|

시장보고서

상품코드

2063904

마이크로러닝 플랫폼 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Microlearning Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

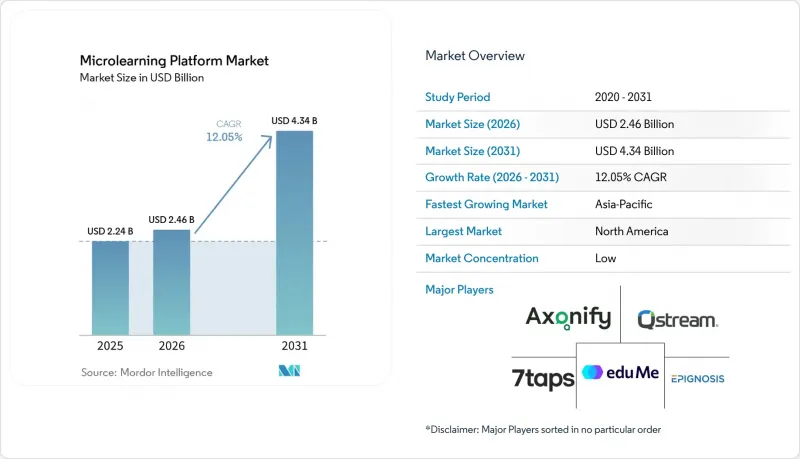

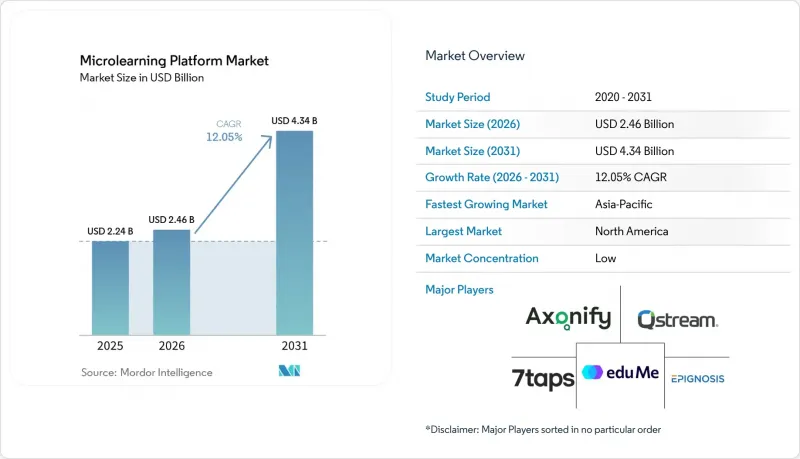

Mordor Intelligence에 의하면, 마이크로러닝 플랫폼 시장 규모는 2025년 22억 4,000만 달러, 2026년 24억 6,000만 달러에서 2031년까지 43억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 12.05%를 나타낼 것으로 예측됩니다.

본 보고서는 플랫폼 유형(독립형 마이크로러닝 플랫폼 등), 도입 모델(클라우드 등), 기업 규모(대기업, 중소기업), 용도(규정 준수 교육, 직원의 역량 강화 및 재교육 등), 업종(은행/금융서비스/보험 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 마이크로러닝 플랫폼 시장 동향과 인사이트

직원들의 지속적인 역량 강화 및 재교육에 대한 수요 증가

마이크로러닝 플랫폼 시장은 현재 직원들의 역량과 디지털 도구, 자동화, 그리고 직무 설계의 변화 속도 사이에 뚜렷한 불일치가 존재하기 때문에 성장세를 보이고 있습니다. 『The Future of Jobs 2025』 보고서에 따르면, 근로자의 핵심 역량의 39%가 5년 이내에 갱신되어야할 것으로 예상되며, 이에 따라 민간 및 공공 기관을 막론하고 지속적인 학습이 고용주의 최우선 과제로 자리 잡고 있습니다. 이러한 압박감으로 인해, 긴 연수 형식보다 신속하게 업데이트할 수 있고 더 자주 할당되는 단시간 학습 과정이 유리해지고 있습니다. 또한, AI를 활용한 컨텐츠 제작을 통해 새로운 모듈을 만드는 데 필요한 시간과 노력이 절감됨에 따라, 마이크로러닝 플랫폼 시장의 비즈니스 타당성도 강화되고 있습니다. 스킬 재습득 주기가 단축됨에 따라, 컨텐츠의 신속한 업데이트와 워크플로우 기반의 배포를 지원하는 벤더는 역할 요건이 변화하는 대규모 조직에 대응하는 데 유리한 입장에 있습니다. 이것이 바로 마이크로러닝 플랫폼 시장이 단순한 정기 교육에 그치지 않고, 일상적인 생산성 인프라로 자리매김해 가고 있는 이유입니다.

데스크가 없는 환경 및 분산 근무 직원을 대상으로 한 모바일 우선 학습에 대한 수요

마이크로러닝 플랫폼 시장은 업무 중 데스크톱 시스템을 사용하지 않는 데스크리스 및 분산형 직원들의 학습 수요에 힘입어 성장하고 있습니다. 모바일 우선 방식의 컨텐츠 제공은 근무 시간 중, 업무 틈새, 또는 통신 환경이 불안정한 상황에서 직원들에게 교육을 제공해야 하는 소매, 창고, 현장 서비스, 외식 산업, 의료 현장에 적합합니다. 모바일 앱이나 텍스트 형식을 통해 제공되는 짧은 모듈은 기술이 필요한 시점과 그 기술이 체화되는 시점 사이의 간극을 좁혀줍니다. Qstream은 2026년 1월, 통신 환경이 불안정한 곳에서 근무하는 제약업계 현장 영업팀을 대상으로 SMS를 활용한 마이크로러닝 제공을 시작했습니다. 이는 각 벤더사가 업무의 현실에 맞추어 형식을 조정하고 있음을 보여줍니다. Bites Learning과 EZShift는 2026년 5월, 교대 근무 인계 워크플로우에 교육을 통합하기 위한 제휴를 발표했습니다. 이는 업무 시스템의 외부가 아닌, 시스템 내부에서의 학습으로 향하는 보다 광범위한 변화를 시사하고 있습니다. 따라서 마이크로러닝 플랫폼 시장은 모바일 접근성뿐만 아니라, 학습 기회와 업무 수행 간의 긴밀한 연계로부터도 혜택을 받고 있습니다.

심층적인 개념적·절차적 습득에 대한 적성의 한계

마이크로러닝 플랫폼 시장은 심도 있는 개념 학습이나 엄격한 순서에 따른 절차 습득이 필요한 이용 사례에서 여전히 구조적인 한계에 직면해 있습니다. 짧은 모듈은 지식의 정착, 회상, 습관 형성에는 효과적이지만, 학습자가 긴 설명, 지도 하에 진행되는 실습, 혹은 다층적인 선행 지식을 필요로 하는 경우에는 그 효과가 떨어집니다. 이는 학습 성과가 깊이와 맥락에 좌우되는 임상 기술, 기술 인증, 고급 소프트웨어 개발, 복잡한 장비의 유지보수 등의 분야에서 중요한 문제가 됩니다. 마이크로러닝을 혼합형이나 강사 주도형 프로그램의 완전한 대체 수단으로 간주하는 공급업체는 고용주의 기대에 부응하지 못할 경우 반발에 직면할 가능성이 있습니다. 이러한 플랫폼이 수행할 수 있는 보다 지속 가능한 역할은 보다 광범위한 학습 시스템의 최상위에 위치한 ‘정착 단계’로서 기능하는 것이지만, 그로 인해 확보할 수 있는 교육 예산의 비율도 제한될 수밖에 없습니다. 따라서 마이크로러닝 플랫폼 시장은 모든 교육 형식을 대체할 수 있는 만능 수단이 아니라, 혼합형 학습 아키텍처의 일부로 판매될 때 가장 효과적으로 성장합니다.

부문별 분석

2025년 기준으로 통합형 LMS 플랫폼은 마이크로러닝 플랫폼 시장의 46.21%를 차지했으나, AI 기반 학습 플랫폼은 2031년까지 연평균 성장률(CAGR) 15.42%로 성장할 것으로 전망됩니다. 이러한 세부 내역은 기업들이 여전히 기존의 학습 기록, 역량 이력 및 관리자용 대시보드와의 연속성을 중시하고 있음을 보여줍니다. 많은 중견 및 대기업은 새로운 워크플로우나 중복된 보고서 작성, 맞춤형 통합이 필요한 독립적인 도구를 추가하는 것보다 현재의 LMS 환경을 확장하는 것을 선호합니다. 이것이 바로, 특히 학습 운영 체계가 잘 정립된 기업에서 통합성이 마이크로러닝 플랫폼 시장의 주요 구매 기준으로 계속 자리 잡고 있는 이유입니다. 독립형 벤더는 여전히 보다 간소화된 도입 프로세스와 특화된 사용자 경험을 원하는 팀들로부터 관심을 받고 있지만, 수요는 기존 기업 시스템과 통합할 수 있는 플랫폼 쪽으로 계속해서 쏠리고 있습니다.

AI 지원 플랫폼의 부상으로 인해 의사결정 과정은 변화하고 있습니다. 왜냐하면 구매자들은 컨텐츠 라이브러리뿐만 아니라, 시스템이 학습 자료를 얼마나 신속하게 제작하고, 개인화하며, 업데이트할 수 있는지를 평가하게 되었기 때문입니다. Pluralsight는 2026년 4월, 새로운 AI 샌드박스 및 가이드형 학습 환경을 출시하며, 짧은 학습 과정에 실시간 실습 피드백을 추가했습니다. 이는 AI가 단순한 부가 기능이 아니라 제품의 차별화 요소 중 하나로 자리 잡고 있음을 보여줍니다. Axonify는 2025년 6월 ‘Co-Creator’를 출시하여, 현장 관리자가 교육 설계에 대한 전문 지식이 없더라도 브랜드화된 마이크로러닝 컨텐츠를 제작할 수 있도록 했습니다. 이로 인해 빈번한 컨텐츠 업데이트의 장벽이 한층 더 낮아졌습니다. 마이크로러닝 플랫폼 업계는 업무상의 변화를 얼마나 신속하게 실용적인 학습 기회로 전환할 수 있는지에 따라 평가받게 되었기 때문에 이러한 움직임은 중요합니다. 그 결과, 플랫폼 선정은 단순히 ‘자체 개발인가, 외부 조달인가’라는 선택에서 제작 속도, 개인화 품질, 데이터의 지속성 등 세부적인 평가로 점차 전환되고 있습니다.

2025년 마이크로러닝 플랫폼 시장 규모에서 클라우드 기반 도입이 68.71%를 차지했으나, 하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 14.13%로 성장할 것으로 전망됩니다. 클라우드는 도입이 신속하고, 인프라 비용이 저렴하며, 업데이트가 용이하고, 여러 기기를 사용하는 분산형 근로자에 대한 지원이 잘 갖춰져 있어 여전히 주요 선택지로 자리 잡고 있습니다. 이러한 장점은 컨텐츠를 학습자에게 신속하게 전달하고, 빈번한 변경이 필요한 마이크로러닝 플랫폼 시장의 일상적인 요구 사항과 잘 부합합니다. 또한, 클라우드 시스템은 공급업체가 새로운 기능을 보다 신속하게 출시할 수 있게 해주며, 이는 현재 AI 도구, 보고서 기능, 워크플로 통합이 꾸준히 추가되고 있는 이 분야에서 중요한 요소입니다. 많은 고용주, 특히 여러 지역에 흩어져 있는 현장 팀을 보유한 기업들에게 있어 클라우드 도입은 IT 관련 부담을 크게 늘리지 않으면서도 사업 규모를 확장할 수 있는 가장 현실적인 방법입니다.

일부 업계에서는 학습자의 데이터와 성과 기록을 모두 로컬 관리 범위 밖으로 옮기지 않으면서도 클라우드의 유연성을 추구하기 때문에 하이브리드 도입이 급속히 확대되고 있습니다. 은행, 국방, 의료, 공공 부문의 조직에서는 데이터 보관 장소에 대한 요건, 감사 또는 내부 정책상의 이유로 기밀 데이터를 특정 환경에 보관해야 하는 경우가 종종 있습니다. Docebo는 2026년 4월, AWS, Azure, Google Cloud의 각 리전에 걸쳐 설정 가능한 데이터 저장 위치 제어 기능을 도입함으로써 이러한 조달 관련 우려 사항에 직접 대응했습니다. 하이브리드 아키텍처 지원은 클라우드의 확장성과 체계적인 데이터 관리 두 가지 측면에 동시에 주의를 기울여야 하기 때문에 벤더에게는 더 어려운 과제가 됩니다. 이 과제는 대형 제공업체와 중소 업체를 구분 짓는 기술적 장벽이 되며, 마이크로러닝 플랫폼 시장에서 광범위한 기업용 벤더와 보다 제한적인 도입 역량을 가진 전문 업체 간의 경계를 명확히 하는 요인이 되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 마이크로러닝 플랫폼 시장의 38.66%를 차지하며, 지역별로는 최대의 수익원이 되었습니다. 이 지역은 기업 연수 비용이 높은 수준이며, 기업 소프트웨어 기반이 탄탄하고, 디지털 학습이 업무의 당연한 일부로 널리 받아들여지고 있다는 장점이 있습니다. 미국 기업들은 이미 성숙한 LMS 환경을 운영하고 있으며, 다수의 직원을 대상으로 마이크로러닝을 확대할 수 있는 정식 학습·개발 팀을 보유하고 있어, 계속해서 수요의 기반이 되고 있습니다. 캐나다와 멕시코에서는 제조업 및 공공 부문에서 연수 제도가 더욱 체계화됨에 따라 지역 성장에 기여하고 있습니다. 이에 따라 기존 인프라와 폭넓은 기업 고객 기반 모두를 통해 북미의 마이크로러닝 플랫폼 시장은 견조한 성장세를 보이고 있습니다.

아시아태평양은 마이크로러닝 플랫폼 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR) 16.21%로 확대될 것으로 전망됩니다. 이러한 성장은 정부 주도의 역량 강화 프로그램, 모바일 우선의 학습자 행동, 그리고 체계적인 연수를 뒷받침하는 정규직 고용 체제의 확대에 힘입어 이루어지고 있습니다. 일본 경제산업성은 2024년 7월 ‘디지털 기술 표준’ 버전 1.2를 발표하여, 디지털 인재의 역량에 관한 국가 기준의 정립에 기여했습니다. 인도의 국립기술 개발공사(NSDC)는 2025년 2월까지 1,300만 명 이상의 수강생이 해당 공사의 플랫폼을 통해 등록했다고 보고했으며, 이는 인도 내 체계적인 기술 개발 활동의 규모를 보여주고 있습니다. 한국 역시 2025년에 AI 및 디지털 역량 강화를 위해 169억 원(1,250만 달러)을, 또한 ‘AID 30+’ 인력 재교육 이니셔티브를 통해 1,100억 원(8,000만 달러)을 투자하여, 디지털 학습 확대를 지원했습니다.

유럽은 여전히 성숙한 지역 시장이며, 독일, 영국, 프랑스가 수익 기반의 대부분을 차지하고 있으며, 데이터 거버넌스 요건이 조달 결정에 점점 더 큰 영향을 미치고 있습니다. 따라서 마이크로러닝 플랫폼 시장 전반에 걸쳐, 공급업체 선정 시 보안 인증, 거주지 관리, AI 규정 준수의 중요성이 더욱 커지고 있습니다. 중동, 특히 사우디아라비아와 아랍에미리트에서는 노동력 다각화 프로그램이 확장 가능한 디지털 학습에 대한 수요를 확대시키고 있어, 유망한 성장 분야로 부상하고 있습니다. 아프리카와 남미는 여전히 수익 규모가 작지만, 스마트폰 보급률이 높아 분산된 근무 환경에서 모바일 배포가 실질적인 이점을 발휘하고 있습니다. 아프리카의 남아프리카공화국, 나이지리아, 케냐, 그리고 남미의 브라질, 아르헨티나, 콜롬비아는 기업의 디지털화가 학습 기술 도입으로 점차 확대됨에 따라 각 지역에서 수요를 주도하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the microlearning platform market size is projected to expand from USD 2.24 billion in 2025 and USD 2.46 billion in 2026 to USD 4.34 billion by 2031, registering a CAGR of 12.05% between 2026 to 2031.

This report is Segmented by Platform Type (Standalone Microlearning Platforms, and More), Deployment Model (Cloud, and More), Enterprise Size (Large Enterprises, and SME), Application (Compliance Training, Workforce Upskilling and Reskilling, and More), Industry Vertical (Banking, Financial Services, and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Microlearning Platform Market Trends and Insights

Growing Need For Continuous Workforce Upskilling And Reskilling

The microlearning platform market is gaining momentum due to a clear mismatch between current workforce skills and the pace of change in digital tools, automation, and job design. The Future of Jobs 2025 report stated that 39% of workers' core skills will need updating within 5 years, which keeps continuous learning high on employer agendas across both private and public organizations. That pressure favors short learning sequences because they can be updated faster and assigned more frequently than longer training formats. It also strengthens the business case for the microlearning platform market, as AI-assisted authoring reduces the time and effort required to create new modules. As reskilling cycles become shorter, vendors that support rapid content refreshes and workflow-based delivery are better placed to serve large organizations with shifting role requirements. This is why the microlearning platform market is moving closer to day-to-day productivity infrastructure rather than remaining limited to periodic training.

Mobile-First Learning Demand Across Deskless And Distributed Workforces

The microlearning platform market is also being supported by learning demand from deskless and distributed employees who do not spend the workday on desktop systems. Mobile-first delivery fits retail, warehousing, field service, food service, and healthcare settings where training has to reach employees during shifts, between tasks, or in low-connectivity environments. Short modules delivered through mobile apps or text-based formats reduce the gap between when a skill is needed and when it is reinforced. Qstream expanded into SMS-based microlearning delivery in January 2026 for pharmaceutical field sales teams working in low-connectivity settings, showing how vendors are adapting the format to operational realities. Bites Learning and EZShift announced a partnership in May 2026 to embed training into shift handover workflows, signaling a broader shift toward learning within operational systems rather than outside them. The microlearning platform market is therefore benefiting not only from mobile access but also from the closer alignment between learning moments and work execution.

Limited Suitability For Deep Conceptual Or Procedural Mastery

The microlearning platform market still faces a structural ceiling in use cases that require deep conceptual learning or tightly sequenced procedural mastery. Short modules are effective for reinforcement, recall, and habit formation, but they are less effective when learners need long-form explanations, supervised practice, or layered prerequisite knowledge. This matters in areas such as clinical skills, technical certification, advanced software development, and complex equipment maintenance, where learning outcomes depend on depth and context. Vendors that position microlearning as a full replacement for blended or instructor-led programs may face pushback if employer expectations are not met. A more durable role for these platforms is as a reinforcement layer on top of broader learning systems, but that also limits how much of the total training budget they can capture. The microlearning platform market, therefore, expands most effectively when sold as part of a mixed learning architecture rather than as a universal substitute for all training formats.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered Personalization And Faster Content Authoring

- Rising Use Of Microlearning For Compliance And Risk Management

- Data Privacy And Cybersecurity Concerns In Cloud And Mobile Delivery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated LMS platforms held 46.21% of the microlearning platform market share in 2025, while AI-enabled learning platforms are projected to grow at a 15.42% CAGR through 2031. That split shows that enterprises still value continuity with their existing learning records, competency histories, and manager dashboards. Many mid-sized and large organizations prefer to extend their current LMS environments rather than add a separate tool that requires new workflows, duplicate reporting, or custom integrations. This explains why integration remains a primary buying criterion for the microlearning platform market, especially among employers with mature learning operations. Standalone vendors still attract interest from teams seeking a simpler deployment path and a more focused user experience, but demand continues to lean toward platforms that integrate with existing enterprise systems.

The rise of AI-enabled platforms is changing that decision process because buyers now assess not only content libraries, but also how quickly a system can produce, personalize, and refresh learning material. Pluralsight launched a new AI sandbox and guided learning environment in April 2026 that added real-time practice feedback within short learning paths, which shows how AI is becoming part of product differentiation rather than a side feature. Axonify launched Co-Creator in June 2025, enabling frontline managers to build branded microlearning content without instructional design expertise, further lowering the barrier to frequent content updates. These moves matter because the microlearning platform industry is increasingly judged by how fast it can turn operational changes into usable learning moments. As a result, platform selection is shifting from a simple build-versus-buy choice to a more detailed evaluation of authoring speed, personalization quality, and data continuity.

Cloud-based deployment accounted for 68.71% of the microlearning platform market size in 2025, while hybrid deployment is forecast to grow at a 14.13% CAGR through 2031. Cloud remains the leading choice because it offers faster implementation, lower infrastructure costs, easier updates, and better support for distributed workers using multiple devices. Those advantages align well with the day-to-day requirements of the microlearning platform market, where content must reach learners quickly and change frequently. Cloud systems also help vendors release new features faster, which matters in a category that is now adding AI tools, reporting layers, and workflow integrations at a steady pace. For many employers, especially those with dispersed frontline teams, cloud deployment remains the most practical way to scale without adding significant IT overhead.

Hybrid deployment is expanding faster because some sectors want cloud flexibility without placing all learner data and performance records outside local control. Banking, defense, healthcare, and public-sector organizations often need to keep sensitive data in specific environments for residency, audit, or internal policy reasons. Docebo introduced configurable data residency controls across AWS, Azure, and Google Cloud regions in April 2026, which directly addressed those procurement concerns. Supporting hybrid architecture is more demanding for vendors because it requires parallel attention to cloud scalability and controlled data management. That challenge creates a technical barrier that can separate larger providers from smaller players, and it gives the microlearning platform market a clearer split between broad-based enterprise vendors and specialists with narrower deployment capabilities.

Geography Analysis

North America accounted for 38.66% of the global microlearning platform market in 2025, making it the largest regional revenue contributor. The region benefits from high corporate training spend, a deep enterprise software base, and widespread acceptance of digital learning as a normal part of work. Enterprises in the United States continue to anchor demand because they already operate mature LMS environments and have formal learning and development teams that can scale microlearning across large employee populations. Canada and Mexico are adding to regional growth as training systems become more formal in manufacturing and public-sector settings. This keeps the microlearning platform market well-supported in North America through both installed infrastructure and a broad enterprise customer base.

Asia-Pacific is the fastest-growing region in the microlearning platform market and is projected to advance at a 16.21% CAGR through 2031. Growth is being driven by government-backed upskilling programs, mobile-first learner behavior, and the expansion of formal employment structures that can support structured training. Japan's Ministry of Economy, Trade, and Industry released Digital Skill Standard version 1.2 in July 2024, which helped define a national benchmark for digital workforce capabilities. India's National Skill Development Corporation reported by February 2025 that more than 13 million candidates had enrolled through its platform, showing the scale of organized skill development activity in the country. South Korea also supported the expansion of digital learning through KRW 16.9 billion (USD 12.5 million) for AI and digital upskilling in 2025, and KRW 110 billion (USD 80 million) through the AID 30+ workforce reskilling initiative.

Europe remains a mature regional market, with Germany, the United Kingdom, and France accounting for much of the revenue base, and data governance requirements increasingly shape procurement decisions. That makes security credentials, residency controls, and AI compliance more important in vendor selection across the microlearning platform market. The Middle East is emerging as a meaningful growth pocket, especially in Saudi Arabia and the United Arab Emirates, where workforce diversification programs are expanding demand for scalable digital learning. Africa and South America still represent smaller revenue pools, but strong smartphone adoption gives mobile delivery a practical edge in dispersed workforce environments. South Africa, Nigeria, and Kenya in Africa, and Brazil, Argentina, and Colombia in South America, are leading demand in their regions as enterprise digitalization gradually extends into learning technology procurement.

- Axonify Inc.

- Qstream, Inc.

- eduMe Ltd.

- Epignosis LLC

- 7taps OpCo LLC

- Neovation Corporation

- Gnowbe Pte. Ltd.

- MobieTrain Corp.

- Digemy Pty Ltd.

- Bites Learning Ltd.

- Arist Holdings Inc.

- Throwing Boulders, LLC

- LEADx, Inc.

- RapL Inc.

- Handy Training Technologies Private Limited

- 5Mins AI Ltd.

- Uptime App Ltd.

- Fivel Systems Corporation

- iSpring Solutions, Inc.

- Bigtincan Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Need for Continuous Workforce Upskilling and Reskilling

- 4.2.2 Mobile-First Learning Demand Across Deskless and Distributed Workforces

- 4.2.3 Ai-Powered Personalization and Faster Content Authoring

- 4.2.4 Rising Use of Microlearning for Compliance and Risk Management

- 4.2.5 Flow-of-Work Delivery Through Collaboration Apps, Text Messaging, and Quick-Response Code Triggers

- 4.2.6 Ai Translation and Localization for Global Rollouts

- 4.3 Market Restraints

- 4.3.1 Limited Suitability for Deep Conceptual or Procedural Mastery

- 4.3.2 Data Privacy and Cybersecurity Concerns in Cloud and Mobile Delivery

- 4.3.3 Weak Roi Attribution Across Embedded Learning Journeys

- 4.3.4 Notification Fatigue and Content Fragmentation

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 Standalone Microlearning Platforms

- 5.1.2 Integrated LMS Platforms

- 5.1.3 AI-Enabled Learning Platforms

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Application

- 5.4.1 Employee Onboarding and New Hire Readiness

- 5.4.2 Compliance Training

- 5.4.3 Sales Enablement and Product Training

- 5.4.4 Workforce Upskilling and Reskilling

- 5.4.5 Leadership and Soft Skills Development

- 5.4.6 Customer and Partner Education

- 5.5 By End User Industry Vertical

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Retail and E-commerce

- 5.5.4 Manufacturing

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Education

- 5.5.7 Government and Public Sector

- 5.5.8 Media and Entertainment

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Singapore

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Turkey

- 5.6.4.4 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Nigeria

- 5.6.5.3 Kenya

- 5.6.5.4 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Colombia

- 5.6.6.4 Chile

- 5.6.6.5 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Axonify Inc.

- 6.4.2 Qstream, Inc.

- 6.4.3 eduMe Ltd.

- 6.4.4 Epignosis LLC

- 6.4.5 7taps OpCo LLC

- 6.4.6 Neovation Corporation

- 6.4.7 Gnowbe Pte. Ltd.

- 6.4.8 MobieTrain Corp.

- 6.4.9 Digemy Pty Ltd.

- 6.4.10 Bites Learning Ltd.

- 6.4.11 Arist Holdings Inc.

- 6.4.12 Throwing Boulders, LLC

- 6.4.13 LEADx, Inc.

- 6.4.14 RapL Inc.

- 6.4.15 Handy Training Technologies Private Limited

- 6.4.16 5Mins AI Ltd.

- 6.4.17 Uptime App Ltd.

- 6.4.18 Fivel Systems Corporation

- 6.4.19 iSpring Solutions, Inc.

- 6.4.20 Bigtincan Holdings Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment