|

시장보고서

상품코드

2063937

바이오테크놀러지용 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Biotechnology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

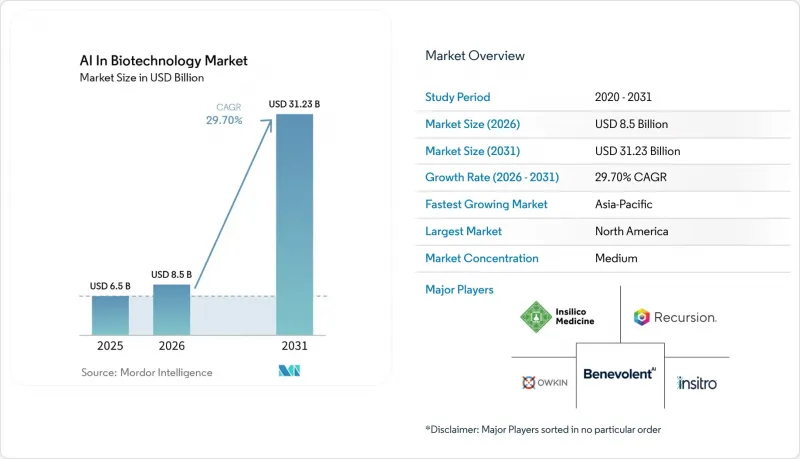

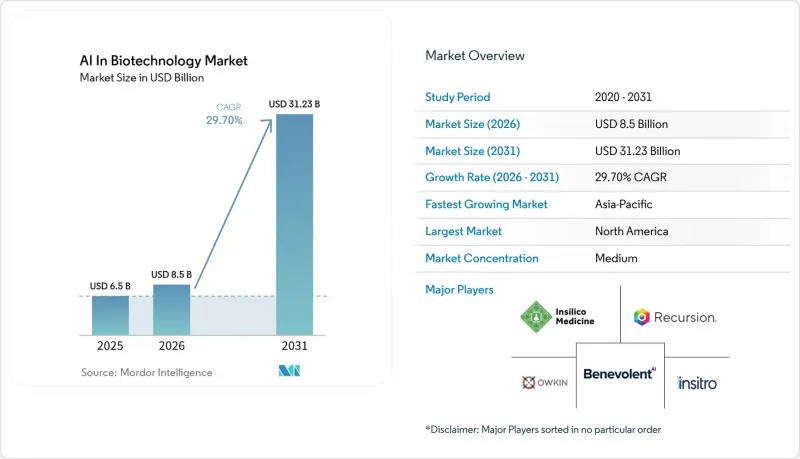

Mordor Intelligence에 의하면, 바이오테크놀러지용 AI 시장 규모는 2025년에 65억 달러로 평가되었고, 2026년에는 85억 달러로 추정되고, 2031년까지 312억 3,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 연평균 성장률(CAGR)은 29.70%를 나타낼 것으로 전망됩니다.

본 보고서는 제공 형태별(소프트웨어, 하드웨어, 서비스), 용도별(신약 개발, 멀티오믹스, 임상 개발, 진단, 바이오프로세싱), 기술별(머신러닝, 컴퓨터 비전, 기타), 도입 형태별(클라우드, 하이브리드, 온프레미스), 최종 사용자별(제약 기업, 생명공학 기업, CRO/CDMO, 학술 기관, 헬스케어), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 바이오테크놀러지용 AI 시장 동향 및 인사이트

AI 주도 신약 개발이 가속화되고 있습니다.

AI는 모델의 성능은 물론 속도와 화합물 합성의 효율성에 중점을 두어, 신약 개발의 초기 단계에서 놀라운 진전을 가져오고 있습니다. 2025년, 렌트셀치브는 AI를 통해 완전히 설계 및 발견된 최초의 약물로 제IIa상 임상시험을 완료했으며, 특발성 폐섬유증 환자에서 위약군의 약 20.3mL에 비해 평균 강제 폐활량이 +98.4mL 개선되었음을 보여주었습니다. Recursion은 업계 평균이 42개월에 2,500개의 화합물인 반면, 17개월 만에 프로그램당 약 330개의 화합물을 합성함으로써 자사 플랫폼의 효율성을 입증했습니다. 이 회사의 REC-4881 프로그램에서 2상 임상시험에 참여한 환자들을 대상으로 한 결과, 12주 시점에서 총 용종 부하가 중앙값 기준으로 43% 감소했습니다. 이러한 발전은 AI가 신약 개발의 경제성을 어떻게 혁신하고 있는지를 여실히 보여주고 있으며, 제약 기업들이 대상과 적응증을 다양화하고 보수적인 접근 방식에 대한 의존도를 낮출 수 있게 해주고 있습니다.

정밀 의학과 바이오마커가 주역으로 부상합니다.

바이오테크놀러지용 AI 시장은 바이오마커 중심의 연구와 함께 발전하고 있으며, 모델의 품질은 분자 수준, 임상 수준, 환자 수준의 데이터를 통합하는 데 달려 있습니다. 사노피의 ‘AI 리서치 팩토리’는 면역학, 종양학, 신경학 분야에서 유효 성분 식별 효율을 기존 방식에 비해 20-30% 향상시켰으며, 2019년 이후 AI를 활용해 개발된 생물학적 제제와 백신의 수를 두 배로 늘렸습니다. 정밀의학 프로그램에는 견고한 환자 군 분류, 바이오마커 선정, 초기 반응의 변동성에 대한 인사이트이 요구됩니다. 유전체과 트랜스크립톰 계층을 분석할 수 있는 AI 플랫폼을 통해, 스폰서는 조기에 고빈도군을 식별할 수 있게 되었으며, 특히 희귀질환이나 특수 질환의 경우, 소규모이고 복잡한 환자 집단에서도 상업적으로 타당성을 확보할 수 있게 되었습니다.

높은 도입 및 검증 비용

바이오테크놀러지용 AI 시장은 시범 운영 예산을 초과하는 생산 등급 도입 비용으로 인해 높은 진입 장벽에 직면해 있습니다. 과제는 모델 구축에 그치지 않고, 데이터 정제, 워크플로우 통합, 검증 기록, 규제 대상 용도에 대한 사내 팀의 지원까지 포함됩니다. 소규모 생명공학 기업이나 대학에서 분사된 기업은 확립된 법적·계산적 체계가 부족하기 때문에 상업화 과정에서 대형 제약사보다 12-24개월 정도 뒤처지는 경우가 많습니다. 미국의 주요 거점 이외의 지역에서는 GPU나 전문적인 인프라에 대한 접근이 제한적이기 때문에 자금력이 풍부한 플랫폼이나 대기업 구매자들이 더욱 유리한 입장에 서게 되어, 소규모 기업의 실험적 AI 신약 개발이 실용화로 이어지는 과정이 지연되고 있습니다.

부문별 분석

2025년, 소프트웨어는 바이오테크놀러지용 AI 시장에서 38.25%를 차지했으며, 제공 서비스 중 주도적인 위치를 유지했습니다. 이러한 우위는 Insilico Medicine이나 Recursion Pharmaceuticals와 같은 기업들이 채택한 플랫폼 주도형 비즈니스 모델에서 비롯된 것으로, 라이선스 및 API 접근을 통해 지속적인 수익을 창출하고 있습니다. 훈련된 모델을 여러 프로그램에서 재사용하더라도 비용이 비례하여 증가하지 않는다는 점은 소프트웨어의 역할을 더욱 강화하고 있습니다. 2025년 9월에 출시된 일라이 릴리의 TuneLab 플랫폼은 독자적인 데이터를 보호하면서도 외부 파트너에게 신약 개발 모델에 대한 접근 권한을 제공함으로써, 확장 가능한 소프트웨어 제공의 모범 사례가 되고 있습니다. 이 소프트웨어는 접근 가능한 모델과 워크플로우를 필요로 하는 제약 기업의 요구를 충족시켜 주며, 여전히 주요 수익원 역할을 하고 있습니다.

서비스 부문은 바이오테크놀러지용 AI 시장에서 가장 빠르게 성장하고 있는 부문으로, 2031년까지 연평균 성장률(CAGR)이 31.45%를 나타낼 것으로 전망됩니다. 많은 제약 기업들은 사내에서 역량을 구축하는 대신, 모델 개발이나 데이터 큐레이션과 같은 업무를 외부에 위탁하는 것을 선호합니다. 이러한 추세는 단순히 도구에 대한 접근뿐만 아니라, 도입을 성공적으로 이루어내기 위해서는 전문 지식, 모델 튜닝, 규제 측면의 지원이 필요하기 때문에 앞으로도 지속될 것으로 보입니다.

2025년 기준으로, 신약 개발은 바이오테크놀러지용 AI 시장에서 45.3%를 차지했으며, 가장 큰 용도 부문으로 자리 잡고 있습니다. AI 우선 플랫폼은 적중률을 유지하거나 향상시키면서, 프로그램당 합성 분자 수를 90% 이상 대폭 줄입니다. Recursion 플랫폼은 연간 1억 분자 이상을 생성하여 실험실 업무량을 40% 줄이는 동시에, 제약 연구개발 분야의 비용 및 일정 문제를 해결하고 있습니다. AI를 활용한 신약 개발은 후보 화합물 풀을 좁히고, 우선순위를 개선하며, 프로그램을 진행하기 전의 실험실 작업을 최소화함으로써 도입을 촉진하고 있습니다.

임상 개발은 바이오테크놀러지용 AI 시장에서 가장 빠르게 성장하고 있는 용도 분야로, 2031년까지 연평균 성장률(CAGR)이 33.24%를 나타낼 것으로 전망됩니다. AI는 속도, 피험자 모집 계획, 실시 과정을 개선함으로써 임상 검사의 운영을 강화합니다. 예를 들어, AI 플랫폼을 통해 환자 등록 기간과 3상 임상시험 비용이 대폭 절감되었습니다. 이러한 운영상의 이점으로 인해 임상 개발 분야에서의 AI 도입 확대가 정당화되었으며, 신약 개발이 가장 큰 용도 부문인 반면, 임상 개발은 가장 빠르게 성장하고 있는 부문이 되었습니다.

지역별 분석

2025년, 북미는 바이오테크놀러지용 AI 시장에서 41.7%라는 압도적인 점유율을 차지하며 지역별 1위 자리를 확고히 다졌습니다. 이 지역은 강력한 벤처 캐피털 기반, 풍부한 AI 연구 인력, 제약 기업의 연구개발(R&D) 본사가 집중되어 있다는 이점을 누리고 있습니다. 대규모 인프라 투자를 통해 컴퓨팅, 생물학, 의약품 개발이 서로 연계되고 있으며, 주요 공동 연구는 공유된 신약 개발 환경에 대한 투자 규모를 반영하고 있습니다. 이러한 자원들의 결합을 통해 북미는 플랫폼 개발 및 기업 도입 분야에서 선도적인 위치를 확고히 하고 있습니다.

유럽은 견고한 제약 기반과 체계적으로 조정된 AI 정책 체계를 결합함으로써, 바이오테크놀러지용 AI 시장에서 중요한 위치를 차지하고 있습니다. 독일, 영국, 프랑스, 이탈리아, 스페인 등 주요 허브가 상업 활동을 주도하는 한편, 오스트리아와 북유럽 국가들은 연구의 깊이를 더하고 있습니다. 이 지역의 학계, 생명공학 산업, 제약 산업이 서로 연계된 네트워크는 신약 개발 연구부터 중개연구에 이르기까지의 과정을 뒷받침하고 있습니다. 거버넌스의 강화는 규정 준수 측면에서 과제를 야기하는 한편, 헬스케어 AI를 위한 공식적인 체계를 확립하고 있습니다.

아시아태평양은 바이오테크놀러지용 AI 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지의 예상 연평균 성장률(CAGR)은 35.5%입니다. 이러한 성장은 중국, 일본, 한국, 인도에서의 정책 지원, 연구 역량 확대, 현지 플랫폼 개발을 통해 주도되고 있습니다. 주요 진전으로는 중국의 AI 기반 신약 개발 가상 스크리닝 플랫폼 구축과 지능형 신약 설계용 AI ‘Kongming’의 도입을 꼽을 수 있습니다. 이러한 움직임은 해당 지역이 국내 모델 구축과 확장 가능한 연구 시스템 구축에 주력하고 있음을 보여줍니다. 중동 및 아프리카는 여전히 초기 단계에 있지만, GCC(걸프협력회의) 회원국들의 정밀의학 프로그램과 남아프리카공화국의 유전체 연구 기반이 향후 도입을 위한 토대를 마련하고 있습니다. 브라질의 임상 연구 생태계가 주도하는 남미 역시 개발 초기 단계에 있습니다. 현재로서는 규모는 작지만, 이러한 지역들은 생명공학 워크플로우에 AI를 보다 광범위하게 도입하기 위한 기반을 마련해 나가고 있습니다. 북미가 주도하고 있으며, 유럽은 여전히 중요한 역할을 수행하고 있고, 아시아태평양이 가장 빠른 성장을 이끌고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aI in biotechnology market size was valued at USD 6.5 billion in 2025 and is estimated to grow from USD 8.5 billion in 2026 to reach USD 31.23 billion by 2031, at a CAGR of 29.70% during the forecast period (2026-2031).

This report is Segmented by Offering (Software, Hardware, Services), Application (Drug Discovery, Multi-Omics, Clinical Development, Diagnostics, Bioprocessing), Technology (ML, Computer Vision, and More), Deployment (Cloud, Hybrid, On-Premises), End User (Pharma, Biotech, CROs/CDMOs, Academic, Healthcare), and Geography (North America, Europe, and More). Value Forecasts (USD).

Global AI In Biotechnology Market Trends and Insights

AI-Led Drug Discovery Accelerates

AI is driving significant advancements in early drug discovery, focusing on speed and compound efficiency alongside model performance. In 2025, Rentosertib became the first fully AI-designed and AI-discovered drug to complete Phase IIa trials, showing a mean forced vital capacity improvement of +98.4 mL compared to -20.3 mL for placebo in idiopathic pulmonary fibrosis patients. Recursion demonstrated its platform's efficiency by synthesizing nearly 330 compounds per program in 17 months, compared to the industry average of 2,500 compounds in 42 months, with its REC-4881 program achieving a 43% median reduction in total polyp burden at 12 weeks in Phase 2 patients.These developments highlight how AI is reshaping drug discovery economics, enabling pharmaceutical companies to diversify targets and indications, reducing reliance on conservative approaches.

Precision Medicine and Biomarkers Take Center Stage

The AI in biotechnology market is advancing with biomarker-guided research, where model quality depends on integrating molecular, clinical, and patient-level data. Sanofi's AI Research Factory improved active ingredient identification in immunology, oncology, and neurology by 20-30% over traditional methods, doubling the number of biologics and vaccines developed with AI since 2019. Precision medicine programs require robust patient stratification, biomarker selection, and early response variability insights. AI platforms capable of analyzing genomic and transcriptomic layers are enabling sponsors to identify enriched populations early, making smaller, complex patient groups commercially viable, especially in rare diseases and specialty areas.

High Implementation and Validation Costs

The AI biotechnology market faces high entry barriers due to production-grade deployment costs exceeding pilot budgets. Challenges extend beyond model building to include data cleaning, workflow integration, validation records, and internal team support for regulated use. Smaller biotechnology firms and academic spinouts often lag large pharmaceutical companies by 12-24 months in commercial deployment due to the absence of established legal and computational frameworks. Limited access to GPUs and specialized infrastructure outside major U.S. hubs further favors well-funded platforms and large enterprise buyers, slowing smaller firms' transition from experimental AI drug discovery to operational use.

Other drivers and restraints analyzed in the detailed report include:

- Harnessing the Power of Vast Genomic and Multi-Omics Datasets

- Biopharma-Tech Collaborations Gain Momentum

- Data Privacy and Regulatory Compliance Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software accounted for 38.25% of the AI in biotechnology market, maintaining its leading position among offerings. This dominance stems from platform-driven business models by companies like Insilico Medicine and Recursion Pharmaceuticals, leveraging recurring revenues through licenses and API access. The reuse of trained models across multiple programs without proportional cost increases further strengthens software's role. Eli Lilly's TuneLab platform, launched in September 2025, exemplifies scalable software delivery by providing external partners access to drug discovery models while safeguarding proprietary data. Software remains the revenue anchor, aligning with pharmaceutical companies' needs for accessible models and workflows.

Services are the fastest-growing segment in the AI in biotechnology market, with a projected CAGR of 31.45% through 2031. Many drug manufacturers prefer outsourcing tasks like model development and data curation instead of building in-house capabilities. This trend persists as successful deployment requires domain expertise, model tuning, and regulatory support, beyond just tool access.

Drug discovery and development held 45.3% of the AI in biotechnology market share in 2025, making it the largest application area. AI-first platforms significantly reduce synthesized molecules per program by over 90% while maintaining or improving hit rates. Recursion's platform generates over 100 million molecules annually, reducing wet-lab work by 40% and addressing cost and timing challenges in pharmaceutical R&D. AI drug discovery drives adoption by narrowing candidate pools, improving prioritization, and minimizing lab work before advancing programs.

Clinical development is the fastest-growing application in the AI in biotechnology market, with a projected CAGR of 33.24% through 2031. AI enhances trial operations by improving speed, enrollment planning, and execution. For example, AI platforms have reduced patient registration times and Phase III costs significantly. These operational gains justify broader AI deployment in clinical development, making it the fastest-growing area while drug discovery remains the largest application.

Geography Analysis

In 2025, North America commanded a dominant 41.7% share of the AI in biotechnology market, solidifying its top regional position. The region benefits from a strong venture capital base, extensive AI research talent, and a high concentration of pharmaceutical R&D headquarters. Significant infrastructure investments connect computing, biology, and drug development, with major collaborations reflecting the scale of investment in shared discovery environments. This combination of resources positions North America as a leader in platform development and enterprise adoption.

Europe holds a significant position in the AI in biotechnology market, combining a strong pharmaceutical foundation with a coordinated AI policy framework. Key hubs like Germany, the UK, France, Italy, and Spain drive commercial activity, while Austria and Nordic countries contribute research depth. The region's interconnected academic, biotech, and pharmaceutical networks support adoption across discovery and translational research. Stricter governance adds compliance challenges but establishes a formal framework for healthcare AI.

Asia-Pacific is the fastest-growing region in the AI in biotechnology market, with a forecast CAGR of 35.5% through 2031. Growth is driven by policy support, expanding research capacity, and local platform development in China, Japan, South Korea, and India. Milestones include China's launch of an AI-driven drug virtual screening platform and the introduction of AI Kongming for intelligent drug design. These developments highlight the region's focus on building domestic models and scalable research systems. The Middle East and Africa remain in early stages, with GCC precision medicine programs and South Africa's genomics base laying the groundwork for future adoption. South America, led by Brazil's clinical research ecosystem, is also in the early stages of development. While smaller today, these regions are building the foundation for broader AI adoption in biotechnology workflows. North America leads, Europe remains pivotal, and Asia-Pacific drives the fastest growth.

- BenevolentAI SA

- BPGbio, Inc.

- CytoReason Ltd.

- Deep Genomics, Inc.

- DNAnexus, Inc.

- Genialis, Inc.

- Iktos SA

- Illumina

- Insilico Medicine

- Insitro, Inc.

- NVIDIA

- Owkin, Inc.

- PathAI, Inc.

- QIAGEN

- Recursion Pharmaceuticals

- Schropdinger, Inc.

- SOPHiA GENETICS SA

- Tempus AI, Inc.

- Valo Health, Inc.

- XtalPi, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Led Drug Discovery Acceleration

- 4.2.2 Precision Medicine and Biomarker-Guided Therapeutics

- 4.2.3 Scaling Genomic and Multi-Omics Datasets

- 4.2.4 Biopharma-Tech Partnerships and Funding Momentum

- 4.2.5 Self-Driving Labs and Closed-Loop Wet-Lab Automation

- 4.2.6 Federated Multi-Institution Model Training

- 4.3 Market Restraints

- 4.3.1 High Implementation and Validation Cost

- 4.3.2 Data Privacy and Regulatory Compliance Burden

- 4.3.3 GPU and Advanced Compute Bottlenecks

- 4.3.4 IP And GxP Auditability Uncertainty

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Drug Discovery and Development

- 5.2.2 Genomics and Multi-Omics Analysis

- 5.2.3 Clinical Development

- 5.2.4 Diagnostics and Decision Support

- 5.2.5 Precision Medicine

- 5.2.6 Bioprocessing and Manufacturing

- 5.3 By Technology

- 5.3.1 Machine Learning and Deep Learning

- 5.3.2 Generative AI and Foundation Models

- 5.3.3 Natural Language Processing and Knowledge Graphs

- 5.3.4 Computer Vision

- 5.3.5 Graph, Causal, and Systems Biology Models

- 5.4 By Deployment Mode

- 5.4.1 Cloud-Based

- 5.4.2 Hybrid

- 5.4.3 On-Premises

- 5.5 By End User

- 5.5.1 Pharmaceutical Companies

- 5.5.2 Biotechnology Companies

- 5.5.3 CROs and CDMOs

- 5.5.4 Academic and Research Institutes

- 5.5.5 Healthcare Providers and Diagnostic Laboratories

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 BenevolentAI SA

- 6.3.2 BPGbio, Inc.

- 6.3.3 CytoReason Ltd.

- 6.3.4 Deep Genomics, Inc.

- 6.3.5 DNAnexus, Inc.

- 6.3.6 Genialis, Inc.

- 6.3.7 Iktos SA

- 6.3.8 Illumina, Inc.

- 6.3.9 Insilico Medicine

- 6.3.10 Insitro, Inc.

- 6.3.11 NVIDIA Corporation

- 6.3.12 Owkin, Inc.

- 6.3.13 PathAI, Inc.

- 6.3.14 QIAGEN N.V.

- 6.3.15 Recursion Pharmaceuticals, Inc.

- 6.3.16 Schropdinger, Inc.

- 6.3.17 SOPHiA GENETICS SA

- 6.3.18 Tempus AI, Inc.

- 6.3.19 Valo Health, Inc.

- 6.3.20 XtalPi, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space and unmet-need assessment