|

시장보고서

상품코드

2063955

AI 기반 규제 정보 관리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)AI In Regulatory Information Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

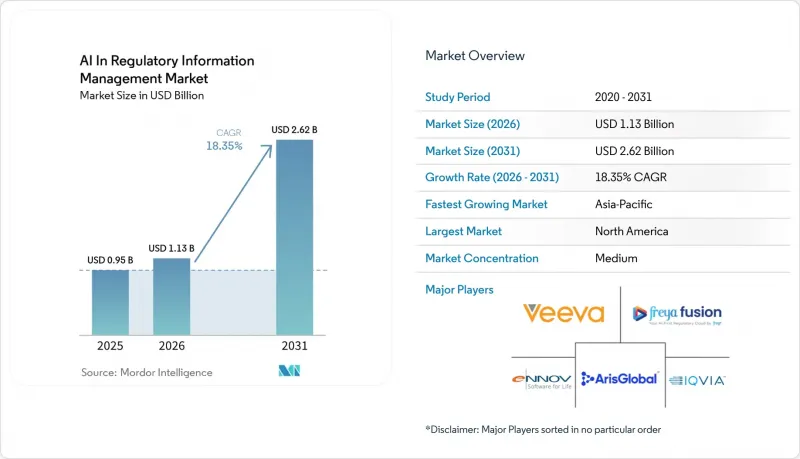

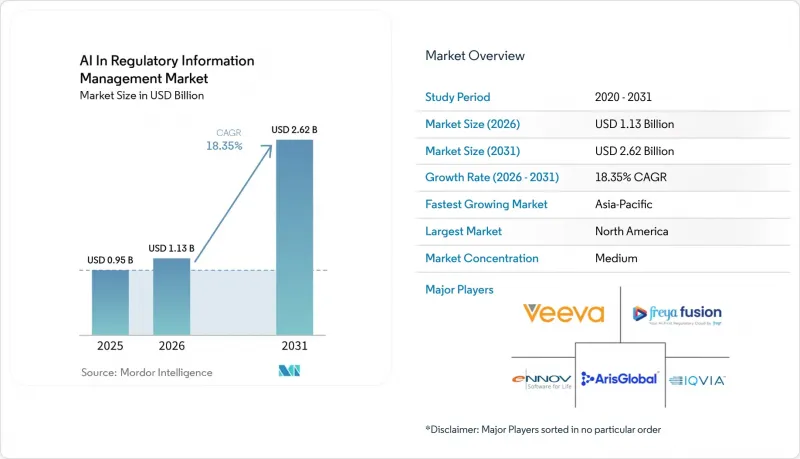

Mordor Intelligence에 의하면, AI 기반 규제 정보 관리 시장 AI 시장 규모는 2025년 9억 5,000만 달러, 2026년 11억 3,000만 달러에서 2031년까지 26억 2,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 18.35%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 플랫폼 및 서비스), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), AI 기능(자연어 처리, 문서 인텔리전스 등), 용도(규제 인텔리전스 등), 최종 사용자(제약 회사 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

전 세계 AI 기반 규제 정보 관리 시장 동향 및 인사이트

증가하는 신청 및 변경 신청 건수: 수작업 처리 능력을 초과한 규모의 문제

AI 기반 규제 정보 관리 시장은 현재 접수되는 건수가 증가함에 따라 수작업으로만 처리하기 어려운 업무량이 늘어나면서 성장하고 있습니다. FDA는 2025 회계연도에 143건의 NDA 및 BLA를 승인했으며, FAERS에는 2024년에 2,000만 건이 넘는 이상반응 보고가 접수되었습니다. 이는 규제 대상 컨텐츠의 양이 얼마나 급격히 증가했는지를 보여줍니다. 또한, 승인할 때마다 그에 따른 변경 신청, 갱신, 라벨 갱신 및 약속 이행 추적 작업이 발생하기 때문에 규제상의 부담은 최초 신청이라는 이정표를 훨씬 넘어 확장됩니다. 대형 제약사의 팀은 이미 매달 수백 건의 신청을 처리하고 있으며, 수작업만으로는 규모와 속도, 그리고 내부 일관성을 유지하기가 점점 더 어려워지고 있습니다. 이로 인해 규제 부서는 반복적인 문서 작성에서 벗어나 과학적 판단, 심사 전략 및 과제 해결에 주력해야 하는 상황에 놓여 있습니다. 그 결과, 워크로드의 요인은 구조적인 것이며 일시적인 자동화 주기에 국한되지 않기 때문에 AI 기반 RIM 도구에 대한 수요가 지속적으로 증가하고 있습니다.

신청 서류 처리 기간 단축에 대한 압박: 몇 주 단위로 측정되는 경쟁상의 시간적 여유

규제 정보 관리 시장에서 AI는 초안 작성, 심사, 공개에 소요되는 기간을 단축해야 한다는 압박이 커지고 있는 점에서도 혜택을 보고 있습니다. 심사 기간은 상업적으로 중요하기 때문에 기업들은 초안의 조기 완성, 부서 간 협력의 원활화, 그리고 후기 단계에서의 재작업 감소를 요구하고 있습니다. IBM은 자사의 Regulate.AI 플랫폼을 통해 규제 문서 작성자의 작업 시간을 50%에서 60%까지 단축했다고 밝혔으며, Yseop과 Indegene은 모두 메디컬 라이팅 및 신청 서류 작성의 효율화를 목표로 한 자동화 로드맵을 추진하고 있습니다. 제작 속도의 향상은 품질 향상으로도 이어집니다. 팀이 과학적 논리에 대한 검토에 더 많은 시간을 할애함으로써, 모듈 간의 불일치를 수정하는 데 소요되는 시간을 줄일 수 있기 때문입니다. 이 점은 중요합니다. 왜냐하면 섹션 간의 불일치는 종종 질문이나 정보 요청, 그리고 피할 수 있는 검토 과정상의 마찰을 야기하기 때문입니다. 따라서 검증된 워크플로우 내에서 작성, 버전 관리, 재사용, 공개를 통합하는 벤더는 독립형 문서 작성 도구보다 더 큰 주목을 받고 있습니다.

GxP 검증과 AI 거버넌스의 부담: 규정 준수 아키텍처의 불일치

규제 정보 관리 시장에서 AI는 여전히 거버넌스상의 부담에 직면해 있습니다. 그 이유는 많은 검증 모델이 확률론적 AI의 출력이 아니라, 결정론적 소프트웨어를 위해 구축되어 있기 때문입니다. FDA가 2025년 1월에 발표한 지침 초안에서는 의약품 및 생물학적 제제의 규제상 의사결정을 지원하기 위해 사용되는 AI에 대한 7단계 신뢰성 프레임워크가 도입되었으며, 증거, 시험 및 문서화에 대한 기대치가 높아지고 있습니다. 의약품 수명 주기에 있어 AI에 관한 EMA의 고찰 문서 역시, AI 활용에는 위험 기반 관리, 인적 감독, 추적성 및 문서화된 수명 주기 접근 방식이 필요함을 명확히 하고 있습니다. 이러한 요건들 때문에 품질이 매우 중요한 워크플로우에서의 도입이 지연되고 있습니다. 왜냐하면 기업은 시스템 그 자체와, 규제 대상인 의사결정 과정에서 그 시스템이 산출하는 결과의 역할, 이 두 가지를 모두 검증해야 하기 때문입니다. 이로 인해 많은 이용 사례에서 거버넌스 업무가 두 배로 늘어나게 되며, 확립된 컴플라이언스 프로세스가 없는 신규 진출기업에게는 진입 장벽이 높아집니다. 이러한 부담이 AI 도입을 가로막는 것은 아니지만, 잠금 처리된 모델, 감사 추적 기록, 검사 대응이 완료된 증거 패키지를 제공할 수 있는 공급업체에게 유리한 조건을 만들어 줍니다.

부문별 분석

2025년 기준으로, 규제 정보 관리(RIM) 시장에서 AI 점유율 중 소프트웨어 플랫폼이 45.16%를 차지하는 반면, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 20.88%로 확대될 것으로 예측됩니다. 플랫폼에 대한 수요는 이미 클라우드 기반 RIM 제품군을 통해 제출, 등록 및 인텔리전스 워크플로우를 통합하고 있는 주요 바이오의약품 기업들 사이에서 가장 견조했습니다. Veeva사에 따르면, 2025년에는 세계 상위 20대 바이오의약품 기업 중 19곳을 포함한 450개 이상의 기업이 자사의 RIM 플랫폼을 이용할 것으로 예상되며, 이는 통합형 엔터프라이즈 플랫폼이 이미 선도 기업들 사이에서 깊이 자리 잡고 있음을 보여줍니다. 이러한 도입의 확산은 소프트웨어 공급업체에 견고한 도입 기반을 마련해 주지만, 한편으로는 디지털화 주기의 초기 단계에 비해 주요 고객들이 신규 라이선스로의 전환에 예전만큼 적극적인 태도를 보이지 않는다는 것을 의미하기도 합니다. 그 결과, 규제 정보 관리(RIM) 시장의 AI 분야에서는 소프트웨어 계층이 여전히 전략적 중심에 위치하고 있지만, 그 성장은 현재 단순한 사용자 수 증가보다는 기능의 심화에 크게 의존하는 양상을 보이고 있습니다.

많은 기업이 이러한 플랫폼을 기업 차원에서 운영하기 위해 여전히 외부 지원이 필요하기 때문에 서비스 분야의 성장이 가속화되고 있습니다. GxP 준수 구현, 전환 설계, 검증, 분류 체계 정리 및 운영 모델 재설계에는 많은 규제 부서가 사내에 보유하고 있지 않은 전문 역량이 요구됩니다. 중규모 바이오의약품 기업이나 신생 스폰서 기업도 사내 팀 규모가 작은 경우, 출판, 신청 서류 작성 및 규제 정보 수집 업무에 있어 서비스 파트너에 의존하고 있습니다. 이로 인해, 특히 초기 플랫폼 선정이 이미 완료된 이후에는 소프트웨어의 소유 자체보다 가치 실현이 지출의 우선순위로서 더 중요해집니다. AI 기반 규제 정보 관리 업계에서는 기업 수요가 플랫폼 확보에서 플랫폼 활용 및 지속적 이용으로 전환되고 있기 때문에 서비스가 여전히 가장 확실한 성장 동력으로 자리 잡고 있습니다.

2025년 도입 방식별 시장 규모에서 클라우드 기반 도입은 규제 정보 관리 AI 시장의 38.17%를 차지했으나, On-Premise 도입은 2031년까지 연평균 성장률(CAGR) 19.12%를 나타낼 것으로 예측됩니다. 클라우드가 여전히 가장 널리 채택되는 형태인 이유는 제출 관리, 인텔리전스, 협업 업무 전반에 걸쳐 통일된 워크플로우, 손쉬운 업데이트, 그리고 보다 강력한 재사용을 가능하게 하기 때문입니다. EMA의 Scientific Explorer 데이터 보호 관련 공지(2026년 3월)에는 처리가 EU 지역의 Azure 서버 내에서 이루어지며, EMA의 데이터는 AI 모델 재훈련을 위해 저장되거나 사용되지 않는다는 점이 명시되어 있습니다. 이는 규제 대상 사용자가 현재 기대하고 있는 문서화된 클라우드 관리 조치의 유형을 반영한 것입니다. 이러한 운영 모델은 지역 고유의 처리 관리 조치를 AI 기반 규제 환경에 통합할 수 있음을 보여주고 있으며, 클라우드 도입을 촉진하고 있습니다. 따라서 규제 정보 관리 시장의 AI 분야에서 클라우드의 우위는 여전히 확고하며, 특히 사업 부문이나 국가를 초월한 워크플로우 공유를 필요로 하는 다국적 기업의 경우 더욱 그러합니다.

On-Premise 배포의 성장이 가속화되고 있다는 사실은 언뜻 보기에는 직관과 상반되는 것처럼 보이지만, 이는 일부 관할권에서 데이터 소재지, 주권 및 국경을 넘는 전송과 관련된 우려와 일치합니다. 중국, 인도, 중동 일부 지역 및 기타 민감한 시장에서 신청 절차를 진행하는 기업들은 신청과 관련된 제품 정보나 보충 자료에 대해 현지에서 보다 엄격한 관리가 필요한 경우가 많습니다. 따라서 하이브리드 아키텍처는 중앙에서 워크플로우를 조정할 수 있게 하면서도, 일부 규제 대상 데이터 저장소를 현지 관리 하에 둘 수 있기 때문에 현실적인 타협점으로 자리 잡고 있습니다. 이로 인해 도입 모드는 단순한 IT상의 선호 문제가 아니라, 규제상 및 설계상의 선택이 됩니다. 이는 상충되는 각국의 요건을 충족해야 하는 세계 기업들에게 특히 해당됩니다. 이러한 경향은 AI 기반 규제 정보 관리 시장이 단일 표준으로 급속히 수렴하기보다는 여러 도입 모델을 계속해서 지원하고 있는 이유를 설명하는 데에도 도움이 됩니다.

지역별 분석

2025년, 북미는 AI 기반 규제 정보 관리 시장 점유율에서 39.18%를 차지했습니다. 이 지역이 1위를 차지한 이유는 FDA의 성숙한 eCTD 생태계, 엄격한 심사 일정, 그리고 세계에서 가장 밀집해 있는 대형 제약 및 바이오기술 기업의 연구개발(R&D) 거점이 결합된 결과입니다. 또한, 2025년 1월 FDA가 발표한 의약품 및 생물학적 제제 승인 신청 시 AI의 신뢰성에 관한 지침 초안은 시장에 보다 명확한 규제 체계를 제공함으로써, 공급업체와 신청사의 보다 체계적인 투자를 촉진했습니다. 또한 북미에는 Veeva, IQVIA, Clarivate, Indegene 및 다수의 AI 네이티브 스타트업을 포함한 탄탄한 벤더 기반이 구축되어 있어, 이를 통해 제품의 피드백 루프가 단축되고 기능 개발이 가속화되고 있습니다. 이러한 엄격한 규제, 기업의 구매력, 그리고 공급업체와의 근접성이 맞물려, 다른 지역들이 성장을 가속화하고 있는 상황에서도 북미는 AI 기반 규제 정보 관리 시장에서 중심적인 위치를 유지하고 있습니다.

유럽은 AI 기반 규제 정보 관리 시장에서 가장 규제 주도적인 지역 블록 중 하나입니다. EMA는 2024년에 클라우드 전환을 완료하고, 2026년 초에 NDSG 2026-2028년 업무 계획을 채택했으며, 2026년 3월에는 AI가 탑재된 Scientific Explorer 도구를 각국의 규제 당국에 공개했습니다. 이는 AI 도입에 대한 기관의 적극적인 참여를 보여줍니다. 또한, 이 지역에서는 구조화된 데이터 관련 활동이 집중되고 있습니다. 이는 판매 승인 보유자가 보다 광범위한 디지털 규제 업무를 지원하기 위해 제품 데이터의 품질과 거버넌스를 개선해야 하기 때문입니다. 독일, 프랑스, 영국은 대형 제약 기업의 연구개발 활동과 규제 시스템에 관한 우수한 엔지니어링 및 서비스 인력을 모두 갖추고 있어 도입을 주도하고 있습니다. 이탈리아와 스페인은 제조, 의약품 안전성 모니터링, 수명 주기 관리 의무로 인해 디지털 규제 관리의 필요성이 지속적으로 확대되고 있어, 2차적인 성장 잠재력을 지니고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 19.36%로 확대될 것으로 예상되며, 지역별 AI 기반 규제 정보 관리 시장 규모 측면에서 가장 빠른 성장이 기대되는 지역이 될 것입니다. PMDA는 2025년 10월에 AI 활용 행동 계획을 발표하고, 2026년 4월부터 업무에 생성형 AI 도입을 시작하는 한편, 같은 달부터 신약 신청 시 eCTD 4.0 제출을 의무화했습니다. 이는 일본에서 근대화의 과정이 일제히 진행되고 있음을 보여줍니다. 중국의 2026년 이행 지침 및 국가의약품감독관리국(NMPA) 정보센터가 추진하는 의약품 규제에 대한 대규모 언어 모델 관련 노력은 제도적 AI 도입 준비가 정책적 선언 단계를 넘어 운영 시스템으로 전환되고 있음을 보여줍니다. 한국과 호주는 규모는 작지만 확고한 시장으로 남아 있는 반면, 남미, 중동 및 아프리카는 여전히 초기 단계 시장이며, 일반적으로 다국적 기업의 등록 포트폴리오에 대한 서비스 중심의 지원을 통해 대응하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the aI in regulatory information management market size is projected to expand from USD 0.95 billion in 2025 and USD 1.13 billion in 2026 to USD 2.62 billion by 2031, registering a CAGR of 18.35% between 2026 to 2031.

This report is Segmented by Component (Software Platforms and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), AI Capability (Natural Language Processing and Document Intelligence, and More), Application (Regulatory Intelligence, and More), End User (Pharmaceutical Companies, and More), and Geography (North America, Europe, and More). Forecasts are in Value (USD).

Global AI In Regulatory Information Management Market Trends and Insights

Rising Submission and Variation Volumes: A Scale Problem Beyond Manual Capacity

The AI in regulatory information management market is being driven by a workload curve that manual teams cannot absorb at current filing volumes. The FDA approved 143 NDAs and BLAs in fiscal 2025, and FAERS received more than 20 million adverse event reports in 2024, which shows how sharply regulated content volumes have expanded. Each approval also creates follow-on variations, renewals, labeling updates, and commitment tracking work, so the regulatory burden extends well beyond the first submission milestone. Large pharmaceutical teams already manage hundreds of submissions each month, which makes scale, speed, and internal consistency more difficult to maintain with manual methods alone. This is pushing regulatory groups to shift effort away from repetitive document production and toward scientific judgment, review strategy, and issue resolution. The result is recurring demand for AI-enabled RIM tools because the workload driver is structural and not limited to one temporary automation cycle.

Pressure to Shorten Dossier Cycle Times: Competitive Windows Measured in Weeks

The AI in regulatory information management market is also benefiting from stronger pressure to shorten drafting, review, and publishing timelines. Review windows are commercially important, so companies want earlier draft completion, cleaner cross-functional coordination, and fewer late-stage rework cycles. IBM said its Regulate.AI platform reduced regulatory writer time by 50% to 60%, while Yseop and Indegene both advanced automation roadmaps aimed at faster medical writing and dossier preparation. Faster authoring also improves quality because teams can spend more time reviewing scientific logic and less time repairing inconsistencies across modules. That matters because inconsistencies across sections often trigger questions, information requests, and avoidable review friction. Vendors that combine authoring, version control, reuse, and publishing inside a validated workflow are therefore gaining stronger attention than stand-alone drafting tools.

GxP Validation and AI Governance Burden: A Compliance Architecture Mismatch

The AI in regulatory information management market still faces a governance burden because many validation models were built for deterministic software and not for probabilistic AI outputs. The FDA's January 2025 draft guidance introduced a seven-step credibility framework for AI used to support regulatory decision-making for drugs and biological products, which increases evidence, testing, and documentation expectations. EMA's reflection paper on AI in the medicinal product lifecycle also makes clear that AI use needs risk-based controls, human oversight, traceability, and a documented lifecycle approach. These requirements slow implementation in quality-critical workflows because companies must validate both the system and the role of its outputs in regulated decisions. That doubles governance work for many use cases and raises the bar for new entrants that lack established compliance processes. The burden does not stop adoption, but it does favor vendors that can offer locked models, audit trails, and inspection-ready evidence packages.

Other drivers and restraints analyzed in the detailed report include:

- eCTD 4.0 and IDMP Structured-data Readiness: Infrastructure for the AI-Native Submission Era

- Continuous Regulatory Intelligence Automation: From Reactive Monitoring to Proactive Risk Management

- Fragmented Global Data Standards: An Obstacle Embedded in Foundational Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software Platforms held 45.16% of the AI in regulatory information management market share in 2025, while Services is projected to expand at 20.88% CAGR through 2031. Platform demand remained strongest among large biopharma companies that had already centralized submission, registration, and intelligence workflows on cloud RIM suites. Veeva said more than 450 companies, including 19 of the top 20 global biopharma firms, operated on its RIM platform in 2025, which shows how deeply unified enterprise platforms are already embedded in the top tier. That depth of adoption gives software vendors a strong installed base, but it also means the largest accounts are less open to net-new license displacement than they were earlier in the digitization cycle. As a result, the software layer remains strategically central in the AI in regulatory information management market, but its growth now depends more on added capability depth than on pure seat expansion.

Services are growing faster because many companies still need outside support to make those platforms work at enterprise scale. GxP-ready implementation, migration design, validation, taxonomy cleanup, and operating model redesign all require skills that many regulatory teams do not hold internally. Mid-sized biopharma companies and emerging sponsors also rely on service partners for publishing, dossier preparation, and regulatory intelligence operations when internal teams are lean. This makes value realization a bigger spending priority than software ownership alone, especially after the initial platform decision has already been made. In the AI in regulatory information management industry, this keeps services as the clearest growth outlet because enterprise demand is shifting from platform acquisition toward platform activation and sustained usage.

Cloud-based deployment accounted for 38.17% of the AI in regulatory information management market size by deployment in 2025, while on-premises deployment is projected to grow at 19.12% CAGR through 2031. Cloud remained the largest model because it supports unified workflows, easier updates, and stronger reuse across submission management, intelligence, and collaboration tasks. EMA's Scientific Explorer data protection notice stated in March 2026 that processing takes place within EU-region Azure servers and that EMA data is not stored or used to retrain AI models, which reflects the type of documented cloud controls that regulated users now expect. That kind of operating model supports cloud adoption because it shows that region-specific processing controls can be built into AI-enabled regulatory environments. The cloud lead in the AI in regulatory information management market therefore remains intact, especially for multinational organizations that want shared workflows across business units and countries.

The faster growth of on-premises deployment looks counterintuitive at first, but it aligns with data residency, sovereignty, and cross-border transfer concerns in several jurisdictions. Companies filing across China, India, parts of the Middle East, and other sensitive markets often need tighter local control over submission-related product information and supporting records. Hybrid architecture is therefore becoming the practical middle ground because it allows central workflow orchestration while keeping some regulated data stores under local control. This makes deployment mode a regulatory design choice and not just an IT preference, especially for global companies that must satisfy conflicting national requirements. The same pattern also helps explain why the AI in regulatory information management market continues to support multiple deployment models rather than converging quickly toward a single standard.

Geography Analysis

North America accounted for 39.18% of the AI in regulatory information management market share in 2025. The region led because it combined the FDA's mature eCTD ecosystem, tight review timelines, and the world's deepest concentration of large pharmaceutical and biotech R&D operations. The FDA's January 2025 draft guidance on AI credibility in drug and biological product submissions also gave the market a clearer regulatory framework, which supports more structured vendor and sponsor investment. North America also has a dense vendor base that includes Veeva, IQVIA, Clarivate, Indegene, and multiple AI-native startups, which shortens product feedback loops and supports faster feature development. This combination of regulatory formality, enterprise buying power, and vendor proximity keeps North America central to the AI in regulatory information management market even as other regions accelerate.

Europe is one of the most mandate-driven regional blocks in the AI in regulatory information management market. EMA completed its cloud migration in 2024, adopted the NDSG 2026 to 2028 workplan in early 2026, and launched the AI-enabled Scientific Explorer tool to national competent authorities in March 2026, which shows active institutional participation in AI adoption. The region also concentrates structured-data work because marketing authorization holders must improve product data quality and governance to support broader digital regulatory operations. Germany, France, and the United Kingdom lead adoption because they combine major pharma R&D activity with strong engineering and service talent around regulatory systems. Italy and Spain add secondary growth potential as manufacturing, pharmacovigilance, and lifecycle management obligations continue to widen the need for digital regulatory control.

Asia-Pacific is projected to expand at 19.36% CAGR through 2031, making it the fastest-growing regional outlook within the AI in regulatory information management market size by geography. PMDA published its AI utilization action plan in October 2025, began using generative AI in operations from April 2026, and made eCTD 4.0 mandatory for new drug applications from the same month, which signals synchronized modernization in Japan. China's 2026 implementation opinions and the NMPA Information Centre's work on large language models in drug regulation show that institutional AI readiness is moving beyond policy language into operational systems. South Korea and Australia remain smaller but established markets, while South America and the Middle East and Africa are still earlier-stage markets that are usually served through services-led support for multinational registration portfolios.

- AmpleLogic

- Aris Global

- Celegence

- Clarivate

- DnXT Solutions

- Ennov

- Essenvia

- EXTEDO

- FREYR / Freya Fusion

- Generis

- Indegene

- IQVIA

- LORENZ Life Sciences

- MasterControl

- Navitas Life Sciences

- Parexel International

- RegDesk

- Rimsys

- Veeva Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Submission and Variation Volumes

- 4.2.2 Pressure to Shorten Dossier Cycle Times

- 4.2.3 Cloud-Native RIM Consolidation Programs

- 4.2.4 Continuous Regulatory Intelligence Automation

- 4.2.5 eCTD 4.0 and IDMP Structured-Data Readiness

- 4.2.6 Health-Authority Query Mining and Response Reuse

- 4.3 Market Restraints

- 4.3.1 GxP Validation and AI Governance Burden

- 4.3.2 Fragmented Global Data Standards

- 4.3.3 Explainability During Inspections and HA Challenge

- 4.3.4 Weak Metadata Governance in Legacy RIM Estates

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By AI Capability

- 5.3.1 Natural language processing and document intelligence

- 5.3.2 Generative AI authoring and summarization

- 5.3.3 Regulatory knowledge graph and semantic search

- 5.3.4 Predictive analytics and risk scoring

- 5.3.5 Workflow orchestration and agentic automation

- 5.4 By Application

- 5.4.1 Regulatory intelligence

- 5.4.2 Dossier authoring and content assembly

- 5.4.3 Regulatory submissions and publishing

- 5.4.4 Product registration and approvals

- 5.4.5 Labeling and artwork change management

- 5.4.6 Health authority interactions and commitments management

- 5.4.7 Data migration and master data stewardship

- 5.4.8 Pharmacovigilance and safety reporting

- 5.5 By End User

- 5.5.1 Pharmaceutical companies

- 5.5.2 Biotechnology companies

- 5.5.3 Medical device and diagnostics companies

- 5.5.4 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AmpleLogic

- 6.3.2 ArisGlobal

- 6.3.3 Celegence

- 6.3.4 Clarivate

- 6.3.5 DnXT Solutions

- 6.3.6 Ennov

- 6.3.7 Essenvia

- 6.3.8 EXTEDO

- 6.3.9 FREYR / Freya Fusion

- 6.3.10 Generis

- 6.3.11 Indegene

- 6.3.12 IQVIA

- 6.3.13 LORENZ Life Sciences

- 6.3.14 MasterControl

- 6.3.15 Navitas Life Sciences

- 6.3.16 Parexel

- 6.3.17 RegDesk

- 6.3.18 Rimsys

- 6.3.19 Veeva Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment