|

시장보고서

상품코드

2063925

콜드체인 관리 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Cold Chain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

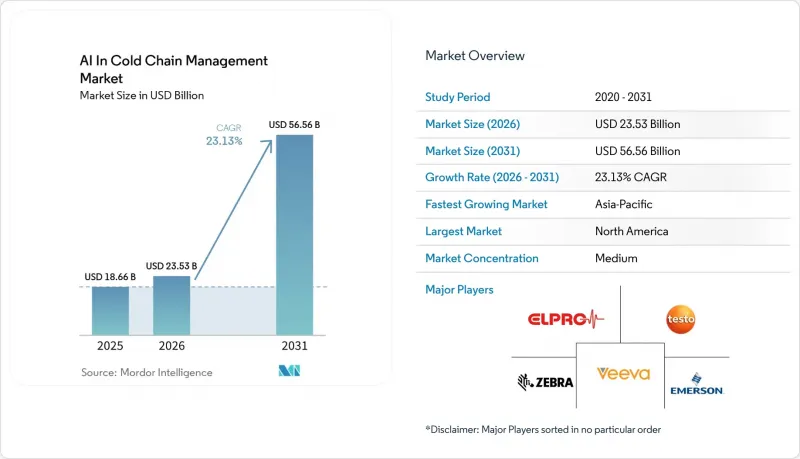

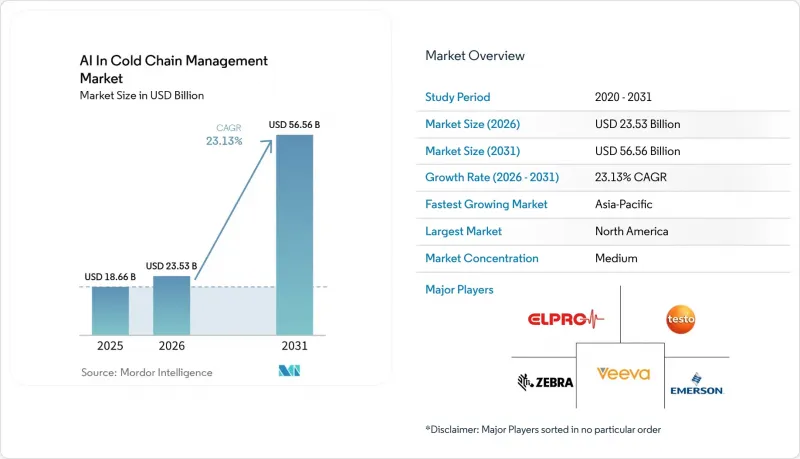

Mordor Intelligence에 의하면, 콜드체인 관리 AI 시장 규모는 2025년 186억 6,000만 달러로 평가되었고, 2026년에는 235억 3,000만 달러로 추정되고, 2031년까지 565억 6,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 23.13%로 성장할 것으로 전망됩니다.

본 보고서는 컴포넌트별(하드웨어, 소프트웨어, 서비스), 온도 범위별(냉장, 냉동, 초저온, 극저온), 물류 단계별(보관, 운송), 최종 이용 산업별(식음료, 의약품 및 의료, 기타), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 콜드체인 관리 AI 시장 동향 및 인사이트

규정 준수를 중심으로 한 디지털 추적성이 콜드체인의 IT 아키텍처를 혁신하고 있습니다.

추적성은 백오피스 기능에서 규제 대상 공급망 내 일상 업무의 핵심 요소로 발전했습니다. AI 주도형 콜드체인 관리 시장에서 일련번호가 부여된 식별자 및 이벤트 기록은 상호 운용성과 정확성을 확보하면서 인계 과정에서 원활하게 이전되어야 합니다. DSCSA에 따른 FDA의 포장 단위 전자 추적 요건으로 인해, 이해관계자들은 EPCIS 규격을 준수하는 데이터 교환으로 전환하고 있으며, 실시간 데이터 처리가 가능한 시스템에 대한 수요가 증가하고 있습니다. 당초에는 규정 준수에 중점을 두었던 이러한 이벤트 스트림은 현재, 특히 의약품 및 기타 콜드체인 업무 분야에서 특정 경로나 시설 전체의 위험을 평가하는 예측 모델의 입력 데이터로 활용되고 있습니다.

생물학적 제제 및 전문 의약품의 콜드체인 확장에 필요한 좁은 범위의 고정밀도

바이오의약품, mRNA 플랫폼, 첨단 치료법의 성장에 따라 허용 온도 범위가 더욱 엄격해지면서, 콜드체인에 대한 지속적인 모니터링의 필요성이 높아지고 있습니다. 이에 따라, 온도 편차를 방지하기 위해 환경 조건을 모니터링하고 분석하는 정밀 센서 및 소프트웨어에 대한 수요가 증가하고 있습니다. 강화된 모니터링 시스템은 온도 편차 감소 및 감사 효율 향상 등 운영 측면에서 큰 이점을 입증하고 있습니다. 온도 편차로 인한 막대한 경제적 손실을 고려할 때, 정밀한 모니터링과 적시적인 개입이 필수적이며, AI 도입은 전문 의약품의 확대와 발맞추어 진행되고 있습니다.

높은 도입 비용과 ROI 달성 여부가 불투명하다는 점이 기업의 도입을 지연시키고 있습니다.

콜드체인 관리에 AI를 도입하려면 기업용 등급의 하드웨어, 검증된 소프트웨어, 통합 지원이 필요하기 때문에 투자 측면에서 큰 과제가 있습니다. 1,000대의 차량에 IoT를 도입하려면 막대한 비용이 소요되므로, 소규모 사업자의 경우 본격적인 도입이 경제적으로 어렵습니다. 콜드체인 업무의 대부분을 담당하는 이러한 소규모 기업들은 회수 기간이 장기화될 위험을 관리할 만한 재정적 여유가 부족한 경우가 많습니다. 이 문제는 규제가 엄격한 환경에서 더욱 두드러지며, 검증, 문서화 및 감사 기준 준수가 비용을 더욱 증가시킵니다. 그 결과, 규정 준수 요건, 제품 리스크 또는 고객 요구 사항에 따라 투자 회수 전망이 더 명확해질 때까지 도입이 미뤄지는 경우가 종종 있습니다.

부문별 분석

2025년 기준으로 콜드체인 관리 AI 시장 점유율 중 71.34%를 하드웨어가 차지했으며, 이는 물리적 감지 및 연결성이 대부분의 도입 사례에서 여전히 초기 투자 단계임을 보여줍니다. 하드웨어 기반에는 온도 센서, 게이트웨이, 엣지 프로세서, 연결 모듈이 포함되며, 이를 통해 출하, 팔레트, 차량, 시설 각 단계에서 상태 데이터를 활용할 수 있게 됩니다. 신뢰할 수 있는 현장 데이터가 부족하거나 간헐적으로만 확보될 경우, 어떤 분석 스택도 확장할 수 없기 때문에 이러한 경향은 콜드체인 관리 AI 시장 발전 과정과 일치합니다.

하드웨어의 매출 비중이 높다고 해서 소프트웨어의 중요성이 떨어지는 것은 아닙니다. 왜냐하면, 가장 급격한 가치 증가는 대개 센서 기반이 이미 구축된 후에 나타나기 때문입니다. 이 소프트웨어 시장은 2026-2031년 연평균 성장률(CAGR) 28.55%를 나타낼 것으로 예측되며, 이는 기존 인프라에서 더 많은 가치를 창출하기 위한 분석, 자동화된 규정 준수 보고, 경로 위험 점수 산정, 디지털 트윈 도구에 대한 수요 증가를 반영한 것입니다.

2025년 기준으로, 콜드체인 관리 AI 시장 규모 중 61.45%를 ‘냉장’ 부문이 차지했으며, 다른 온도대를 크게 앞지르며 최대 부문으로 자리매김했습니다. 이 온도대는 인슐린, GLP-1 주사제, 유제품, 신선식품, 다양한 일반 백신을 포함한 광범위한 제품군을 아우르기 때문에 출하량은 보다 전문적인 온도대에 비해 당연히 더 많아집니다. 냉동(Frozen) 부문은 2031년까지 연평균 성장률(CAGR) 27.79%를 나타낼 것으로 예측되며, 이는 고부가가치 의약품이 더 낮은 온도의 환경에서 운송됨에 따라 정밀한 온도 관리에 대한 수요가 증가하고 있음을 반영합니다.

지역별 분석

2025년, 북미 콜드체인 관리 AI 시장 점유율 42.45%를 차지했으며 최대 수익원으로서의 입지를 확고히 했습니다. 이러한 경쟁력은 해당 지역의 첨단 의약품 유통 시스템, 견고한 콜드체인 물류 인프라, 그리고 디지털 추적성 및 모니터링의 발전을 가속화한 조기 규제 조치에 의해 뒷받침되고 있습니다. DSCSA(의약품 안전 추적법)의 시행은 일상 업무에서 데이터의 상호 운용성과 포장 단위별 추적성을 우선시함으로써, 이 시장에서 매우 중요한 역할을 해왔습니다. 소규모 조제 업체에 대해 2026년 11월까지 연장된 DSCSA의 단계적 준수 기한이, 의약품 유통 네트워크 전반에 걸친 조달 활동 및 시스템 업그레이드를 지속적으로 촉진하고 있습니다. 또한, 북미에서는 온도 관리가 필요한 의약품의 유통량이 방대하기 때문에 라스트 마일 배송 업무에 있어 예측 모니터링, 검증된 데이터 수집, 서비스 기준 개선이 조기에 도입되었습니다.

아시아태평양은 콜드체인 관리 AI 시장에서 가장 높은 성장률을 나타낼 것으로 예상되며, 2031년 연평균 성장률(CAGR)은 29.67%에 달할 전망입니다. 중국은 시장 규모 면에서 1위를 차지하고 있지만, 인도는 중요한 성장 기회를 품고 있습니다. 두 시장 모두 방대한 신선식품 유통량과 디지털 전환의 큰 잠재력을 모두 갖추고 있기 때문입니다. 이 지역의 성장은 식품 유통 수요 증가, 냉장 물류 네트워크의 확대, 온도 관리가 필요한 공급망에서 손실을 줄여야 할 필요성에 힘입어 이루어지고 있습니다. 또한, 많은 기업들이 기본적인 가시화 단계에서 한 발 앞서 예측하고 개입하는 단계로 전환하고 있는 만큼, 아시아태평양은 저통합형 솔루션을 제공하는 벤더들에게 큰 기회가 되고 있습니다. 이로 인해, 특히 콜드체인의 현대화가 이미 진행되고 있는 부문에서 하드웨어에 대한 즉각적인 수요와 소프트웨어 기능 강화의 장기적인 가능성이라는 이중의 성장 시나리오가 나타나고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aI in cold chain management market size is expected to increase from USD 18.66 billion in 2025 to USD 23.53 billion in 2026 and reach USD 56.56 billion by 2031, growing at a CAGR of 23.13% over 2026-2031.

This report is Segmented by Component (Hardware, Software, Services), Temperature Range (Chilled, Frozen, Deep-Frozen, and Cryogenic), Logistics Stage (Storage, Transportation), End-Use Industry (Food and Beverages, Pharmaceuticals and Healthcare, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Cold Chain Management Market Trends and Insights

Compliance-Led Digital Traceability Is Rewriting Cold-Chain IT Architecture

Traceability has evolved from a back-office function to a critical part of daily operations in regulated supply chains. In the AI-driven cold chain management market, serialized identifiers and event records must transition seamlessly across handoffs while ensuring interoperability and accuracy. The FDA's package-level electronic tracing requirements under DSCSA have driven stakeholders toward EPCIS-aligned data exchanges, increasing the demand for systems capable of real-time data processing. These event streams, initially compliance-focused, now serve as inputs for predictive models assessing risks across specific routes and facilities, particularly in pharmaceuticals and other cold-chain operations.

Biologics and Specialty Pharma Cold-Chain Expansion Demands Narrow-Range Precision

The growth of biologics, mRNA platforms, and advanced therapies has tightened acceptable temperature ranges, driving the need for continuous intelligence in cold chains. This has increased demand for advanced sensors and software that monitor and interpret conditions to prevent temperature excursions. Enhanced monitoring systems have demonstrated significant operational benefits, such as reducing temperature excursions and improving audit efficiency. With substantial financial losses linked to temperature excursions, precise oversight and timely interventions are critical, aligning AI deployment with the expansion of specialty pharmaceuticals.

High Implementation Cost and Unclear ROI Realization Slow Enterprise Adoption

Adopting AI in cold chain management presents significant investment challenges, as enterprises require enterprise-grade hardware, validated software, and integration support. Deploying IoT for a fleet of 1,000 vehicles incurs high costs, making full-scale implementation unaffordable for smaller operators. These smaller companies, which dominate cold-chain operations, often lack the financial capacity to manage extended payback periods. The issue is more pronounced in regulated environments, where compliance with validation, documentation, and audit standards further increases costs. As a result, adoption is often delayed until compliance demands, product risks, or customer requirements make the returns more evident.

Other drivers and restraints analyzed in the detailed report include:

- Food-Waste Reduction and Perishable E-Grocery Growth Create Parallel AI Demand Curve

- Shift from Passive Logging to Real-Time Predictive Monitoring Restructures Operating Models

- ERP-WMS-TMS-IoT Interoperability Gaps Create Systemic Data Blind Spots

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware held 71.34% of AI in the cold chain management market share in 2025, which shows that physical sensing and connectivity remain the first investment layer in most deployments. The hardware base includes temperature sensors, gateways, edge processors, and connectivity modules that make condition data available at shipment, pallet, vehicle, and facility levels. This pattern is consistent with how the AI in the cold chain management market has developed, because no analytics stack can scale if reliable field data is weak or intermittent.

The revenue weight of hardware does not reduce the importance of software, because the fastest compounding value often appears after the sensor estate is already in place. Software is projected to record a 28.55% CAGR during 2026-2031, reflecting rising demand for analytics, automated compliance reporting, route risk scoring, and digital twin tools that extract more value from installed infrastructure.

Chilled accounted for 61.45% of AI in cold chain management market size in 2025, making it the largest temperature segment by a clear margin. This range covers a broad mix of products, including insulin, GLP-1 injectables, dairy, fresh produce, and many standard vaccines, so shipment volumes are naturally deeper than they are in more specialized ranges. Frozen is projected to grow at a 27.79% CAGR through 2031, which reflects the stronger need for precise control as advanced pharmaceutical products move through colder environments.

Geography Analysis

In 2025, North America accounted for 42.45% of the AI-driven cold chain management market share, securing its position as the leading revenue contributor. This dominance is driven by the region's advanced pharmaceutical distribution systems, strong cold logistics infrastructure, and early regulatory initiatives that have expedited advancements in digital traceability and monitoring. The implementation of DSCSA has played a pivotal role in this market by prioritizing data interoperability and package-level traceability in daily operations. Phased compliance deadlines for DSCSA, extending through November 2026 for smaller dispensers, continue to drive procurement activities and system upgrades across pharmaceutical distribution networks. Additionally, North America's significant volume of temperature-sensitive pharmaceutical flows has facilitated the early adoption of predictive monitoring, validated data capture, and enhanced service standards in last-mile delivery operations.

Asia-Pacific is projected to achieve the highest growth rate in the AI-driven cold chain management market, with a CAGR of 29.67% through 2031. China leads in scale, while India represents a key growth opportunity, as both markets combine substantial perishable flows with significant potential for digital transformation. The region's growth is supported by increasing food distribution demands, the expansion of refrigerated logistics networks, and the need to reduce losses in temperature-sensitive supply chains. Asia-Pacific also presents a substantial opportunity for vendors offering low-integration solutions, as many operators are transitioning from basic visibility to proactive prediction and intervention. This creates a dual growth scenario, with immediate demand for hardware and long-term potential for software enhancements, particularly in areas where cold-chain modernization efforts are already underway.

- Controlant

- DeltaTrak

- ELPRO-BUCHS AG

- Emerson

- Geotab

- ORBCOMM

- Monnit

- Roambee

- Samsara

- SAP

- Sensitech

- SmartSense by Digi

- SpotSee

- Testo

- Tive

- Vaisala

- Veeva Systems

- Wiliot

- Zebra Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Compliance-Led Digital Traceability Adoption

- 4.2.2 Biologics and Specialty Pharma Cold-Chain Expansion

- 4.2.3 Food-Waste Reduction and Perishable E-Grocery Growth

- 4.2.4 Shift From Passive Logging to Real-Time Predictive Monitoring

- 4.2.5 GLP-1 Direct-To-Patient Cold-Chain Complexity

- 4.2.6 Automated Product-Release Decisioning in Pharma

- 4.3 Market Restraints

- 4.3.1 High Implementation Cost and Unclear ROI Realization

- 4.3.2 ERP-WMS-TMS-IoT Interoperability Gaps

- 4.3.3 Tariff-Driven Inflation in Sensing and Edge Hardware

- 4.3.4 Refrigeration and Reefer Technician Shortages

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Temperature Range

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.2.3 Deep-frozen and cryogenic

- 5.3 By Logistics Stage

- 5.3.1 Storage

- 5.3.2 Transportation

- 5.4 By End-use Industry

- 5.4.1 Food and Beverages

- 5.4.2 Pharmaceuticals and Healthcare

- 5.4.3 Chemicals

- 5.4.4 Agriculture and Horticulture

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Controlant

- 6.3.2 DeltaTrak

- 6.3.3 ELPRO-BUCHS AG

- 6.3.4 Emerson

- 6.3.5 Geotab

- 6.3.6 ORBCOMM

- 6.3.7 Monnit

- 6.3.8 Roambee

- 6.3.9 Samsara

- 6.3.10 SAP

- 6.3.11 Sensitech

- 6.3.12 SmartSense by Digi

- 6.3.13 SpotSee

- 6.3.14 Testo SE & Co. KGaA

- 6.3.15 Tive

- 6.3.16 Vaisala

- 6.3.17 Veeva Systems

- 6.3.18 Wiliot

- 6.3.19 Zebra Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment