|

시장보고서

상품코드

2063912

의료 품질 관리 분야 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Healthcare Quality Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

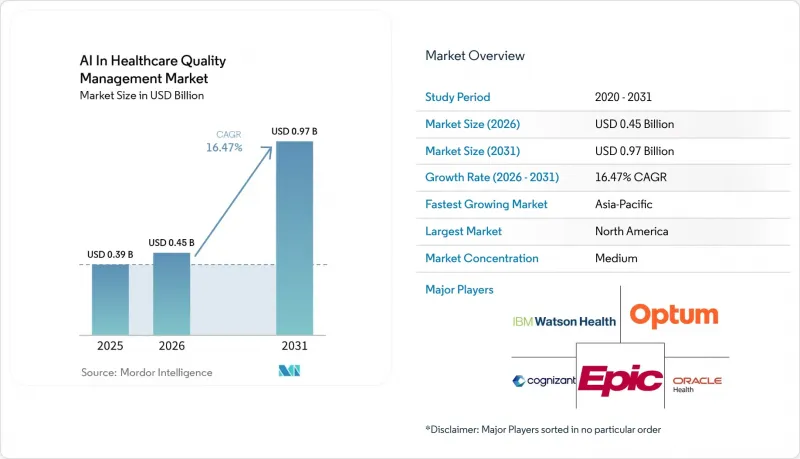

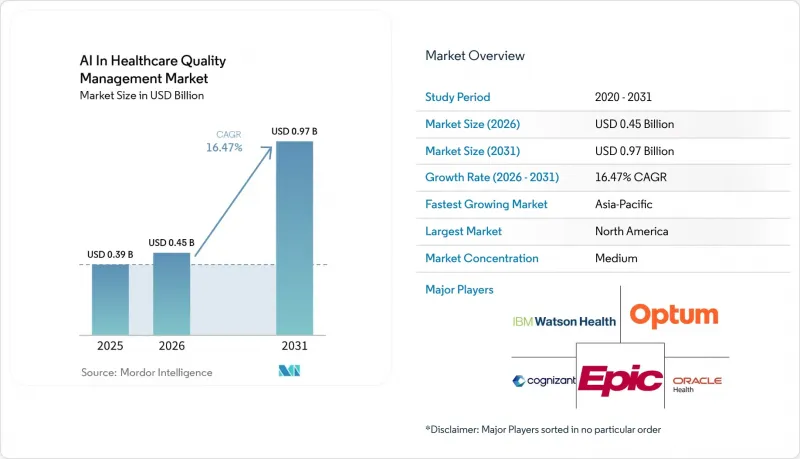

Mordor Intelligence에 의하면, 의료 품질 관리 분야 AI 시장 규모는 2025년에 3억 9,000만 달러로 평가되었고, 2026년에 4억 5,000만 달러로 추정되고, 2031년까지 9억 7,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 16.47%로 성장할 것으로 전망됩니다.

본 보고서는 구성 요소별(소프트웨어 및 서비스), 용도별(신약 개발, 기타), 기술별(머신러닝, 기타), 도입 형태별(온프레미스 및 클라우드), 분석 유형별(기술적 분석, 기타), 데이터 출처별(청구·과금 데이터, 기타), 최종 사용자별, 지역별로 분류되어 있습니다. 시장 규모와 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계의 의료 품질 관리 분야 AI 시장 동향 및 인사이트

정부의 의무화 및 품질 보고에 관한 규정

연방 및 국경 간 정책 조치는 현재 의료 품질 관리 시장에서 AI를 촉진하는 가장 뚜렷한 구조적 요인 중 하나입니다. WISeR 모델은 2026-2031년 운영될 전망이며, AI와 머신러닝을 활용하여 6개 주에서 사전 승인을 처리합니다. 이를 통해 알고리즘 기반 심사 워크플로우에서 결제와 직접 연계된 활용 사례가 창출됩니다. 또한, CMS(미국 의료보험서비스센터)는 인공지능 활용 시 환자 안전과 관련된 2026년 품질 결제 프로그램(QPP) 개선 방안을 최종 확정하고, 해당 임상 의사들에게 일상적인 의료 서비스 제공 과정에서 AI로 인해 발생한 사건과 그 완화 조치를 기록하도록 의무화했습니다. 이와 동시에, FDA와 EMA는 2026년 1월, 규제 대상 개발 환경에서 AI를 활용할 때 의약품 개발자에게 라이프사이클 거버넌스, 성능 모니터링, 인적 감독을 요구하는 공동 원칙을 발표했습니다. 이러한 정책 동향은 이미 컴플라이언스 체제를 구축한 벤더나 사용자에게 유리하게 작용하여, 의료 품질 관리 시장 내 AI 부문에 대한 중소기업의 진입 장벽을 높이는 결과를 초래할 것입니다.

점점 늘어나는 의료 데이터의 양과 복잡성

의료 데이터의 양은 의료 품질 관리 시장의 AI 관련 규제 대상 워크플로우 대부분에서 수동으로 품질 검토를 수행하는 것이 더 이상 현실적이지 않은 수준에 이르렀습니다. 현재 환자 5명 중 1명의 임상 차트 분량이 20만 6,000단어를 초과함에 따라, 품질 관리 팀과 임상 검토 담당자의 요약 작업 부담이 급격히 증가하고 있습니다. 메이요 클리닉 플랫폼의 ‘Discover’ 데이터 세트에는 현재 1,360만 건 이상의 환자 기록, 39억 건의 영상 기록, 12억 5,000만 건의 임상 기록이 포함되어 있으며, 이는 현재 검증 및 모니터링 요구 사항을 형성하고 있는 데이터 환경의 규모를 여실히 보여주고 있습니다. 또한, 복잡성은 핵심 EHR 데이터를 넘어 확대되고 있습니다. Illumina사의 ‘Billion Cell Atlas’ 프로그램은 아스트라제네카, 머크, 일라이 릴리의 창립 멤버들이 참여하여 매년 20페타바이트 규모의 단일 세포 전사체 데이터를 생성할 예정입니다. 임상 데이터셋과 오믹스 데이터셋 모두에 대해 품질 평가를 수행하고 문제를 추적할 수 있는 조직은 향후 의약품 개발 및 품질 관리 업무에서 더욱 견고한 입지를 다지게 될 것으로 보입니다.

데이터 보안, 개인정보 보호, HIPAA/GDPR(EU 개인정보보호규정) 규정 준수 관련 장애물

보안 및 개인정보 보호와 관련된 의무는 도입 비용과 지속적인 운영 부담 모두를 증가시키기 때문에 의료 품질 관리 시장에서 AI 도입을 가로막는 주요 요인으로 계속 작용하고 있습니다. 유럽에서는 GDPR(EU 개인정보보호규정) 제9조에 따라 건강 정보를 특별 범주의 데이터로 취급하고 추가적인 관리 조치를 의무화하고 있을 뿐만 아니라, 유럽 건강 데이터 공간(European Health Data Space)은 모델 개발 시의 2차 이용에 대해 새로운 요건을 추가하고 있습니다. 미국에서는 암호화, 다단계 인증, 위험 평가, 보호 대상 의료 정보의 관리된 취급에 관한 더 엄격한 요건으로 인해, 관리가 느슨한 배포 모델의 여지가 줄어들고 있습니다. 많은 상용 AI 도구는 여전히 규제 대상인 의료 워크플로우에는 적합하지 않습니다. 이는 구매자가 일반 소비자용 제품이 제공하는 것 이상의, 보다 강력한 계약상 및 기술적 관리를 필요로 하기 때문입니다. 이로 인해 제약 기업의 품질 관리 팀은 기업 전체 규모 또는 엄격하게 관리되는 배포 모델로 전환할 수밖에 없게 되었으며, 이는 규정 준수 자원이 부족한 소규모 조직의 도입 지연을 초래하고 있습니다.

부문별 분석

2025년 의료 품질 관리 분야 AI 시장 규모 중 소프트웨어가 58.23%를 차지했습니다. 이는 제약 산업 및 CRO(의약품 개발 수탁 기관) 환경에서 구매자들이 클라우드 네이티브 품질 관리 시스템, 전자 데이터 수집 도구, AI를 활용한 워크플로우 계층을 얼마나 강력하게 지지하고 있는지를 보여줍니다. 이러한 우위는 제한적인 포인트 솔루션보다 통합 플랫폼이 선호되는 경향을 반영하고 있습니다. 왜냐하면 광범위한 시스템은 데이터 이관 문제를 완화하고, 규제 대상 프로세스 전반에 걸쳐 보다 일관된 검증을 지원하기 때문입니다. 모듈형 솔루션의 도입은 여전히 중요하지만, 구매자들은 주요 품질 관리 스택 외부에서 작동하는 도구보다는 거버넌스가 적용된 플랫폼 내에 통합된 모듈을 점점 더 선호하고 있습니다. 프로토콜 위반의 분류에 활용된 로슈의 안전한 AWS 도입 사례는 이러한 경향을 여실히 보여주고 있습니다. 왜냐하면 그 모델은 경량형 독립형 용도이 아니라, 관리되는 운영 환경 내에 배치되어 있었기 때문입니다.

서비스 부문은 2025년 기준 규모는 작지만, 의료 품질 관리 분야 AI 시장에서 2031년까지 연평균 성장률(CAGR)이 17.23%로 가장 빠르게 성장이 전망되는 부문입니다. 이러한 성장은 구현의 복잡성, 검증 작업, 거버넌스 설계, 지속적인 모델 성능 검토에서 기인한 것이며, 많은 고객사는 이러한 업무를 사내에서 처리할 수 있는 인력을 확보하지 못하고 있습니다. 데이터 상황이 시간이 지남에 따라 변화하기 때문에 모델을 업데이트하고, 재검증하며, 모니터링해야 하므로, 이 서비스에 대한 수요는 일회성 성격이 아닙니다. 그 결과, 소프트웨어 기반을 둘러싼 정기적인 서비스 계층이 형성되어 벤더에 대한 충성도 향상은 물론, 의료 품질 관리 분야 AI 시장에서 서비스의 성장을 기업 계정 성장과 밀접하게 연계하게 될 것입니다.

2025년 기준으로, 의료 품질 관리 분야 AI 시장 규모 중 38.54%를 환자 예후 예측이 차지했으며, 이는 이상반응, 질병 진행, 예상되는 반응 패턴을 감지하는 모델에 대한 다년간의 투자가 뒷받침하고 있습니다. 이러한 이용 사례는 임상 프로그램 전반에 걸친 치료 단계의 격상, 모니터링 강도, 문서화의 완전성에 영향을 미치기 때문에 품질 관리에서 핵심적인 역할을 수행하고 있습니다. 실시간 병세 악화 모니터링은 무작위 배정된 검사 환경에서 병원 내 사망률을 35.6% 감소시킨 실적이 있으며, 이는 예측형 품질 관리 도구의 지속적인 도입을 뒷받침하고 있습니다. 이것이 바로 환자 예후 예측이 의료 품질 관리 분야 AI 시장에서 여전히 가장 큰 활용 분야인 이유 중 하나입니다.

임상 검사의 최적화는 가장 빠르게 성장하고 있는 응용 분야로, 의뢰 기관들이 피할 수 있는 검사 변경, 시설의 저조한 성과, 선별 검사의 비효율성을 줄이려 노력함에 따라 2031년까지 연평균 16.94%의 성장률을 보일 것으로 전망됩니다. 공개된 증거에 따르면, NLP를 활용한 사전 선별 검사는 인간에 의한 검토만 했을 때의 71.5%에 비해 진료 기록 수준의 정확도에서 76.1%에 달하며, 환자 수가 많은 암 센터에서는 주당 10-20명의 추가 선별 검사가 가능해집니다. 또한 ConcertAI는 AI를 활용한 실행 가능성 검증을 통해 검사 전체 기간을 10-20개월 단축하고, 프로토콜 수정을 50% 줄일 수 있다고 보고하고 있습니다. 따라서 의료 품질 관리 분야에서 AI의 폭넓은 활용은 사후 품질 점검에서 조기 개입 및 보다 우수한 프로토콜 설계로 점차 전환되고 있습니다.

머신러닝은 결과 예측, 위험도 평가, 이상치 분류의 근간을 이루는 핵심 기법으로 자리매김하고 있어, 2025년 의료 품질 관리 분야 AI 시장에서 45.26%를 차지했습니다. 이러한 우위는 이미 업무상의 품질 요구 사항을 충족하는 지도 학습 및 강화 학습 방식의 최적화 과제에서 입증된 활용 실적을 반영하고 있습니다. 또한, 머신러닝은 새로운 생성형 접근 방식에 비해 검증 실적이 오래되었습니다는 장점도 있는데, 이는 규제가 엄격한 환경에서 중요한 요소가 됩니다. 따라서 의료 품질 관리 분야 AI 시장에서 가장 확고하게 자리 잡은 기술 분야로 자리매김하고 있습니다.

자연어 처리는 가장 빠르게 성장하고 있는 기술로, 2031년까지 18.96%의 성장률이 예상됩니다. 이는 의료 품질 관리 업무의 상당 부분이 여전히 비정형화된 메모, 기록, 규정 문서 속에 존재하기 때문입니다. 병리 보고서 추출 과정에서 EHR(전자건강기록)에서 파생된 대규모 언어 모델은 구조화된 변수에 대해 99.8%의 정확도를 달성했습니다. 이는 텍스트 추출 기능이 현재 조사 워크플로우의 실제 운영을 지원할 수 있음을 보여줍니다. 종양학 분야에서 발표된 사전 선별 연구에서도 NLP를 활용한 리뷰의 정확도 향상이 입증되었으며, 이는 임상 검사 운영 및 품질 데이터 추출에 있어 NLP의 가치를 뒷받침하는 것입니다. 컴퓨터 비전 및 지식 그래프 도구의 도입은 여전히 초기 단계에 있습니다. 그러나 의료 품질 관리 분야 AI 시장에서 품질 관리 팀이 시퀀싱 출력이나 그 밖의 복잡한 데이터 객체를 해석해야 하는 상황에서는 이러한 도구의 중요성이 커지고 있습니다.

지역별 분석

2025년 기준으로 북미는 의료 품질 관리 분야 AI 시장 규모의 35.43%를 차지했으며, 이는 해당 지역의 활발한 규제 활동, 대규모 의료 데이터 세트, 강력한 기업 구매자의 존재가 밀접하게 연관되어 있음을 반영합니다. 미국은 대형 제약사의 본사, 주요 CRO(의약품 개발 수탁 기관)의 사업 거점, 광범위한 디지털 인프라를 갖춘 의료 시스템이 융합되어 있어 여전히 지역 수요의 중심지 역할을 하고 있습니다. CMS(미국 의료보험 및 의료서비스 센터)의 환급 프로그램과 연방 정부의 AI 거버넌스 원칙은 IT 예산 전체가 압박을 받고 있는 상황에서도 여전히 강력한 수요 신호를 보내고 있습니다. 캐나다와 멕시코는 여전히 소규모 시장이지만, 두 나라 모두 사이트 간에 보다 표준화된 품질 프로세스가 요구되는 북미 임상 개발 네트워크 내에서 수행하는 역할 덕분에 혜택을 보고 있습니다. 유럽은 EU AI법, 유럽 헬스 데이터 스페이스, 규제 대상 AI의 이용에 관한 라이프사이클 거버넌스에 대한 합의 형성이 진행되고 있는 것을 배경으로, 의료 품질 관리 분야 AI 시장에서 두 번째 주요 지역 거점으로서의 입지를 공고히 하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 규제 현대화, 강력한 CRO(의약품 개발 수탁 기관) 역량, 헬스케어 및 기술 분야 신규 진출기업 간의 더욱 활발한 협력에 힘입어 2031년 연평균 성장률(CAGR)은 22.54%를 나타낼 것으로 전망됩니다. 일본은 중요한 거점이며, 2026년 2월에는 시오노기 제약과 히타치가 생성형 AI 솔루션을 발표하여 임상 검사 보고서 작성 시간을 50%, 임상 검사 프로토콜 작성 시간을 20% 단축했습니다. 또한, 2026년 4월 NTT 데이터와 주외제약이 제휴함에 따라 인터뷰 양식 초안 작성 기간이 1-2개월 단축되었으며, 약물감시 및 규제 품질 관리 워크플로가 빠르게 자동화로 전환되고 있음이 밝혀졌습니다. 중국과 인도는 대규모 임상 검사를 실시함으로써 시장 규모를 확대하고 있으며, 베이징대학교 종양병원의 연구에 따르면, AI를 활용한 품질 관리(QC) 플랫폼이 2023년 발표된 211건의 조사 보고서 중 19.9%를 품질상 시정 조치가 필요한 사례로 식별한 것으로 나타났습니다.

중동 및 아프리카와 남미는 의료 품질 관리 분야 AI 시장 규모가 여전히 작지만, 두 지역 모두 긍정적인 추세를 보이고 있습니다. GCC는 보다 광범위한 AI 의료 인프라에 대한 투자를 추진하고 있으며, 이로 인해 현지에서 대규모 구축 없이도 확장 가능한 품질 관리 플랫폼을 위한 조기 진출 기회가 생겨나고 있습니다. 현재의 지역 구성에서 브라질과 아르헨티나는 여전히 남미 최대 시장으로 자리 잡고 있는 반면, 남아프리카공화국은 사하라 이남 아프리카의 중요한 거점으로 자리 잡고 있습니다. 두 지역 모두에서 주요 도시권 이외의 지역은 데이터 인프라와 전문적인 IT 역량의 구축 수준이 고르지 않기 때문에 클라우드 기반 SaaS 모델은 현지 온프레미스 방식보다 유리한 입장에 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the aI in healthcare quality management market size is projected to be USD 0.39 billion in 2025, USD 0.45 billion in 2026, and reach USD 0.97 billion by 2031, growing at a CAGR of 16.47% from 2026 to 2031.

This report is Segmented by Component (Software and Services), Application (Drug Discovery & Development, and More), Technology (Machine Learning, and More), Deployment (On-Premise and Cloud), Analytics Type (Descriptive, and More), Data Source (Claims & Billing, and More), End User, and Geography. The Market and Forecasted in Terms of Value (USD).

Global AI In Healthcare Quality Management Market Trends and Insights

Government Mandates & Quality-Reporting Regulations

Federal and cross-border policy actions are now one of the clearest structural drivers for AI in the healthcare quality management market. The WISeR model is active from 2026 through 2031 and uses AI and machine learning to process prior authorizations across 6 states, which creates a direct payment-linked use case for algorithmic review workflows. CMS also finalized a new 2026 Quality Payment Program improvement activity on patient safety in the use of artificial intelligence, requiring eligible clinicians to document AI-attributable events and mitigation steps in routine care delivery. In parallel, the FDA and EMA issued joint principles in January 2026 that press drug developers toward lifecycle governance, performance monitoring, and human oversight for AI use in regulated development settings. These policy moves favor vendors and users that already have compliance infrastructure in place, and they raise entry barriers for smaller companies in the AI in healthcare quality management market.

Growing Healthcare Data Volume & Complexity

Healthcare data volume has reached a level where manual quality review is no longer workable for many regulated workflows in the AI in healthcare quality management market. One in 5 patients now has a clinical chart exceeding 206,000 words, which sharply increases the abstraction burden for quality teams and clinical reviewers. The Mayo Clinic Platform Discover dataset currently includes more than 13.6 million patient records, 3.9 billion imaging records, and 1.25 billion clinical notes, which highlights the scale of data environments now shaping validation and monitoring needs. Complexity is also expanding beyond core EHR data, as Illumina's Billion Cell Atlas program is set to generate 20 petabytes of single-cell transcriptomic data each year with founding participation from AstraZeneca, Merck, and Eli Lilly. Organizations that can score quality and trace issues across both clinical and omic datasets are likely to hold a stronger position in future drug development and quality operations.

Data-Security, Privacy & HIPAA/GDPR Compliance Hurdles

Security and privacy obligations remain a material restraint on the AI in the healthcare quality management market because they raise both implementation cost and ongoing operating burden. In Europe, GDPR Article 9 treats health information as special category data and requires additional controls, while the European Health Data Space adds new requirements for secondary use in model development. In the United States, stricter expectations around encryption, multi-factor authentication, risk assessment, and governed handling of protected health information are narrowing the room for lightly controlled deployment models. Many off-the-shelf AI tools remain unsuitable for regulated healthcare workflows because buyers need stronger contractual and technical controls than standard consumer-grade offerings provide. This pushes pharma quality teams toward enterprise-scale or tightly managed deployment models, which slows adoption among smaller organizations with fewer compliance resources.

Other drivers and restraints analyzed in the detailed report include:

- Advancement of AI-Based Predictive & Prescriptive Analytics

- Shift to Value-Based Reimbursement Incentives

- Algorithmic Bias & Clinical Explainability Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 58.23% of the AI in healthcare quality management market size in 2025, which shows how strongly buyers favor cloud-native quality systems, electronic data capture tools, and AI-enabled workflow layers across pharmaceutical and CRO settings. This lead reflects the preference for integrated platforms over narrow point solutions, because broader systems reduce data handoff issues and support more consistent validation across regulated processes. Modular deployment still matters, but buyers increasingly want modules that sit inside a governed platform rather than tools that operate outside the main quality stack. Roche's secure AWS deployment for protocol deviation classification illustrates this pattern, since the model sat within a controlled operating environment rather than a lightweight standalone application.

Services, while smaller in 2025, are the fastest-growing component with a 17.23% CAGR through 2031 in the AI in healthcare quality management market. Growth comes from implementation complexity, validation work, governance design, and ongoing model performance review, which many clients cannot staff internally. This service demand is not one-time in nature because models must be updated, revalidated, and monitored as data conditions change over time. The result is a recurring service layer around the software base, which improves vendor stickiness and keeps services tied closely to enterprise account growth in the AI in healthcare quality management market.

Patient outcome prediction held 38.54% of AI in the healthcare quality management market size in 2025, supported by long-running investment in models that flag adverse events, disease progression, and likely response patterns. These use cases are central to quality management because they influence care escalation, monitoring intensity, and documentation completeness across clinical programs. Real-time deterioration surveillance has already shown a 35.6% reduction in in-hospital mortality in randomized settings, which supports ongoing procurement of predictive quality tools. This helps explain why patient outcome prediction remains the largest application area in the AI in healthcare quality management market.

Clinical trial optimization is the fastest-growing application and is projected to grow at 16.94% through 2031, as sponsors try to reduce avoidable amendments, site underperformance, and screening inefficiency. Published evidence shows NLP-assisted prescreening can reach 76.1% chart-level accuracy versus 71.5% for human-only review and can add 10 to 20 patients screened each week in a high-volume cancer center. ConcertAI also reported that AI-driven feasibility validation can shorten overall trial timelines by 10 to 20 months and reduce protocol amendments by 50%. The broader application mix in the AI in healthcare quality management industry is therefore moving from reactive quality checks toward earlier intervention and better protocol design.

Machine learning accounted for 45.26% of the 2025 AI in healthcare quality management market because it remains the core method behind outcome prediction, risk scoring, and deviation classification. Its lead reflects established use in supervised prediction and reinforcement-style optimization tasks that already fit operational quality needs. Machine learning also benefits from a longer validation history than newer generative approaches, which matters in tightly regulated settings. That makes it the most established technology layer within the AI in healthcare quality management market.

Natural language processing is the fastest-growing technology and is projected to expand at 18.96% through 2031 because much of healthcare quality work still sits inside unstructured notes, narratives, and regulatory documents. In pathology report extraction, EHR-derived large language models achieved 99.8% accuracy on structured variables, which shows that text extraction can now support production use in research workflows. Published prescreening work in oncology also showed accuracy gains for NLP-assisted review, which reinforces its value in trial operations and quality abstraction. Computer vision and knowledge graph tools are still early in adoption. Still, they are gaining relevance where quality teams must interpret sequencing outputs and other complex data objects in the AI in healthcare quality management market.

Geography Analysis

North America held 35.43% of AI in healthcare quality management market size in 2025, which reflects the region's dense mix of regulatory activity, large healthcare datasets, and strong enterprise buyer presence. The United States remains the center of regional demand because it combines large pharma headquarters, major CRO operations, and health systems with broad digital infrastructure. CMS reimbursement programs and federal AI governance principles continue to create a strong demand signal even when broader IT budgets face pressure. Canada and Mexico remain smaller markets, but both benefit from their role in North American clinical development networks that require more standardized quality processes across sites. Europe follows as the second major regional base in the AI in healthcare quality management market, supported by the EU AI Act, the European Health Data Space, and growing alignment around lifecycle governance for regulated AI use.

Asia-Pacific is the fastest-growing region, with a 22.54% CAGR through 2031, driven by regulatory modernization, strong CRO capacity, and more active collaboration between healthcare and technology players. Japan is a key anchor, where Shionogi and Hitachi launched a generative AI solution in February 2026 that reduced clinical study report preparation time by 50% and clinical trial protocol drafting time by 20%. NTT DATA's April 2026 collaboration with Chugai Pharmaceutical also shortened draft preparation for Interview Forms by 1 to 2 months, showing that pharmacovigilance and regulatory quality workflows are moving quickly toward automation. China and India add scale through high-volume clinical trial execution, and work from Beijing University Cancer Hospital showed that an AI-enabled QC platform flagged 19.9% of 2023 study reports for quality intervention across 211 studies.

The Middle East and Africa and South America remain smaller in the AI in healthcare quality management market, but both regions show a positive direction of travel. GCC countries are investing in broader AI healthcare infrastructure, which creates early openings for quality management platforms that can scale without heavy local buildout. Brazil and Argentina remain the largest South American country markets in the current regional mix, while South Africa serves as an important base within sub-Saharan Africa. Across both regions, cloud-based SaaS models are better placed than local on-premise approaches because data infrastructure and specialized IT capability remain uneven outside major urban centers.

- Berg Health

- Change Healthcare

- Cognizant

- Epic Systems

- GE Healthcare

- Health Catalyst

- IBM

- LeanTaaS

- Medtronic Care Management

- Merative

- Optum

- Oracle Health

- Palantir Foundry for Health

- Koninklijke Philips

- Premier

- Qventus

- SAS Institute

- Tempus Labs

- Wolters Kluwer Health

- Zebra Medical Vision

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Mandates & Quality-Reporting Regulations

- 4.2.2 Growing Healthcare Data Volume & Complexity

- 4.2.3 Advancement of AI-Based Predictive & Prescriptive Analytics

- 4.2.4 Shift to Value-Based Reimbursement Incentives

- 4.2.5 Proliferation of Real-World Evidence from Connected Devices

- 4.2.6 Generative-AI Automation of Quality-Measure Abstraction

- 4.3 Market Restraints

- 4.3.1 High Implementation & Integration Costs

- 4.3.2 Data-Security, Privacy & HIPAA/GDPR Compliance Hurdles

- 4.3.3 Fragmented Interoperability Standards (FHIR, HL7, ICD-11)

- 4.3.4 Algorithmic Bias & Clinical Explainability Limitations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Application

- 5.2.1 Drug Discovery & Development

- 5.2.2 Clinical Trial Optimisation

- 5.2.3 Patient Outcome Prediction

- 5.2.4 Quality Measure Benchmarking

- 5.2.5 Adverse Event Detection & RCA

- 5.2.6 Others

- 5.3 By Technology

- 5.3.1 Machine Learning

- 5.3.2 Natural-Language Processing (NLP)

- 5.3.3 Computer Vision

- 5.3.4 Knowledge Graphs & Reasoning

- 5.3.5 Others

- 5.4 By Deployment

- 5.4.1 On-premise

- 5.4.2 Cloud

- 5.5 By Analytics Type

- 5.5.1 Descriptive

- 5.5.2 Predictive

- 5.5.3 Prescriptive

- 5.6 By Data Source

- 5.6.1 Electronic Health Records (EHR)

- 5.6.2 Genomics / Multi-omics

- 5.6.3 Clinical-Trial & RWE datasets

- 5.6.4 Claims & Billing

- 5.6.5 Others

- 5.7 By End User

- 5.7.1 Pharmaceutical Companies

- 5.7.2 Biotechnology Companies

- 5.7.3 Contract Research Organizations (CROs)

- 5.7.4 Others

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 India

- 5.8.3.3 Japan

- 5.8.3.4 Australia

- 5.8.3.5 South Korea

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East & Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of MEA

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Berg Health

- 6.3.2 Change Healthcare

- 6.3.3 Cognizant

- 6.3.4 Epic Systems

- 6.3.5 GE HealthCare

- 6.3.6 Health Catalyst

- 6.3.7 IBM Watson Health

- 6.3.8 LeanTaaS

- 6.3.9 Medtronic Care Management

- 6.3.10 Merative

- 6.3.11 Optum

- 6.3.12 Oracle Health

- 6.3.13 Palantir Foundry for Health

- 6.3.14 Philips Healthcare

- 6.3.15 Premier Inc.

- 6.3.16 Qventus

- 6.3.17 SAS Institute

- 6.3.18 Tempus Labs

- 6.3.19 Wolters Kluwer Health

- 6.3.20 Zebra Medical Vision

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment