architectures that can read clinical notes, scientific literature, and variant databases in the same workflow. Tempus One added GenAI capabilities in January 2025 that supported patient timeline synthesis, prior authorization assistance, and querying across large volumes of unstructured documents. In the AI in genomics market, this moves NLP from a background enrichment role into the main clinical interface layer. Computer vision also retains a meaningful role in spatial multi-omic and digital pathology workflows, especially where image and molecular data need to be read together. Other methods, including reinforcement learning for design tasks and Bayesian methods for uncertainty handling, are still smaller parts of the mix but continue to widen the technical base of the AI in genomics market.

Geography Analysis

North America held the largest regional position, with 38.52% share in 2025, and that reflects a mature base of sequencing capacity, commercial AI genomics platforms, and earlier reimbursement traction for advanced diagnostics. Tempus AI reported Q1 2026 revenue of USD 348.1 million, up 36.1% year over year, with hereditary testing volume growth of 54% and minimal residual disease test volume growth of more than 500%. Those operating figures show how the AI in genomics market is moving from specialist oncology settings toward broader clinical use in North America. The United States remains the regional center of commercial activity, while Canada signaled its intention in September 2025 to build sovereign genomic data and AI infrastructure through a national genomics strategy and precision health initiative.

Europe remains a major contributor to the AI in genomics market because it combines dense clinical genomics networks with a regulatory framework that increasingly shapes global product design. The EU AI Act is pushing vendors toward validated and auditable systems, and that favors platforms that can document model behavior and workflow controls in detail. The UK Cancer 2.0 program and wider clinical deployment activity across the region show that Europe is not only regulating AI genomics tools, but also expanding the use cases for them. reported in March 2026 that it ended 2025 with 528 core genomics customers across more than 90 countries, including new signings at the Royal Infirmary of Edinburgh, AZ Delta in Belgium, and Ruhr University Bochum in Germany. France's 2025 strategy for artificial intelligence and health data also shows a clear policy push toward interoperable genomic data systems at scale.

Asia-Pacific is the fastest-growing region in the AI in genomics market, with a projected CAGR of 42.81% through 2031. The regional outlook is supported by national genome programs, a broader build-out of AI-native diagnostic infrastructure, and a rising need for local data resources that improve cross-ancestry performance. The AI in genomics market in Asia-Pacific also benefits from the simple fact that new capacity is being added from a lower installed base, which supports faster expansion than in mature regions. Australia and South Korea continue to add weight through national genome initiatives and hospital-linked sequencing programs, while other markets in the region are building out clinical and translational capacity.

Middle East and Africa and South America remain smaller in current revenue terms, but both are moving further into the early commercial phase of adoption. stated in March 2026 that liquid biopsy adoption at King Abdullah International Medical Center in Saudi Arabia and platform use at Brazil's Human Genome and Stem Cell Research Center show that deployment is broadening outside the main established regions.

- Benevolent AI

- Complete Genomics

- Congenica

- Deep Genomics

- DNAnexus

- Fabric Genomics

- Freenome

- GeneDx

- Genomenon

- Genoox

- Illumina

- Lifebit

- NVIDIA

- Oxford Nanopore Technologies

- QIAGEN

- SeqOne

- SOPHiA GENETICS

- Tempus AI

- Velsera

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Genomic Data Explosion Outpacing Manual Interpretation

- 4.2.2 Precision Medicine Scaling Across Oncology and Rare Disease

- 4.2.3 AI-Led Drug Discovery Shortening Hypothesis Cycles

- 4.2.4 Falling Sequencing Costs Widening Multi-Omic Adoption

- 4.2.5 Noncoding Variant Interpretation Lifting Diagnostic Yield

- 4.2.6 Genomic Foundation Models Improving Multi-Task Inference

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Clinical AI Compliance Burden

- 4.3.2 Scarcity of AI-Genomics Talent and Curated Labels

- 4.3.3 Eurocentric Training Data Limiting Cross-Ancestry Accuracy

- 4.3.4 Data Sovereignty and Compute Cost Inflation Slowing Scale

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.2 By Technology

- 5.2.1 Machine Learning

- 5.2.2 Deep Learning

- 5.2.3 Natural Language Processing

- 5.2.4 Computer Vision

- 5.2.5 Other AI Technologies

- 5.3 By Functionality

- 5.3.1 Genome Sequencing

- 5.3.2 Gene Editing

- 5.3.3 Clinical Workflow

- 5.3.4 Predictive Genetic Testing

- 5.3.5 Other Functionalities

- 5.4 By Application

- 5.4.1 Drug Discovery & Development

- 5.4.2 Precision Medicine

- 5.4.3 Clinical Diagnostics

- 5.4.4 Agriculture & Animal Research

- 5.4.5 Other Applications

- 5.5 By Deployment Model

- 5.5.1 Cloud-Based

- 5.5.2 On-Premise

- 5.5.3 Hybrid

- 5.6 By End User

- 5.6.1 Pharmaceutical & Biotechnology Companies

- 5.6.2 Healthcare Providers

- 5.6.3 Clinical Laboratories & Diagnostic Centers

- 5.6.4 Academic & Research Institutes

- 5.6.5 Other End Users

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 BenevolentAI

- 6.3.2 Complete Genomics

- 6.3.3 Congenica

- 6.3.4 Deep Genomics

- 6.3.5 DNAnexus

- 6.3.6 Fabric Genomics

- 6.3.7 Freenome

- 6.3.8 GeneDx

- 6.3.9 Genomenon

- 6.3.10 Genoox

- 6.3.11 Google

- 6.3.12 Illumina, Inc.

- 6.3.13 Lifebit

- 6.3.14 NVIDIA

- 6.3.15 Oxford Nanopore Technologies

- 6.3.16 QIAGEN

- 6.3.17 SeqOne

- 6.3.18 SOPHiA GENETICS

- 6.3.19 Tempus AI

- 6.3.20 Velsera

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment